[QUESTION]

63. A consolidated balance sheet

a. includes the net assets of the parent company and all of its subsidiaries.

b. reports separately the net assets of the parent company and its subsidiaries

c. includes the net assets of the parent company and all components in which it owns

more than 75% of the outstanding voting stock.

d. includes the net assets of only the subsidiary companies.

64. Which of the following statements about retained earnings is not true?

a. Retained earnings reflect the net income of previous accounting periods only.

b. Retained earnings measures the cumulative earnings of the company since inception,

minus dividends distributed.

c. Retained earnings represents cumulative earnings that have been reinvested in the

business.

d. Retained earnings may represent a large portion of stockholders’ equity.

65. Information found on a company’s balance sheet can tell a story about

a. the company and its strategies.

b. the company’s industry.

c. the company’s performance.

d. All of these can be derived from the information on the balance sheet.

66. The U.K. Equity account “Share premium” is reported on U.S. GAAP balance sheets

as

a. capital reserve.

b. revaluation reserve.

c. capital in excess of par.

d. an accumulated other comprehensive income account.

67. The U.K. Equity account “Hedging reserve” is reported on a U.S. GAAP balance

sheet as

a. capital reserve.

b. revaluation reserve.

c. capital in excess of par.

d. an accumulated other comprehensive income account.

68. When adjusting accrual earnings to obtain cash flows from operations,

a. an increase in Accounts Payable is added to determine cash flow from operations.

b. a decrease in Accounts Payable is added to determine cash flow from operations.

c. an increase in Accounts Payable is deducted to determine cash flows from operations.

d. it is not necessary to consider any changes to Accounts Payable.

69. Cash collected from customers can be derived

a. by analyzing changes in the Accounts Payable balance.

b. by appropriately adjusting revenue for changes in accounts receivable.

c. by appropriately adjusting revenue for changes in accounts payable.

d. by analyzing changes to the reserve for doubtful accounts.

70. The sale of productive assets

a. does not impact the period cash flows.

b. is always considered a related party transaction.

c. represents an investing activity.

d. represents an operating activity.

71. Paying dividends to stockholders

a. represents an investing activity.

b. does not impact the period cash flows.

c. represents an operating activity.

d. represents a financing activity.

72. Operating activities result from the cash effects of

a. paying dividends to shareholders.

b. producing and delivering goods.

c. selling equipment.

d. issuing long-term debt.

73. The Summary of Significant Accounting Policies

a. explains the important accounting choices the reporting entity uses to account for

selected transactions and accounts.

b. does not contain an explanation of the company’s revenue recognition policies.

c. is generally a part of the equity section of the balance sheet.

d. is only required as part of a prospectus for the sale of new shares of stock.

74. Subsequent events

a. are those significant events that occur after the financial statements are issued.

b. are subject to optional disclosure based on a recommendation from top management.

c. are required to be disclosed if they are material and likely to influence investors’

appraisal of the risk and return prospects of the reporting entity.

d. are those significant events that occur in the last quarter of the reporting period.

75. The cash flow from operating activities

a. is required to be presented using the direct method by U.S. GAAP and IFRS.

b. can be presented by using either the direct method or the indirect method.

c. comprises only the increase in cash arising from the firm’s profit-making activities.

d. can vary depending on whether the presentation is done under the direct method or the

indirect method.

76. The balance sheet

a. provides a summary of a firm’s assets, liabilities, equity and cash flows as of a specific

date.

b. classifies assets as current if they are expected to be converted into cash within 24

months.

c. is an expression of the accounting equation.

d. is comprised of items shown only at historical costs.

77. The following information is available from Moran Industries’ accounting system for

the year ended December 31, 2018.

Cash received from customers

$750,000

Cash paid to suppliers

$300,000

Cash paid to employees

$150,000

Taxes paid

$25,000

Cash dividends paid

$50,000

What would the company’s statement of cash flows report as cash flow from operations?

a. $225,000

b. $275,00

c. $300,000

d. $250,000

78. Liabilities represent amounts that are

a. probable future economic benefits obtained or controlled by an entity as a result of past

transactions or events.

b. always classified as current on the balance sheet.

c. never shown on the balance sheet at historical cost.

d. netted against assets on the balance sheet.

79. On balance sheets prepared in accordance with U.S. GAAP

a. assets are generally listed from least liquid to most liquid.

b. liabilities are generally netted against assets.

c. assets are generally listed from most liquid to least liquid.

d. both tangible and intangible long-lived assets can be revalued upward periodically.

