P16-4. Equity method and fair value option

Requirement 1:

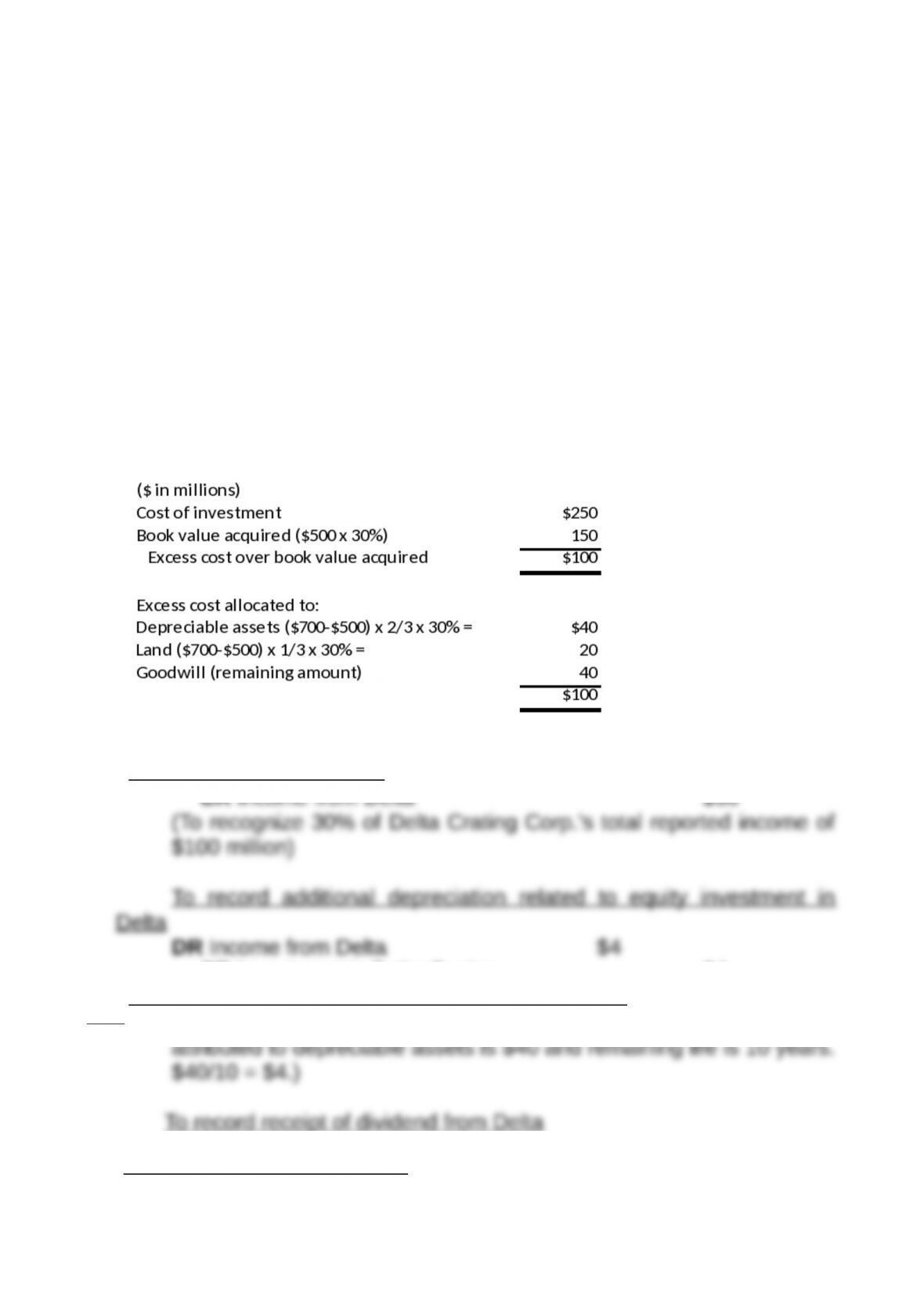

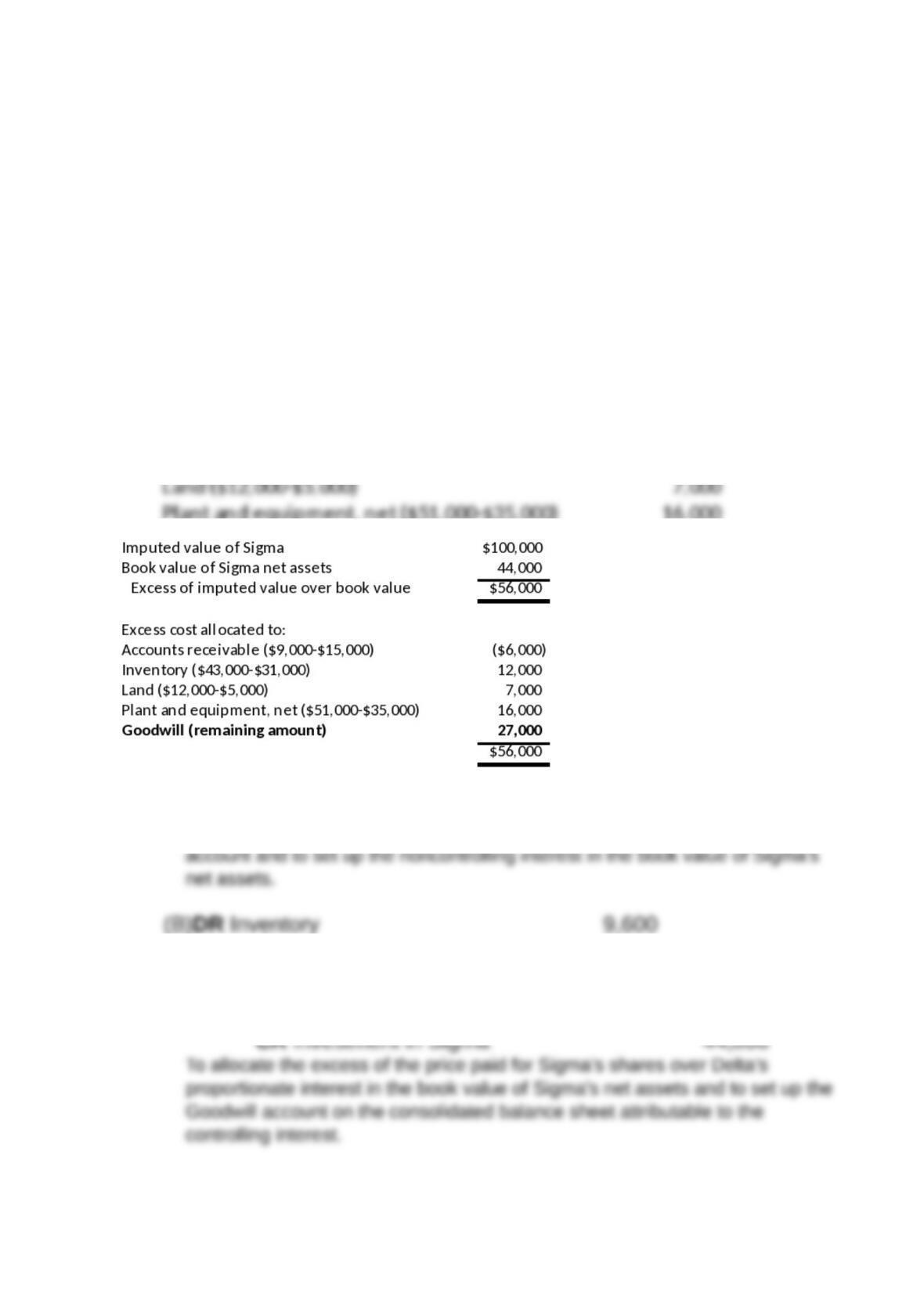

The determination of excess cost and its allocation is as follows:

2017 Journal entries:

January 1, 2017 – Initial acquisition

DR Investment in Delta Crating $250

$100 million)

To record additional depreciation related to equity investment in

Delta

DR Income from Delta $4

$40/10 = $4.)

To record receipt of dividend from Delta

DR Cash $9

16-1

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

CR Investment in Delta Crating $9

2018 Journal entries:

To record equity in Delta’s net income

$80 million)

