E13-17. Computing tax due, deferred taxes, and tax expense

Requirement 1:

The calculation of tax due for 2017 is as follows:

Requirement 2:

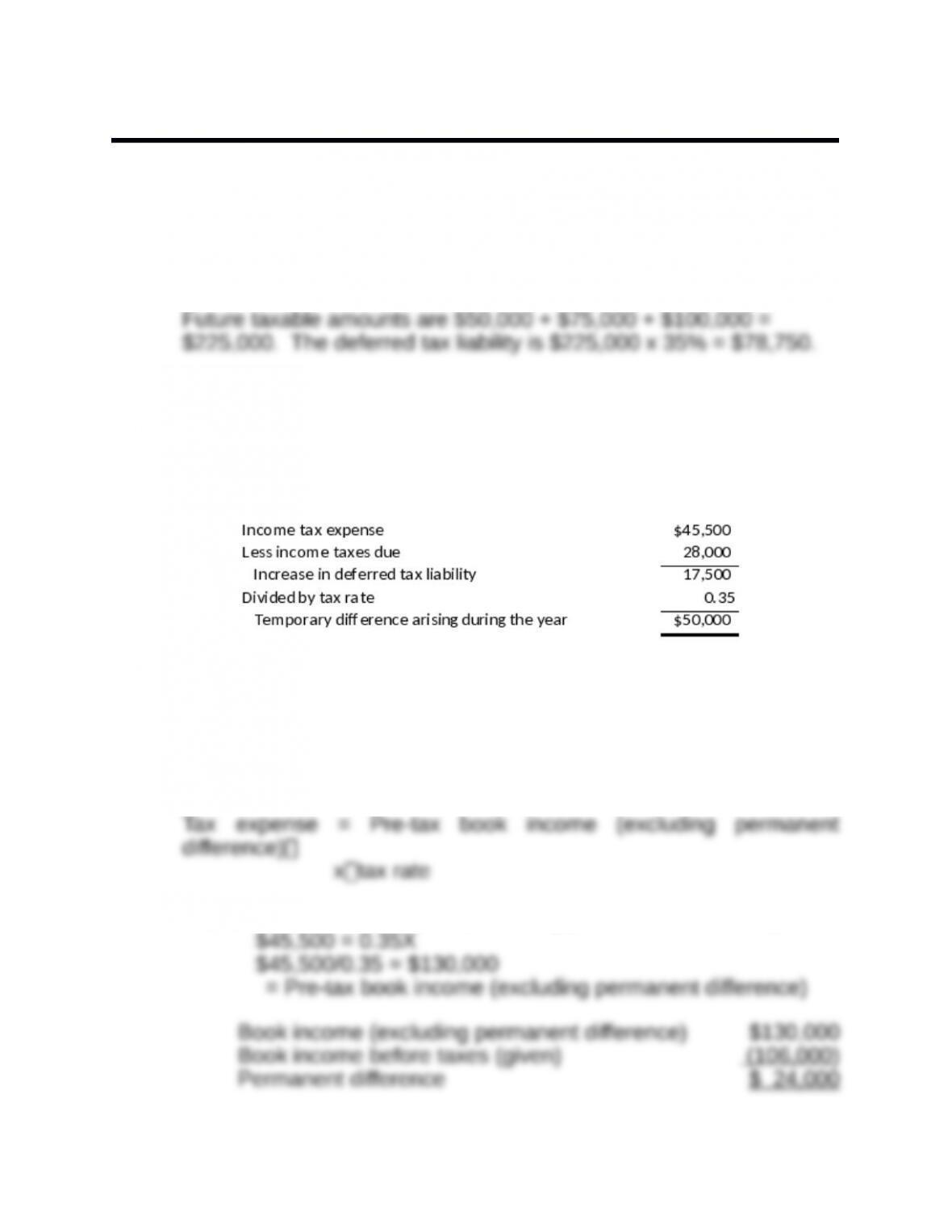

Changes in deferred taxes for 2017:

Temporary difference

Requirement 3:

