P10-21. IFRS impairment and revaluation (LO 10-10)

Requirement 1: Cost model

12/31/2016:

No entry

12/31/2017:

12/31/2018:

Requirement 2: Revaluation model

12/31/2016:

12/31/2018:

P10-22. IFRS impairment and revaluation (LO 10-10)

Requirement 1: Cost model

12/31/2016:

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale

or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted

on a website, in whole or part. 10-1

*2,100,000/30 years x ½ year

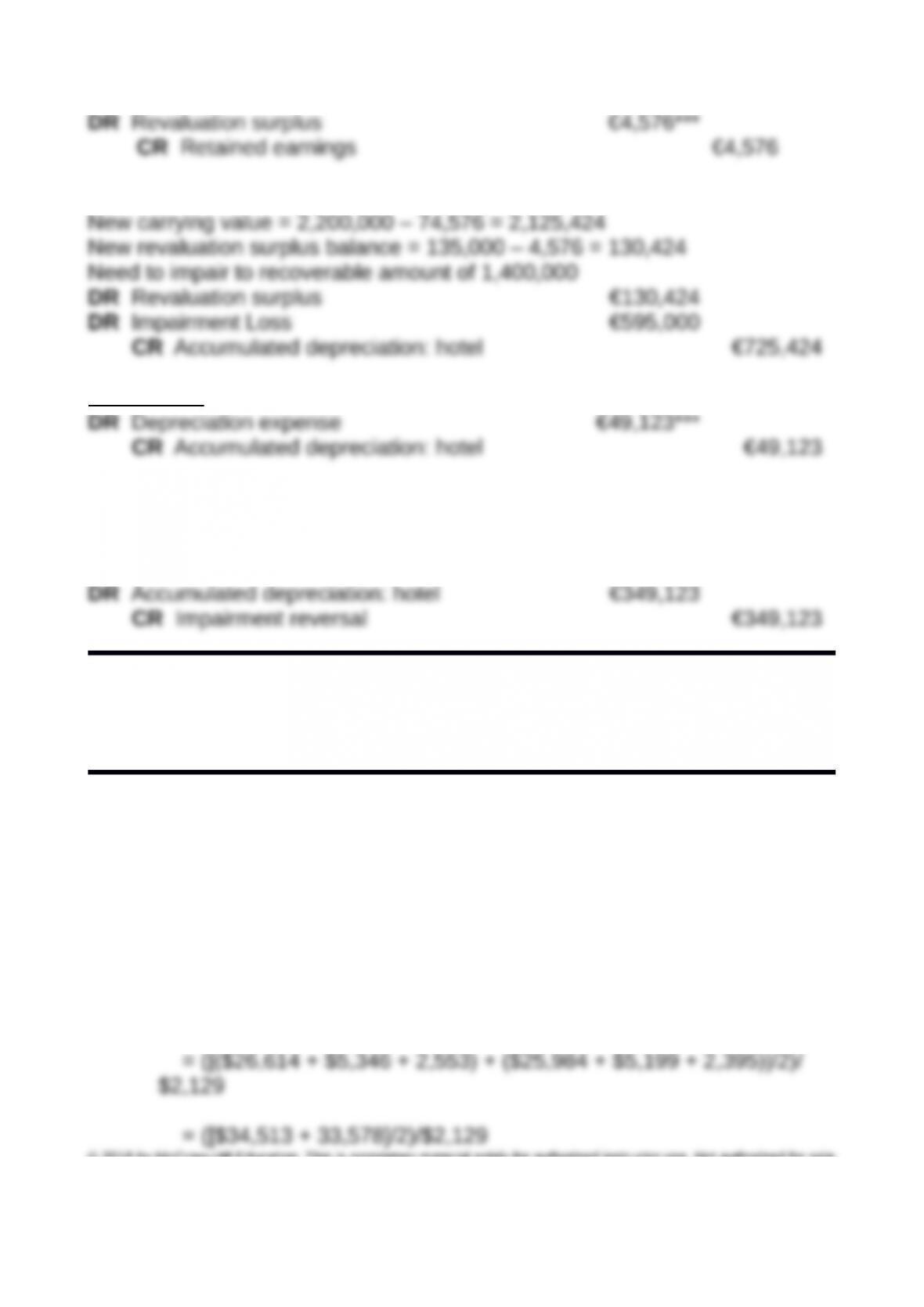

12/31/2017:

***1,400,000/28.5 years

New carrying value = 1,400,000 – 49,123 = 1,350,877

Need to reverse impairment (limited to 595,000 of prior impairment

write-downs)

*2,100,000/30 years x ½ year. This catches up depreciation before the

revaluation.

