Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

P5-14 Explaining changes in financial ratios

(AICPA adapted)

1) a,b,d Inventory turnover is defined as the cost of goods sold

divided by average inventory. A lower inventory would cause the

inventory turnover ratio to increase, as would a higher cost of

goods sold. Consignment items should still be included in

2) a,b,e Accounts receivable turnover is net credit sales divided by

average accounts receivable. Recording goods shipped on

consignment before they are actually sold overstates accounts

3) a,b,e If the allowance for doubtful accounts increased in dollars,

but the allowance decreased as a percentage of accounts

receivable, then accounts receivable must have increased by a

4) p The refinancing of short-term debt as long-term debt at a

higher interest rate would cause the long-term debt to increase,

5) l,p Net income for the year can be found from operating income

less interest expenses and federal income taxes. If operating

5-1

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

6) h Gross margin percentage is defined as gross margin divided

by sales. If the gross margin percentage remained constant

while the gross margin increased, then sales must have

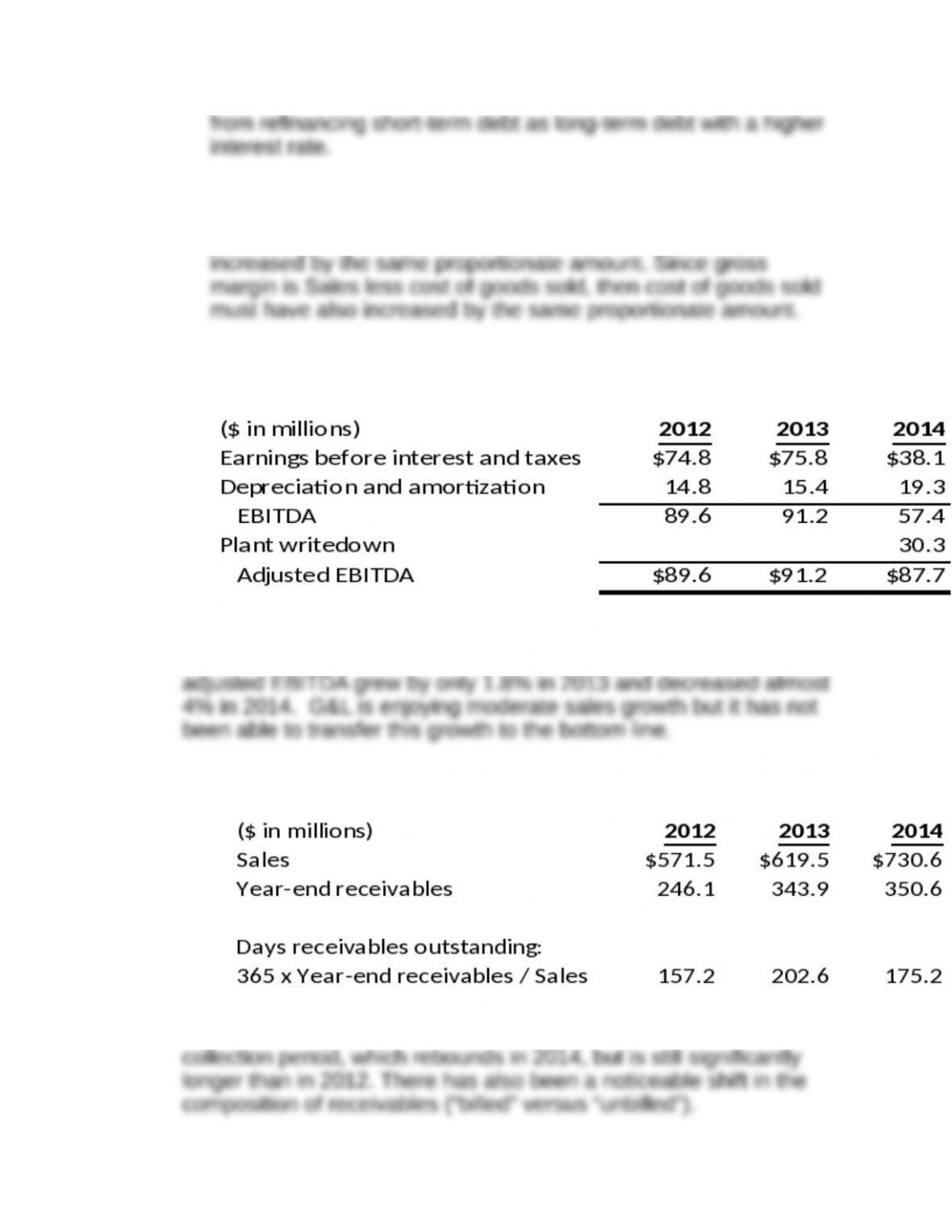

P5-15 EBITDA and revenue recognition

Requirement 1:

Requirement 2:

Sales at G&L grew at 8.4% in 2013 and almost 18% in 2014 while

Requirement 3:

GG&L’s sales growth is accompanied by a longer receivables

5-2

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

Receivable Composition 2012 2013

One reason for the increase in days accounts receivable

Requirement 4:

G&L uses percentage-of-completion to record revenue on its

long-term construction projects. (Note that the dates in the problem

pre-date the new revenue recognition standard.) This approach

assigns revenue to the period when G&L does the work—i.e., when

the revenue is “earned”. However, the exact amount of “work done”

each year, and thus the amount of revenue earned that year, is a

judgment call made by management. One way a company can

make it look like sales are growing (and profits are holding steady)

Under the new revenue recognition standard, effective in 2017 for

calendar-year companies, revenue may still be recognized over

P5-16 Analyzing ratios: Alpine Chemical

(CFA adapted)

Requirement 1:

5-3

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

a) EBIT/interest expense =

1, 629 + 318

318

= 6.12

b) Long-term debt/total capitalization =

1,491

(1,491 + 3,075)

= 33%

Note: Some students may include the $1,900 note payable as

c) Funds from operations/total debt:

(Net income + Depreciation expense)/(Long-term debt + Notes

payable)

=

(1,479 + 511) =59%

(1,491 + 1,900)

d) Operating income/sales =

2,458 =13%

19,460

Requirement 2:

a) EBIT/interest expense measures Alpine Chemical’s ability to

make its interest payments from pre-tax earnings. A ratio of less

b) Long-term debt/total capitalization measures Alpine’s financial

leverage. A highly leveraged company can find that issuing new

c) Funds from operations/total debt measures Alpine’s ability to

d) Operating income/sales measures Alpine’s profitability.

5-4

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

increased, or costs reduced, to generate the same level of operating

Requirement 3:

a) EBIT/interest expense. With the exception of 2013, interest

coverage has been consistently above 4.00. The year 2017 shows

b) Long-term debt/total capitalization. This leverage measure has

been stable in the past three years. During the six-year period,

c) Funds from operations/total debt. The cash flow ratio has been

d) Operating income/sales. Operating margins remain stable but

Financial Reporting and Analysis (7th Ed.)

Chapter 5 Solutions

Essentials of Financial Statement Analysis

Cases

Cases

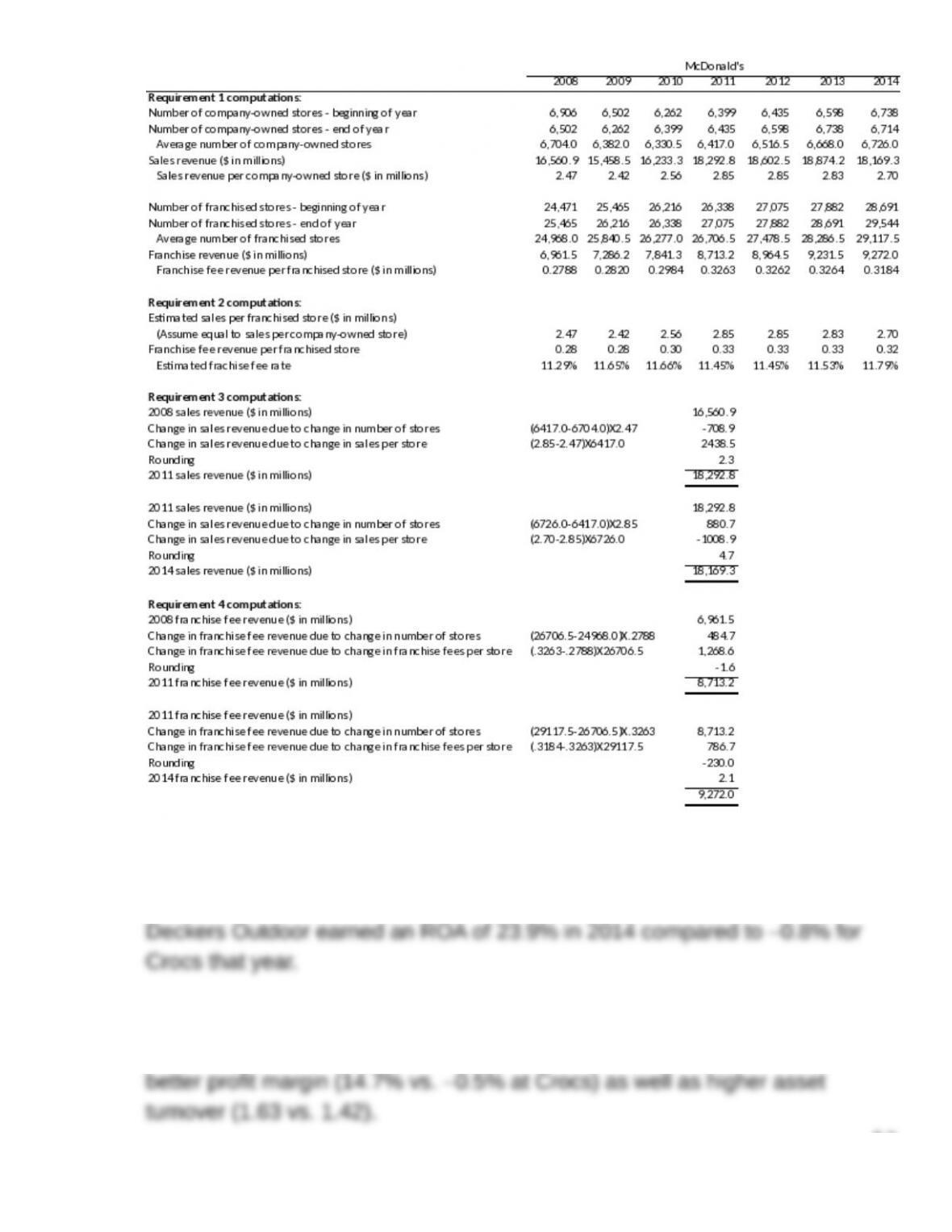

C5-1 McDonald’s and Buffalo Wild Wings: Comparing two restaurant

chains

Requirements 1 and 2:

5-5

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

Buffalo Wild Wings’ sales per company-owned store have grown

substantially in the last several years, and now exceed that of

McDonald’s ($3.08 million versus $2.70 million). However,

franchise fees per store are significantly greater at McDonald’s

suggesting McDonald’s is able to charge a larger franchise fee rate.

Requirements 3, 4 and 5:

2011 versus 2008

Sales at company-owned Buffalo Wild Wings stores grew from

$379.7 million in 2008 to $717.4 million in 2011. That growth

resulted from both an increase in the number of stores open ($233.2

million) and growth in sales per store ($104.0 million). In contrast,

Similarly, more of Buffalo Wild Wings’ franchise fee growth is due to

2014 versus 2011

From 2011 to 2014, sales at company-owned Buffalo Wild Wings

stores again grew due to both factors, with more of the growth

5-6

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

$880.7 million. However, this increase was more than offset by

falling sales per store ($2.70 million per store versus $2.85 million),

Buffalo Wild Wings’ franchise fee revenue grew as a result of both

more store and greater fees per store. Like its results for

Summary

These analyses illustrate the two different strategies these

companies employ, probably due where each is in its life cycle.

McDonald’s is much more mature and therefore has fewer growth

In contrast, Buffalo Wild Wings is still getting a substantial amount

of growth from new locations, both company-owned and franchised.

From 2008 to 2014, it has more than doubled the number of

5-7

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

5-8

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

C5-2. Crocs and Deckers Outdoor: Comparing footwear manufacturers

Requirement 1:

Requirement 2:

The superior ROA earned in 2014 by Deckers Outdoor can be traced to a

5-9

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Requirement 3:

In 2012, Crocs reported a strong ROA of 25.5%. It fell substantially the next

year, suggesting either a decline in profitability or that the quality of 2012

Requirement 4:

Deckers had a greater number of days receivables outstanding and inventory

held until 2014, when it cut both substantially. This decrease coincides with

strong sales growth (16.7% in 2014 versus 2013), suggesting Deckers was

Requirement 5:

Days receivables outstanding and days inventory held could be affected by

the year-end, as they are based on balance sheet amounts. When a

company’s operations have a seasonal component to it, certain balance

C5-3. Argenti Corporation: Evaluating credit risk

Requirement 1:

Operating cash flows for 2016 ($356) million

The company’s operating cash flows are described in the case exhibit. The

long-term debt repayment is the account balance decrease (from $423 million

to $87 million).

5-10

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Property, plant, and equipment, and investments declined during 2016, which

suggests that these items provided cash rather than consumed it. There

Thus, two factors seem responsible for the increased short-term borrowing:

repayment of the company’s existing long-term debt and the negative cash

There are several aspects of the financial statements that point to a company

Requirement 2:

By almost any measure, Argenti’s credit risk has increased substantially

since 2012: sales have declined, losses are being recorded, operating cash

flows are negative, and the company has already violated its existing loan

Under normal circumstances, this would not be the time for a lender to

expand its credit position with the company from $165 million to $1.5 billion.

But circumstances are not normal since GE Capital is also Argenti’s largest

What happened?

This case is drawn from the experience of Montgomery Ward & Company,

which was taken private in a $3.8 billion leveraged buyout by GE Capital and

the then CEO, Bernard Brennan, in 1988. Shortly after releasing its first-

5-11

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.