To record additional depreciation related to equity investment in Delta

DR Income from Delta $4

To record receipt of dividend from Delta

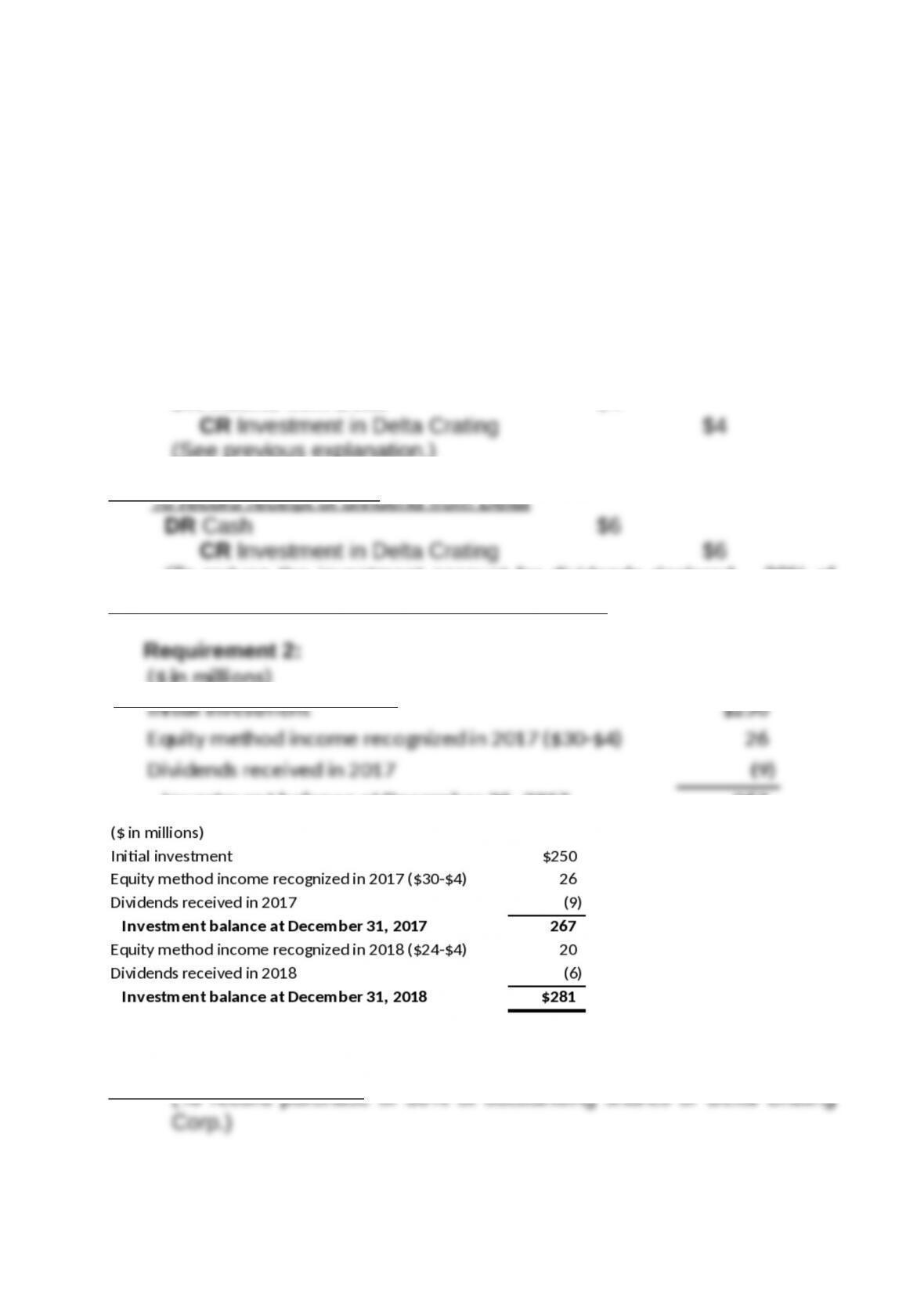

Requirement 2:

Requirement 3:

2017 Journal entries:

January 1, 2017 – Initial acquisition

Corp.)

