Financial Reporting and Analysis (7th Ed.)

Chapter 14 Solutions

Pensions and Postretirement Benefits

M,;nbklExercises

Exercises

E14-1. Determining projected benefit obligation (LO14-3)

(AICPA adapted)

The projected benefit obligation on 12/31/17 is computed as follows:

Pension benefit obligation 12/31/17 $82 ,200

E14-2. Determining balance sheet pension asset (liability) (LO14-2,

LO14-3)

(AICPA adapted)

GAAP requires that companies recognize the funded status on the

$2,250,000).

E14-3. Determining balance sheet pension asset (liability) (LO14-3)

(AICPA adapted)

Funded status of the plan 12/31/17:

Contributions $1,000,000

Amount of plan overfunding $ 480 ,000

So, $480,000 is the amount of the balance sheet asset (liability).

E14-4. Determining PBO and ABO (LO14-1, LO14-2)

Birthday # 60 Birthday # 65 Birthday # 80

1/1/2017 1/1/2022 1/1/2037

Ms. Abbott is expected to receive 15 benefit payments of $36,000.

Calculations required:

projected benefit payments as of 1/1/2017.)

Requirement 1:

Compute the projected benefit obligation at 1/1/2017:

Discount rate = 8%

Factor for the annuity or the single sum.

PVOA at 1/1/2022 = Benefit payment x PVOA@8%, 15

PV at 1/1/2017 = $308,141 x 0.68058

PV at 1/1/2017 = $ 209,715

Projected Benefit Obligation at 1/1/2017 is $ 209,715

Requirement 2:

Compute the accumulated benefit obligation at 1/1/2017:

Same calculation as Requirement 1, except benefit payment ignores

future salary increases, and is based on current salary level.

PVOA at 1/1/2022 = Benefit payment x PVOA@8%, 15

PV at 1/1/2017 = $246,513 x 0.68058

PV at 1/1/2017 = $ 167,772

Accumulated Benefit Obligation at 1/1/2017 is $ 167,772

E14-5. Determining PBO and ABO (LO14-1, LO14-2)

payment 1/1/2023.

Ms. Abbott’s expected benefit payment is $36,000 ($60,000 x 60%).

Ms. Abbott is expected to receive 15 benefit payments of $36,000.

payments as of 1/1/2022.)

projected benefit payments as of 1/1/2017.)

Requirement 1:

Compute the projected benefit obligation at 1/1/2017:

Discount rate = 11%

Present Value of a Single Amount (PV) periods = 5

PV at 1/1/2017 = PVOA at 1/1/2022 x PV@11%, 5

Projected Benefit Obligation at 1/1/2017 is $ 153,627

Requirement 2:

Compute the accumulated benefit obligation at 1/1/2017:

Same calculation as Requirement 1, except benefit payment ignores

future salary increases, and is based on current salary level.

Present Value of a Single Amount (PV) periods = 5

PVOA at 1/1/2022 = Benefit payment x PVOA@11%, 15

PV at 1/1/2017 = $207,097 x 0.59345

E14-6. Determining actual return on plan assets (LO14-2, LO14-3)

(AICPA adapted)

The actual return on plan assets is determined by solving for ? in

the formula below:

Benefits paid to retirees (85,000)

E14-7. Determining balance sheet pension asset (liability) (LO14-3,

LO14-4)

(AICPA adapted)

The balance sheet pension asset (liability) as of 12/31/17 is the

assets and thus the pension asset

The following entries could be made to reflect the funded status on

the balance sheet:

Cash $40,000

Pension asset $1,000

An alternative approach would be to recognize that the balance

Beginning balance $ 2,000

Ending balance $ 7 ,000

E14-8. Determining balance sheet pension asset (liability) (LO14-3,

LO14-4)

(AICPA adapted)

The amount on the balance sheet is the funded status. The ending

amount is computed as:

Ending funded status $(1 ,412,808)

E14-9. Determining balance sheet pension asset (liability) and AOCI

balance (LO14-3, LO14-4)

(AICPA adapted)

