Financial Reporting & Analysis (7th Ed.)

Chapter 17 Solutions

Statement of Cash Flows

Exercises

Exercises

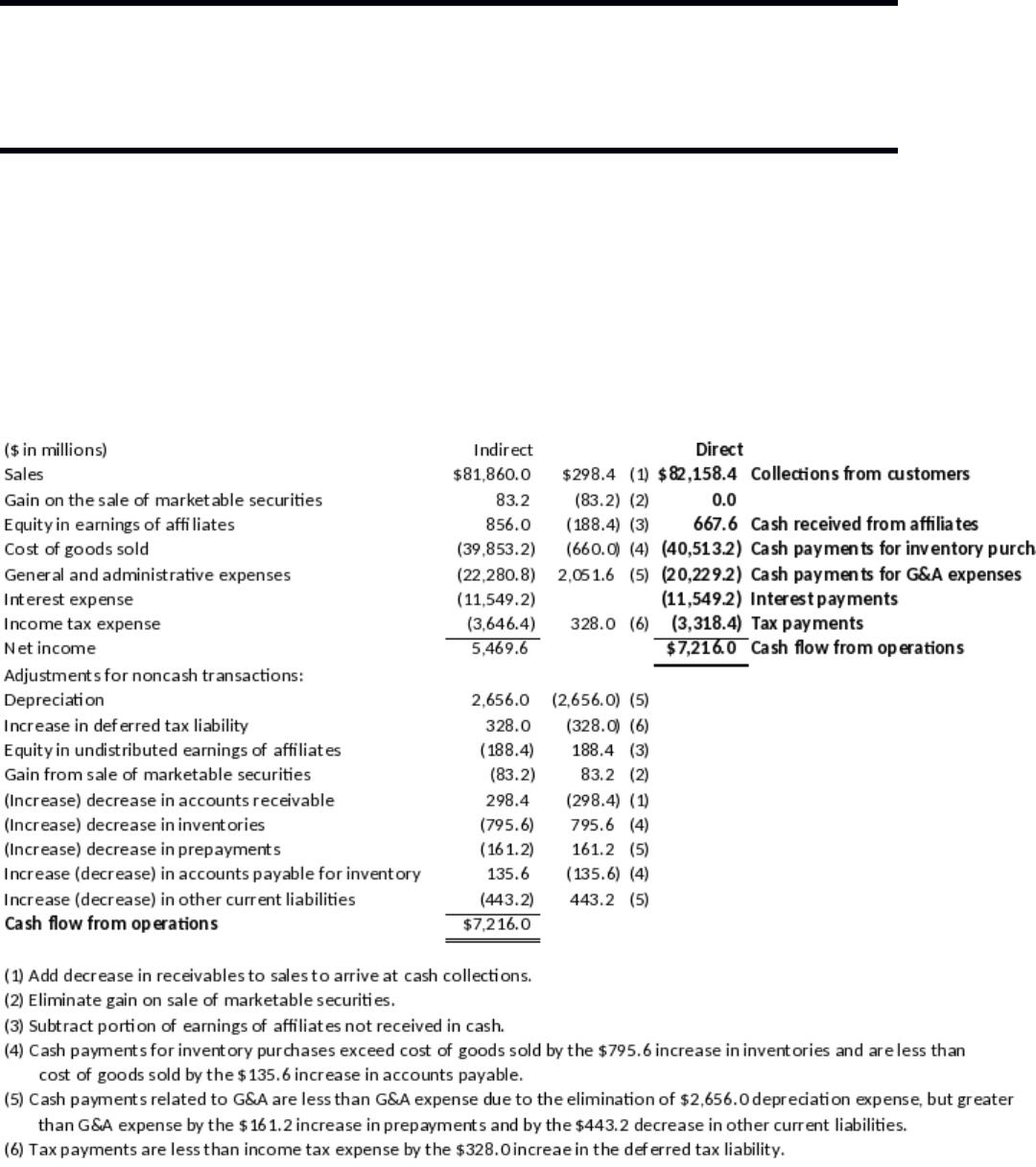

E17-1. Deriving a direct method presentation of cash flow from

operating activities

ABC Mining Company

Cash Flow from Operations

For the Year Ended December 31, 2017

E17-2. Determining cash flow from operating activities

(AICPA adapted)

Lino’s net cash from operating activities is calculated below:

1The increase in accounts receivable is net of the allowance for doubtful accounts.

