File: Chapter 4 Structure of the Balance Sheet and Statement of Cash Flows

True/False

[QUESTION]

1. Liquidity refers to how quickly noncurrent assets will be converted into cash to pay

liabilities.

2. A common-size balance sheet presents each item as a percentage of total assets.

3. Companies having cash denominated in foreign currency units will not translate those

units into U.S. dollars because cash has the same value in all currencies.

4. Inventory and accounts receivable are both carried at net realizable value.

5. Deferred income taxes will be reported as either a noncurrent asset or noncurrent

liability.

6. It is permissible for a firm that reports in accordance with IFRS to emphasize its

liquidity by placing current assets and current liabilities in close proximity to one another

on the balance sheet.

7. A related party transaction occurs when a company enters a transaction with

individuals or other companies that are connected in some way with it or its management.

8. Events that occur after the financial statements are issued are referred to as subsequent

events.

9. The statement of cash flows shows the user why a firm’s investments and financial

structure have changed between two balance sheets dates.

10. The cash flow statement explains why a firm’s cash position has changed between

successive balance sheet dates while simultaneously explaining the changes that have

taken place in the firm’s noncash asset, liability, and stockholders’ equity accounts over

the same period.

11. Investing activities include the cash effects of selling stocks and bonds to raise capital

to purchase fixed assets.

12. Depreciation is added back to net income to determine cash from operating activities

under the indirect method.

13. Under the direct method for cash flow statement preparation, net cash flows from

operating activities is calculated by adjusting net income for the differences between

accrual-basis revenues and expenses and cash inflows and outflows during the period.

14. Under U.S. GAAP, cash interest from investments is reported on the statement of

cash flows as part of investing activities whereas under IFRS, cash interest from

investments is reported as part of financing activities.

15. When adjusting accrual earnings to obtain cash flows from operations, an increase in

Prepaid Rent Expense is subtracted to arrive at cash flow from operations.

Multiple Choice

[QUESTION]

16. Probable future economic benefits obtained or controlled by an entity as a result of

past transactions or events defines

a. assets.

b. liabilities.

c. equity.

d. retained earnings.

17. The residual interest in the resources of an entity that remains after deducting its debts

to third parties defines

a. assets.

b. liabilities.

c. equity.

d. retained earnings.

18. Probable future sacrifices of economic benefits arising from an entity’s present

obligations to transfer resources or provide services to other entities in the future as a

result of past transactions or events defines

a. assets.

b. liabilities.

c. equity.

d. retained earnings.

19. The balance sheet provides information on all of the following except

a. how management invested its money.

b. where the money came from.

c. assessing rates of return.

d. the market price of the company’s stock.

20. Contributed capital might be a negative dollar amount because

a. net losses exceeded net income over the years.

b. excess liabilities reduced contributed capital.

c. treasury stock was in excess of stock originally issued.

d. dividends paid were in excess of net income accumulated in retained earnings.

21. Accrued liabilities represent

a. income that has not yet been recognized on the income statement.

b. expenses that have not yet been recognized on the income statement.

c. expenses that have been recognized on the income statement but not yet been paid.

d. income that has been recognized on the income statement but not yet collected.

22. Balance sheet amounts would not be measured as

a. effective value.

b. fair value.

c. present value.

d. historical cost value.

23. Goodwill arising from a business combination is reported on the balance sheet as a(n)

a. current asset.

b. fair value asset.

c. impaired asset.

d. intangible asset.

24. Balance sheets prepared in other countries using international accounting standards

(IFRS) might use different account titles than are allowed for US. GAAP, such as

a. Capital reserve.

b. Share premium.

c. Hedging reserve.

d. all of these answer choices might be used in balance sheets prepared using IFRS.

25. Balance sheets prepared in compliance with U.S. GAAP reflect a mixture of

a. historical cost and future cash values.

b. current value and discounted future cash flows.

c. discounted cash flows and future values.

d. historical cost, fair value, net realizable value, and discounted present values.

26. Current assets are assets expected to

a. be converted to cash within twelve months.

b. be converted to cash within twelve months or one operating cycle if the operating cycle

is longer than twelve months.

c. remain on the books for at least twelve months.

d. remain on the books for at least twelve months or one operating cycle if the operating

cycle is longer than twelve months.

27. Cash is always measured for the balance sheet at

a. future transaction value.

b. current market value.

c. realizable future value.

d. net transaction value.