80. A balance sheet prepared in accordance with U.S. GAAP typically

a. includes both “noncurrent liability” and “long–term obligation” sections.

b. reports inventory at historical costs.

c. reports cash at its current market value.

d. reports retained earnings comprised of the cumulative earnings less dividends since the

inception of the entity.

81. A balance sheet prepared in accordance with U.S. GAAP typically

a. reports common stock at the current market price of the stock.

b. provides critical information for understanding a firm’s capital structure.

c. helps to determine the proper mix of debt and equity financing.

d. provides critical information for understanding a firm’s profitability.

82. A temporary difference is the result of

a. a revenue or expense item reported in different periods for book purposes and tax

purposes.

b. fluctuations in the exchange rate.

c. adjustments between the trial balance and general ledger.

d. delays between the sale of a product and the recording of the account receivable.

83. The indirect method of presenting cash flow from operating activities

a. is strongly recommended by both U.S. GAAP and IFRS.

b. focuses on how cash flows deviate from a natural benchmark – net income.

c. presents cash transactions related to the determination of net income.

d. is more difficult than the direct method to incorporate working capital changes into a

financial model.

84. A related-party transaction

a. is assumed to be an arms-length transaction.

b. can take place between subsidiaries of a common parent.

c. does not need to be disclosed in financial statements prepared under U.S. GAAP.

d. presents less risk than a similar transaction with a third party.

85. Properly prepared statements of cash flows

a. include stock issued for cash as an investing activity.

b. present depreciation as a subtraction from net income to arrive at a firm’s cash flow

from operations under the indirect method.

c. are frequently used by investment analysts to cash flows from operations across two or

more companies.

d. will show the change in cash during a period to be equal to the net income for the

period.

86. On a balance sheet prepared under U.S. GAAP

a. accounts receivable is presented at net realizable value.

b. inventories are presented at current market price.

c. any cash denominated in a foreign currency is disclosed in a footnote.

d. most short-term investments are presented at historical cost.

87. Long-term debt

a. consists of monetary obligations that fall due beyond two years from the balance sheet

date.

b. when issued, is carried at an amount based on the proceeds received.

c. usually has an effective yield that is much different than the cost of borrowing.

d. never has any portion classified as a current liability.

88. Goodwill

a. is a tangible asset recognized as part of a business combination.

b. is not subject to impairment.

c. is initially measured as the difference between the consideration given in an acquisition

and the fair value of the separately identifiable net assets acquired on the acquisition date.

d. is classified on the balance sheet as a current asset.

89. Other comprehensive income

a. consists of certain gains and losses included in comprehensive income but not yet

recognized in the income statement.

b. is never adjusted for tax effects.

c. does not include foreign currency gains and losses.

d. is consistently defined in international balance sheet presentation.

90. Which of the following is not true regarding the tax note to the financial statements?

a. The tax note is never required to include any information on foreign tax rate

implications.

b. The tax note can describe how financial reporting differs from tax accounting.

c. The tax note can describe how tax disputes may affect future tax payments.

d. The tax note can explain how foreign tax rates affect income tax expense.

91. The rules used for determining taxable income in various countries

a. have the same objective as the rules used for determining income for financial

reporting purposes.

b. have an objective designed to provide a basis for funding government operations.

c. are not the result of a political process.

d. measure changes in a firm’s underlying economic condition.

92. Which of the following statements is not true regarding cash flow from operating

activities?

a. Most firms use the indirect method for presentation.

b. Each line item in a direct method cash flow statement is actually a cash flow.

c. The direct method begins with net income and then shows the differences between

operating cash flow and net income.

d. There are two methods for presenting cash flow from operating activities.

93. A balance sheet prepared under U.S. GAAP includes the following elements except

a. an asset section

b. a liabilities section

c. an equity section

d. a cash flow section

94. The summary of significant accounting policies does not help explain

a. the cost flow assumptions for valuing inventory.

b. management’s assessment of the financial condition of the firm.

c. the method used for determining depreciation expense.

d. whether certain investments are accounted for using the equity method.

95. A balance sheet prepared under U.S. GAAP can have amounts presented in the

following measurement bases except

a. foreign currency

b. historical costs

c. discounted present values

d. current replacement costs

96. Which of the following statements is not true regarding the cash flow statement?

a. The cash flow statement provides information about changes in all the balance sheet

accounts.

b. The change in cash is classified into cash flow from three categories: operating

activities, investing activities and financing activities.

c. The cash flow statement generally shows that cash flows and accrual earnings are

substantially the same.

d. The cash flow statement explains the causes for year-to-year changes in cash and cash

equivalents.