**(2,200,000)/29.5 years

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale

or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted

on a website, in whole or part. 10-2

***(135,000)/29.5 years

12/31/2018:

***1,400,000/28.5 years

New carrying value = 1,400,000 – 49,123 = 1,350,877

Need to reverse impairment (limited to 595,000 of prior impairment

write-downs)

Financial Reporting and Analysis (6th Ed.)

Chapter 10 Solution

Long-Lived Assets and Depreciation

Cases

Cases

C10-1. Target Corporation and Wal-Mart Stores, Inc. (Walmart):

Identifying depreciation differences and performing financial

statement analysis (LO 10-8)

Requirement 1:

The estimated average useful life of Target’s assets is:

Average useful life = average gross PP&E (excluding land and

construction in progress)/depreciation expense

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale

or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted

on a website, in whole or part. 10-3

The estimated average useful life of Walmart’s assets is:

Average useful life = average gross PP&E (excluding

land)/depreciation expense

= 16.4 years

Requirement 2:

Walmart’s revised, estimated depreciation expense would be:

= Average gross PP&E (excluding land)/Target life

Walmart’s revised, estimated depreciation expense is higher because

of the shorter average useful life of Target’s assets.

Walmart’s income before taxes would decrease by $9,314 – 9,100, or

$214 (i.e., the increase in the depreciation expense that would have

Walmart’s Income from continuing operations of $16,814 for the year

ended January 31, 2015 would decrease by $139.1 [$214 * (1-0.35)]

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale

or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted

on a website, in whole or part. 10-4

Requirement 3:

Target’s revised, estimated depreciation expense for the year would

be:

Target’s revised, estimated depreciation expense is lower because of

the longer average useful life of Walmart’s assets.

The following calculations are simply the flip side of those in

Requirement 2.

Target’s earnings before income taxes would increase by $2,129 –

$2,075.9, or $53.1 (i.e., the decrease in the depreciation expense that

Target’s net earnings from continuing operations of $2,449 would

Requirement 4:

The comparability of the financial statements of firms in the same

industry, hence, comparisons involving their financial ratios, can be

hindered by differences in depreciation policy. The analysis above

Requirement 5:

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale

or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted

on a website, in whole or part. 10-5

Some factors that affect the reliability and accuracy of the adjustments

made above include:

a The analysis assumes that the firms have similar proportions of the

b The analysis above assumes that the salvage values used by the

methods for a portion of its long-term assets.

d The extent to which the different useful life choices are, in fact,

during the construction period would be understated and income in the

years after the assets are placed in service would be overstated.