Calculation of income tax expense for 2017:

Income tax expense = Taxes due for year + Increase in deferred

tax

Because there is no change in the tax rate, income tax expense can

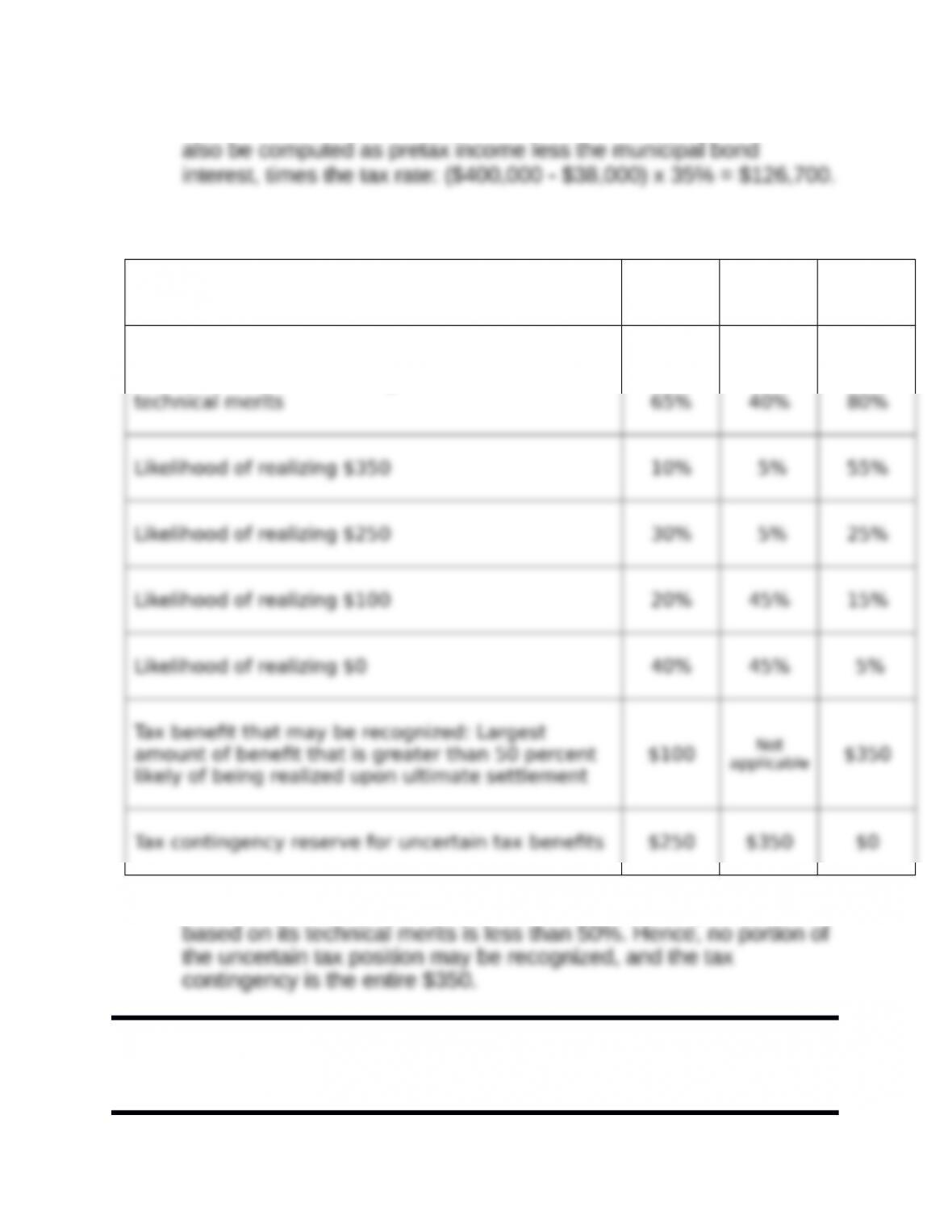

E13-18. Determining tax benefit for uncertain tax position

Case 1 Case 2 Case 3

Management’s assessment of the likelihood of the

uncertain tax position being sustained based on

Note that in case 2, the likelihood of Collins sustaining the position

Financial Reporting and Analysis (7th Ed.)

