P7-6. Tying bonus to EPS performance

Requirement 1:

According to the bonus formula, Mr. Brincat would receive a bonus of

$500,000 if the company reported net after-tax earnings of $50 million and

the EPS increase was 10 percent.

Requirement 2:

According to the bonus formula, Mr. Brincat would receive a bonus of

$846,140 if the company reports net after-tax earnings of $50 million and the

EPS increase is 30 percent.

Assuming the company has not issued or repurchased stock during the

So, earnings last year must equal $50 / (1.30) or $38.462 million.

Requirement 3:

Most shareholders would not feel very comfortable if managers had this type

of compensation package. Consider, for example, the incentive bonus. It is

based on annual increases in EPS, and the larger the EPS increase, the

The combination of annual bonuses and stock options tied to EPS growth

sends a clear signal to management: EPS is all that matters. Shareholders,

P7-7. Earnings quality and pay

Requirement 1:

7-1

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

The first thing to note about the suggested adjustments is that there is no

mention of the nonoperating income items and gains. The list provided by

company managers is one-sided: It identifies nonoperating items that

Consider the three income-reducing special items:

a) Loss on early retirement of debt

The compensation committee could determine that the bonus should be paid

solely on the basis of reported net income and that no adjustment is

On the other hand, a reasonable argument can be made for excluding (a)

from the bonus calculation. Here, changes in the company’s optimal financial

A similar argument can be made to exclude (b) and (c) from the bonus

calculation. Changes in the company’s economic environment may have

contributed to the need for a restructuring and the discontinued operations.

Requirement 2:

(a) Income from continuing operations. The rationale here is to exclude

(b) Income from continuing operations, adjusted for all nonrecurring

items. The idea is to exclude nonrecurring losses so that managers have an

7-2

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

(c) Income from continuing operations, adjusted for nonrecurring

losses only. As in (b), the rationale here is to provide managers with an

P7-8. Avoiding debt covenant violations

Requirement 1:

For most companies, the fixed charges ratio is a variation of the interest

coverage ratio. With only two weeks until the books are closed, the company

Accelerate the recognition of revenue from the first few days of next year

Delay the recognition of expenses from the last few days of this year until

Postpone discretionary expenses like maintenance, research and

Change one or more accounting methods to increase reported earnings. For

Change one or more accounting estimates. For instance, increase the

Requirements 2 and 3:

Some actions that could be taken to avoid violating the tangible net worth

ratio are:

7-3

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

To reduce the ratio of consolidated debt to total capitalization (i.e., to total

Requirement 4:

Answers to this question will vary from student to student. The dilemma

confronting the banker involves a trade-off between (a) using covenants to

P7-9. Accounting in regulated industries

Requirement 1:

Duke Energy is alerting readers of its financial statements that certain

reported asset and liability items are unique to the rate-making process, and

Requirement 2:

In this particular instance, Duke Energy is reminding readers that some

interest costs are assigned to the balance sheet, and thus are not included in

Duke Energy is also reminding financial statement readers that certain

(implicit) equity costs are also assigned to the balance sheet as part of

Requirement 3:

The chapter provides several examples of regulatory expense shifting where

firms have incentives to classify a cost (e.g., corporate advertising) as an

allowed operating cost rather than a cost not allowed for rate determination.

7-4

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

P7-10. Understanding rate regulation and accounting choices

Requirement 1:

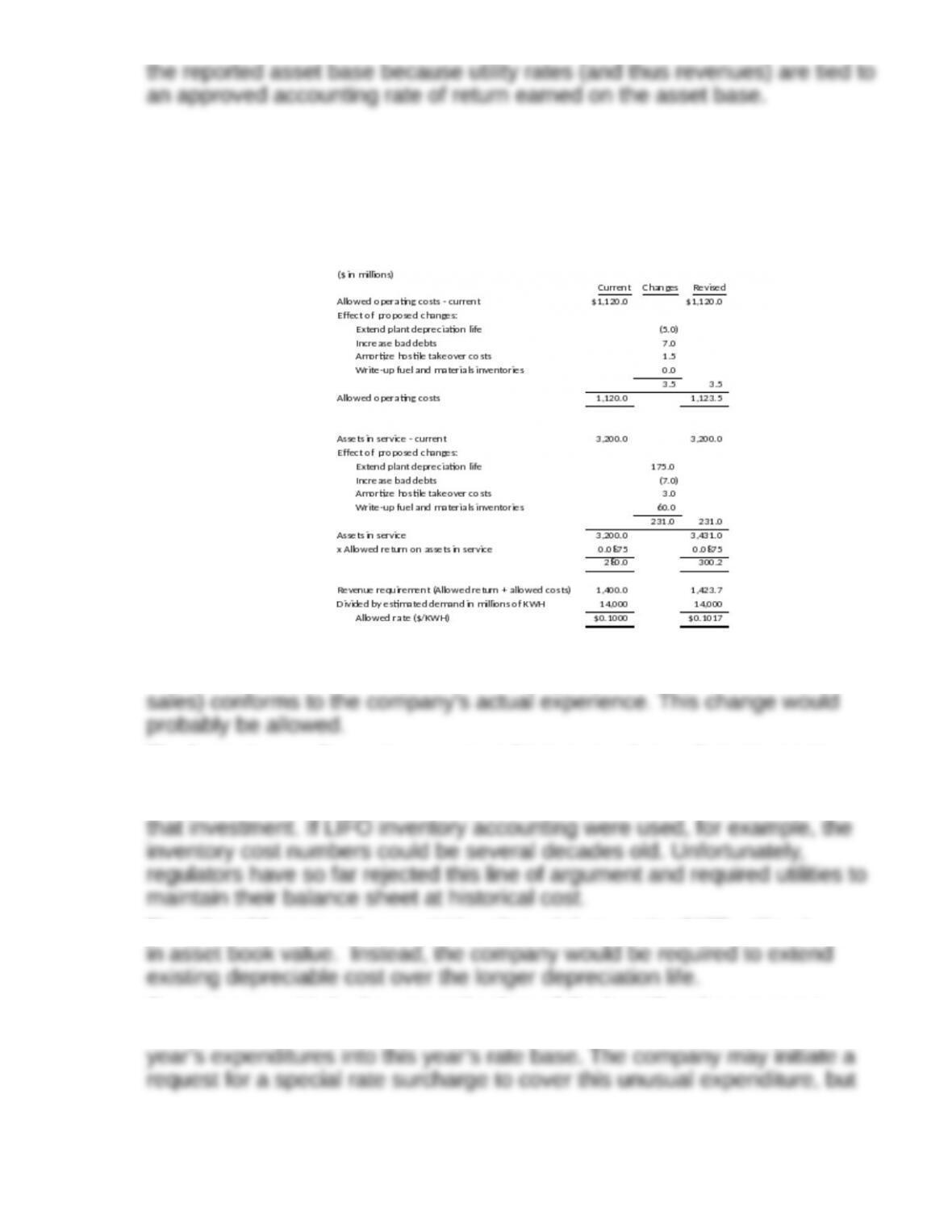

The following table shows the impact of the proposed accounting changes on

2017’s revenue requirement and rate per kilowatt hour:

Requirement 2:

The bad debt increase is plausible as long as the revised estimate (1.5% of

The inventory write-up to current replacement value makes economic

sense. Investors should be allowed to earn a fair return (8.75%) on their

current investment in the company, not on an outdated historical measure of

The plant life extension would be allowed, but not the $175 million increase

Regulators would disallow amortization of the hostile takeover cost

incurred last year. This is nothing more than a bold attempt to get one of last

7-5

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

that too is likely to be rejected because the outlay was of little benefit to

customers.

Financial Reporting and Analysis (7th Ed.)