E17-3. Calculating cash flows from operating activities, direct method

Cash flow from operating activities for Hamilton Corporation is

presented below:

Net cash provided by operating activities $109,800

Supporting calculations:

Cash paid to suppliers $207 ,000

4Cash paid for insurance:

E17-4. Determining cash collections from customers

The following analysis is to determine the amount of cash collected

on accounts receivable during 2017:

Accounts Receivable

Beginning balance $170,00

0$25,000 Write-offs

Total cash collected from customers $711,300

E17-5. Determining cash flows from investing and operating activities

(AICPA adapted)

Requirement 1:

Net income $300,000

+ Depreciation 52,000

– Gain on sale of equipment (5 ,000)

1Computation of cash from sale of equipment:

Cost of equipment $25,000

2Computation of cash paid for equipment:

Karr would also indicate with a supplemental disclosure that

$30,000 of equipment purchases were paid by issuance of a note.

E17-6. Determining cash flows from investing and financing activities

Requirement 1:

Requirement 2:

Dividends paid ($19,000)

E17-7. Determining cash flows from investing activities

(AICPA adapted)

Purchase of stock in Maybel ($26,000)

Net cash used in investing activities ($41 ,000)

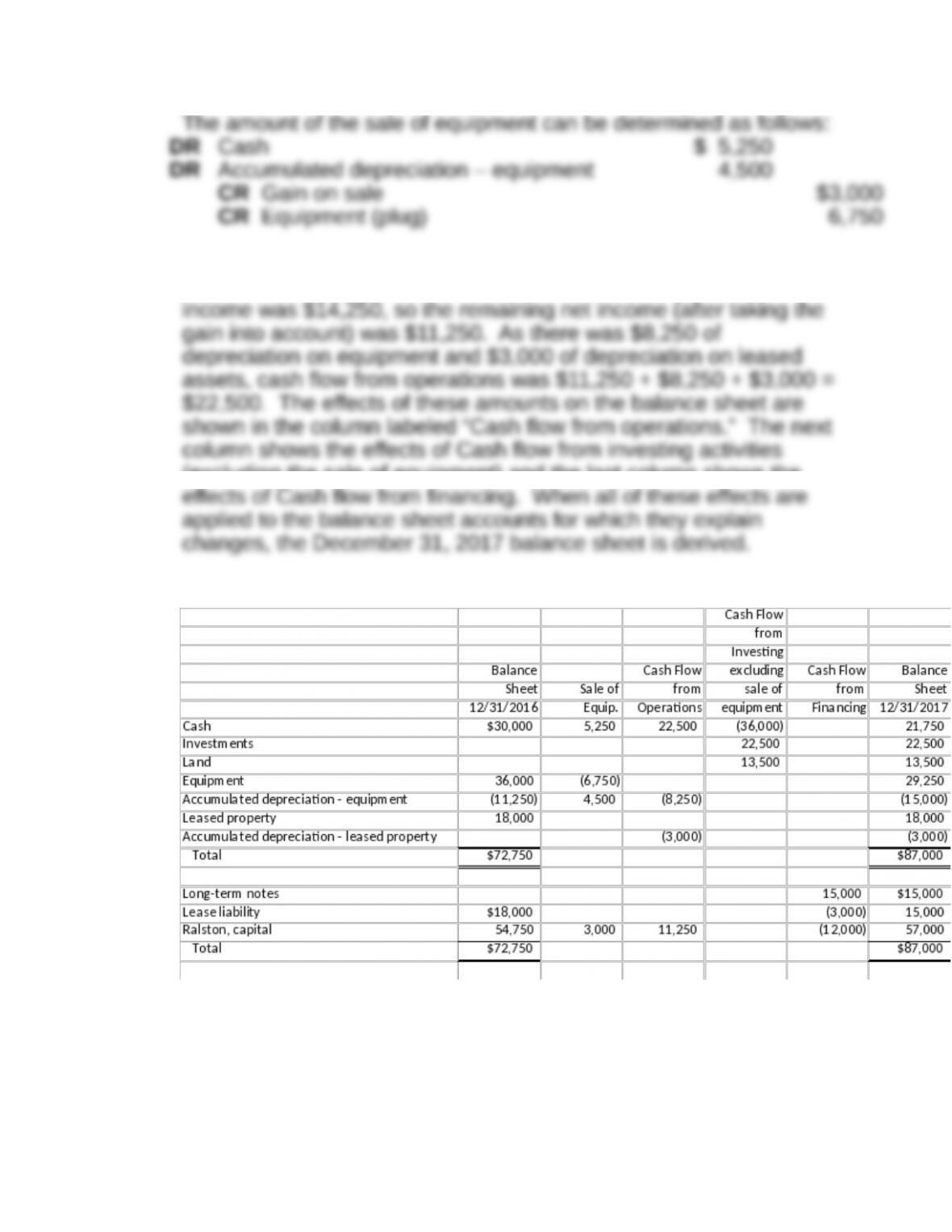

E17-8. Relationship between balance sheet and statement of cash

flows

Solution approach: The following journal entries can be derived

from the information given. Posting the entries then yields the

