Financial Reporting and Analysis (7th Ed.)

Chapter 5 Solutions

Essentials of Financial Statement Analysis

Exercises

Exercises

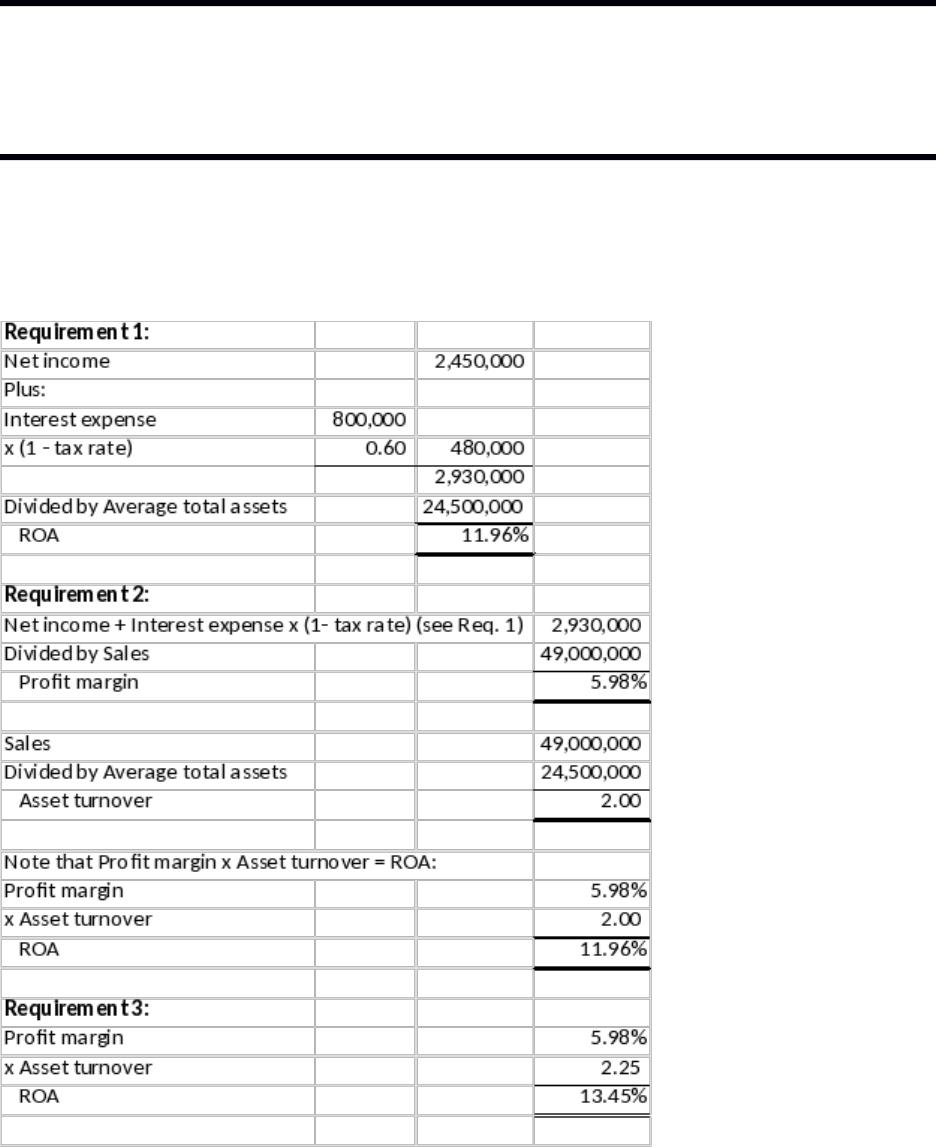

E5-1 Calculating profitability ratios

(AICPA adapted)