Chapter 7 Solutions

The Role of Financial Information in Contracting

Cases

Cases

C7-1. Maxcor Manufacturing: Compensation and earnings quality

Requirement:

There are several reasons why Ms. Magee should feel uneasy about

Maxcor’s computation of 2017 operating profits:

Some research and development (R&D) expenses are shown above the

operating profit line (in cost of goods sold) and some are below the line (as

research and development expense). The classification decision may allow

Plant closing costs lowered net income for the year. The issue here is

whether management should be penalized (or rewarded) for this business

Should the 100% bonus payout for 2017 be approved? Probably not. Sales

are down nearly 12%. Operating costs fell by a similar percentage, but much

Here are some possible changes to the bonus formula:

7-6

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Use a “bonus bank” that spans several years to guard against the

Charge for the capital used in the company so that bonus payments reflect

Use stock options, phantom shares, or stock purchases to make managers

C7-2. Whole Foods Market: EVA-based compensation

Requirement 1:1

Whole Foods Market describes its EVA performance metric as “equivalent to

net operating profits after taxes minus a charge for the cost of capital

First, performance is based on a measure of operating profits, which means

that non-operating gains and losses that might otherwise flow through GAAP

Second, EVA subtracts a cost of capital charge that is omitted from GAAP

earnings. To see why this capital charge can be important to companies such

as Whole Foods Market, put yourself in the shoes of a regional manager and

assume that your incentive compensation is based on GAAP operating

earnings. You could grow earnings—and increase your incentive pay—in any

1 EVA® is a trademark held by Stern Stewart & Company, a consulting firm that has developed a proprietary

approach to the use of economic value added as business management and analysis tool. Whole Foods

Market does not associate the trademark symbol (®) with EVA in its narrative discussion, and we follow that

same practice here.

7-7

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Requirement 2:

The company says that “stock price performance has not been a factor in

determining annual compensation because the price of the Company’s

Whole Foods Market grants stock options and restricted stock to managers

and executives. These pay mechanisms presumably help align the interests

Requirement 3:

At Whole Foods Market, EVA is based on GAAP operating earnings so

managers still have incentives to use accounting discretion to boost the

earnings component of EVA. At other firms, it is common for the EVA

Requirement 4:

The annual EVA bonus for a particular Team Member is first deposited in a

“pool”, and then a portion of the pool balance is paid out annually. The

payout amount is 100% of the pool “up to certain job-specific dollar amounts

To understand how the EVA bonus pool can help overcome the tendency of

management to focus on the short term, consider the bonus pool of one

7-8

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

year. The remaining $15,000 of the bonus stays in the pool for possible

payout next period. And that’s the rub! The advertising curtailment this

period may harm sales next period thus reducing future EVA and bonus

Requirement 5:

When an average of several metrics is used, it is more difficult for managers

to “game the system” by maximizing a single metric when doing so is not

optimal. For example, if a single metric of sales growth is used, managers

have an incentive to seek all avenues of increasing sales, even when doing

so is not profitable due to thin or even negative operating margins. In

C7-3 Duke Power Corp: Rate regulation and earnings management

Requirement 1:

Utility companies that fall short of their regulatory rate-of-return profit goals

can appeal to state utility commissions for rate relief—an increase in the

Requirement 2:

If the $10 million consulting fee is considered by regulators to be “above the

line,” it will be included among the operating expenses that are used to

determine the prices charged customers (i.e., the company’s allowed utility

rates). On the other hand, if the fee is viewed by regulators as “below the

Requirement 3:

7-9

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Regulated firms such as banks, insurance companies, and Duke Power use

regulatory accounting practices (RAP) when preparing the financial

statements they submit to their regulatory agencies. The GAAP used by

C7-4. Computer Associates International: Compensation and accounting

irregularities

Requirement 1:

Two features of the plan may have contributed to illegal backdating of sales

contracts. The plan has a minimum performance threshold below which no

bonus is awarded. The bonus award jumps from zero to 50% of salary if the

Once the minimum earnings threshold is exceeded, managers receive larger

bonuses as performance increases (up to a maximum of 200% of salary). As

Requirement 2:

When executives have a large fraction of the personal wealth tied to stock

options, they have incentives to cater to Wall Street (e.g., analysts, investors,

and the financial press) and thereby maintain or increase the company’s

Requirement 3:

Auditors routinely look for an unusual clustering transactions at the end of a

quarter or year, particular if the amounts involved are large and help the

company just meet or beat Wall Street sales or earnings expectations,

achieve management bonus targets, or comply with loan covenants.

However, the business model at Computer Associates created a natural

7-10

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

7-11

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.