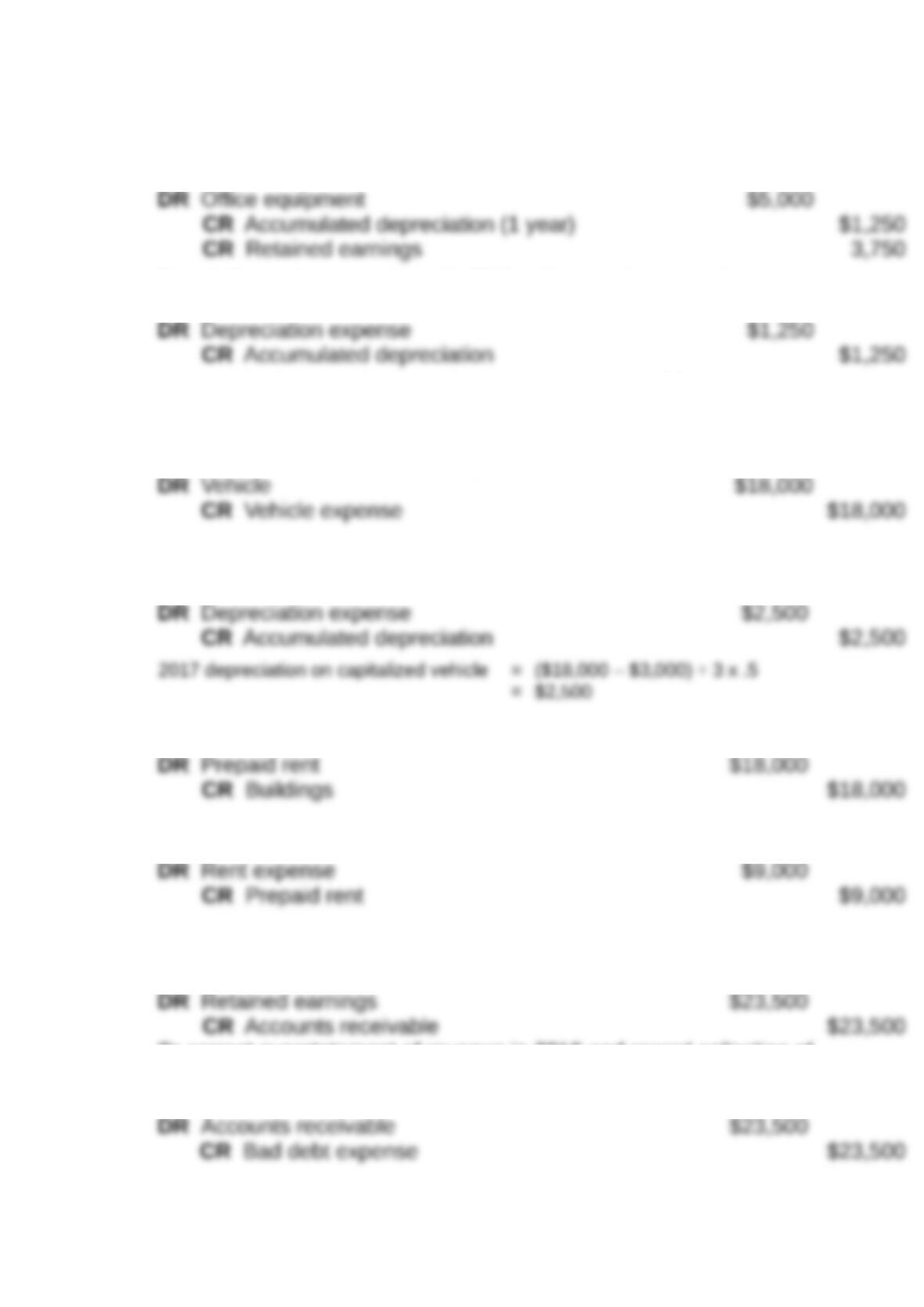

P2-14. Correcting errors

1) Correcting entries in 2017 for equipment improperly expensed in

2016:

To capitalize equipment purchased in 2016 and improperly expensed.

To record 2017 depreciation on equipment ($5,000 ÷ 4 = $1,250)

2) To capitalize vehicle improperly expensed in 2017:

To properly capitalize vehicle that was expensed when purchased.