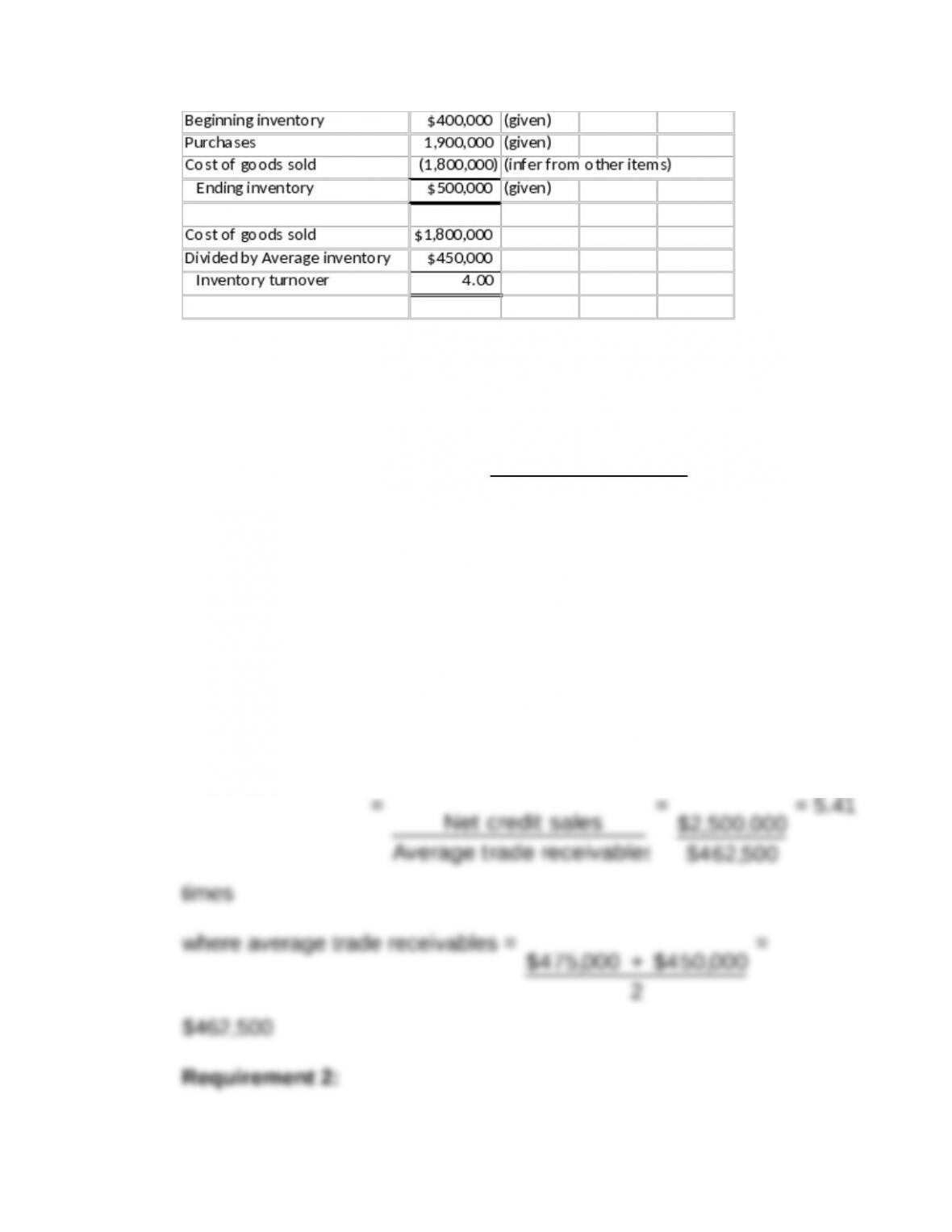

E5-2 Determining inventory turnover

(AICPA adapted)

E5-3 Determining receivable turnover

(AICPA adapted)

Accounts receivable turnover =

Total credit sales

Average receivables

= 5.0 and

Average receivables = ($250,000 + $300,000)/2 = $275,000. So,

Total credit sales = $275,000 x 5.0 = $1,375,000. Therefore, Total

net sales = $1,375,000 + $100,000 = $1,475,000.

E5-4 Assessing receivable and inventory turnover

(AICPA adapted)

Requirement 1:

Accounts receivable turnover

=

Net credit sales

Average trade receivables

=

$2,500,000

$462,500

= 5.41

times

where average trade receivables =

$475,000 + $450,000

2

=

$462,500

Requirement 2:

Inventory turnover =

Cost of goods sold

Average inventory

=

$2,000,000

$575,000

= 3.48

times

$600,000 + $550,000

2

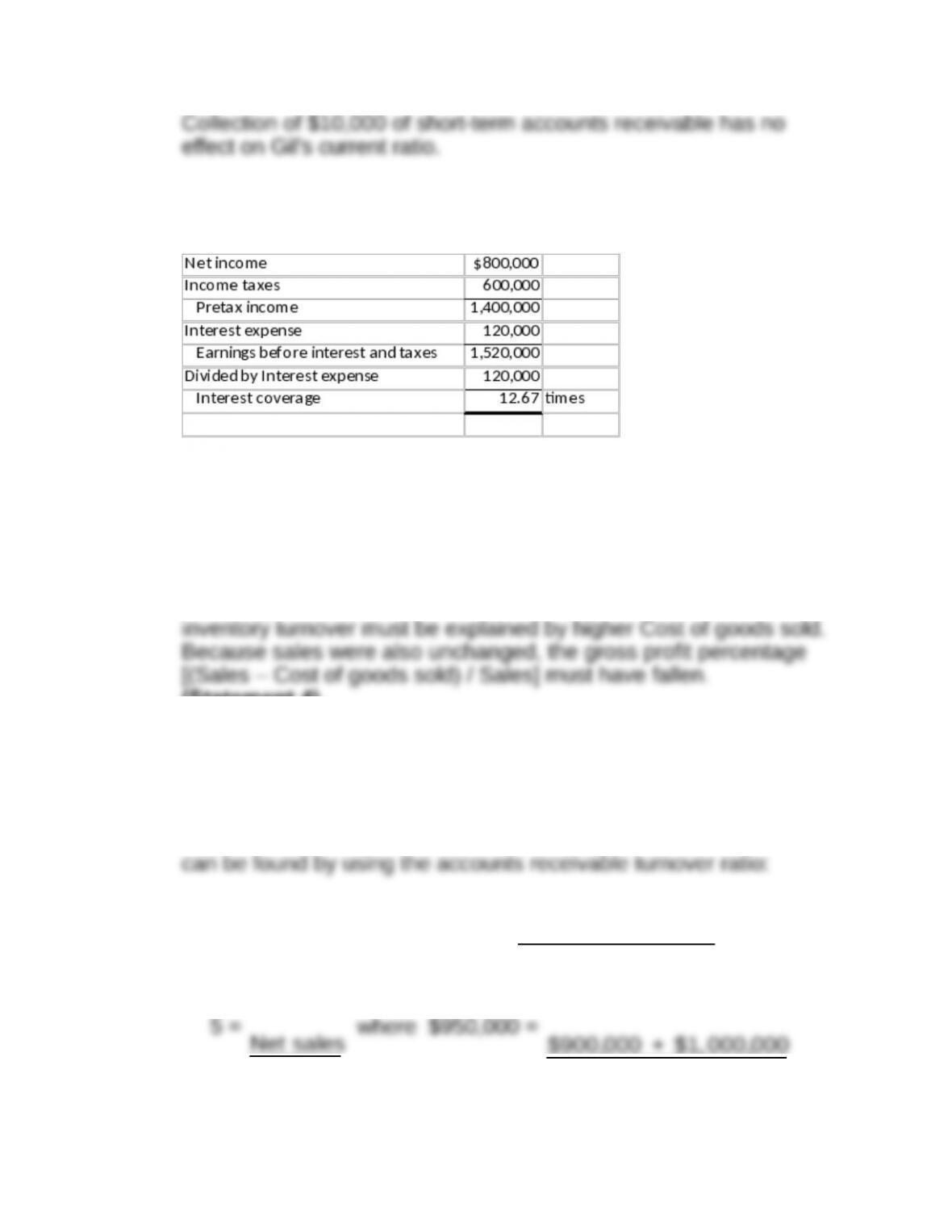

E5-5 Analyzing current and quick ratios

(AICPA adapted)

The write-off of obsolete inventory would decrease Todd

Corporation’s current assets, thus decreasing the current ratio. The

E5-6 Analyzing effects on current ratio

(AICPA adapted)

Requirement 1:

The refinancing of a $30,000 long-term mortgage with a short-term

Requirement 2:

Purchasing $50,000 of inventory with a short-term account payable

would increase Gil’s current assets to $140,000, and increase the

Requirement 3:

Paying $20,000 of short-term accounts payable decreases both the

current assets and liabilities by $20,000, making the current ratio

Requirement 4:

E5-7 Calculating interest coverage

(AICPA adapted)

E5-8 Analyzing why inventory turnover increased

(AICPA adapted)

Inventory turnover is Cost of goods sold divided by Average

inventory. The inventory level was unchanged, so an increase in

(Statement 4).

