P14-5. Calculating PBO, ABO and pension expense (LO 14-1, LO 14-2, LO 14-3)

Requirement 1:

Calculation of PBO on January 1, 2017:

Annual pension benefits starting on 12/31/2031 and continuing for 10 years

thereafter (11 years total = 76 – 66).

PVOA of expected pension benefits as of 1/1/2031 (date of retirement):

Projected benefit obligation on 1/1/2017 (date plan adopted):

Accumulated benefit obligation on actual salary level attained as of the date of

computation (ignores future salary increase):

Benefits tied to actual salary as of 1/1/2017:

credit and salary level as of 1/1/2017 $12 ,500

PVOA of expected pension benefits as of 1/1/2031 (date of retirement):

Accumulated benefit obligation on 1/1/2017 (date of adoption):

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 14-1

Note: Projected benefit obligation > accumulated benefit obligation

Requirement 2:

Calculation of projected benefit obligation on 12/31/2017:

PVOA of expected pension benefits as of 1/1/2031

Projected benefit obligation on 12/31/2017:

Requirement 3:

Calculation of pension expense for 2017:

Service cost component

PV of single amount for 14 periods @ 10% x $1,624

= 0.26333 x $1,624 =

Amortization of prior service cost

$27,210/15 yrs. = + 1,814

Amortization of actuarial gains/losses

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 14-2

0

P14-6. Determining PBO and pension expense (LO14-1, LO14-2, LO14-3)

Requirement 1: Pension expense in 2017

With the entire amount of PBO funded on Jan. 1, 2017, the expected return on

Interest on PBO

10% x $27,210 + 2,721

$27,210/15 yrs. = + 1,814

Amortization of actuarial gain/losses

Requirement 2: Funded status at December 31, 2017

Calculation of PBO at December 31, 2017 after discount rate change:

Years of service credit earned as of 2015: 11 yrs. x $250 $2,750

PV of expected pension benefits as of 2031:

PVOA for 11 periods @ 9% x $17,750 = 6.80519 x $17,750 =

$120,792

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 14-3

Calculation of fair value of plan assets on December 31, 2017:

Initial amount funded on Jan.1, 2017 $27,210

Actual return on plan assets in 2017

Fair value of plan assets on Dec. 31, 2017 $30 ,903

Funded Status ($30,903 less $36,147) $5 ,244

Net actuarial loss at the end of 2017:

PBO at 12/31/2017 at 9% $36,147

Less: PBO at 12/31/2017 at 10% from P12-5 solution 30 ,359

Expected return ($27,210 x 0.12) 3 ,265

Deferred gain (544 )

Net actuarial loss at December 31, 2017 $5 ,244

Explanation for Change in Funded Status:

The funded status declined because of the actuarial loss on PBO. Though the

Requirement 3: Pension expense and funding for 2018

Pension expense for 2018:

Service cost

(PVOA for 11 periods @ 9% x $250

Interest on PBO at January1, 2018

9% x $36,147 3,253

Amortization of prior service costs:

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 14-4

Total pension expense for 2018 $2,648

Amount of pension expense funded in 2018

*Amortization of actuarial loss

Actuarial loss on 1/1/2018 $5,244

Amortization

Requirement 4: Calculation of funded status on December 31, 2018:

Projected benefit obligation on Dec. 31, 2017 $36,147

Service cost

Interest cost 3 ,253

Projected benefit obligation on Dec. 31, 2018 $39 ,955#

Fair value of plan assets on Dec. 31, 2017 $30,903

Actual return on plan assets in 2018

10% x $30,903 3,090

2018 funding on Dec. 31, 2018

Total pension assets on Dec. 31, 2018 $34 ,827

Net underfunded position on 12/31/2018$5,128

#Check on PBO:

Annual pension benefits starting on 12/31/2031 and continuing for 10 years

thereafter (11 years total).