3) To correct prepaid rent improperly charged to “Buildings” account:

To correctly record rent prepayment.

2017 adjusting entry to record use of warehouse for 6 months.

4) To correct error in accounting for receivables:

To correct overstatement of revenue in 2016 and record collection of

account receivable

2-1

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

To reverse improper write-off of account receivable in 2017.

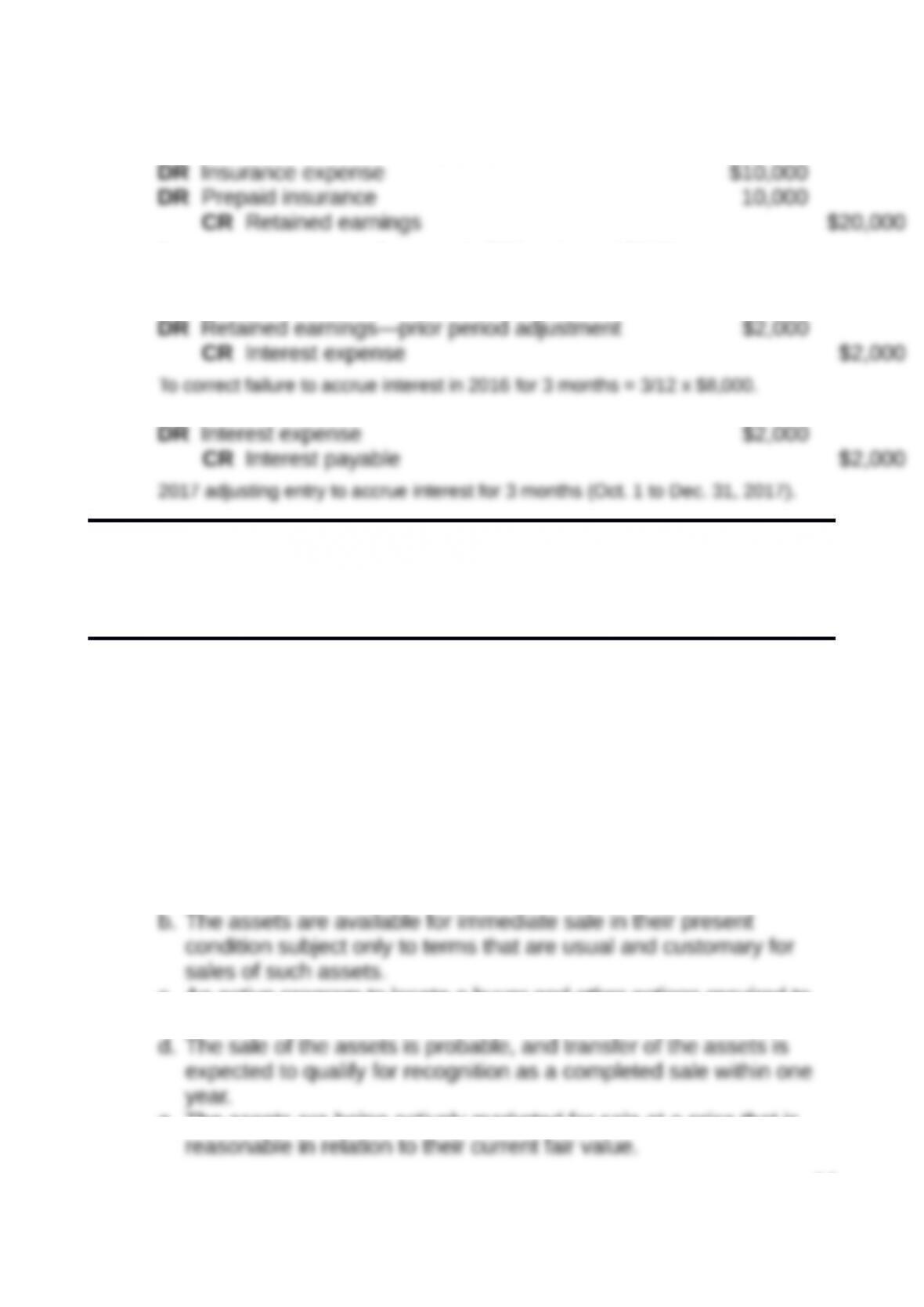

5) To correct error in recording prepaid insurance:

To correct overstatement of expense in 2016 and record 2017 insurance expense.

6) To record adjustment for failure to accrue interest expense in 2016:

Financial Reporting and Analysis (7th Ed.)

Chapter 2 Solutions

Accrual Accounting and Income Determination

Cases

Cases

C2-1. Conducting financial reporting research: Discontinued

operations

Requirement 1:

FASB ASC Paragraph 360-10-45-9 specifies the following criteria to

be met in order to classify assets as held for sale:

a. Management commits to a plan to sell the assets.

c. An active program to locate a buyer and other actions required to

complete the plan to sell the assets have been initiated.

e. The assets are being actively marketed for sale at a price that is

2-2

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

f. Actions required to complete the plan indicate that it is unlikely that

Requirement 2:

At issue is whether the regulatory approval delay violates the

requirement that assets be transferred within one year to qualify for

“held for sale” treatment. FASB ASC Paragraph 360-10-45-11 lists

several exceptions to the “one-year” requirement for completing the

Requirement 3:

The scenario for this requirement implies that management’s plans

have changed since the original disposal plan was adopted. Clearly,

the unit in question is no longer available for immediate sale. While it

is permissible to continue to classify assets as held for sale when

Requirement 4:

Corrpro’s net income would not be affected by denying discontinued

operations treatment to these business units. However, Corrpro has

suffered losses from continuing operations in each of the last three

C2-2. Retrospectively applying a change in accounting principle

2-3

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

Requirement 1:

Requirement 2:

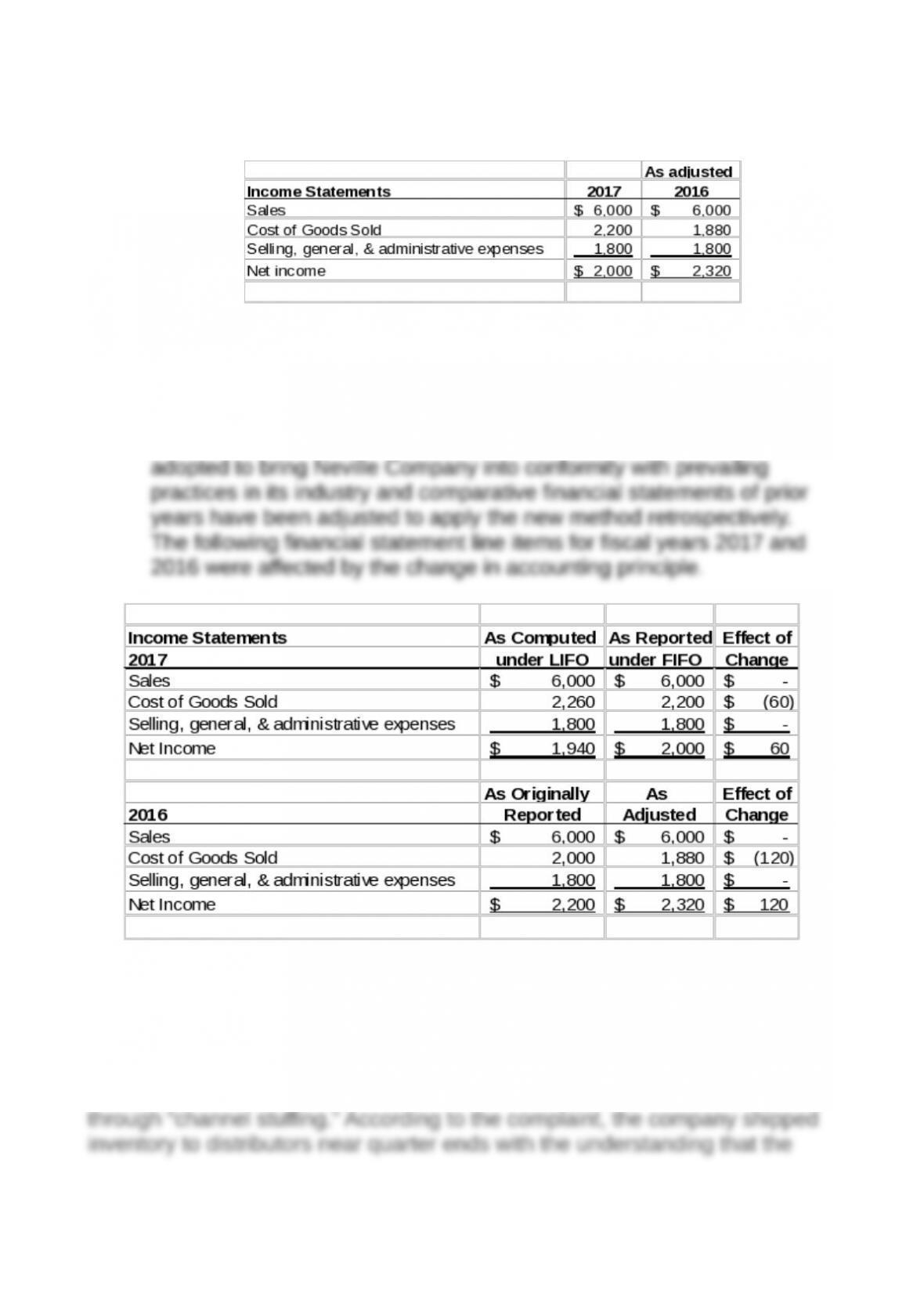

On January 1, 2017, Neville Company changed its method of valuing

its inventory to the FIFO method; in all prior years the LIFO method

was used to value inventory. The new method of accounting was

C2-3. Channel stuffing

Requirement 1

The Securities and Exchange Commission alleged that ClearOne improperly

recognized revenue, thus inflating net income and accounts receivable,

2-4

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

distributors did not have to pay for these products until the distributors resold

Physically transferring inventory to a distributor, but not requiring the

distributor to pay until the goods are resold, does not meet the criteria for

revenue recognition. This case pre-dates the new revenue recognition rules,

so the guiding principle would have been that the earnings process is

Requirement 2

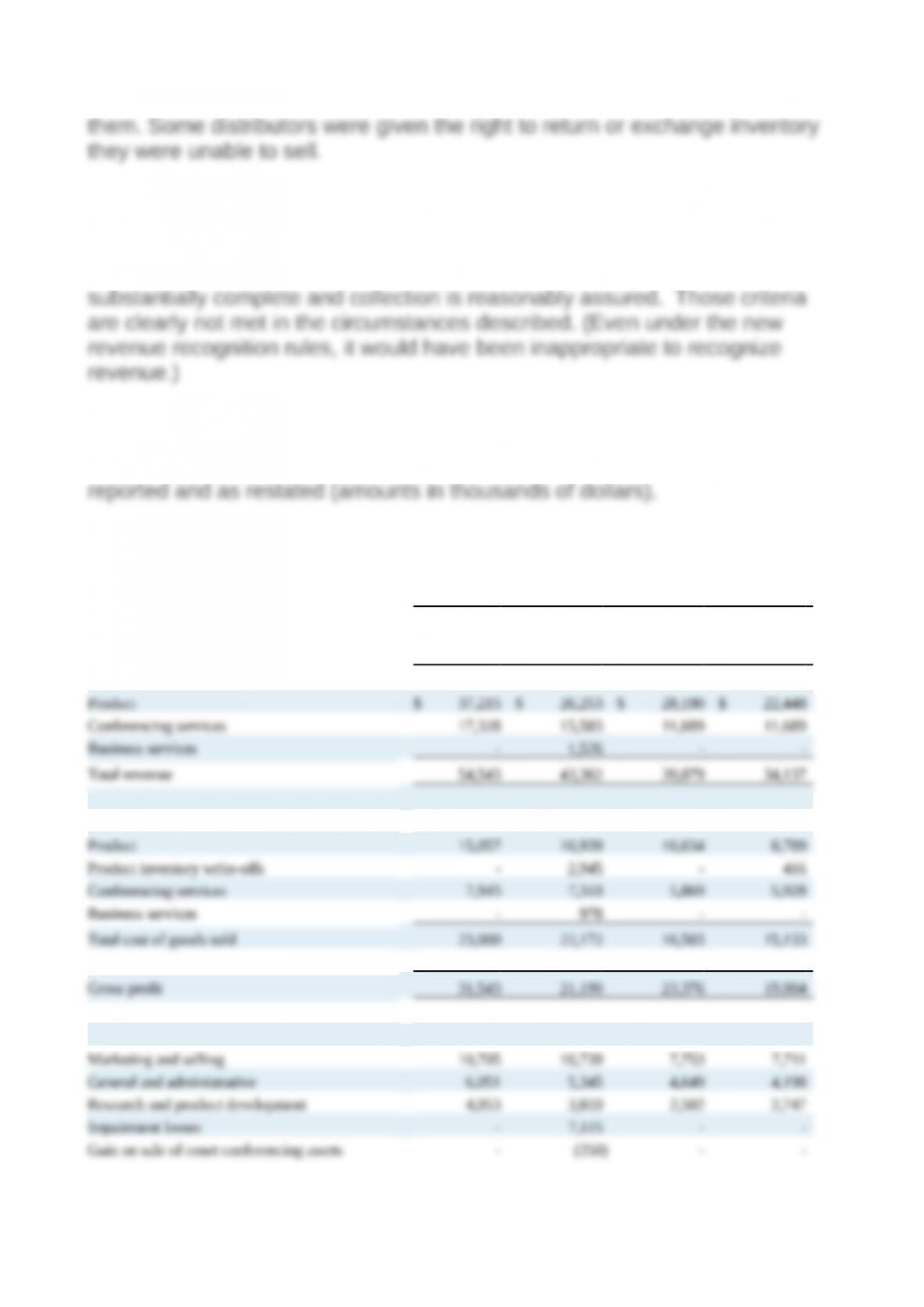

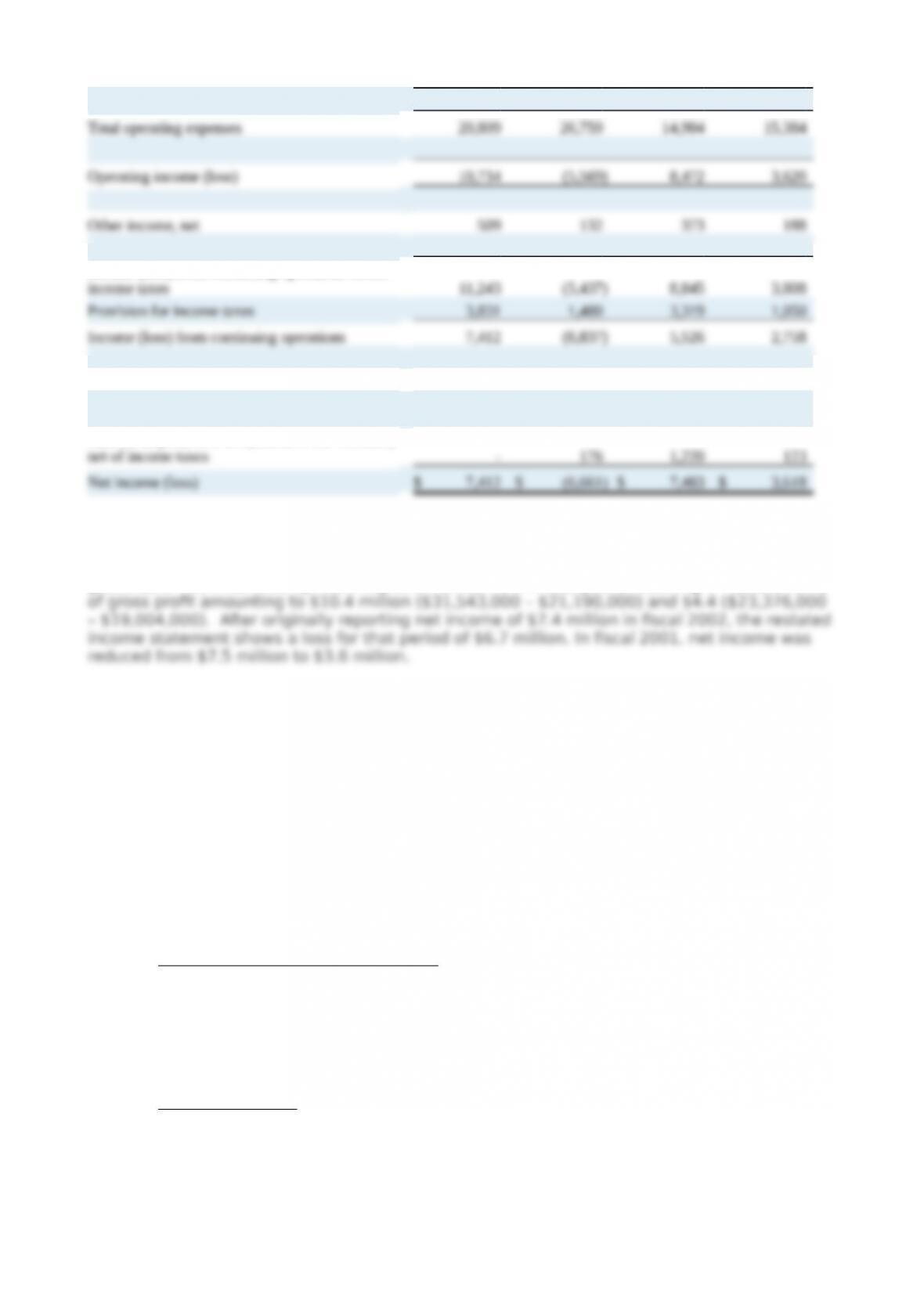

Following are the fiscal 2002 and 2001 income statements as originally

Impact on Consolidated Statements of Operations

As of June 30, 2002 As of June 30, 2001

As

Previously

Reported Restated

As

Previously

Reported Restated

Revenue:

Cost of goods sold:

Operating expenses:

2-5

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

Purchased in-process research and development – – – 728

Income (loss) from continuing operations before

Discontinued operations:

Income from discontinued operations, net of

income taxes – – 737 737

Gain on disposal of a component of our business,

ClearOne had overstated revenue by $11.2 million ($54,543,000 – $43,362,000) and $5.7

million ($39,879,000 – $34,137,000) in $scal 2002 and 2001, respectively. However, cost of

goods sold was misstated by relatively small amounts in those years, resulting in restatements

C2-4. Earnings management

The ethical issues involved are integrity and honesty in financial

reporting, full disclosure, and the accountant’s professionalism. In

violating GAAP, the Chief Accounting Officer also violated the AICPA’s

Code of Professional Conduct. Various parties were affected by the

conduct of the Chief Accounting Officer (and others in Mystery

Technologies management).

Honesty in financial reporting: Although estimates are pervasive in the

preparation of financial statements, accounts are expected to use their

best expectations in making those estimates, and are not permitted to

base estimates on desired reporting outcomes rather than beliefs

about the underlying economics.

Full disclosure: Accountants are expected to provide disclosures that