28. Joe Carie, head accountant, is using the indirect method and the account balance

from the balance sheet and income statement to prepare a statement of cash flows. He

notices that the Retained Earnings account increased from the beginning of the year. This

information is used to

a. increase cash flow from financing as it indicates receipt of payments from customers.

b. decrease cash flow from investing as it indicates payment of debt.

c. increase cash flow from operations as it signifies a net income.

d. decrease cash flow from operations as it indicates a net loss.

29. Joe Carie, head accountant, is using the indirect method and the account balance

from the balance sheet and income statement to prepare a statement of cash flows. Joe

would use an increase in Accumulated Depreciation to

a. increase cash flow from operating activities.

b. increase cash flow from investing activities.

c. decrease cash flow from investing activities.

d. decrease cash flow from operating activities.

30. Joe Carie, head accountant, is using the indirect method and the account balance

from the balance sheet and income statement to prepare a statement of cash flows. An

increase in the Computer Equipment account would

a. decrease cash flow from financing activities.

b. decrease cash flow from investing activities.

c. increase cash flow from operating activities.

d. decrease cash flow from investing activities.

31. Joe Carie, head accountant, is using the indirect method and the account balance

from the balance sheet and income statement to prepare a statement of cash flows. A

decrease in the balance of the Accounts Receivable account would

a. decrease cash flow from financing activities.

b. increase cash flow from investing activities.

c. decrease cash flow from operating activities.

d. increase cash flow from operating activities.

32. Net property, plant and equipment are reported on the balance sheet at

a. current market value.

b. historical cost.

c. historical cost minus accumulated depreciation.

d. net realizable value.

33. Current liabilities are reported on the balance sheet at

a. current market value.

b. historical cost.

c. discounted present value.

d. future value.

34. Long-term debt is reported on the balance sheet at

a. current market value.

b. net realizable value.

c. present value.

d. future value.

35. Cash interest from investments is recorded as _______ in statements of cash flows for

U.S. GAAP, but can be recorded as ________ when using IFRS.

a. cash flows from investing activities / cash flows from financing activities

b. cash flows from financing activities / cash flows from operating activities

c. cash flows from operating activities / cash flows from financing activities

d. cash flows from operating activities / cash flows from investing activities

36. Balance sheets developed under US GAAP

a. may, but are not required to, list assets from most liquid to least liquid.

b. must list assets from most liquid to least liquid.

c. must list assets from least liquid to most liquid.

d. must list assets in alphabetical order.

37. Balance sheets prepared under IFRS

a. may list assets and liabilities from least liquid to most liquid.

b. must list assets, but not liabilities in order of liquidity.

c. must list assets and liabilities from least liquid to most liquid.

d. must list liabilities, but not assets, from most to least liquid.

38. The Common Stock account is reported on the balance sheet at the

a. par value of the stock.

b. current market value of the stock.

c. net realizable value of the stock.

d. discounted present value of the future dividends.

39. The Additional Paid-In Capital account is reported on the balance sheet at the

a. current market value of the stock minus par value.

b. original sales price of the stock minus the par value.

c. net realizable value of the stock minus par value.

d. discounted present value of the future dividends minus par value.

40. The Retained Earnings account is comprised of

a. cash retained in the business.

b. cash reinvested in the business by shareholders.

c. the cumulative earnings less dividends since the inception of the corporation.

d. the earnings of the corporation for the current year.

41. Retained earnings are reported on the balance sheet at

a. historical cost.

b. current market value.

c. net realizable value.

d. a mixture of different measurement bases.

42. In a common-size balance sheet, each balance sheet account is expressed as a

percentage of total

a. liabilities.

b. assets.

c. shareholders’ equity.

d. assets plus shareholders’ equity.

43. Common-size balance sheets may be used for all the following except

a. gaining insights into the nature of a company’s operations.

b. analyzing a company’s asset and financial structure.

c. determining how management assesses the risks a company faces.

d. learning about the underlying economics of an industry.

44. Under U.S. GAAP, assets are presented in decreasing order of liquidity. Under IFRS,

a. tangible assets may be presented first followed by the current assets displayed in

increasing order of liquidity.

b. the current assets are displayed in increasing order of liquidity.

c. investments are listed first in descending order of maturity.

d. a company may present its assets in alphabetical order if it so desires.

45. The term “consolidated” is used in financial statements under U.S. GAAP to refer to

the financial reporting for a parent and its subsidiaries. The equivalent term used on

balance sheets in the United Kingdom is

a. cooperative.

b satellite.

c. consolidated.

d. group.