PVOA of expected pension benefits as of 1/1/31 (date of retirement):

PVOA for 11 periods @ 9% x $18,000

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 14-5

P14-7. Identifying effect of funding and discount rate assumption on pension ex–

pense (LO14-2, LO14-3, LO14-5)

Requirement 1:

Total Vested PV of

End of Annual Cumulative Vested During Discount Total Vested

Year Salary Salary Pension the Year Period PV Factor Pension

1 2 3 4 5 6 7 8

2017 $50,000 $50,000 $12,500 $12,500 4 0.68301 $8,538

2021 – 260,000 65,000 – 0 1.00000 65,000

The above table shows the present value of the total vested pension benefits

over the period 2017–2021. At the end of each year, the total vested pension

for the discount period mentioned in column (6) using a discount rate of 10%.

Based on this information, the pension expense is calculated as follows:

Vested PV of Change

During Total Vested in the Service Interest

Year the Year PV Factor Pension PV Cost Cost

2017 $12,500 0.68301 $8,538 $8,538 $8,538 –

$65 ,000 $52 ,453 $12 ,547

Conceptually, the annual pension expense for an unfunded plan is the change

in the present value of the total vested pension benefit. The service cost is

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 14-6

service cost and the interest cost equals the change in the present value of the

total vested pension benefits.

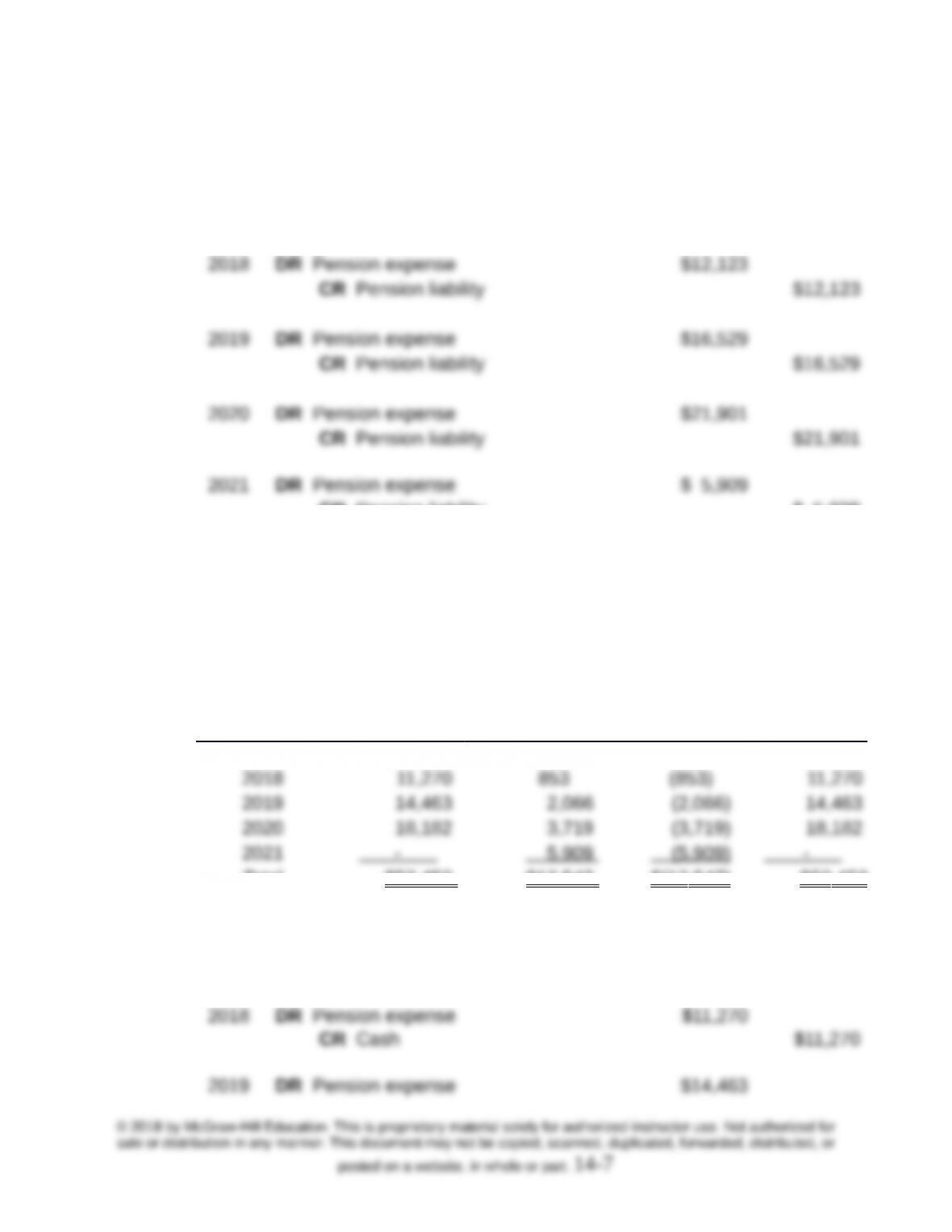

2017 DR Pension expense $ 8,538

CR Pension liability $ 8,538

CR Pension liability $ 5,909

DR Pension liability $65,000

CR Cash $65,000

Requirement 2:

In this case, the pension expense will exactly equal the service cost:

Service Interest Return on Pension

Year Cost Cost Plan Assets Expense

2017 $ 8,538 – – $ 8,538

Total $52 ,453 $12 ,547 $(12 ,547) $52 ,453

2017 DR Pension expense $ 8,538

CR Cash $ 8,538

2021 DR Pension expense –

CR Cash –

Requirement 3:

Under the unfunded scenario, the pension expense is the sum of the service

earn by investing the service cost in an investment that offers an annual rate of

return of 10%?

Annual Investment Future Income

Year Contributions Period FV Factor Value Earned

2017 $ 8,538 4 1.46410 $12,500 $ 3,962

2021 – 0 1.00000 – –

Total $52 ,453 $65 ,000 $12 ,547

Consequently, in the unfunded case, if the company had invested the service

cash saved from not funding the pension plan. This will be compensated by the

higher pension expense.

Pension expense in the fully funded case $52 ,453

Requirement 4:

Discount Rate = 5% Discount Rate = 10% Discount Rate = 15%

Service Interest Total Service Interest Total Service Interes

t

Total

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 14-8

Year Cost Cost Expense Cost Cost Expens

e

Cost Cost Expens

e

2021 – 3 ,095 3 ,095 – 5 ,909 5 ,909 – 8 ,478 8 ,478

6

The following observations emerge from this comparison:

(1) Over the life of a company, the total pension expense is the same

(2) However, the service cost is lower when the discount rate is higher,

(3) Since interest cost represents the time value of money, more of the interest

rates are lower.

P14-8. Determining effect of discount rate assumption on pension expense

and PBO (LO14-2, LO14-3, LO14-5)

Note to the instructor: In order to minimize the effects of rounding errors, the

on plan assets – 10%:

Requirement 1: Annual pension expense

Assumptions: Discount rate = 10% and Rate of return on plan assets =

10%

Total Vested PV of

End of Annual Cumulative Vested During Discoun

t

PV Total Vested

Year Salary Salary Pension the Year Period Factor Pension

1 2 3 4 5 6 7 8

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 14-9

2017 $50,000 $50,000 $12,500 $12,500 4 0.68301 $8,537.63

2021 – 260,000 65,000 – 0 1.00000 65,000.00

Note that the PV of total vested pension represents the projected benefit

obligation.

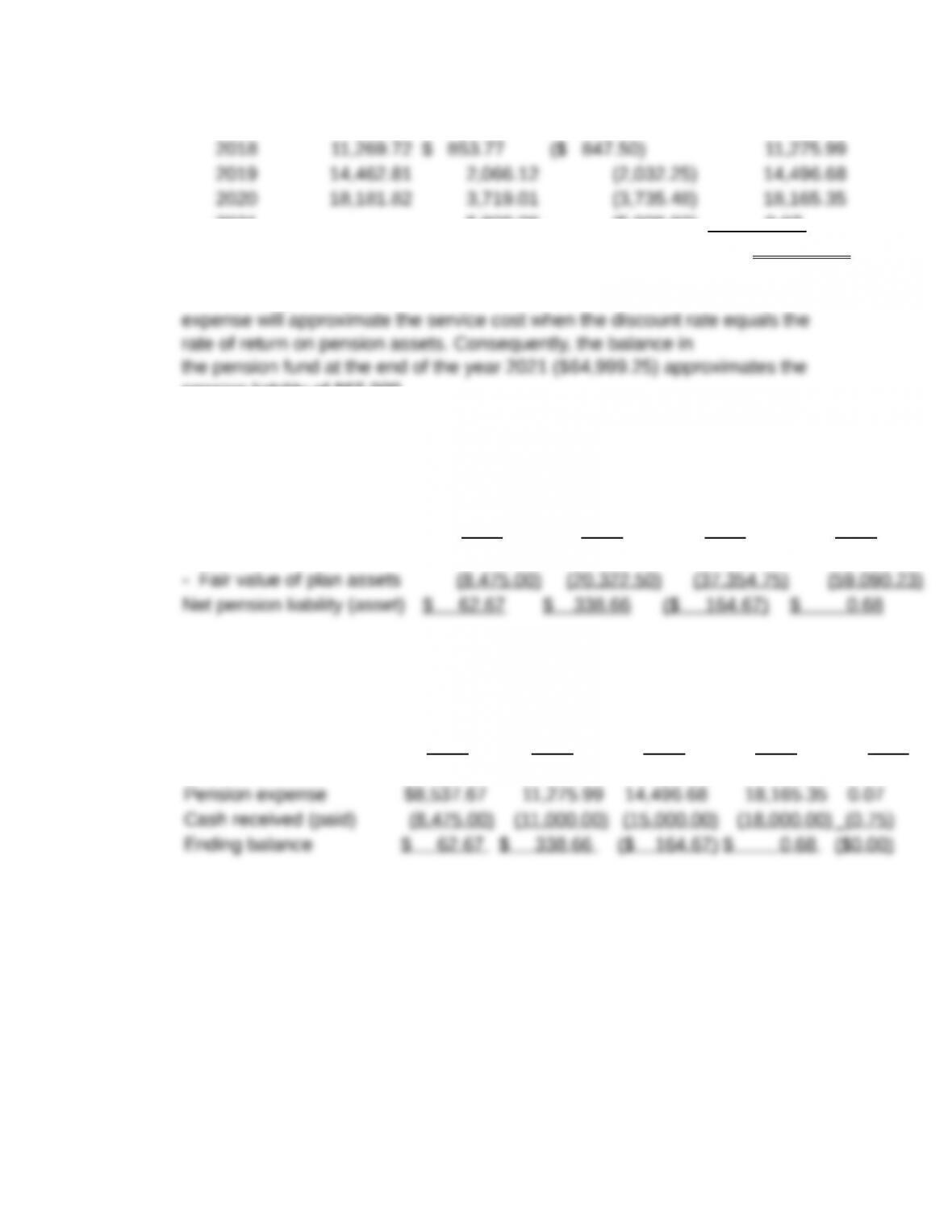

The following table summarizes the activities in the pension fund.

Pension Fund Investments and Earnings

2017 2018 2019 2020 2021 Future

Value

Contributions $8,475.00 $ 847.50 $ 932.25 $ 1,025.48 $ 1,128.02 $12,408.25

Income earned – $ 847.50 $ 2,032.25 $ 3,735.48 $ 5,909.02

The highlighted diagonal figures represent the inflow of cash from Magee Corp.

The figures to the right of these numbers represent the future return earned by

to which each year’s cash inflow will grow by investing at 10% through the end

of 2021. Except for rounding errors, note that the future value of each year’s

cash inflow corresponds to the pension vested during the same year shown in

the previous table.

The row titled “Year-end balance” provides the fair value of the plan assets at

Based on the above information, we now calculate the pension expense as

follows:

Service Interest Return on Pension

Year Cost Cost Plan Assets Expense

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 14-10

2017 $ 8,537.67 – – $ 8,537.67

2021 5,909.09 (5,909.02) 0.07

$52 ,475.76

Note: The figures for pension contributions were chosen such that the pension

pension liability of $65,000.

The funding status of the pension plan is provided below:

Requirement 2: Funded status under 10% discount rate

End of Year 2017 2018 2019 2020

Projected benefit obligation $8,537.67 $20,661.16 $37,190.08 $59,090.91

The balance in net pension liability (asset) can verified by preparing the

T-account:

Pension Liability

(Asset) at Year-End 2017 2018 2019 2020 2021

Beginning balance – $ 62.67 $ 338.66 ($ 164.67) $ 0.68

The tables are now reported under the other two scenarios regarding the

discount rates.

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 14-11