E5-9 Calculating days sales outstanding

(AICPA adapted)

Requirement 1:

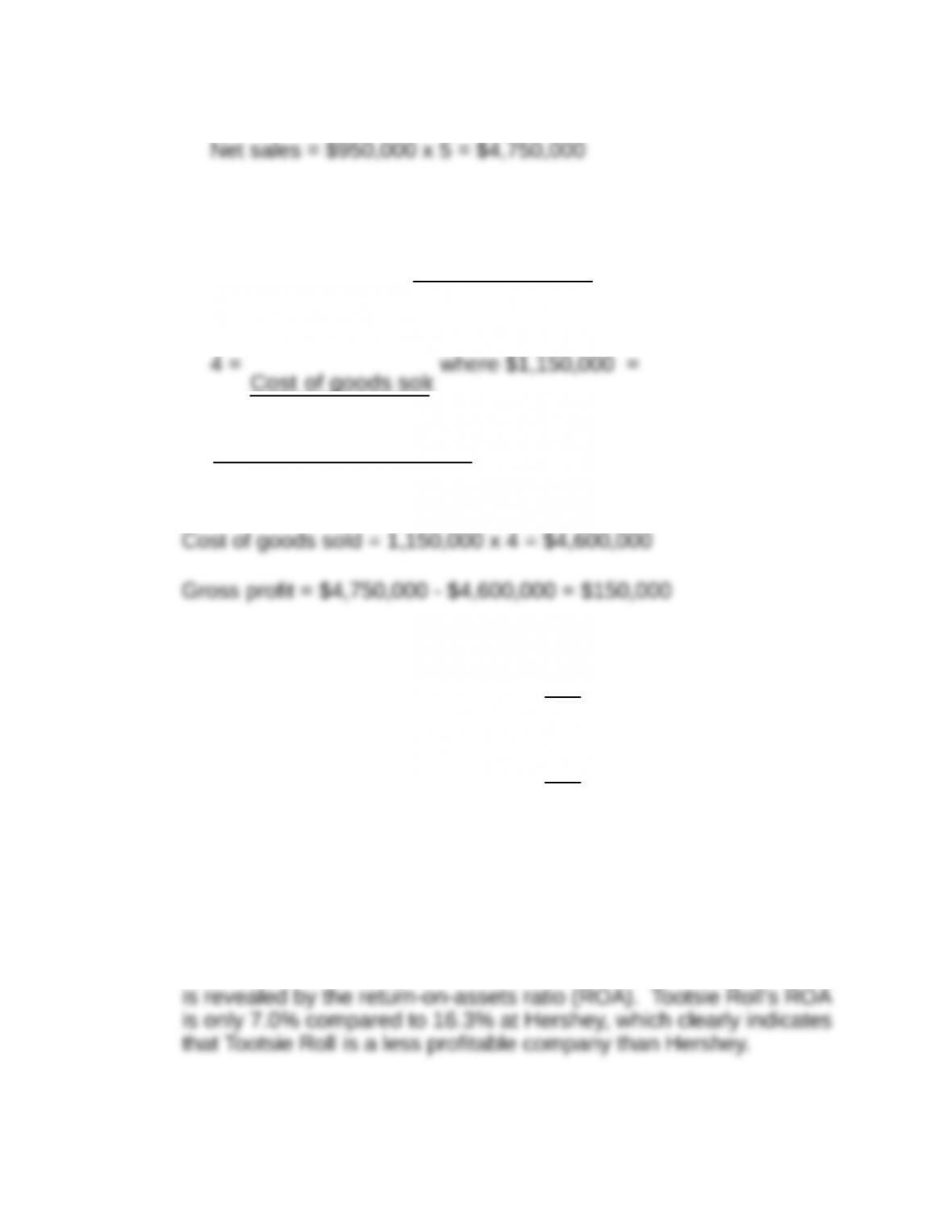

Gross profit equals net sales minus cost of goods sold. Net sales

Accounts receivable turnover =

Net sales

Average receivables

5 =

Net sales

$950,000

where $950,000 =

$900,000 + $1,000,000

2

Cost of goods sold can be found by using the inventory turnover ratio:

Inventory turnover =

Cost of goods sold

Average inventory

4 =

Cost of goods sold

$1,150,000

where $1,150,000 =

$1,100,000 + $1, 200,000

2

Cost of goods sold = 1,150,000 x 4 = $4,600,000

Gross profit = $4,750,000 – $4,600,000 = $150,000

Requirement 2:

Days’ sales in average receivables =

360

5

= 72 days

Days’ sales in average inventories =

360

4

= 90 days

E5-10 Hershey Company and Tootsie Roll Industries

Requirement 1:

Tootsie Roll is the smaller of the two companies as measured by

sales, and thus it should come as no surprise that Tootsie Roll also

reports smaller earnings. However, the real difference in profitability

Decomposing ROA into its profit margin and asset turnover

components shows that Hershey’s results are stronger on both

Requirement 2:

It is important to distinguish between brand familiarity and brand

value. Both companies have familiar (that is, recognizable) brands

but brand recognition does not always translate into brand value.

Companies with valuable brands are able to earn profits that exceed

E5-11 Mentor Graphics and its non-GAAP earnings

Requirement 1:

Here are the items specifically mentioned by management:

equity-based (noncash) employee compensation; severance and

related employee “rebalancing” costs; fees paid to consultants;

losses related to abandonment of excess facility space and to a

Requirement 2:

Calling attention to non-GAAP earnings can benefit analysts and

investors if it helps them to distinguish sustainable from

non-sustainable earnings. The SEC requires firms to provide a

detailed reconciliation of non-GAAP earnings to GAAP earnings so

Requirement 3:

Analysts and investors may be harmed if they naively assume that

excluded costs are non-recurring expenses of the business. Doing

E5-12 Calculating ROCE for Whole Foods Market

Requirements1 and 2:

Computation of ROCE

(Dollar amounts in millions) 2015 2012

Net income and nonrecurring items can be found in Exhibit 5.12.

Average common equity for 2015 is ($3,769 million + $3,813 million)

Requirement 3:

Financial leverage can be viewed as a multiplier that translates ROA

The company’s ROA was 9.7% in 2012 and 9.4% in 2015. Financial

leverage was beneficial in each of these years because ROCE

E5-13 Cause-of-change analysis

Requirement 1:

($ in millions)

Causes of change in net income

Net income – 2016 $1,364.0

Effect of increase in sales

Requirement 2:

Although net income grew by 5.8% ($1,443 vs. $1,364) from 2016

to 2017, sales increased by 18.2% ($6,500 vs. $5,500) over the

same period. The earnings increase did not keep pace with the

sales increase due to deteriorating margins and an increase in the

Financial Reporting and Analysis (7th Ed.)