Chapter 13 Solutions

Income Tax Reporting

Problems

Problems

P13-1. Calculating deferred tax amounts

(AICPA adapted)

P13-2. Calculating the amount of temporary and permanent

differences and tax entry

Requirement 1:

Calculation of temporary difference:

Because tax expense per books is greater than taxes due for the

year, taxable income is lower than book income.

Requirement 2:

Calculation of permanent difference:

Let X = Pre-tax book income (excluding permanent difference)

Book income will be lower than taxable income because of this

permanent difference.

Requirement 3:

Journal entry to record tax expense for year:

Requirement 4:

The effective tax rate is higher than the statutory tax rate of 35%

P13-3. Reporting deferred tax amount on income statement

(AICPA adapted)

Journal entry to record taxes for 2017 (not required):

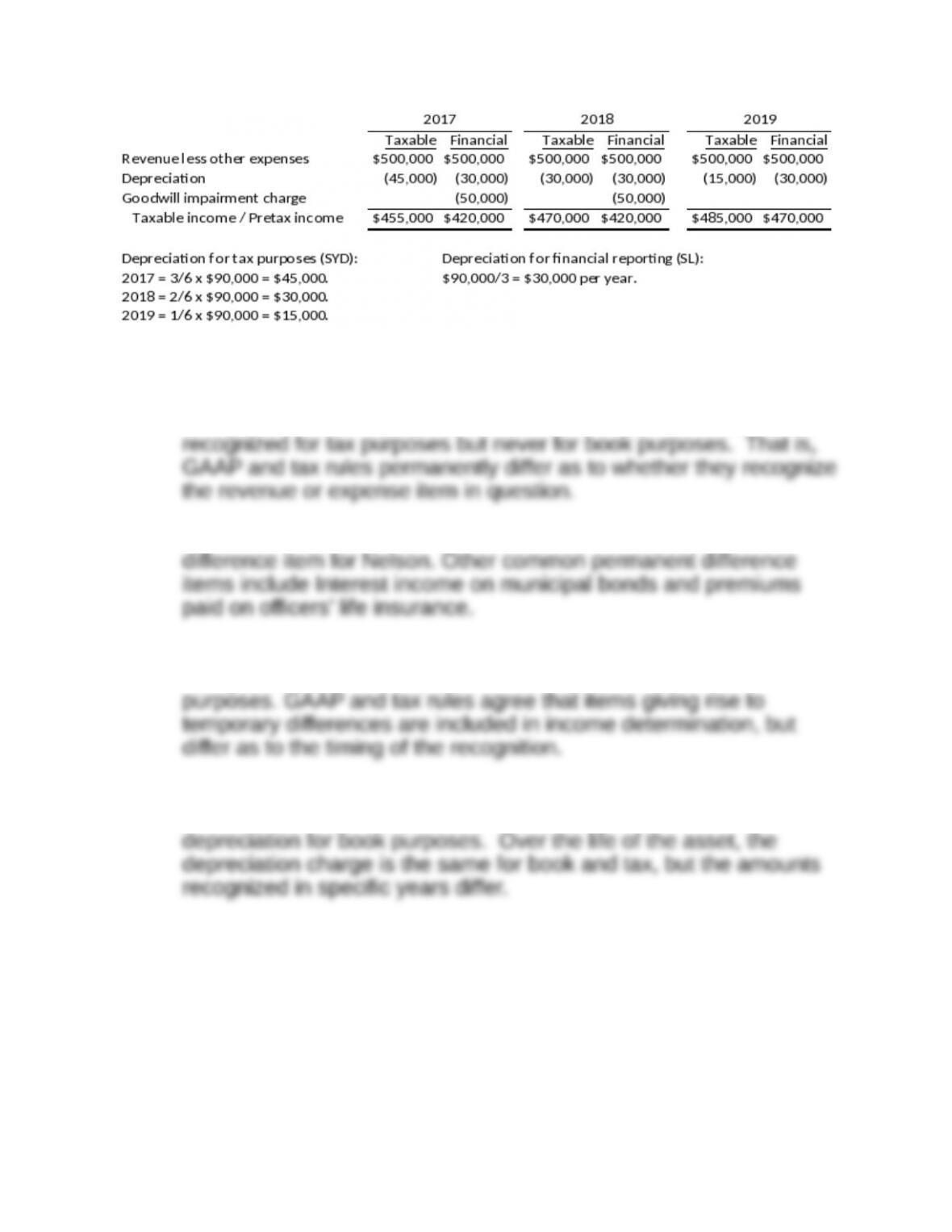

P13-4. Computing tax expense and making deferred tax calculations

Requirement 1:

Requirement 2:

A permanent difference item is a revenue or expense that is

recognized for book purposes but never for tax purposes or

A goodwill impairment charge is an example of a permanent

Temporary differences are revenue or expense items that are

recognized in a different period for book purposes than for tax

An example of a temporary difference for Nelson is the use of

sum-of-years’-digits depreciation for tax purposes and straight-line

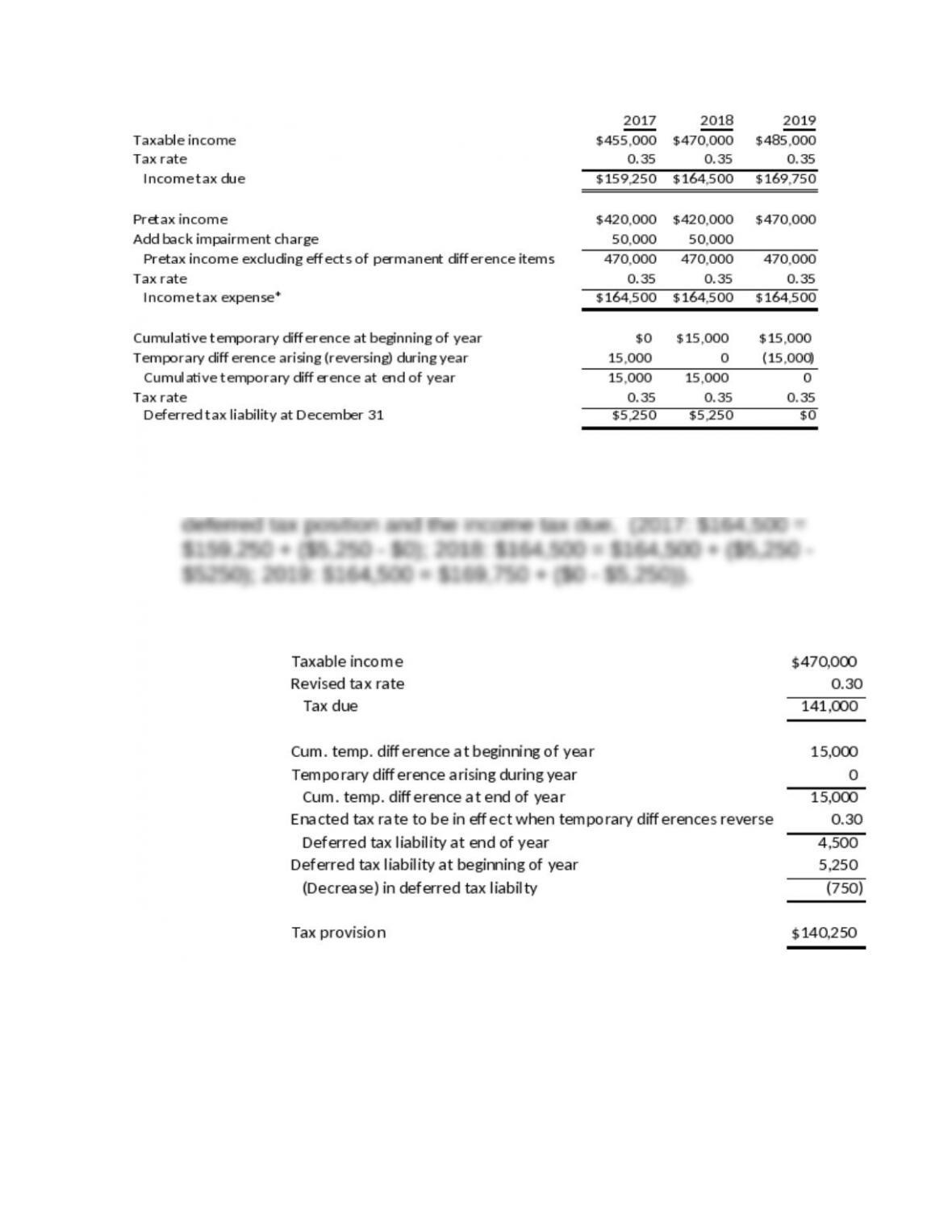

Requirement 3:

*Because the tax rate did not change, this approach to determining

income tax expense is equivalent to summing the change in the

Requirement 4:

Note that even though there was no temporary difference arising or

reversing in 2018, the change in the deferred tax liability resulting

from the change in the income tax rate results in a deferred income

tax provision of –$750.

P13-5. Determining current and deferred portion of tax expense and

reconciling statutory and effective tax rates

All dollar amounts are in thousands.

Requirement 1:

Requirement 2:

The deferred tax assets and liabilities arising in 2017 will reverse in

future periods when the enacted tax rate will be 40%. Therefore, the

Increase in deferred tax liabilities (relating to temporary differences

giving rise to future taxable amounts):

Increase in deferred tax assets (relating to temporary differences

giving rise to future deductible amounts):

Requirement 3:

Tax expense = Taxes due + Increase in deferred tax liability –

Requirement 4:

Reconciliation of statutory and effective tax rates (amounts):

Percenta

ge

of

Pre-Tax

Amount Inco

me

Expected tax expense at statutory rate

P13-6. Tax effects of differences between IFRS and U.S. GAAP related

to impairment charges

All amounts are rounded to the nearest $1.

Requirement 1:

The depreciable cost of the asset is $6,100,000 – $1,100,000 =

