P2-7. Determining income from continuing operations and gain

(loss) from discontinued operations

(AICPA adapted)

Requirements 1 and 2:

The amounts to be reported for income from continuing operations

after taxes excludes the losses from the discontinued operations.

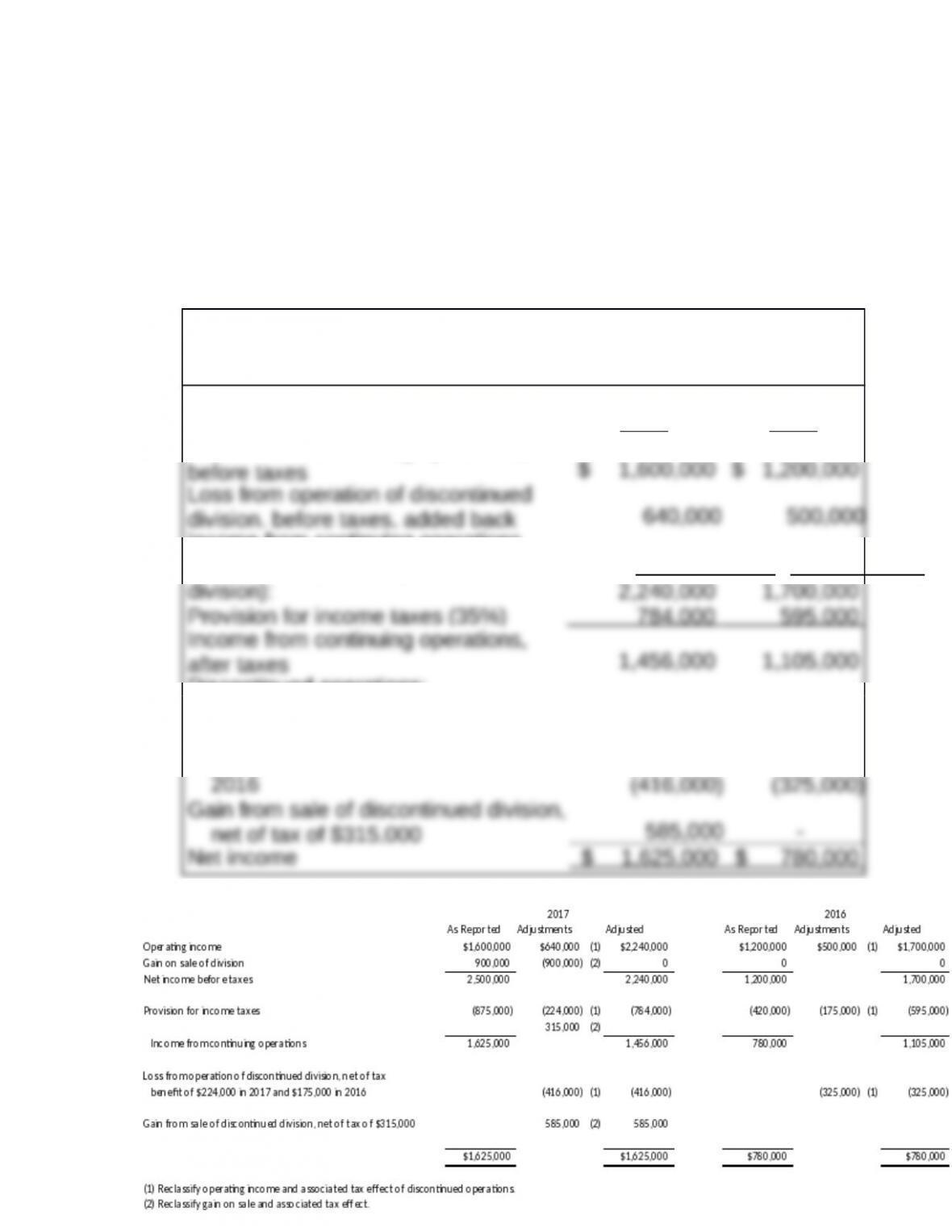

Helen Corporation

Partial Income Statement

For the Years Ended December 31

2017 2016

Income from continuing operations,

Income from continuing operations,

before taxes (excluding discontinued

Provision for income taxes (35%)

784 ,000

595 ,000

Income from continuing operations,

Discontinued operations:

Loss from operation of discontinued

division, net of tax benefits of

$224,000 in 2017 and $175,000 in

The following analysis derives the adjusted income statements shown

above:

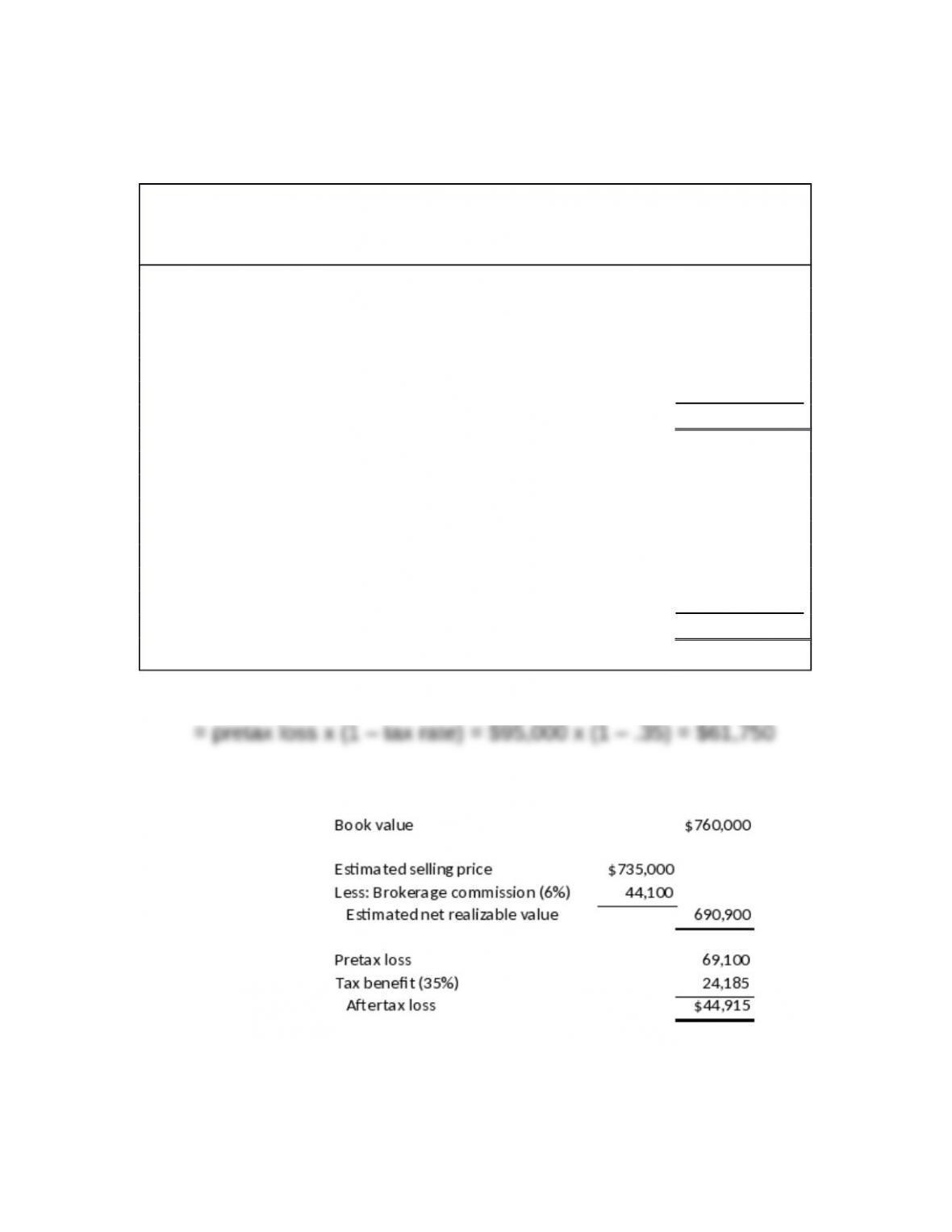

P2-8. Discontinued operations components held for sale

Silvertip Construction, Inc.

