Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

P8-12. Reconstructing T-accounts (LO 8-12)

Requirement 1:

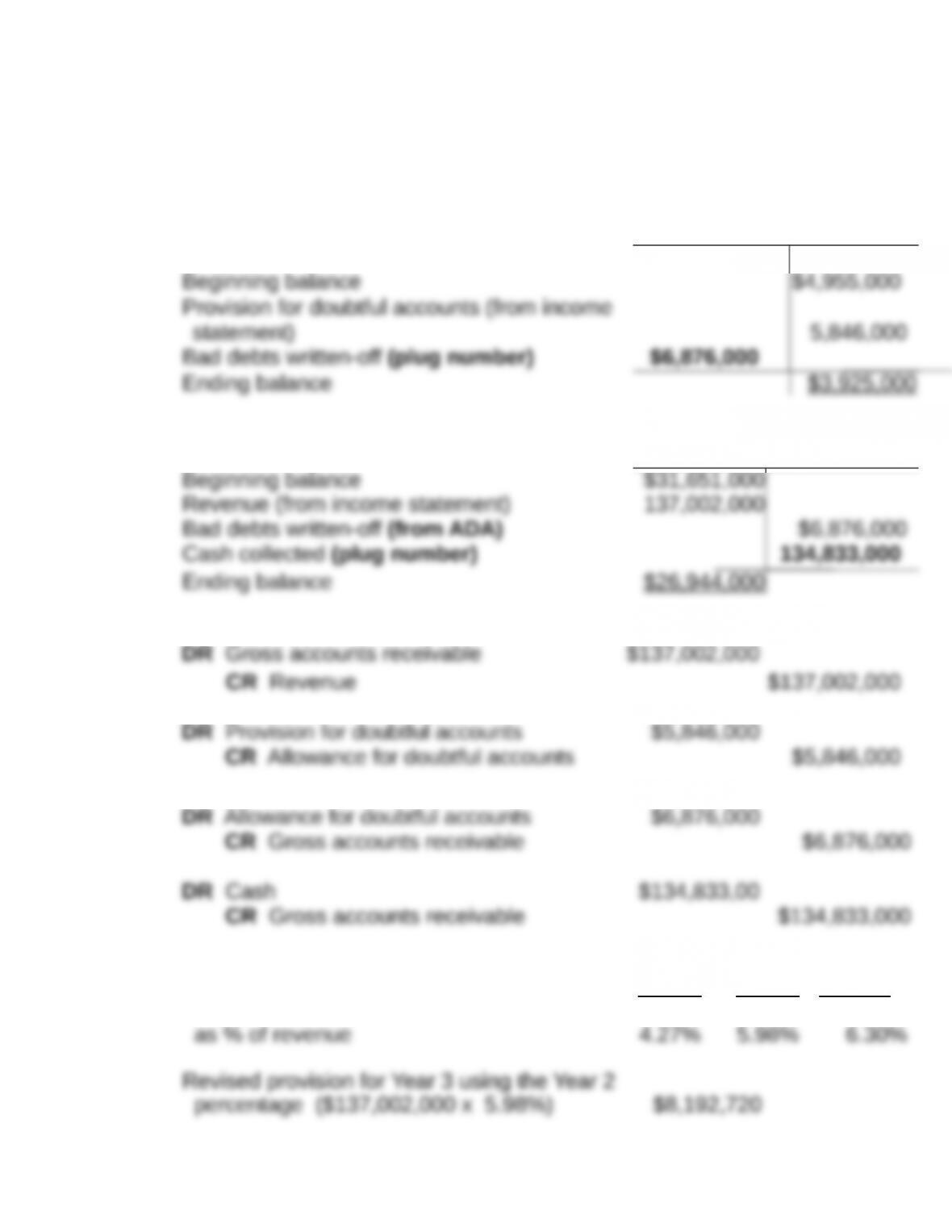

Allowance for doubtful

accounts

Gross accounts

receivable

Journal Entries

Requirement 2:

Year 3 Year 2 Year 1

Provision for doubtful accounts

DR CR

Allowance for doubtful accounts

Balance sheet presentation of receivables (Year 3)

Note: Altering the Year 3 provision for doubtful accounts does not

change gross accounts receivable.