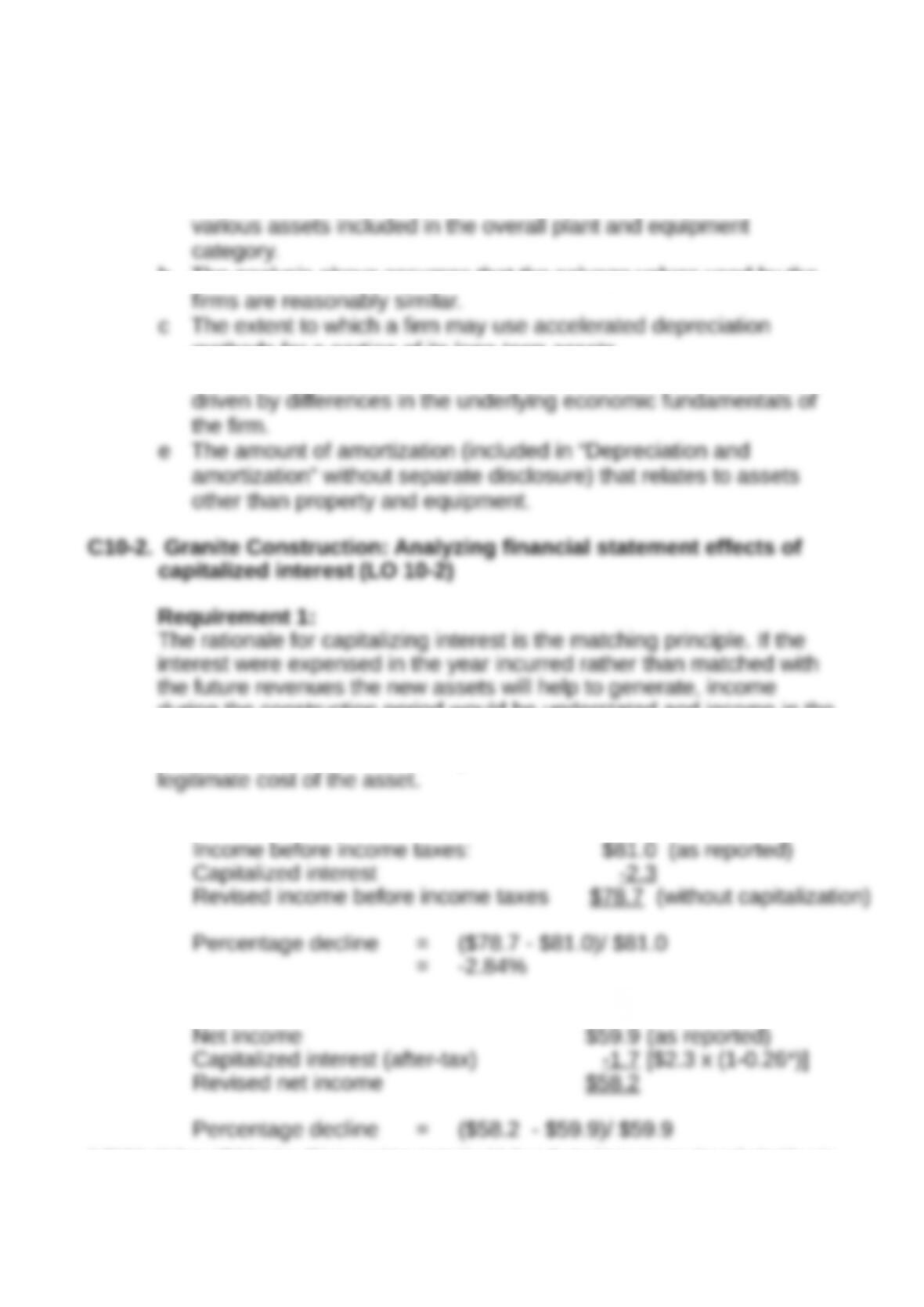

Another rationale for capitalizing interest is that it is considered to be a

Requirement 2:

Requirement 3:

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale

or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted

on a website, in whole or part. 10-6

Requirement 4:

The capitalized interest will reduce future years’ reported earnings—in

C10-3.Diamond Offshore Drilling, Inc.: Analyzing financial statement

effects of capitalized interest (LO 10-2)

Requirement 1:

Requirement 2:

Assuming that the interest was actually paid, the reduction in interest

Requirement 3:

Because the $16,308,000 becomes part of Property and equipment

Depreciation is a non-cash expense and will not affect cash from

Investing activities would not be affected by the depreciation expense.

Requirement 4:

The price of oil fell from $110.00 at the end of 2013 to $37.00 by the

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale

or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted

on a website, in whole or part. 10-7

C10-4.Diamond Offshore Drilling, Inc.: Analyzing financial statement

effects of asset impairment (LO 10-5)

Requirement 1:

The note states that the decline in oil prices led to reductions in

customer capital spending and contract cancellations. Additionally,

drillers have to follow stricter regulations when drilling in the Gulf of

Mexico.

Requirement 2:

Requirement 3:

Effect on Operating income:

Requirement 4:

The impairment loss does not affect cash from operating activities. If

the indirect method is used, the loss would be added back to the net

loss. Managers are often fond of saying that they only need to be

concerned about items that affect cash flows and that the loss only

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale

or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted

on a website, in whole or part. 10-8

C10-5.Royal Dutch Shell, plc: Identifying differences and similarities

between IFRS and GAAP (LO 10-10)

Similarities

3 Although the question asks about Property, plant, and equipment,

the instructor may also want to mention differences related to

intangible assets.

Differences

1. The test for impairment and the subsequent write-down are

different from U.S. GAAP. Shell reduces the carrying amount to

the recoverable amount, which is “the higher of fair value less

2. IFRS allows firms to reverse impairment losses. This is evident

from the impairment loss schedule. In 2014, Royal Dutch Shell

had new impairment losses of $6,983 million, but it also reversed

$344 million of previously recognized impairment losses. Because

C10-6.Marston’s PLC: Identifying differences and similarities between

IFRS and GAAP (LO 10-10)

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale

or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted

on a website, in whole or part. 10-9

Similarities

1. Marston’s uses the straight-line method to depreciate the cost of

the assets, less salvage value, over their useful lives. This

Differences

1. IFRS allows long-lived tangible assets to be valued under the

depreciated cost model or a revaluation model. Marston’s

revalues its properties on a regular basis so that the carrying

value “does not differ significantly from its fair value.” When the

assets are revalued upwards, the Revaluation reserve within

2. The test for impairment and the subsequent write-down are

different from U.S. GAAP. Marston’s states that it recognizes an

impairment loss when the carrying value is less than the

“recoverable amount,” which is “the higher of value in use and fair

3. IFRS allows firms to reverse impairment losses. Marston’s states

that a loss may be reversed if the recoverable amount increases,

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale

or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted

on a website, in whole or part. 10-10