balance sheet found below.

The effects of this journal entry on the balance sheet are shown in

the “Sale of Equipment” column of the worksheet that follows. Net

(excluding the sale of equipment) and the last column shows the

E17-9. Determining operating cash flow

(AICPA adapted)

Net Income $150,000

Net cash provided by operating activities $144 ,900

E17-10. Statement of cash flows preparation

(AICPA adapted)

a) The dividend will not appear in Hoffman’s 2017 statement of

b) The stock repurchase will be listed as a financing outflow for

c) Because depreciation is a noncash expense, it requires no

operating cash and thus is not disclosed in a “direct method”

be listed among the reconciling items.

d) Net income is not an inflow or outflow of cash—nor is the

as well.) The inventory loss is a noncash expense because it

e) Neither the write-off of $20,000 nor the $35,000 bad debt

are reported “net,” the $35,000 will not serve as a reconciling

item as it is already picked up in the reconciling item for “change

in accounts receivable balance.”

f) The $100,000 cash paid for the building and land acquisition

disclosure may be via a separate section in the cash flow

statement.

g) Adding the machine’s book value ($25,000) to the realized gain

cash inflow.

E17-11. Determining cash used in financing activities

(AICPA adapted)

Net cash used in financing activities:

Net cash outflow ($356 ,000)

Note: The conversion of preferred stock to common stock is a

Financial Reporting & Analysis (7th Ed.)