16-2

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

To record receipt of dividend from Delta

DR Cash $9

To record 2017 fair value adjustment

DR Investment in Delta Crating $50

2018 Journal entries:

To record receipt of dividend from Delta

DR Cash $6

To record 2018 fair value adjustment

DR Investment in Delta Crating $60

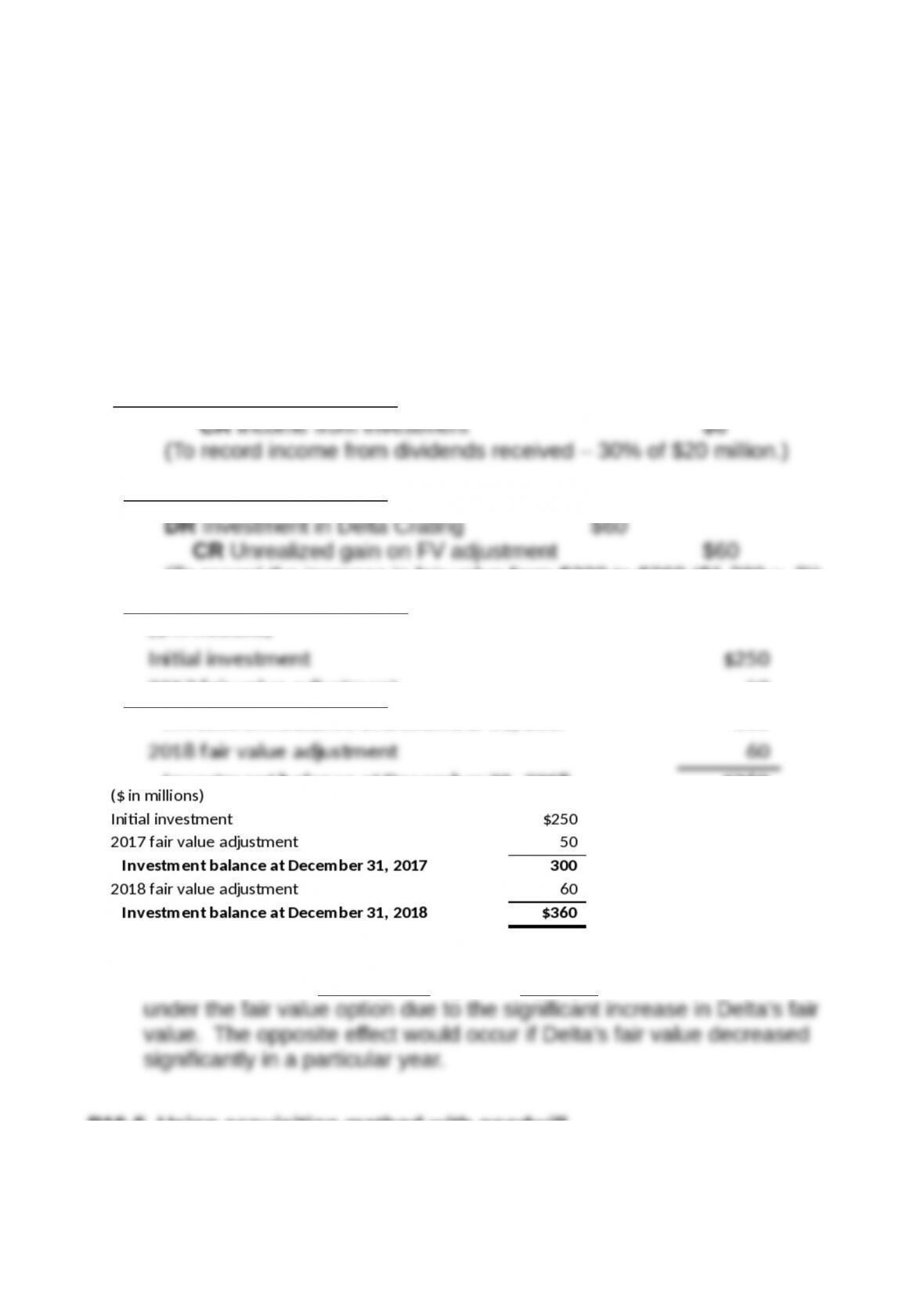

Requirement 4:

Equity Method FV Option

significantly in a particular year.

P16-5. Using acquisition method with goodwill

16-3

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

Requirement 1:

DR Investment in Sigma $80,000

CR Cash

$80,000

Requirement 2:

Requirement 3:

Adjustment and elimination entries:

CR Investment in Sigma (80%) 35,200

To eliminate Sigma’s equity accounts against Delta’s Investment in Sigma

account and to set up the noncontrolling interest in the book value of Sigma’s

net assets.

(B)DR Inventory 9,600

DR Land 5,600

Goodwill account on the consolidated balance sheet attributable to the

controlling interest.

16-4

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

(C)DR Inventory 2,400

DR Land 1,400

DR Plant and Equipment 3,200

the noncontrolling interest—under the acquisition method.

16-5

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

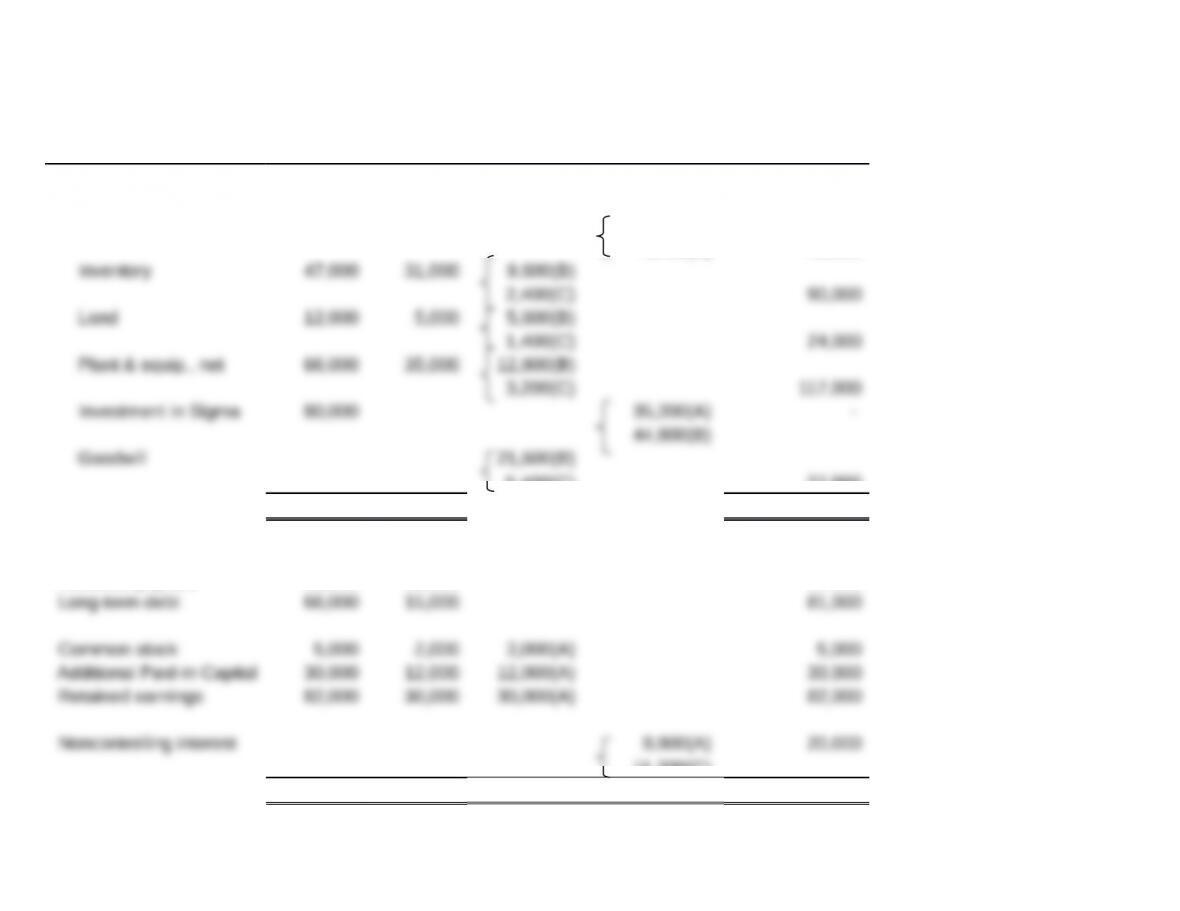

Requirement 4: Consolidated Balance Sheet:

Delta Sigma

Eliminations Consolidated

Dr Cr Balance Sheet

Assets

Cash $ 11,000 $ 8,000 $ 19,000

Accounts receivable 19,000 15,000 4,800(B)

1,200(C) 28,000

5,400(C) 27,000

Total $ 235,000 $ 94,000 $ 305,000

Liabilities & Equity

Accounts payable 52,000 35,000 87,000

11,200(C)

Total $ 235,000 $ 94,000 $106,000 $106,000 $ 305,000

16-6

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

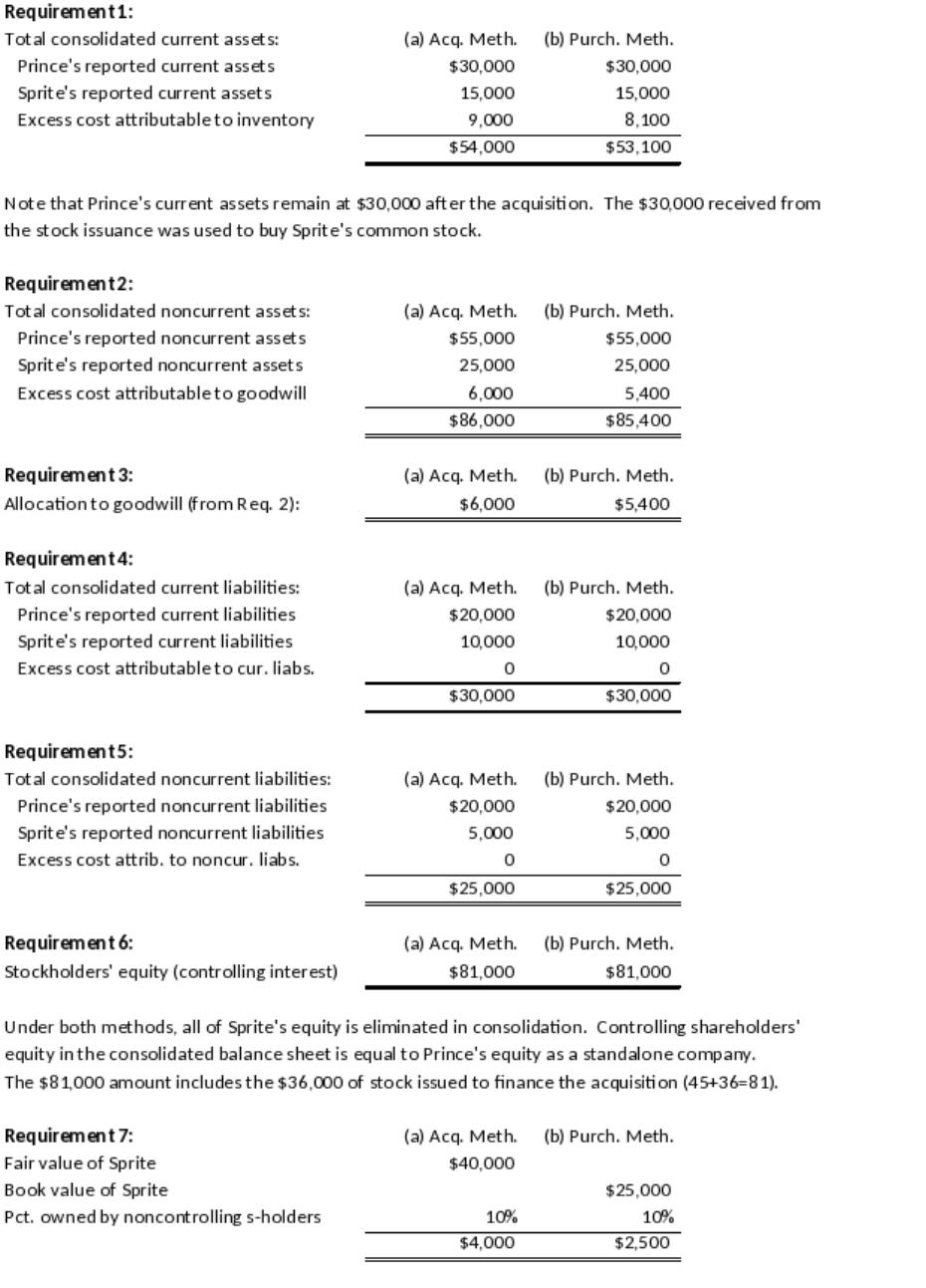

P16-6. Consolidating at acquisition: Acquisition vs. purchase method

90% Imputed 100%

Purchase price of Sprite’s stock $36,000

$40,000*

Goodwill 5,400 (40% x $13,500)

$13,500

*Sprite’s imputed total business fair value at acquisition date is

$40,000 ($36,000/0.9).

16-7

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

16-8

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

NOTE: Under the purchase method, noncontrolling interest of

P16-7. Elimination entries and consolidated balance sheet

Case 1:

Requirement 1:

$180,000

Requirement 2:

DR Common Stock & APIC, Salad $100,000

Requirement 3:

Assets:

Cash $420,000

Accts. Receiv. 70,000

Liab. & Equity:

Accounts Payable $120,000

Total $980 ,000

16-9

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

Note: All balance sheet amounts are equal to the sum of the

equity accounts are eliminated in consolidation.

Case 2:

Requirement 1:

DR Investment in Salad $210,000

Requirement 2:

DR Common Stock & APIC, Salad $100,000

DR Land $10,000

Requirement 3:

Assets:

Cash $390,000

A/R 70,000

Total $980 ,000

Liab. & Equity

Accounts Payable $120,000

Total $980 ,000

16-10

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

Note: All balance sheet amounts are equal to the sum of the

because Salad’s equity accounts are eliminated in consolidation.

16-11

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.