are sufficient to make the financial statements not misleading. Thus,

failing to disclose the over-reserve was a violation of securities laws.

2-6

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

Professionalism: Accountants are expected to act in the interests of

the financial statement users in order to provide faithful representation

of the firm’s economic situation. This requirement is inconsistent with

over-reserving in order to prop up subsequent period earnings

artificially.

Note to the instructor: Details of the SEC’s complaint against the

company this case is based on can be found at:

www.sec.gov/litigation/complaints/comp18194.htm

The Chief Accounting Officer pleaded guilty to criminal

charges based on his conduct at Mystery Technologies, the result

of which was various monetary penalties and the loss of future

employment opportunities.

Mystery Technologies, after an SEC investigation, was

charged with filing false and misleading financial statements.

Mystery Technologies’ auditors were named in shareholder

lawsuits filed as a result of the false and misleading financial

statements. The firm’s professional reputation cannot be enhanced

by the fact that the firm did not detect earnings management

schemes involving millions of dollars.

Investors in Mystery Technologies’ stock suffered. Note to

the instructor: By Year 0, Mystery Technologies’ stock had

climbed to over $40 per share where it more or less remained

before falling rapidly to the low teens in June of Year 1—about the

time that it became public that the SEC was investigating Mystery

Technologies’ reported earnings. (While this drop in share price

may have been purely the result of a down market at the time, suits

were filed that allege otherwise.)

The accounting profession suffers in the eyes of the public

whenever one of its members acts unprofessionally.

Employees of Mystery Technologies were placed in a

position where their superiors were pressuring them to engage in

unethical and/or illegal practices.

2-7

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.