Chapter 17 Solutions

Statement of Cash Flows

Problems

Problems

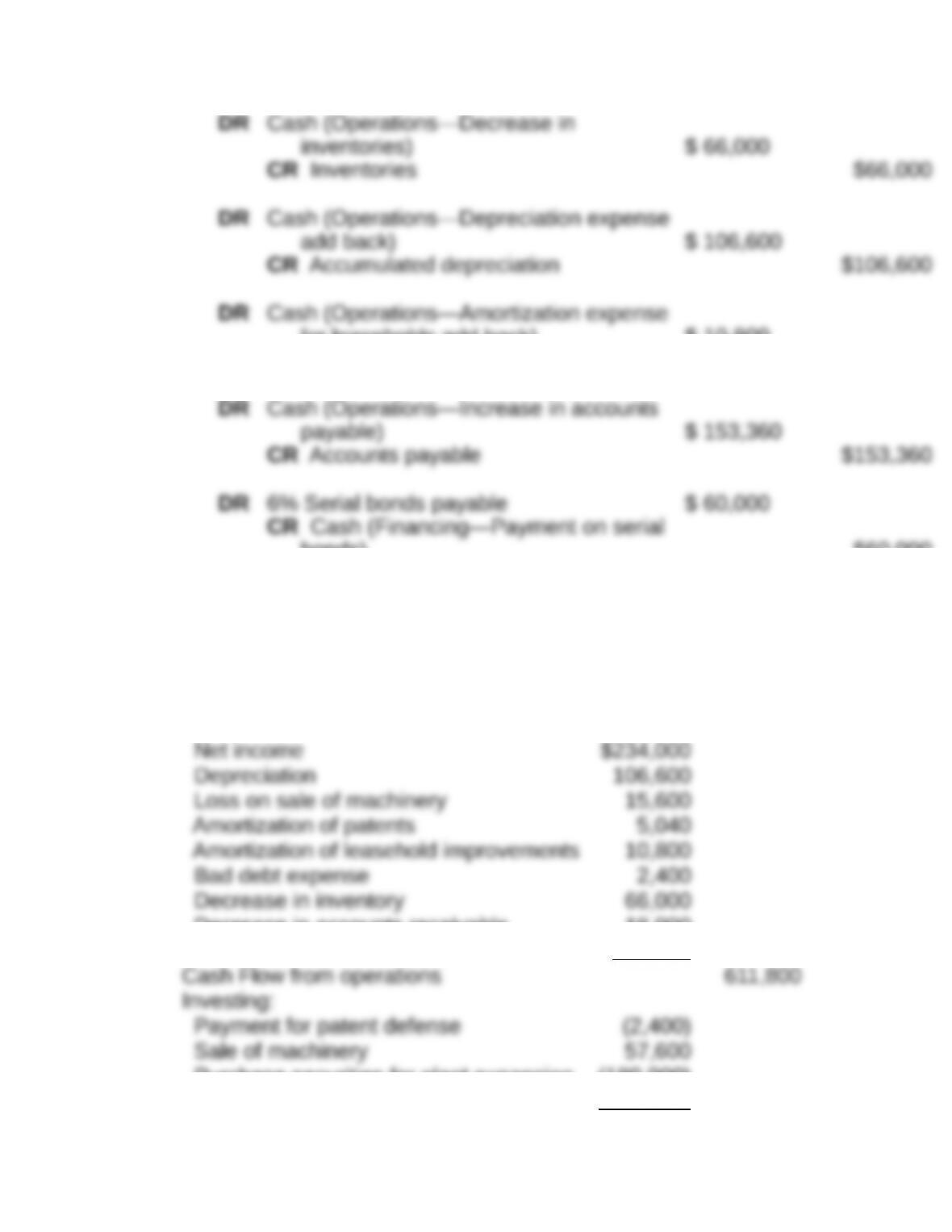

P17-1. Preparing a statement of cash flows under the indirect

method.

(AICPA adapted)

Requirement 1:

(a) DR Cash (Operations—Net income) $ 234,000

DR Machinery and equipment 463,000

CR Cash (Financing—retirement of

preferred stock $13,200

CR Accounts receivable $3,600

(g) DR Securities held for plant expansion $ 180,000

back) $ 2,400

CR Allowance for uncollectible accounts $2,400

for leaseholds add back) $ 10,800

CR Allowance for amortization $10,800

bonds) $60,000

Requirement 2:

Banciu Corporation

Statement of Cash Flows

For the Year Ending December 31, 2017

Operating:

Decrease in accounts receivable 18,000

Increase in accounts payable 153,360

Purchase securities for plant expansion (180,000)

Purchase machinery (463,000)

Cash Flow from Investing (587,800)

Financing:

Cash Balance, December 31, 2017 $174,000