Chapter 5 Solutions

Essentials of Financial Statement Analysis

Problems

Problems

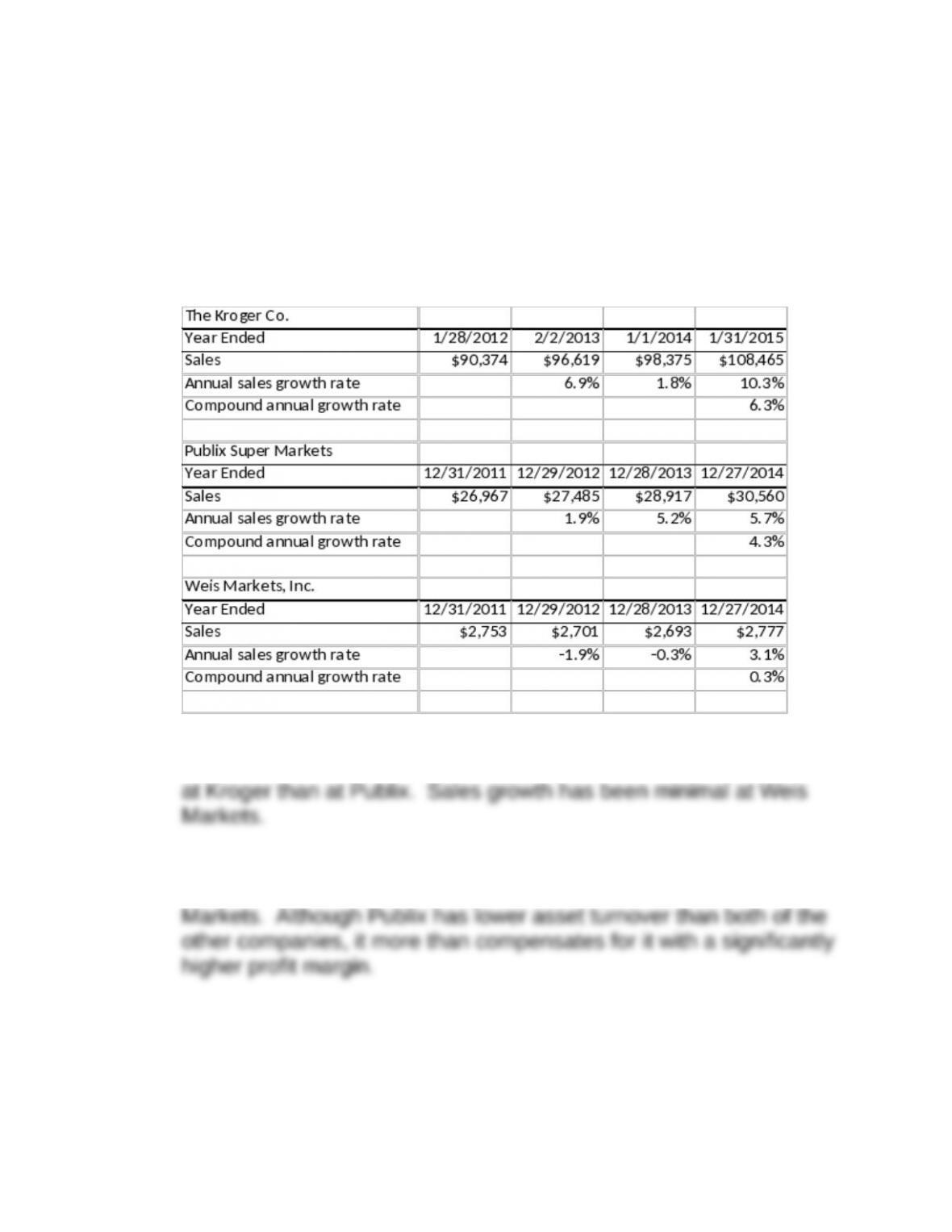

P5-1 Comparing profitability

Requirement 1:

Following are sales growth data for the three companies. All dollar

amounts are in millions.

This analysis indicates that sales growth has been slightly stronger

Requirement 2:

Publix has had consistently higher ROA than both Kroger and Weis

P5-2 Assessing short-term liquidity

Requirement 1:

Ross Stores has the lowest current ratio of the three companies at

1.36. However, its cash conversion cycle is only 22.4 days and the

Requirement 2:

Days inventory held is computed as 365 x Average inventory / Cost

of goods sold. Including occupancy costs in cost of goods sold

reduces the value calculated for days inventory held and therefore

also reduces the reported operating and cash conversion cycles.

Requirements 3 and 4:

Ross has a very low level of receivables relative to sales,

suggesting it extends credit on only a small portion of its sales. In

P5-3 Analyzing credit risk analysis and long-term solvency

Requirement 1:

Two coverage ratios are provided. The interest coverage ratio is

computed as earnings before interest and taxes (EBIT) divided by

interest expense. The cash flow coverage ratio uses operating cash

flow before considering interest and tax payments in the numerator

rather than EBIT. Both ratios suggest the company’s ability to

Requirement 2:

Based on AK Steel’s long-term debt to assets ratio, the company

Requirement 3:

AK Steel does not have significant amounts of intangible assets.

The long-term debt to assets ratio each year is nearly equal to the