Financial Reporting and Analysis (7th Ed.)

Chapter 15 Solutions

Financial Reporting for Owners’ Equity

Exercises

Exercises

E15-1.Understanding Shareholders’ Equity (LO 15-1, LO 15-3, LO 15-6, LO 15-7)

Requirement 1:

Preferred stock is a class of “capital stock” that pays dividends at a specified

rate and that has preference over common stock in the payment of dividends

declared (“set”) quarterly by the company’s directors.

Requirement 2:

Treasury stock is stock (usually common shares) reacquired by the issuing

nor accrue dividends.

Requirement 3:

Redeemable preferred stock is a less permanent form of ownership capital than

is traditional (non-redeemable) preferred stock. The SEC was concerned that

cash flow consequences.

Requirement 4:

The employer’s cost of stock-based compensation—employee stock options

Requirement 5:

The employer’s cost of stock-based compensation is expensed (usually on a

Requirement 6:

Firms that have complex capital structures have financed their business

activities either using (a) securities that are convertible into common stock, or

EPS does not.

E15-2. Issuing common stock (LO 15-5)

Common stock–par value (600,000 shares issued x $3 par) $1,800,000

E15-3.Retiring common stock (LO 15-1)

(AICPA adapted)

Because the shares are “retired” rather than “held in treasury,” they are

entry to record the repurchase is:

DR Common stock par (100,000 shares x $10) $1,000,000

*The original APIC is reduced for retired shares according to the original issue

The account balances after this entry are:

Common stock par (800,000 shares x $10) $8,000,000

E15-4.Analyzing debt and redeemable preferred stock (LO 15-3)

Requirement 1:

The bond will be recorded as a $10 million long-term liability with annual

(not dividends).

E15-5.Analyzing various stock transactions (LO 15-1, LO 15-5)

(AICPA adapted)

The capital transactions are described in the following schedule:

Common Stock Accounts

Cash Par APIC Treasur

y

1/05/17: issued 100,000 shares at $5 each $500,000 $500,00

0

each

Balance at 12/31/2017 $1,100,000 $825,00

0

$275,00

0

$0

E15-6.Determining how many shares? (LO 15-5)

(AICPA adapted)

The number of preferred shares issued can be found by dividing the balance in

$300,000/$5 = 60,000 shares

assuming the shares were issued at this stated value.

E15-7. Treasury Stock (LO 15-1)

Common stock—par $ 4,800,000 (1)

Additional paid-in capital 19,200,000 (2)

share issue price minus $2 per share assigned to par value)

$3,400,000 = 200,000 shares X $17 per share repurchase price.

E15-8. Determining stockholders’ equity after a stock repurchase (LO 15-1, LO

15-5)

(AICPA adapted)

Common Stock Accounts

Par APIC Treasury

Retaine

d

Earning

s

9:

Balance at 12/31/19 $2,000,00

0

$968,000 ($48,000) $370,00

0

E15-9.Stock dividends and retained earnings (LO 15-4, LO 15-5)

(AICPA adapted)

The entry to record the stock dividend (900 shares x $8 = $7,200) is:

The retained earnings balance on March 31, 2018, is:

Balance on 12/31/17 $73,000

E15-10. Weighted-average number of shares (LO 15-6)

Analysis of common shares: Weight Weighted

Number (months) Average

1/1/2017 Shares outstanding at beginning of

year

600,000 12/12 600,000

outstanding

E15-11. Retained earnings transactions (LO 15-1, LO 15-4)

The legality of corporate dividend distributions varies from state to state. In

excess of current-year net income.

Nathan Corporation’s retained earnings balance as of the end of 2017 is

actually pay dividends in such a large amount.

E15-12. Determining stockholders’ equity after a stock split (LO 15-5)

(AICPA adapted)

The stockholders’ equity accounts on June 30, 2017, after the split

Retained earnings 1,350,000

E15-13. Computing basic EPS (LO 15-6)

(AICPA adapted)

Basic EPS =

(Net income- Preferred dividends)

Weighted-average common shares outstanding

10,000 common shares were issued and outstanding the full year, and

another 2,000 shares were issued on July 1. So the weighted-average

common shares outstanding is 10,000 + 2,000 x 1/2 year = 11,000

shares.

This means:

Basic EPS =

$10,000 $1,000

11, 000 shares

= $0.82 per share

E15-14. Finding the number of shares for EPS (LO 15-6)

(AICPA adapted)

Number

of shares

Weight

% of year

EPS

Basic Diluted

Common shares outstanding 1/1/17 5,000,000 100% 5,000,000 5,000,000

Number of shares used in EPS computation 6,000,000 6,100,000

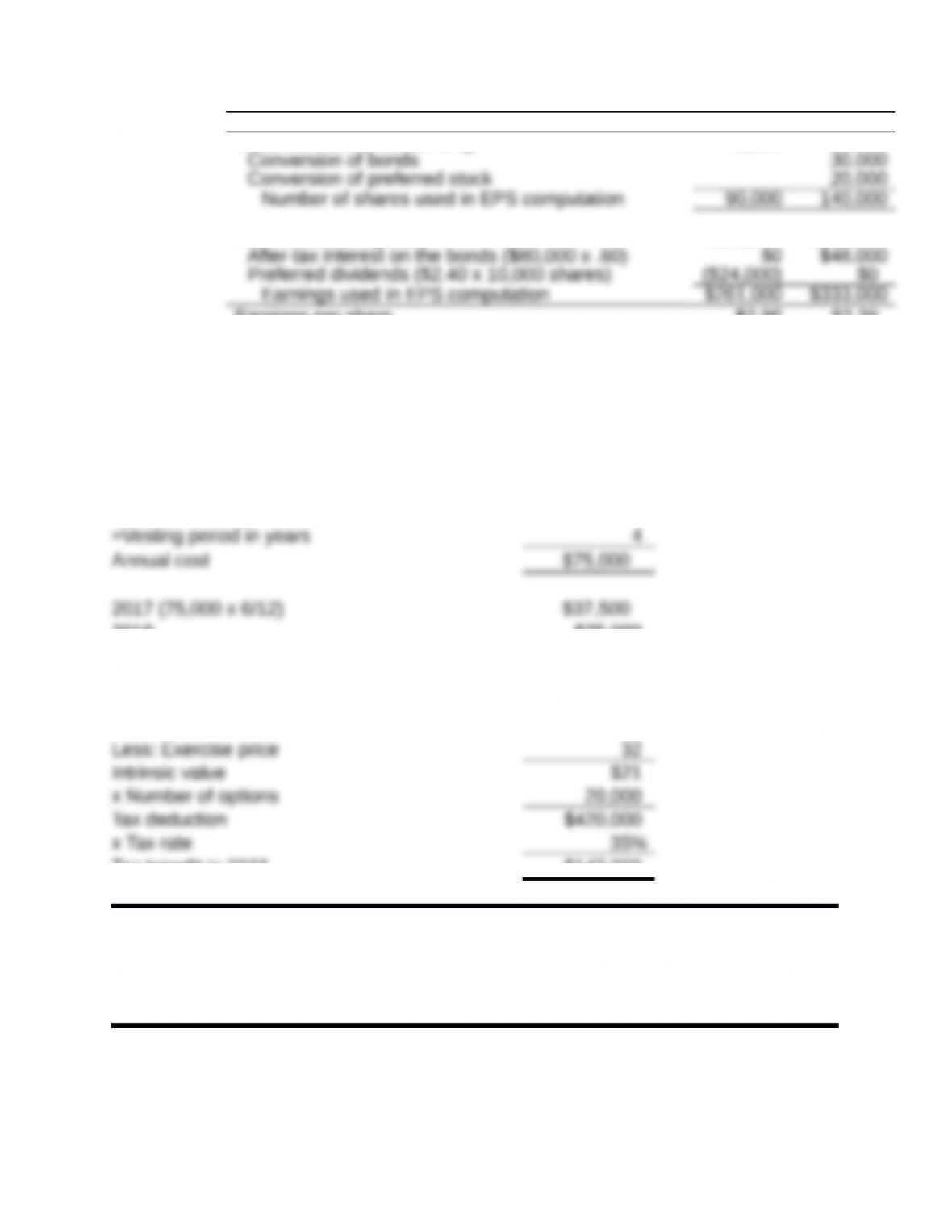

E15-15. Calculating earnings per share (LO 15-6)

(AICPA adapted)

Requirements 1 and 2:

EPS for 2017

Basic Diluted

Common shares outstanding 90,000 90,000

Net income as reported $285,000 $285,000

Earnings per share $2.90 $2.38

E15-16. Employee stock options (LO 15-7, LO 15-8)

(AICPA adapted)

Requirement 1 – Compensation expense in 2017 and 2018

Total compensation cost (15 x 20,000) $300,000

2018 $75,000

Requirement 2 – Tax benefit in 2023

Stock price at date of exercise $53

Tax benefit in 2023 $147,000

Financial Reporting and Analysis (7th Ed.)

Chapter 15 Solutions

Financial Reporting for Owners’ Equity

Problems

Problems

P15-1.Identifying incentives for stock repurchases (LO 15-2)

Requirement 1:

The answer to this question depends on when, during the year, shares

Target 2018 EPS = $5.25 = $10 million/shares

There must be 1,818,182 shares outstanding, so 86,580 shares must be

is borrowed.

Requirement 2:

If the buybacks occur mid-year, Keystone would need to double the number

Requirement 3:

There are several reasons Keystone’s management may want to maintain the

Management compensation and loan agreements may be tied to specific

Maintain credibility with analysts and investors by delivering earnings

P15-2. Understanding convertible debt (LO 15-9)

Requirement 1:

Investors who purchase Massey Coal’s convertible notes receive two distinct

promised interest rate (2%) for the debt component because the notes

include a valuable conversion option.

Requirement 2:

As described in Chapter 11, the financial statement notes for long-term debt

addition, this note typically discloses the average interest rate the firm is

paying on its long-term debt.

Requirement 3:

U.S. GAAP guidelines do not yet require firms to bifurcate the convertible note

component and conversion option, and use the 12% interest rate.

P15-3. Recording cash and stock dividends (LO 15-5)

Requirement 1:

Journal entries for the three dividend events are:

Preferred dividends: $10 per share x 50,000 shares.

DR Retained earnings $250,000

CR Cash

$250,000

Stock dividend: Since the dividend is less than 25%, it is recorded at the market

$12,900,000 or ($135 – $6) x 100,000.

DR Retained earnings $13,500,000

12,900,000

Requirement 2:

The market value of the company’s common stock at the time the stock

unchanged. As a result, the share price will fall from $135 to $122.73

($135,000,000/1,100,000).

P15-4. Determining the effects of splits, dividends, and retained earnings (LO

15-5)

Requirement 1:

Both options allow the company to avoid violating the limit on cash dividend

payments. With regard to option A, a stock split of 12 for 10 means investors

recording the dividend. Retained earnings would be reduced by the par-value

of stock issued, or $1,980,000 (30% x 1,100,000 shares x $6 per share) but

this will not violate the dividend constraint.

Requirement 2:

Stockholders prefer cash dividends and stock price appreciation to just more

dividend payments in the future. Otherwise, it is not clear that stockholders will

have a strong preference for any of these options.