Partial Income Statement

For the Year Ended December 31, 2017

Income from continuing operations

$ 1,650,000

Discontinued operations:

Loss from operation of held for sale business

component, net of tax benefit of $33,250

*(61,750)

Impairment loss on held for sale component,

net of tax benefit of $24,185

**(44,915)

Net income

$ 1,543,335

Earnings per share:

Income from continuing operations

$ 1.65

Discontinued operations:

Loss from operation of held for sale business

component, net of tax

(0.06)

Impairment loss on held for sale component,

net of tax

(0.05)

Net income

$ 1.54

* Operating loss on component

** Impairment loss on component:

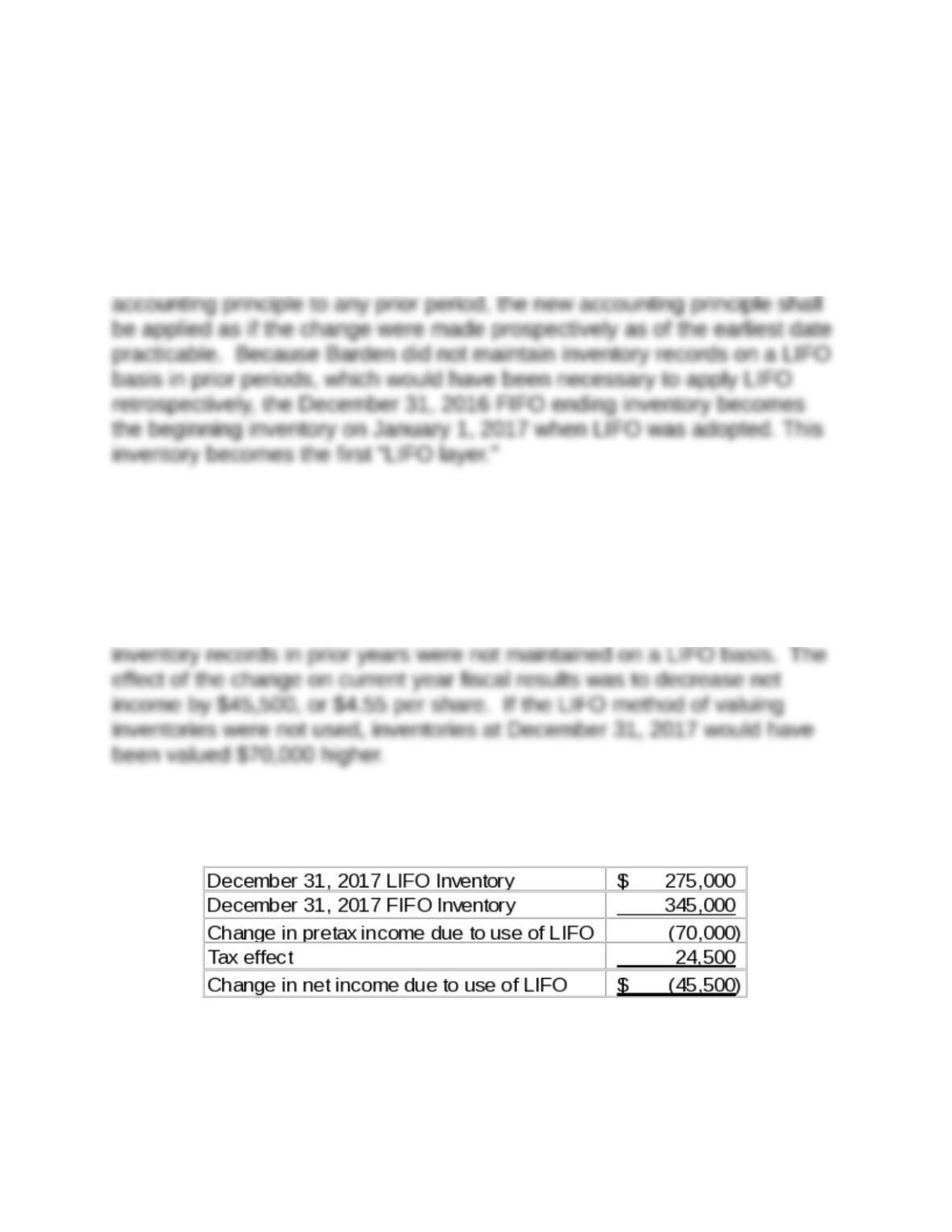

P2-9. Reporting a change in accounting principle

Requirement 1:

GAAP requires an entity to report a change in accounting principle through

retrospective application of the new accounting principle to all prior periods,

unless it is impracticable to do so, as is the case here. When it is

impracticable to determine the cumulative effect of applying a change in

Requirement 2:

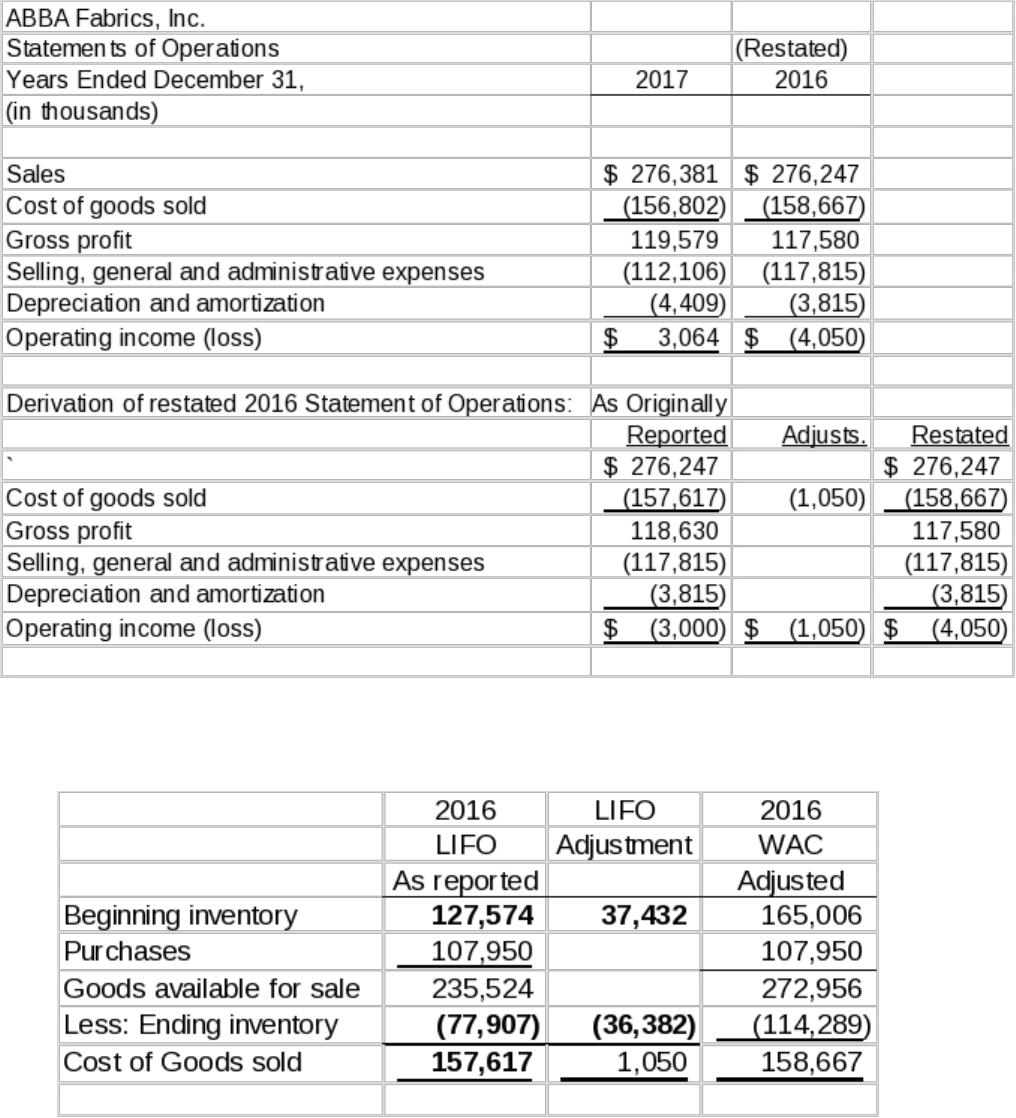

Effective January 1, 2017 the Company adopted the LIFO cost flow

assumption for valuing its inventories. The Company believes that the use

of the LIFO method better matches current costs with current revenues. It

was not practical to apply the change retrospectively to prior years because

Note to the instructor: The effect on the change in inventory method on

2017 income is determined as follows:

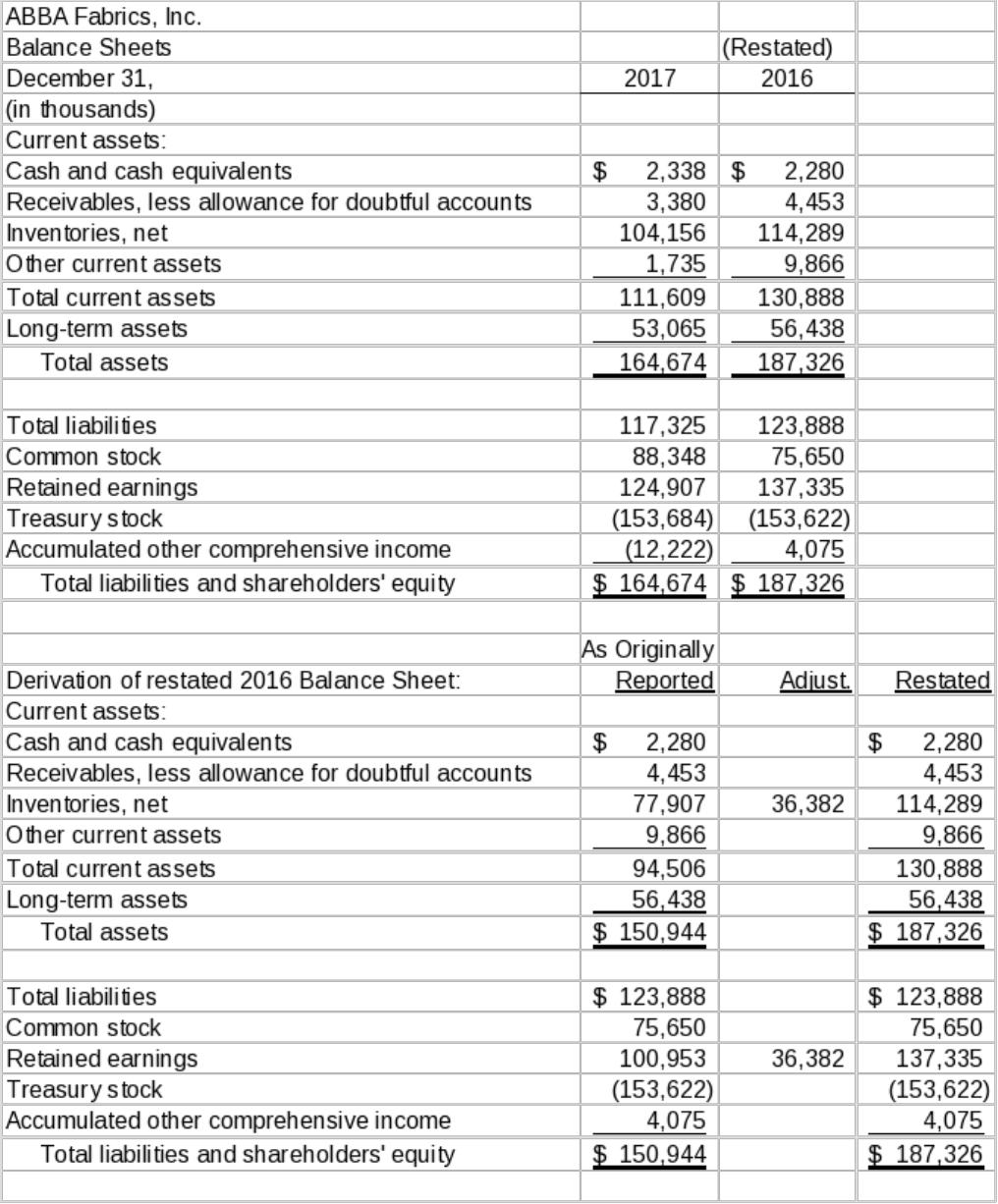

P2-10. Disclosures for change in accounting principle

Requirement 1:

Restated cost of goods sold is determined as follows. (Bold items are given

in the problem):

Requirement 2:

Retrospective Application of a Change in Accounting Principle

During the fourth quarter of 2017, the Company elected to change

its method of valuing inventory to the weighted average cost

(“WAC”) method, whereas in all prior years inventory was valued

Company has applied this change retrospectively to the

consolidated financial statements for the years 2016 and 2015 as

required by FASB ASC Section 250: Accounting Changes and Error

Consolidated Statements of Operations for the fiscal year ended

December 31, 2016

2016 2016

As

LIFO previously

(in thousands) As restated

Adjustmen

t reported

Consolidated Balance Sheet as of December 31, 2016

LIFO As previously

(in thousands) As restated Adjustment reported

Assets

Current assets:

Shareholders’ Equity

Shareholders’ equity:

P2-11. Change in accounting policy

Requirement 1:

Under the new accounting method, in a year there is a cumulative gain

or loss in Accumulated other comprehensive income (AOCI) at the end

of the year, the amount by which that gain or loss exceeds the

recognition threshold is recognized in net income immediately and

“recycled” out of AOCI. There would be no recognition of gain or loss in

the subsequent year unless an additional gain or loss put the cumulative

The net effect of the change is to increase the volatility of reported

earnings. When cumulative gains and losses are past the threshold, the

Requirement 2:

Gains and losses on the pension plan are not related to the fundamental

operating profitability of the firm. So, it is important for an analyst to

understand how those gains and losses affect reported income. Through

P2-12. Manipulation of receivables

Accounts receivable turnover = sales ÷ average accounts

receivable.

Days sales outstanding = 365 ÷ Accounts receivable turnover.

A growing days sales outstanding figure is often a telltale sign that a

company’s receivables are impaired due to channel stuffing or other

revenue recognition issues. This growth results from receivables

growing at a faster rate than sales; the growth rate disparity is

P2-13. Correction of errors and worksheet preparation

Error corrections worksheet

Effect on income Accounts to be adjusted

Description 2015 2016 2017 Dr. Cr.

$4,900 $4,900

Item 2.

Accrued wages—2015 (12,000) 12,000 Counterbalancing error

Item 3.

Depreciation 3,500 (7,000) (6,000) Retained earnings,

Accumulated

Depr.,