$5,000,000. Using straight-line depreciation and a 25-year life gives

The tax basis at December 31, 2018 is $3,130,635, as shown in the

following table:

Year

Beginning

Tax Basis Rate

Tax

Depreciation

Ending

Tax Basis

Note: DDB depreciation rate = 2 x (1/25) = 8%. Because the

amount of depreciation expense in 2018 using the double-declining

Requirement 2:

In 2018, Dolan had tax depreciation of $272,229 (see table in

Requirement 1) versus $200,000 of book depreciation. Because

Note that this amount explains the increase in the deferred tax

liability from December 31, 2017 to December 31, 2018. At any

point in time the deferred tax liability is equal to the cumulative

Requirement 3:

First Dolan must determine whether there is an impairment as of

December 31, 2018. Under U.S. GAAP, an impairment exists if the

book value of the asset exceeds the asset’s undiscounted future

Dolan had $8,200,000 of income before depreciation and taxes in

2018 (given). Tax depreciation was $272,229 (see table in

Income tax expense was computed as the sum of the income tax

due for the year and the increase in the deferred tax liability.

However, note that because there was no change in the income tax

Requirement 4:

First Dolan must determine whether there is an impairment as of

December 31, 2018. Under IFRS, an impairment exists if the book

value exceeds the greater of the fair value (net of cost to sell) or the

value in use. The fair value is $4,300,000 and the cost to sell is

The impairment loss reduces book income but there is no related

income tax deduction in the current period, so there is a temporary

difference. The temporary difference will reverse when DC

Taxable income in 2018 is the same as determined in Requirement

3, resulting in the same income tax due of $2,774,720. The

As a result, income tax expense is lower than in the U.S. GAAP

DR Income tax expense $2,715,300