46. All the following disclosures would appear in the Summary of Significant

Accounting Policies except

a. inventory method.

b. depreciation method.

c. revenue recognition method.

d. financing method.

47. Notes to the financial statements typically contain all the following except

a. a summary of significant accounting policies.

b. disclosure of important subsequent events.

c. management’s discussion and analysis.

d. related-party transactions.

48. Which one of the following equations explains why successive balance sheets can be

used to prepare a firm’s cash flow statement?

a. Assets = Liabilities – Equity

b. Cash – Noncash assets = Liabilities – Equity

c. Cash = Liabilities – Noncash assets + Stockholders’ equity

d. Cash = Liabilities + Stockholders’ equity

49. The change in a firm’s cash position between successive balance sheet dates will not

equal the reported net income for that period for all the following reasons except:

a. Reported net income usually will not equal cash flow from operating activities because

noncash revenues and expenses are often recognized as part of accrual income.

b. Reported net income usually will not equal cash flow from operating activities because

certain operating cash inflows and outflows are not recorded as revenues or expenses

under accrual accounting in the same period the cash flows occur.

c. Changes in cash are also caused by nonoperating investing activities like the purchase

of treasury stock.

d. Additional changes in cash are caused by financing activities like the repayment of a

bank loan.

50. Operating activities result from the cash effects of

a. producing and delivering goods and services.

b. purchasing and disposing of fixed assets used in production of revenue.

c. borrowing and repaying loans used in the production of revenue.

d. selling stocks and bonds to raise capital for the generation of revenue.

51. Investing activities include the cash effects of

a. producing and delivering goods and services.

b. purchasing and disposing of productive assets used in production of revenue.

c. borrowing and repaying loans used to purchase equipment.

d. selling stocks and bonds to raise capital to purchase land.

52. Financing activities include the cash effects of

a. producing and delivering goods and services.

b. purchasing and disposing of productive assets used in production of revenue.

c. purchasing and disposing of debt securities of other companies.

d. selling stocks and bonds to raise capital used to produce revenue.

53. Cash flows from operating activities include:

a. cash payments received from customers.

b. increases in Accumulated Depreciation.

c. deferred income taxes.

d. All of these would be included in cash flows from operating activities.

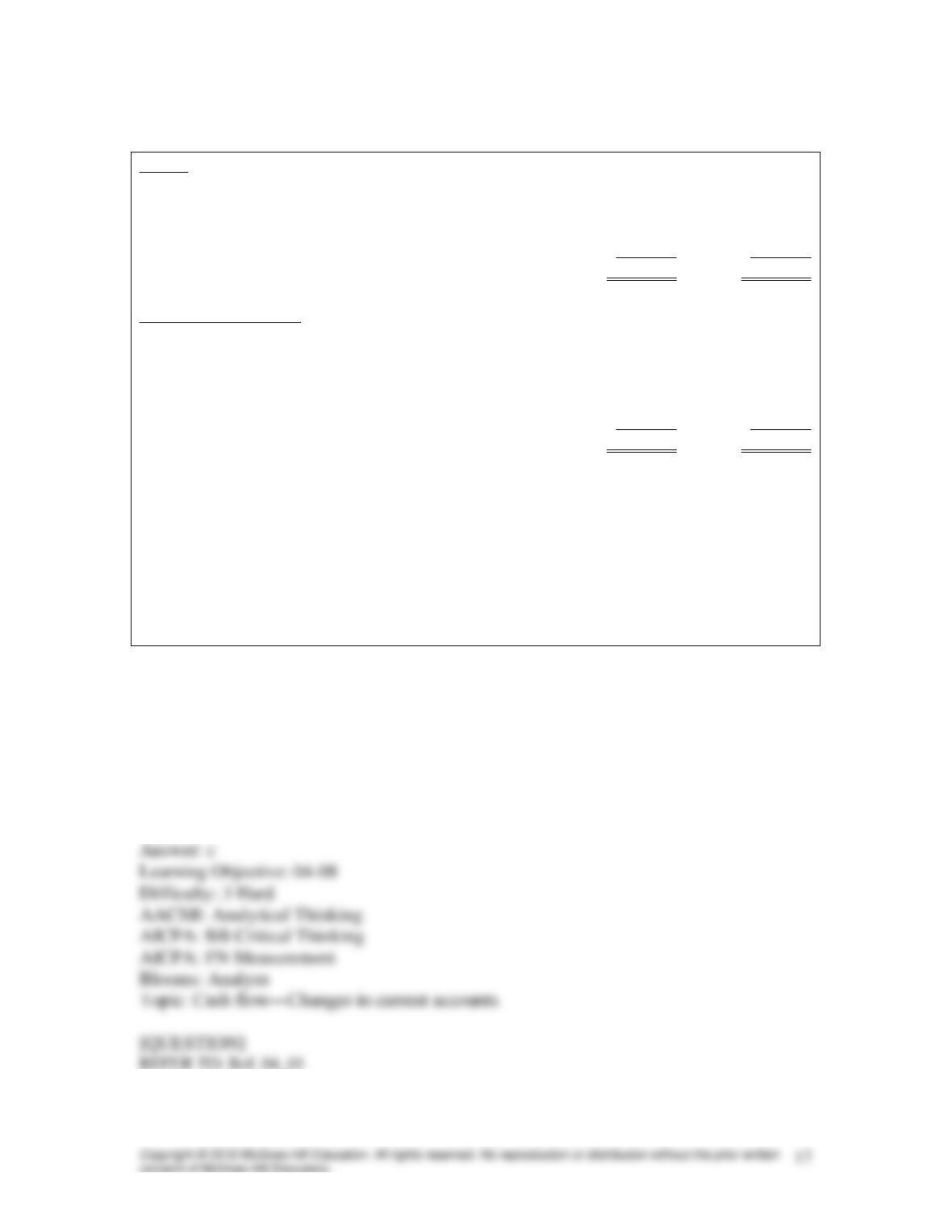

REFERENCE: Ref. 04_01

Selected data for Kris Corporation’s comparative balance sheets for Year 1 and Year 2

are as follows:

Assets

Year 1

Year 2

Cash

$100,000

$(50,000)

Accounts receivable (net)

50,000

100,000

Inventory

100,000

250,000

Equipment (net)

300,000

350,000

Total assets

$550,000

$650,000

Liabilities and Equity

Accounts payable

$150,000

$100,000

Income taxes payable

80,000

30,000

Bonds payable

100,000

80,000

Common stock

100,000

200,000

Retained earnings

120,000

240,000

Total liabilities and Equity

$550,000

$650,000

[QUESTION]

REFER TO: Ref. 04_01

54. Using the indirect method to create the operating activities section of the statement of

cash flows, the cash flow from accounts receivable would be recorded as

a. an increase of $50,000

b. an increase of $150,000

c. a decrease of $50,000

d. a decrease of $150,000

55. Using the indirect method to create the operating activities section of the statement of

cash flows, the cash flow recorded based on the change in inventory would be

a. a decrease of $400,000

b. an increase of $400,000

c. an increase of $150,000

d. a decrease of $150,000.

56. The change in the balance of the common stock account would be recorded on the

statement of cash flows as

a. an increase of $100,000 under financing activities.

b. an increase of $100,000 under investing activities.

c. an increase of $100,000 under operating activities.

d. an increase of $300,000 under financing activities.

57. The changes in the Accounts Payable balance would be recorded on the statement of

cash flows as

a. an increase of $50,000 under financing activities.

b. a decrease of $50,000 under financing activities.

c. an increase of $50,000 under operating activities.

d. an decrease of $50,000 under operating activities.

58. The change in the equipment balance would be recorded on the statement of cash

flows as

a. a decrease of $50,000 under investing activities.

b. am increase of $50,000 under investing activities.

c. a decrease of $150,000 under investing activities.

d. an increase of $150,000 under operating activities.

59. The change in the balance of the Bonds Payable account would be recorded on the

statement of cash flows as

a. an increase of $20,000 under financing activities.

b. an increase of $80,000 under investing activities.

c. a decrease of $20,000 under financing activities.

d. a decrease of $80,000 under operating activities.

60. Which of the following statements is not true?

a. The indirect method begins with net income.

b. Cash flows from operating activities will differ between the direct and indirect

methods.

c. Most firms use the indirect method to prepare the statement of cash flows.

d. The direct method presents cash inflows and outflows.

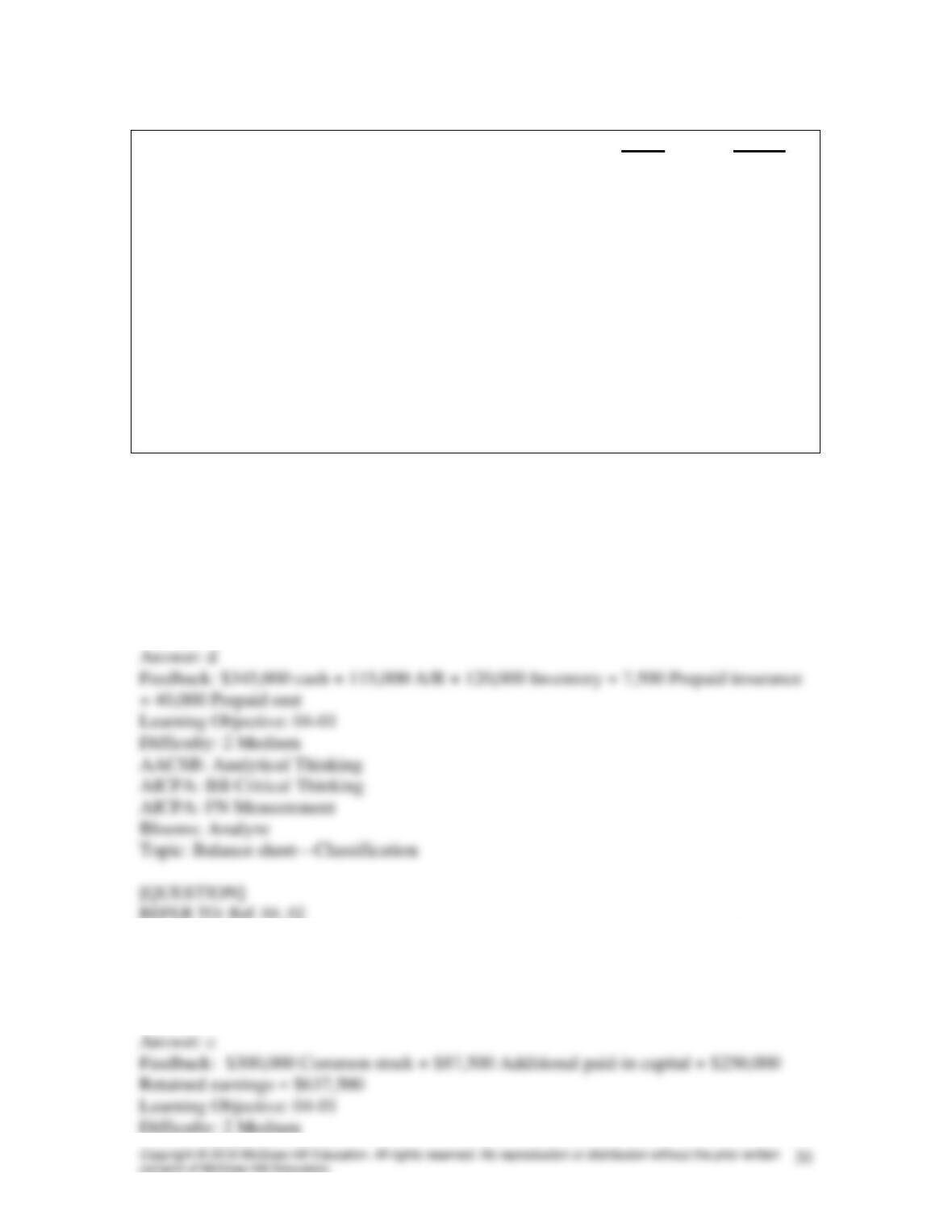

REFERENCE: Ref. 04_02

The Barden Company provides the following trial balance as of December 31, 2018.

Debit

Credit

Cash and cash equivalents

Accounts receivable

$345,000

115,000

Inventory

120,000

Prepaid insurance

7,500

Prepaid rent

Equipment

Accumulated depreciation – Equipment

40,000

265,000

65,000

Accounts payable

Accrued liabilities

Notes payable, due in 2020

Common stock

Additional paid-in capital

Retained earnings

Total

$892,500

45,000

10,000

135,000

300,000

87,500

250,000

$892,500

[QUESTION]

REFER TO: Ref. 04_02

61. What would Barden report as current assets on its balance sheet?

a. $460,000

b. $580,000

c. $892,500

d. $627,500

62. What would Barden report as total stockholders’ equity on its balance sheet?

a. $300,000

b. $387,500

c. $637,500

d. $87,500