97. Blimpy’s Doughnuts, Inc.’s adjusted trial balance appears below.

Required: Prepare a classified balance sheet at December 31, 2018 for Blimpy’s. Hint:

Account categories for several of the items listed are found in parentheses.

Blimpy’s Doughnuts, Inc.

Adjusted Trial Balance (alphabetical order)

December 31, 2018

Debits

Credits

Accounts and notes receivable

$27,603

Accounts payable

$7,874

Accrued litigation settlement (current liability)

86,772

Accumulated deficit

191,010

Accumulated other comprehensive income

1,266

Cash and cash equivalents

36,242

Common stock

310,942

Current maturities of long-term debt

1,730

Deferred income taxes (noncurrent asset)

20

Deferred income taxes (current liability)

20

Depreciation and amortization

21,046

Direct operating expenses

389,379

Equity in (losses) of equity method franchisees

842

General and administrative expenses

48,860

Goodwill and other intangible assets

28,934

Impairment charges and lease termination costs

12,519

Insurance recovery receivable (current asset)

34,967

Interest expense

20,334

Interest income

1,627

Inventories

21,006

Investments in equity method franchisees

3,224

Long-term debt, less current maturities

105,966

Other accrued liabilities

38,474

Other assets

16,842

Other current assets

12,000

Other income

5,105

Other long-term obligations

29,694

Property and equipment

168,654

Provision for income taxes

1,211

Revenues

461,195

Settlement of litigation (expense)

15,972

Totals

$1,050,665

$1,050,665

Blimpy’s Doughnuts, Inc.

Consolidated Balance Sheet

December 31, 2018

ASSETS

Current Assets:

Cash and cash equivalents

Accounts and notes receivable

Inventories

Insurance recovery receivable

Other current assets

Total current assets

Property and equipment

Investments in equity method franchisees

Goodwill and other intangible assets

Deferred income taxes

Other assets

Total assets

Current Liabilities:

Current maturities of long-term debt

Accounts payable

Accrued litigation settlement

Deferred income taxes

Other accrued liabilities

Long-term debt, less current maturities

Other long-term obligations

Common stock

Accumulated other comprehensive income

Accumulated deficit

98. Harry’s Clothing, Inc. used the following headings on the company’s December 31,

2018 balance sheet:

(A) Current assets

(B) Long-term investments

(C) Property and equipment

(D) Intangible assets

(E) Other assets

(F) Current liabilities

(G) Long-term debt

(H) Shareholders’ equity

Required: For each of the following items, indicate its normal balance sheet

classification category. Use (NA) for items that would not appear on the face of the

balance sheet, but would be discussed in the notes to the financial statements.

_____ 1. Accounts receivable

_____ 2. Accrued interest on notes payable (2019 maturity)

_____ 3. Accumulated depreciation

_____ 4. Goodwill

_____ 5. Preferred stock

_____ 6. Common stock

_____ 7. Customer deposits on products to be shipped in a few months

_____ 8. Depreciation methods and estimated lives of equipment

_____ 9. Prepaid insurance

_____ 10. Assets (surplus production equipment) held for sale

99. Below are the condensed balance sheets and income statement for the Beltway

Company, Inc. Reformat the balance sheet as a common-size balance sheet and evaluate

the company’s performance by responding to the questions provided.

Condensed balance sheet December 31, 2018

2017

2018

Assets:

Current assets

Cash

$8

$15

Accounts receivable

53

58

Inventory

52

40

Prepaid insurance

5

3

Property plant and equipment

140

150

Accumulated depreciation

(45)

(55)

Net PP&E

95

95

Total assets

$213

$211

Liabilities:

Accounts payable

$35

$21

Wages payable

12

16

Interest payable

5

2

Taxes payable

3

4

Long-term debt

92

92

Equity:

Common stock

50

50

Retained earnings

16

26

Total liabilities and equity

$213

$211

Required:

1. Reformat the balance sheet to be a common-sized balance sheet

2. Respond to the following question:

a. What does the common-size balance sheet suggest about the company’s

performance? [Hint: Review items that show a significant difference—as a

percentage—from 2017 to 2018.]