The revised operating income is calculated below:

Year 3

Note that the operating income would have decreased by 34% if

Ramsay

had reported the Year 3 bad debts at the same percentage of

revenue

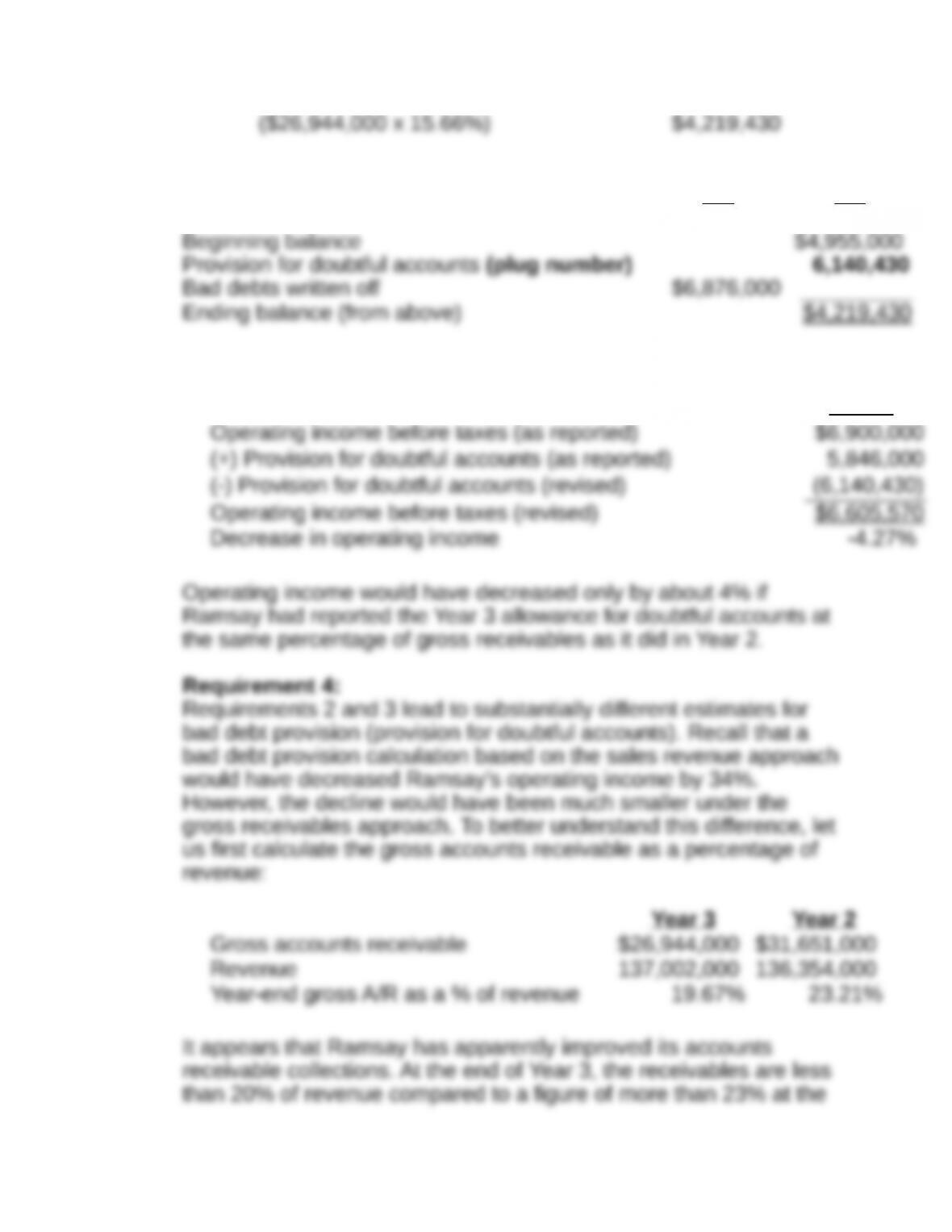

Requirement 3:

Year 3 Year 2

Revised balance in allowance account

DR CR

Allowance for doubtful accounts

The revised operating income is calculated below:

Year 3

Year 3

The above table suggests that Ramsay would have reported almost

$5 million of additional receivables at the end of Year 3 if the

receivables balance continued to be 23.21% of revenue. This

The intertemporal pattern of the bad debt provision is also

consistent with this intuition:

Year 3 Year 2 Year 1

Provision for doubtful accounts as

However, an analyst should obtain corroborating information from

the management to further substantiate this inference. This is

because the observed trend in the provision for doubtful accounts is

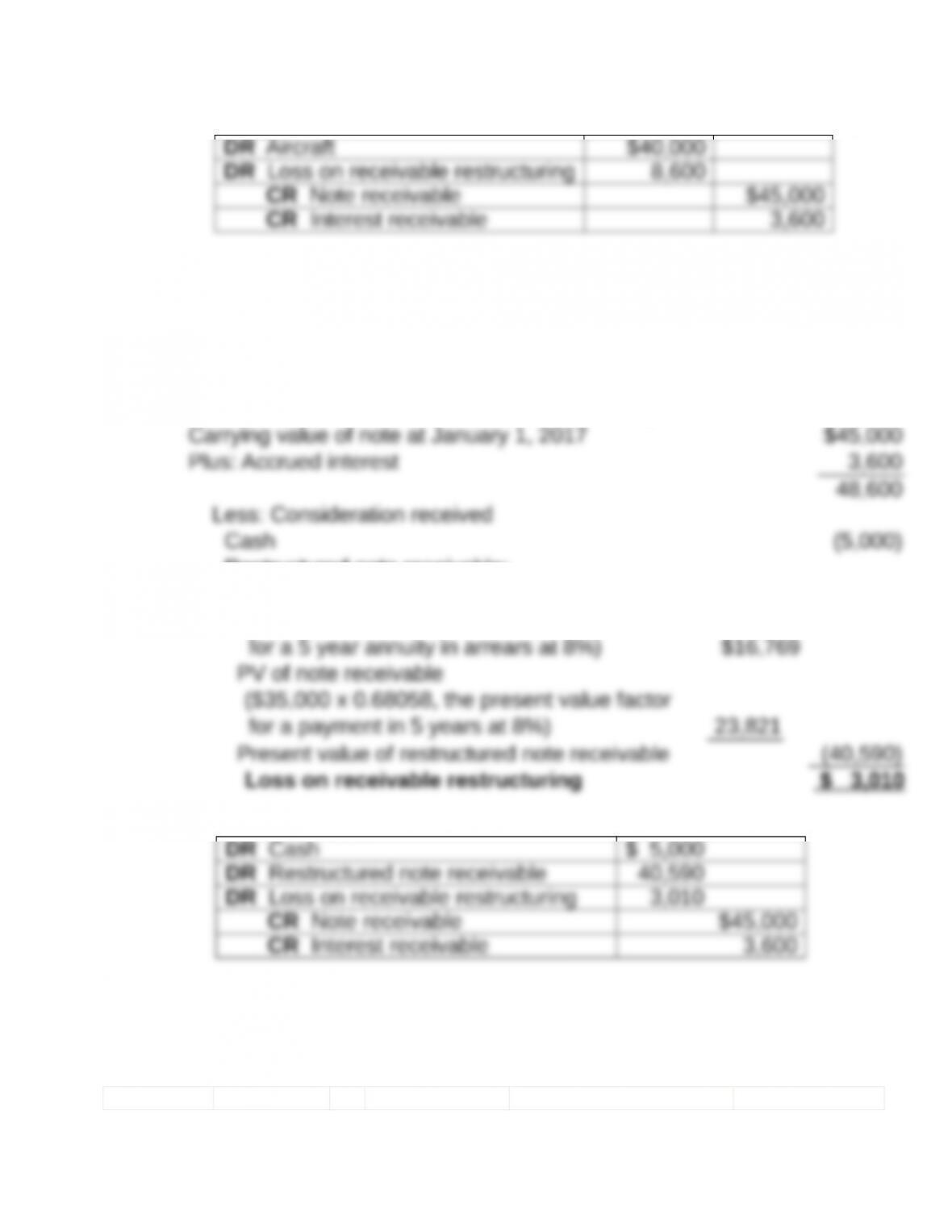

P8-13. Restructuring a note receivable (LO 8-8)

Requirement 1:

Settlement of note receivable by taking aircraft in exchange for note

receivable:

January 1, 2017:

No additional journal entries are required.

Requirement 2:

Restructuring of note receivable by taking cash and new note

receivable in exchange for original note receivable:

Calculation of Restructuring Loss

Restructured note receivable:

PV of interest payments

($4,200 x 3.99271, the present value factor

January 1, 2017:

Note Receivable Amortization Table

( a ) ( b ) ( c ) ( d )

Date Interest income:

[prior (d) x 8%]

Cash payment

received

(given)

Increase (decrease) in

Note receivable: [(a) -

(b)]

Note

receivable:

[prior (d) + (c )]

*rounded

December 31, 2017:

DR Cash $ 4,200

December 31, 2018:

DR Cash $ 4,200

December 31, 2019:

DR Cash $ 4,200

P8-14. Restructuring a note receivable (LO 8-8)

Requirement 1:

Mikeska Companies

1/1/14: To record the fully depreciated asset at its fair value:

DR Equipment

$12,000

CR Gain on disposal of asset $12,000

To record the settlement:

DR

Note payable

$72,000

DR

Interest payable ($72,000 x .05)

3,600

CR Cash

$30,000

CR Equipment

12,000

CR Gain on debt restructuring 33,600

Power-line Manufacturing

To record the settlement:

DR

Cash

$30,000

DR

Equipment

12,000

DR

Loss on receivable restructuring

33,600

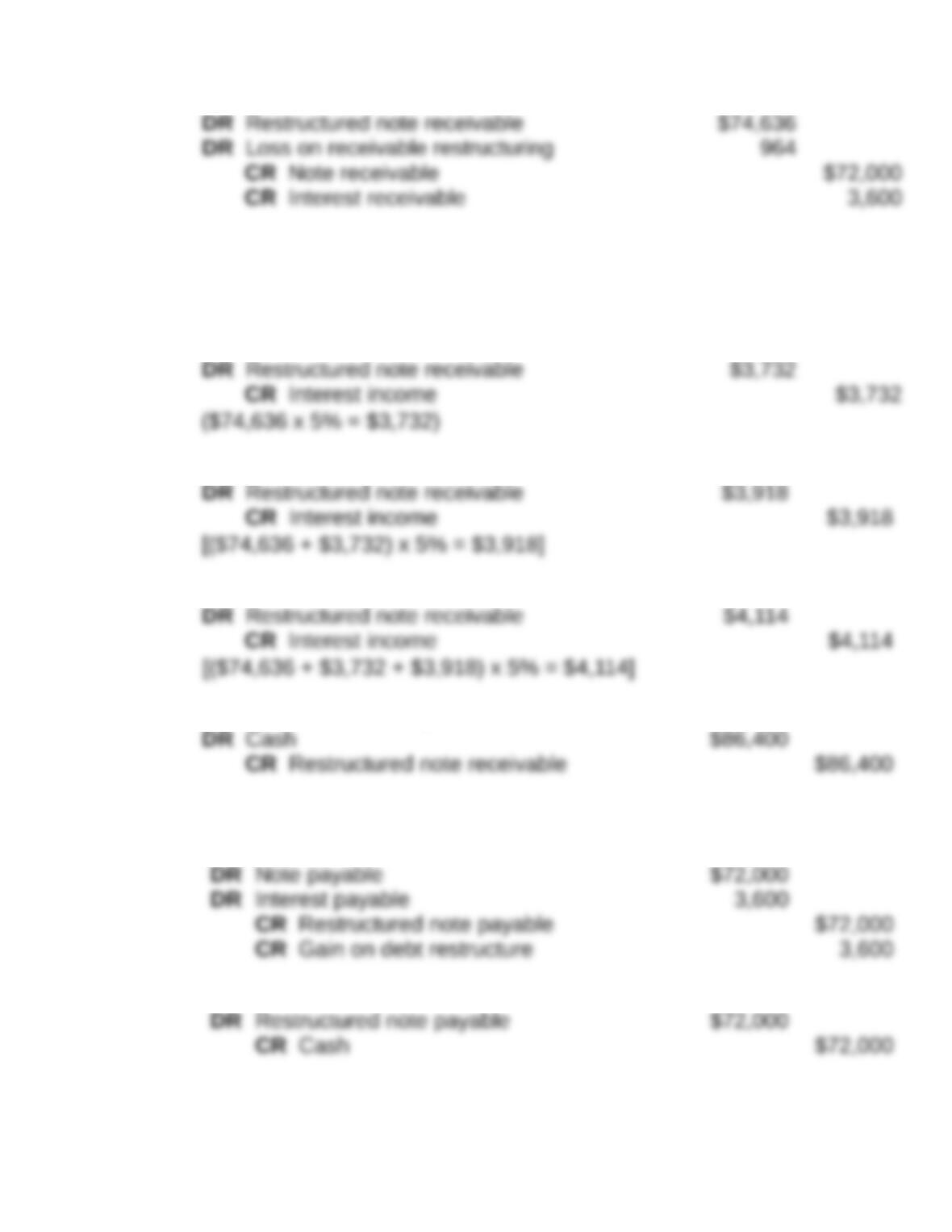

CR Note receivable

$72,000

CR Interest receivable 3,600

Requirement 2:

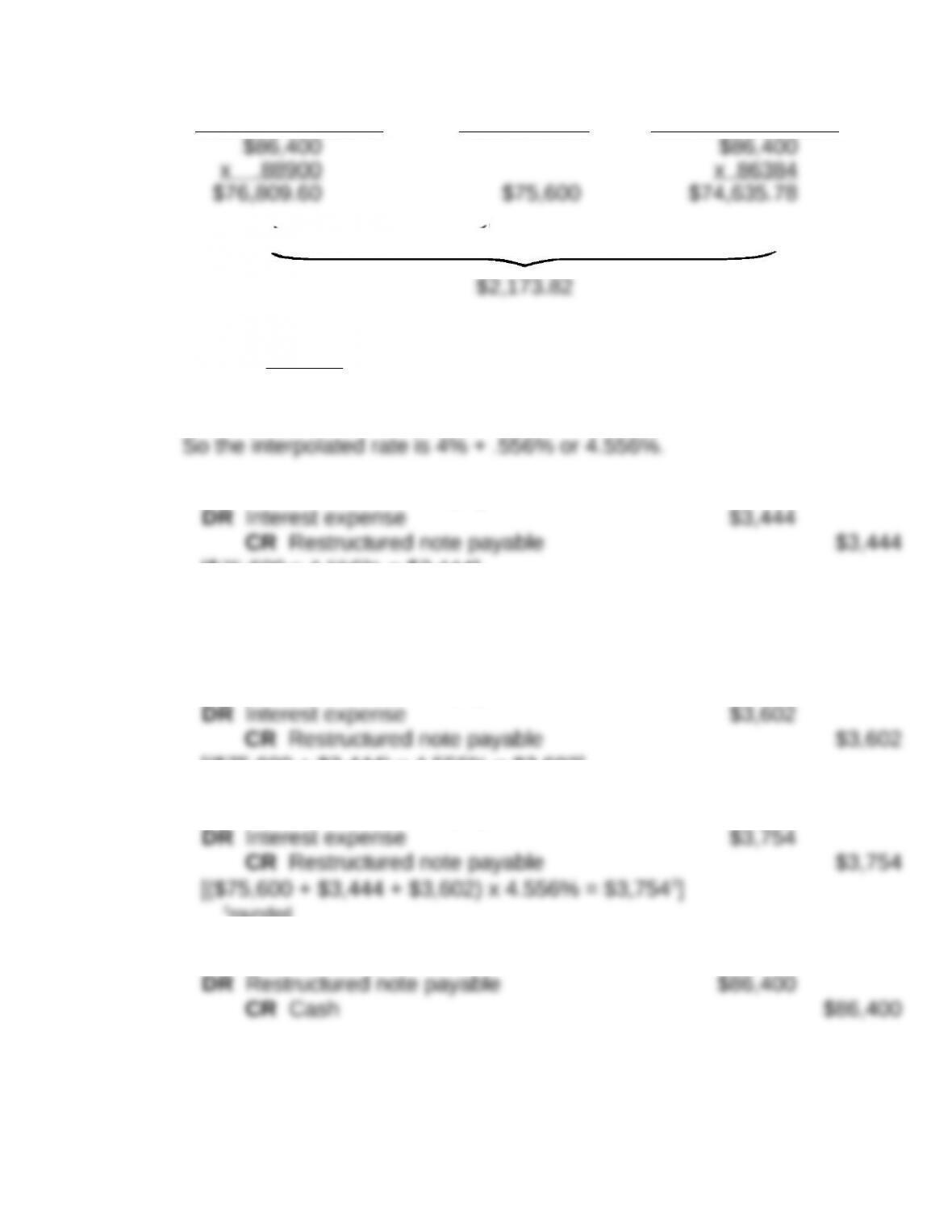

Mikeska Companies

1/1/14: To record the modified sum:

Calculation of Discount Rate:

Present value = future value x present value factor (3 years, ??

interest

rate) i.e., $75,600 = $86,400 x present value factor (3 years, ??

interest rate)

Dividing both sides by $86,400, we have

Alternately, this can also be obtained by interpolation.

Present value of Restructured Present value of

future flows @ 4% note amount future flows @ 5%

$1,209.60

Then,

82.173,2$

60.209,1$

= .556

So the interpolated rate is 4% + .556% or 4.556%.

12/31/14: To record interest payable:

[$75,600 x 4.556% = $3,444]

Interest expense is calculated at 4.556% of the book value of the

notes payable as of January 1, 2017.

12/31/18: To record interest payable:

[($75,600 + $3,444) x 4.556% = $3,602]

12/31/19: To record interest payable:

‡rounded

12/31/19: To record payment of amount due:

Power-line Manufacturing

1/1/17: To record the modified sum:

Note: The restructured note is valued at $74,636, the present value

of $86,400 to be received in three years discounted at 5%. The

factor is .86384.

12/31/17: To record interest receivable:

12/31/18: To record interest receivable:

12/31/19: To record interest receivable:

12/31/19: To record receipt of amount due:

Requirement 3:

Mikeska Companies

1/1/19: To record the modified sum:

12/31/19: To record payment of amount due:

Power-line Manufacturing

1/1/17: To record the modified sum:

Note: The restructured note is valued at $62,196, the present value

of $72,000 to be received in three years discounted at 5%. The

factor is .86384.

12/31/17: To record interest receivable:

[($62,196 + $3,110) x 5% = $3,265]

12/31/19: To record interest receivable: