P12-4. Recording operating lease and comparing to finance lease

treatment under ASU 2016-02 (ASC 842) (LO 12-6)

Part 1 – Lease classification

Part 2 – Amortization table

(A) (B) ( C) (D)

Interest Principal

Date Payment Expense Reduction Balance

.09 x prior (D) (A) – (B) Prior (D) – ( C)

*Rounded.

Requirement 3 – Journal entries

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 12-1

January 1, 2017 January 1, 2018

December 31, 2017 December 31, 2018

aPrincipal reduction from amortization table. Because the payments are the same each year, the amount

for amortization equals the principal reduction in the next lease payment to be made one day later but

which occurs in the next fiscal year. Interest is for year 2017 and the next payment is made in advance

for 2018.

Requirement 4 – Financial statement effects for operating lease

Balance Sheet

Assets December 31

2017 2018

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 12-2

(lease obligation in amortization table after the next

cash payment)

Requirement 5 – Financial statement effects for a finance lease

31-Dec

Balance Sheet 2017 2018

Assets

Income Statement

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 12-3

(Finance lease expense less operating

lease expense) [The amount of income

statement difference in each year

accumulates to the total difference on

the balance sheet: 9,559 + 6,822 =

16,381. At the end of the lease term, the

accumulated difference would be zero.]

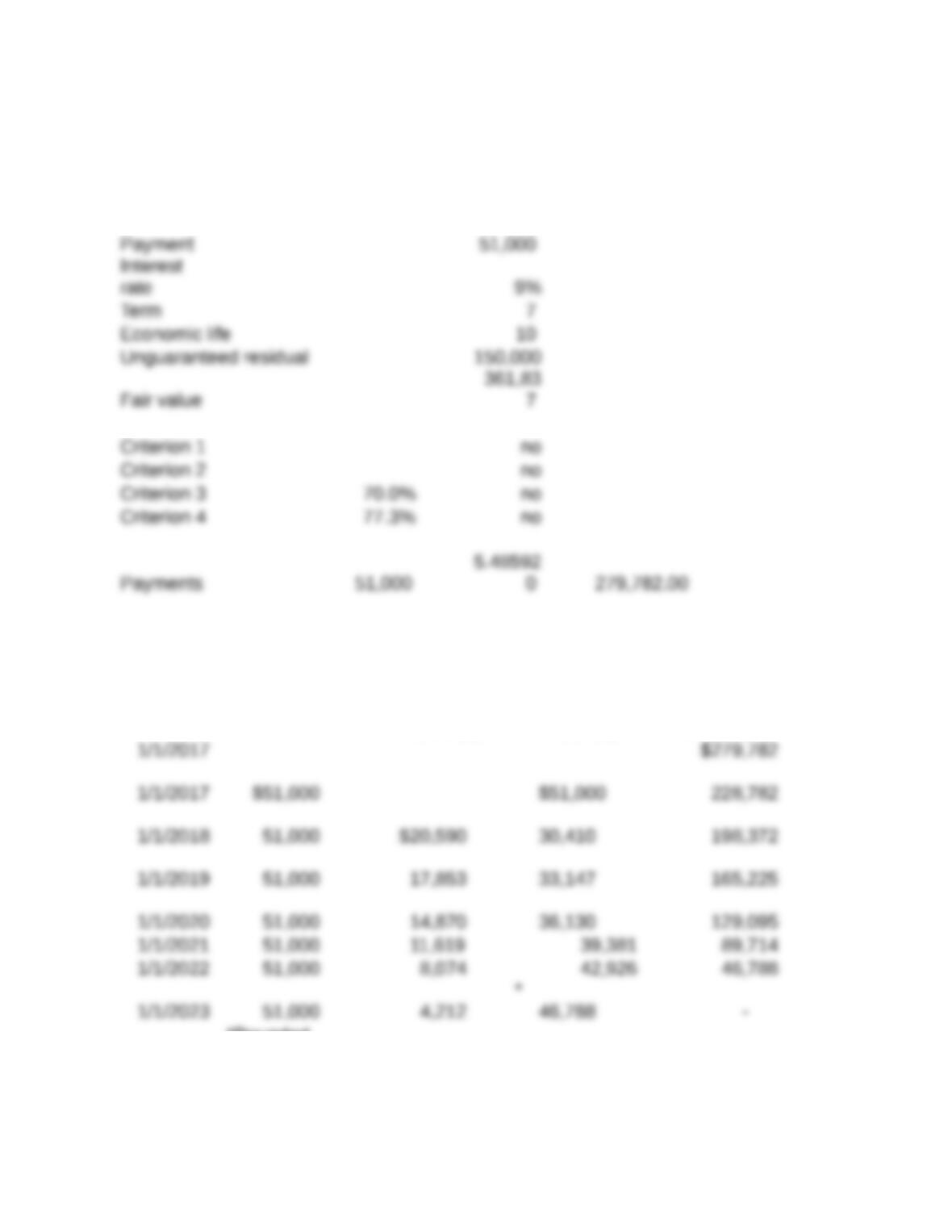

P12-5. Accounting for lessee finance lease including executory costs

and residual value guarantee under ASU 2016-02 (ASC 842) (LO

12-9)

Requirement 1:

This is a finance lease to Bare Trees Company because the lease

term of

3 years is equal to 75% of the asset’s useful life of 4 years.

(The $59,258.09 figure is the $62,258.09 annual lease payment minus the $3,000

annual executory costs).

Appearing below is the amortization schedule for the lease liability:

Amortization of Capital Lease Liability

Bare Trees Company

($15,000 Guaranteed Residual Value)

Interest Cash Liability Lease

Date Portion1Payment2Reduction3Liability4

1/1/17 $161,582.11

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 12-4

*Rounded by $0.05.

1 The interest portion is 9% of the carrying amount at the beginning of the

period.

reduction.

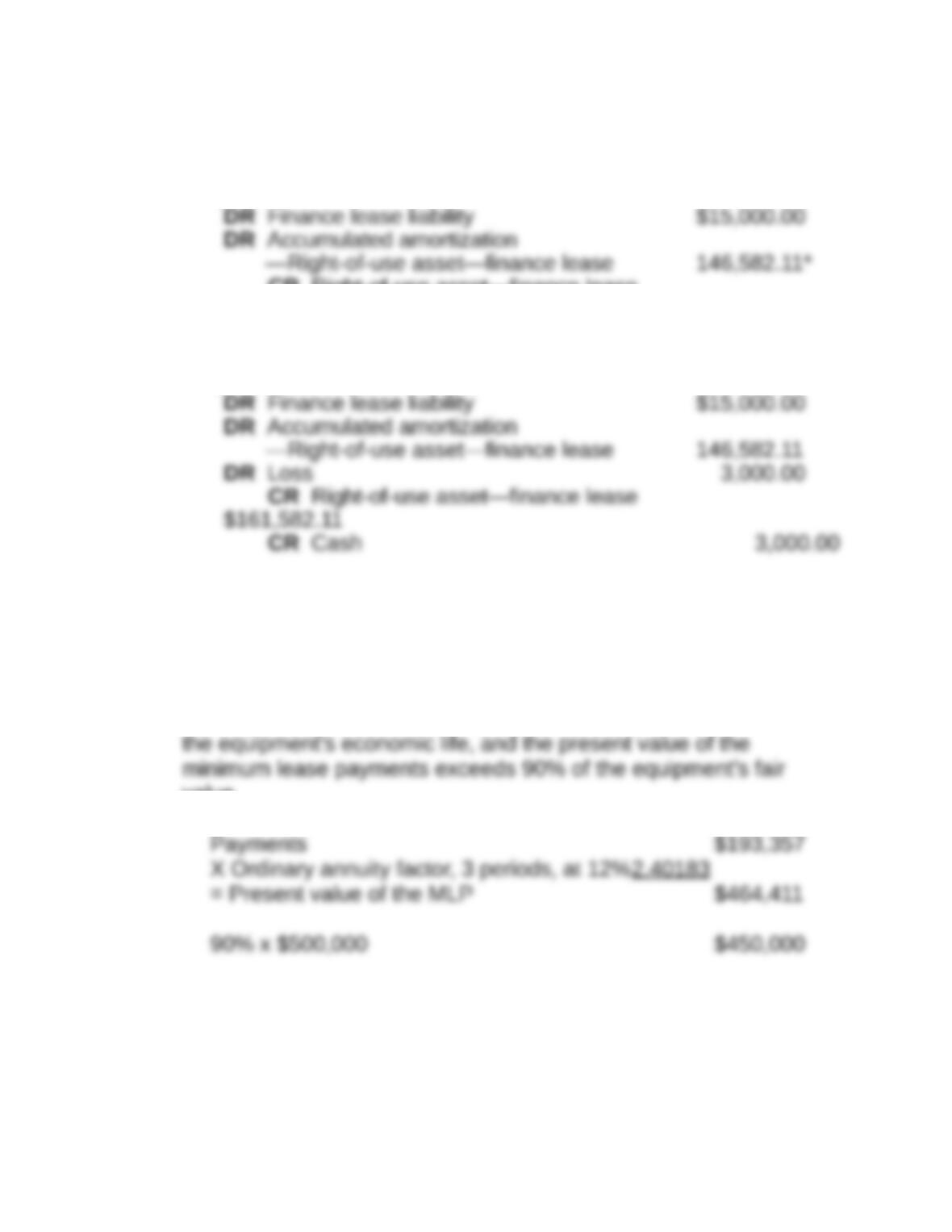

Requirement 2:

The journal entries are:

1/1/17:

CR Finance lease liability

$161,583.11

12/31/17:

CR Cash

$62,258.09

12/31/18:

CR Cash

$62,258.09

2017–2019:

Annual amortization expense =

CR Accumulated amortization

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 12-5

—Right-of-use asset—finance lease

$48,861.70

Requirement 3:

CR Right-of-use asset—finance lease

$161,582.11

*Rounded by $0.01

Requirement 4:

P12-6. Assessing guaranteed and unguaranteed residual values for

the lessee under ASC 840 (LO 12-3, LO 12-5)

Requirement 1:

This is a capital lease for Task because the lease meets at least one

of the criteria for capital lease treatment. The lease term is 75% of

value.

Requirement 2:

(a) (b) (c) (d)

Total Cash Interest Principal

Lease

Obligation

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 12-6

Date Payment Expense Payment Balance

9

Requirement 3:

2017

01/01

12/31

*(This is $464,411 ÷ 3)

@(This is $464,411 x .12)

2019

12/31

#(This is $172,640 x .12)

(To record return of leased asset to lessor.)

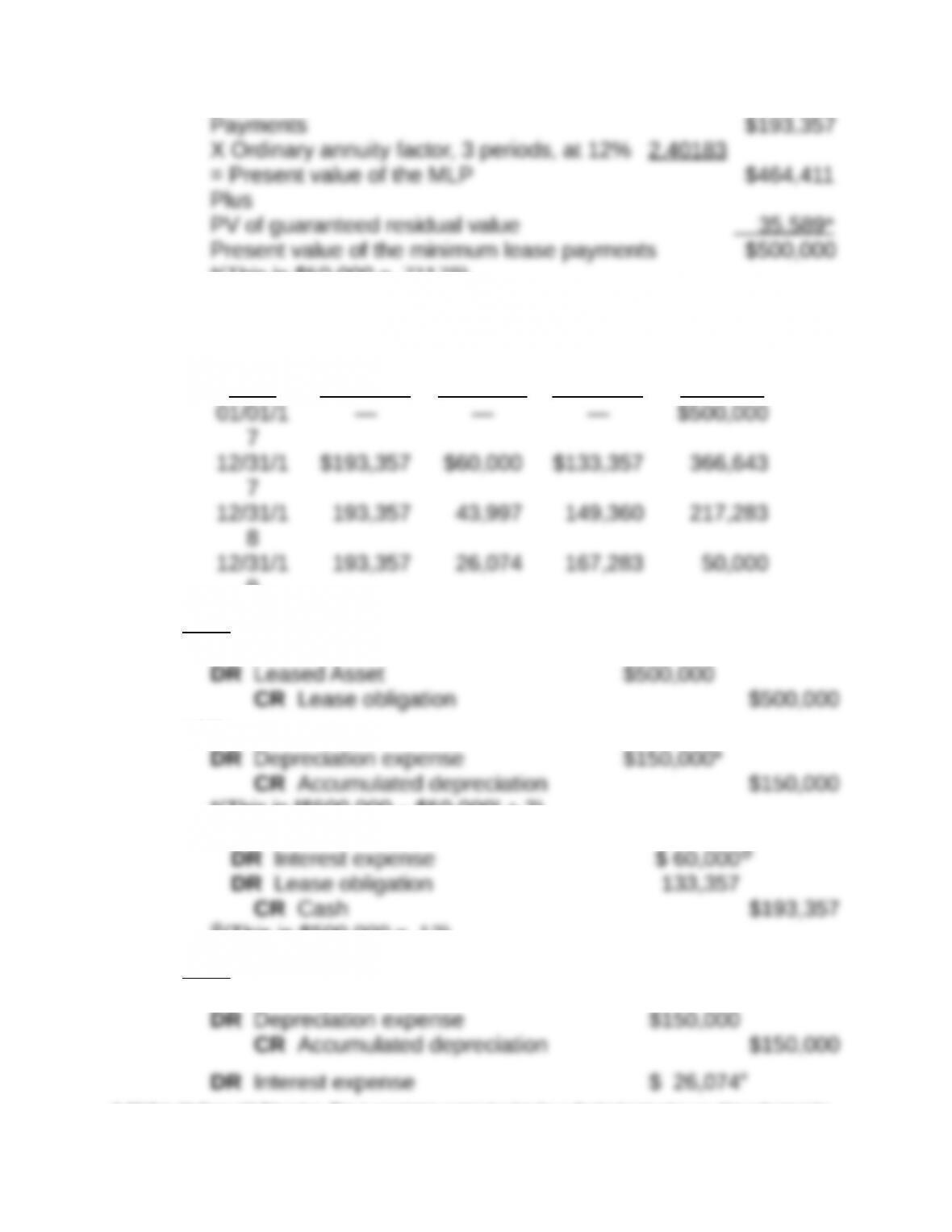

Requirement 4:

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 12-7

*(This is $50,000 x .71178)

(a) (b) (c) (d)

Date

Total

Cash

Payment

Interest

Expense

Principal

Payment

Lease

Obligation

Balance

9

2017

01/01

12/31

*(This is [$500,000 – $50,000] ÷ 3)

@(This is $500,000 x .12)

2019

12/31

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 12-8

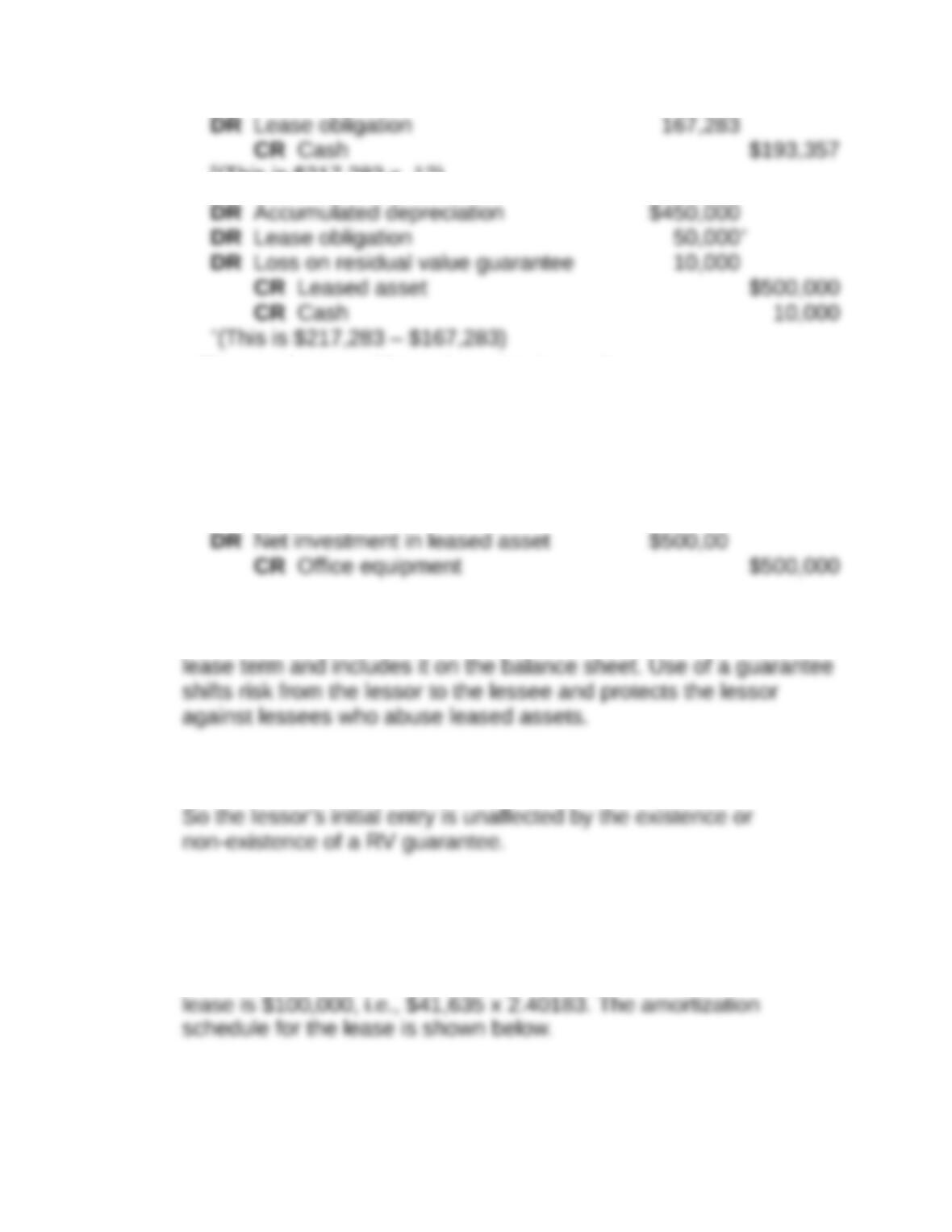

#(This is $217,283 x .12)

(To record return of leased asset to lessor.)

P12-7. Assessing guaranteed and unguaranteed residual value for the

lessor under ASC 840 (LO 12-7, LO 12-8)

Assuming the RV is not guaranteed, the entry at January 1, 2017 is:

NOTE: Although the residual value is not guaranteed by Task,

Coleman fully expects to receive the residual value at the end of the

Assuming the RV is guaranteed, the entry at January 1, 2017 is

identical to the entry made above when the RV is not guaranteed.

P12-8. Evaluating effects of ASU 2016-02 (ASC 842) and IFRS 16 on

ratios and income (LO 12-6)

Requirement 1:

The present value of the lease payments at the inception of the

Annual Reduction Balance

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 12-9

Date

Lease

Payment Interest

of Lease

Liability

of Lease

Liability

Requirement 2: Debt to asset ratio

Before lease

Lease

effects After lease

Requirement 3: Current ratio

Before lease

Lease

effects After lease

The $29,635 is the 2018 principal reduction shown in the amortization

table from Requirement 1.

Requirement 4: Pretax income effect

Before lease

Lease

effects After lease

Requirement 5: Pretax income effect under IFRS 16

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 12-10

Before lease

Lease

effects After lease

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 12-11