P9-4. Determining the effects of absorption and variable costing

(LO 12)

Requirement 1:

Absorption Cost: 2017

Ending inventory [55,000 @ $8]

Absorption Cost: 2018

Ending inventory [70,000 @ $9]

Absorption Cost: 2019

Ending inventory [45,000 @ $8.3478]

There are two factors that affect the gross profit margin when absorption

costing is used:

(1) The relationship between sales and production. When production

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 9-1

(2) Variations in production levels because fixed costs per unit (that

impact both cost of goods sold and inventory) go down as production

increases.

Considering these factors in regards to Mastrolia’s data we find that in

2017, production exceeded sales (as was the case in the previous year)

thus raising gross margin. In 2018, production again exceeded sales, but

overall production was lower than in 2017. So while some of the current

period’s fixed costs went to inventory, the 30,000 units of 2018 production

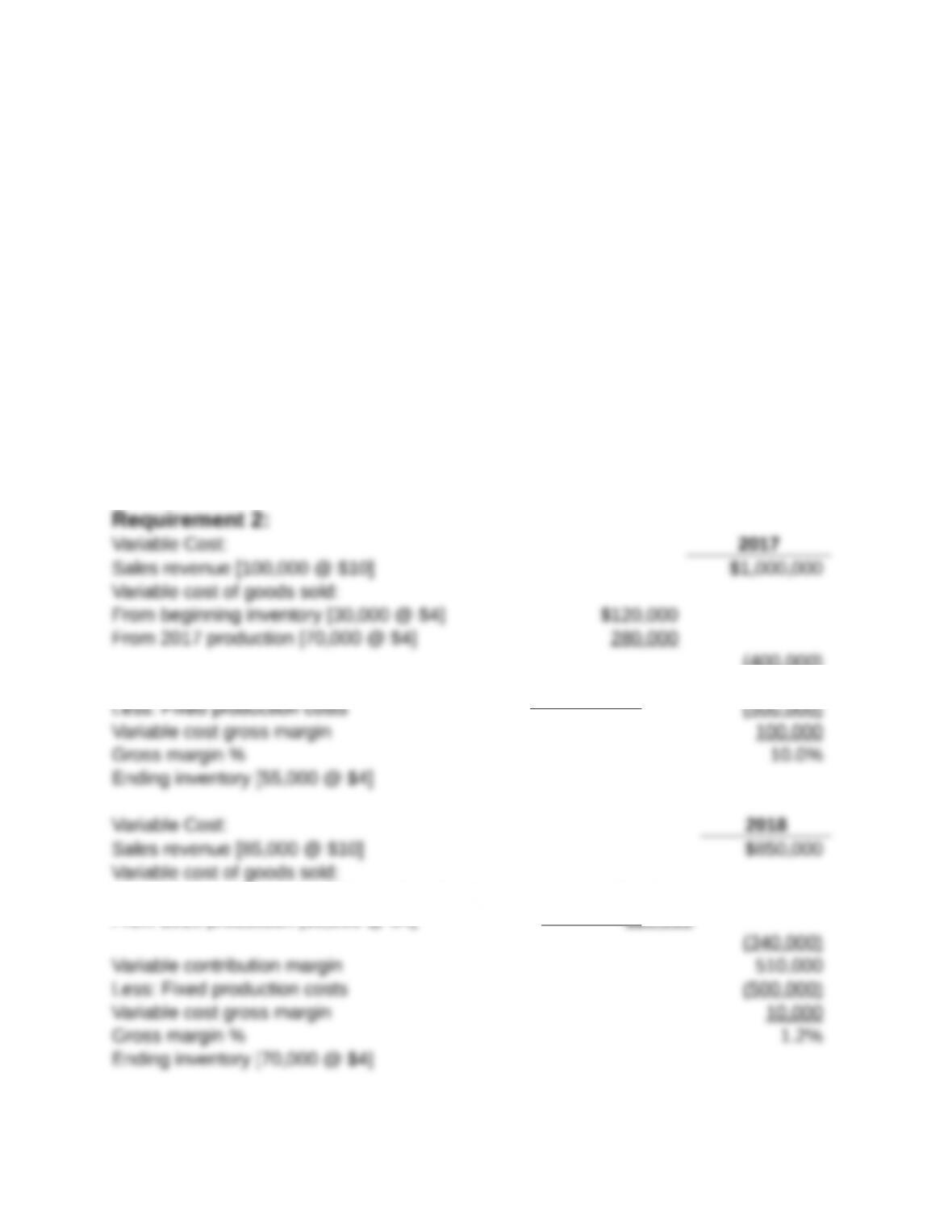

Requirement 2:

Variable Cost: 2017

Ending inventory [55,000 @ $4]

Variable Cost: 2018

Ending inventory [70,000 @ $4]

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 9-2

Variable Cost: 2019

Ending inventory [45,000 @ $4]

Sales volume is the only factor affecting variations in gross profit margin

when variable costing is used. Break even for Mastrolia stands at 83,333

Requirement 3:

As plant manager, I would prefer absorption costing assuming bonus

achievement/maximization is my goal. As explained in Requirement (2),

gross margin under variable costing depends entirely on sales volume. As

P9-5. Determining items to be included in inventory (LO 3)

Inventory Accounts payable Net sales

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 9-3

P9-6. Choosing a cost flow assumption (LO 4, 7, 9)

Responses to each of the issues raised follow.

d. If firms liquidate LIFO layers when inventory levels are falling,

then they may have to pay taxes on LIFO liquidations (i.e.,

cumulative holding gains from inflation). FIFO cannot solve the

e. This is not possible. LIFO ensures better matching, but FIFO

f. Not necessarily. If securities markets are “efficient,” then higher

income due to a different accounting method does not ensure a

income.

P9-7. Choosing a cost flow assumption (LO 4, 5, 7, 9)

Requirement 1:

Units in ending inventory = units purchased – units sold = 72,000 –

62,000 = 10,000.

Ending Inventory under Periodic FIFO

Units Cost/Unit Total

By subtracting the ending inventory amount of $150,000 from the

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 9-4

Requirement 2:

Ending Inventory under Periodic LIFO

Units Cost/Unit Total

By subtracting the ending inventory amount of $150,000 from the

goods available for sale, we compute cost of goods sold as follows:

Gross Margin = $984,000 – $678,000 = $306,000

The company has to disclose the ending LIFO reserve under the

LIFO method.

Since the company started doing business only during 2017, there is

no beginning LIFO reserve.

FIFO COGS = LIFO COGS + Beginning LIFO reserve – Ending

LIFO reserve

Requirement 3:

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 9-5

Current Output Current Input

Operating

Date Units Sold Price Price Margin

Requirement 4:

a) The LIFO inventory accounting method does a good job of

matching revenues and expenses during both inflationary and

b) The specific identification method matches the physical flow of

goods with revenue. However this is not the objective of the

matching principle. The objective is to match the revenue flow

with the cost flow. The specific identification method is

c) Given the inflationary situation faced by the company, the FIFO

inventory accounting method can be used to maximize current

d) Given the inflationary situation faced by the company, the LIFO

inventory accounting method can be used to minimize current

profits and, hence, minimize the present value of future income

e) This is not allowed. Under the LIFO conformity rule, if a company

uses LIFO for tax purposes, it must choose LIFO for financial

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 9-6

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 9-7

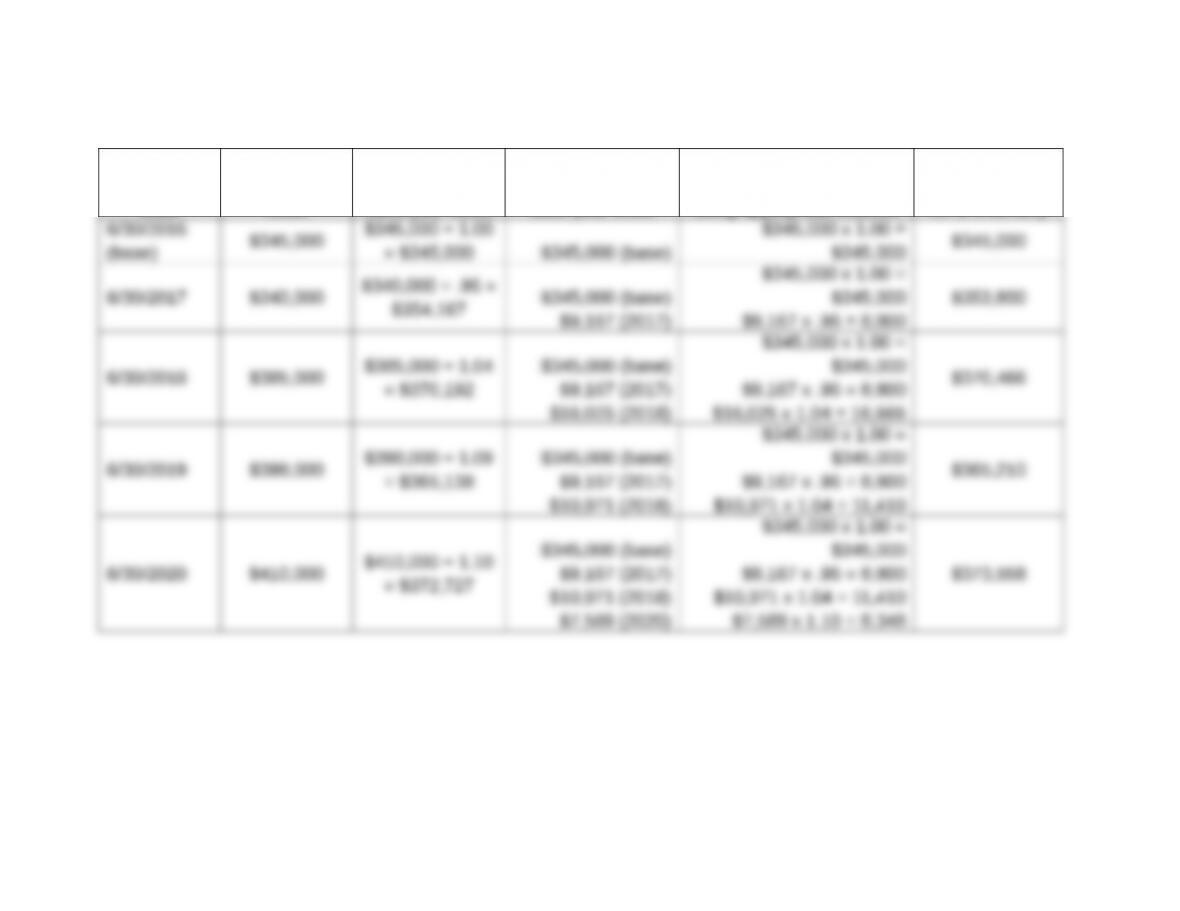

P 9-8. Computing dollar-value LIFO (LO 13)

Date

Inventory @

current year

costs

Inventory @

base year costs

Inventory layers @

base year costs

Inventory layers restated

using appropriate indexes

Dollar-value

LIFO inventory

= $372,727

$10,971 (2018)

$7,589 (2020)

$10,971 x 1.04 = 11,410

$7,589 x 1.10 = 8,348

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This

document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part. 9-8

P9-9. Correcting inventory errors (LO 14)

Effect on

Erro

r

12/31/2017

Ending

inventory

12/31/2018

Ending

inventory

2017 Cost

of goods

sold

2018 Cost

of goods

sold

12/31/2017

Accounts

payable

12/31/2018

Accounts

payable

P9-10. Analyzing gross margins and cash flow sustainability (LO 8)

Requirement 1:

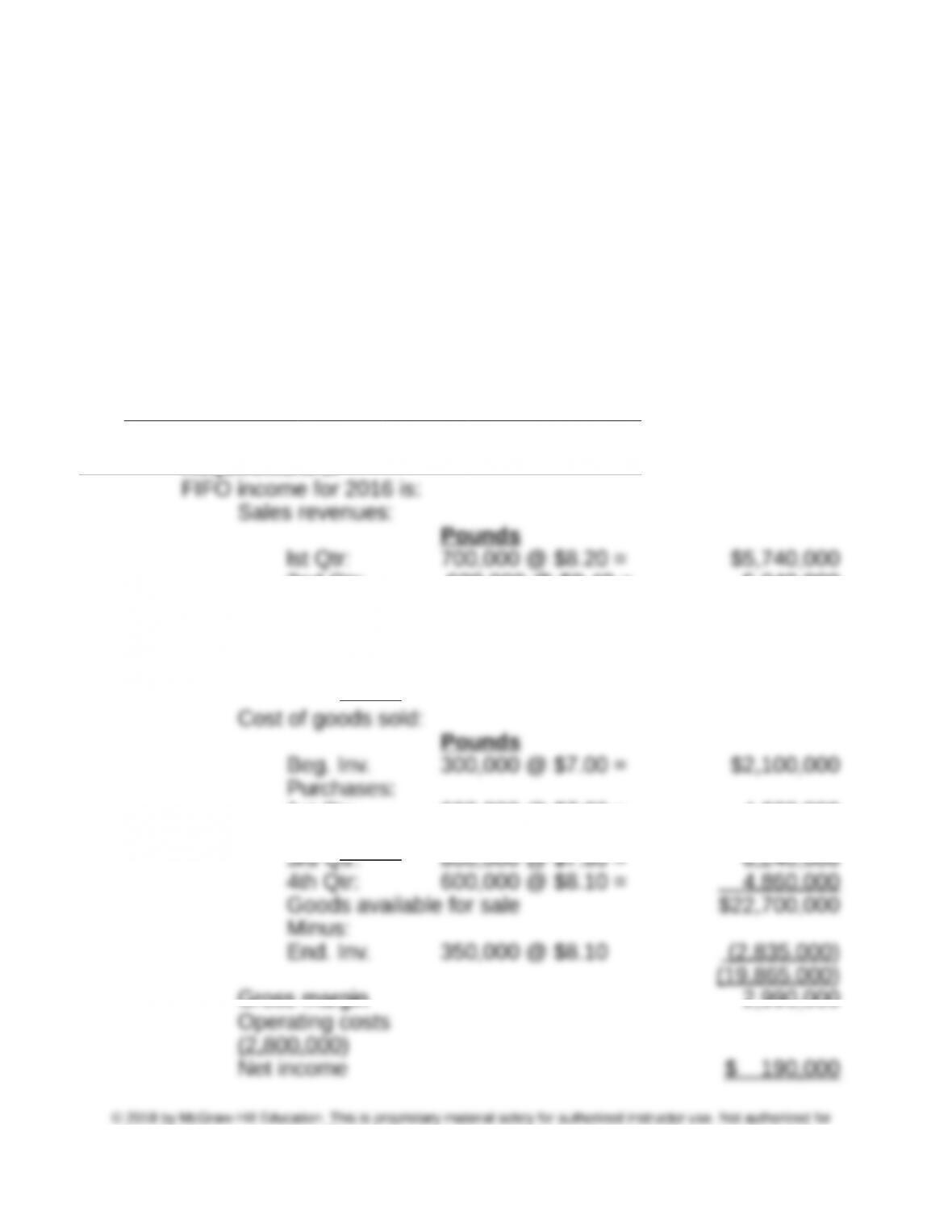

FIFO income for 2016 is:

Sales revenues:

Pounds

Cost of goods sold:

Pounds

Minus:

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 9-9

Requirement 2:

Parque Corporation did not earn a profit from its operating activities

in 2016. This becomes evident after computing the amount of

realized holding gains that are automatically included in the

$190,000 FIFO net income figure in part 1. The computation is:

Date of Yelpin Amount of Pounds Realizable

Cost Change Cost Change in Inventory Holding

Gain

B.I. + Purch. – Sales

Realizable holding gains (i.e., the holding gains that arose during

2016) totaled $340,000. On a FIFO basis, all of these gains were

realized in 2016 and included in income. (Since 4th-quarter sales of

2016 FIFO Income

$190,000

Thus, it is evident that Parque reported profits only because yelpin

costs were rising in 2016.

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 9-10

Requirement 3:

With current sales volume of 2,650,000 pounds and cash operating

costs of $2,800,000, the $1 per pound markup is too low to

generate profitable operating performance. This condition was

Under these conditions, Parque’s ability to repay the loan from

operating profits (which are identical to operating cash flows in this

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 9-11