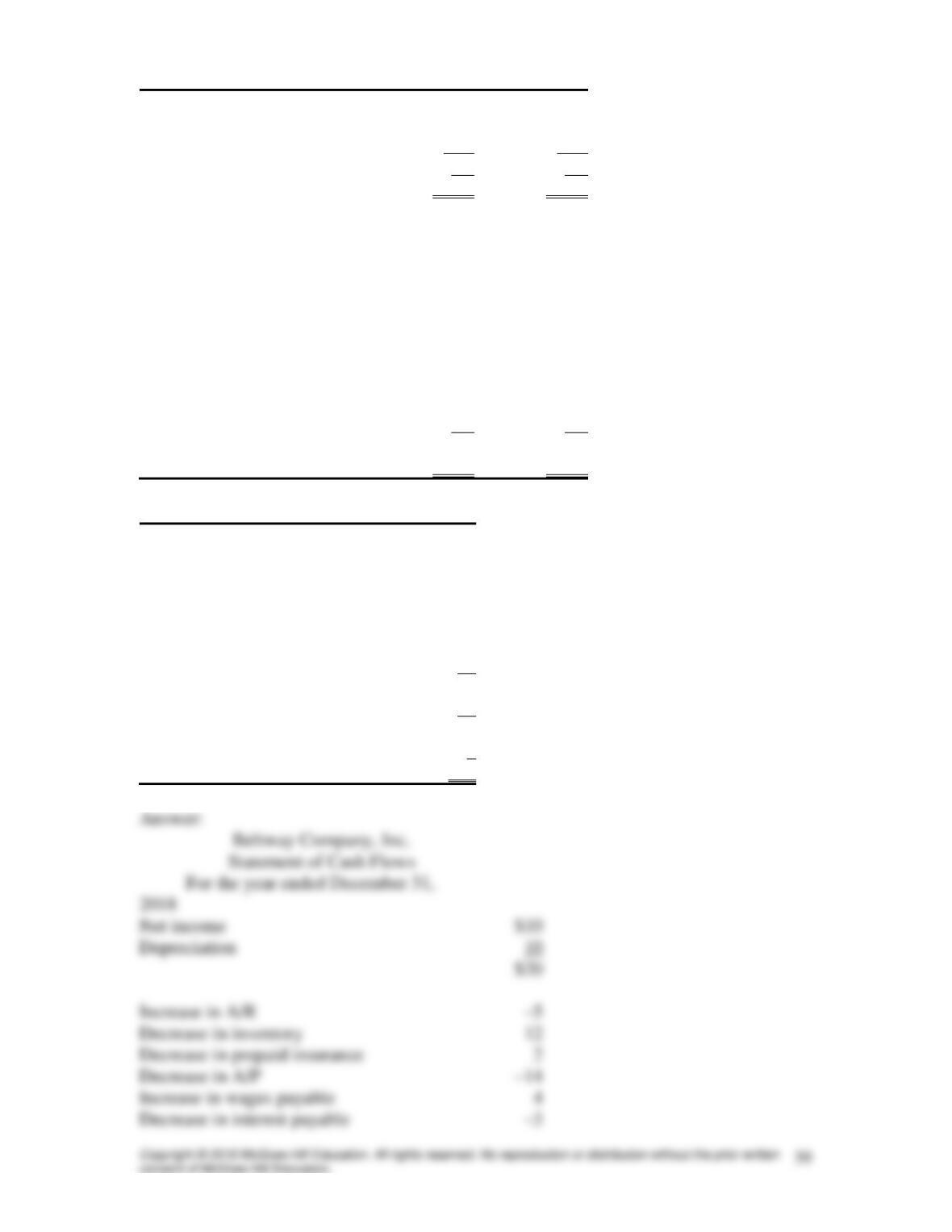

100. Below are the condensed balance sheet and income statement for the Beltway

Company, Inc. Assuming there were no disposals of fixed assets during the year 2018,

provide a statement of cash flows using the indirect method for the year ended December

31, 2018.

Condensed balance sheet December 31, 2018

2017

2018

Assets:

Current assets

Cash

$8

$15

Accounts receivable

53

58

Inventory

52

40

Prepaid insurance

5

3

Property plant and equipment

$140

$150

Accumulated depreciation

(45)

(55)

Net PP&E

95

95

Total assets

$213

$211

Liabilities:

Accounts payable

$35

$21

Wages payable

12

16

Interest payable

5

2

Taxes payable

3

4

Long-term debt

92

92

Equity:

Common stock

50

50

Retained earnings

16

26

Total liabilities and equity

$213

$211

Condensed income statement for year ended December 31, 2018

Sales

$480

COGS

328

Operating expenses:

Wages

103

Utilities

11

Insurance

3

Depreciation

10

Operating income

25

Interest

12

Income before tax

13

Tax

3

Net income

$10