The amount of the pension asset (liability) is the funded status.

the balances follow:

PBO, 1/1/2017 $ (60,000)

Plan assets, 1/1/2017 $ 0

AOCI – prior service cost, 1/1/17 $60,000

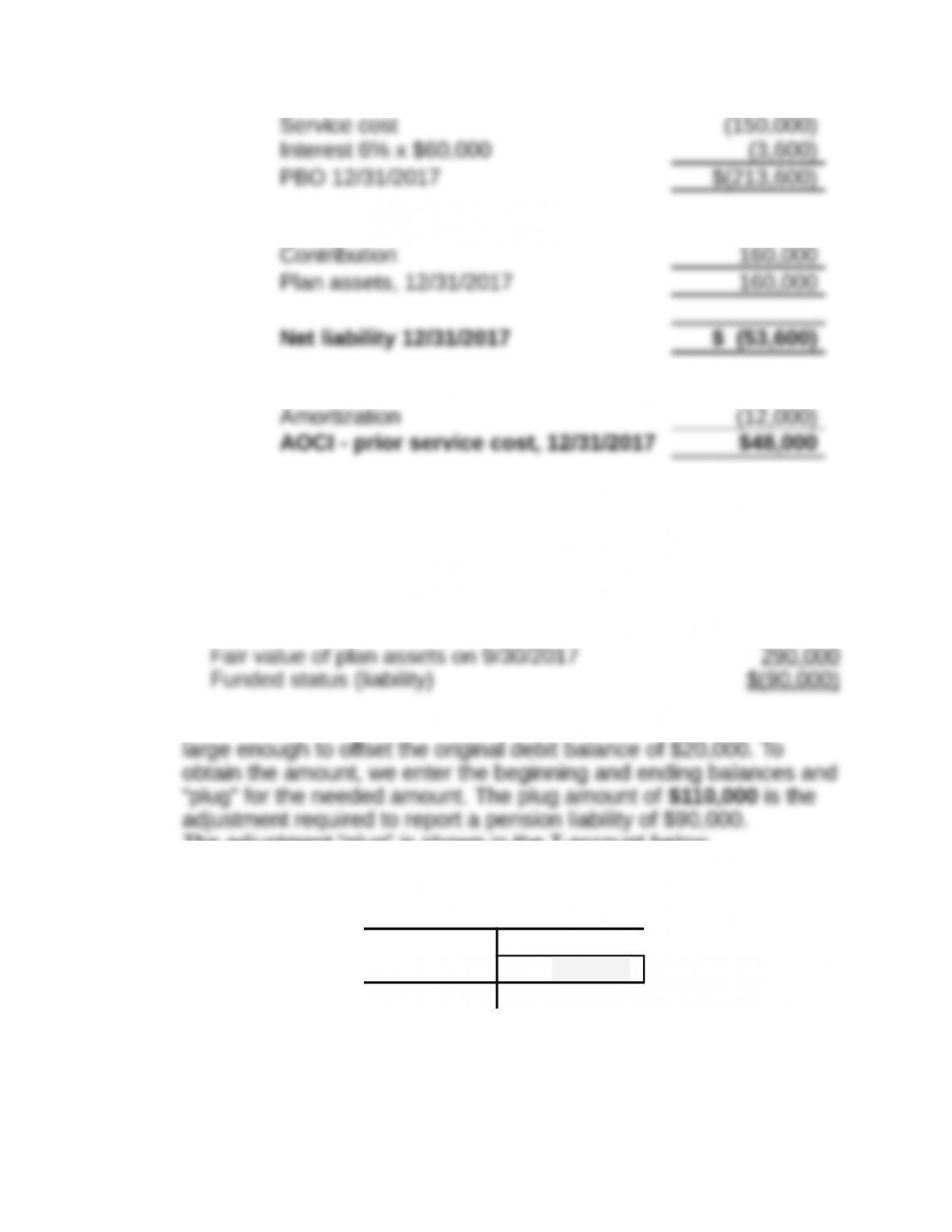

E14-10. Adjusting balance sheet pension asset (liability) (LO14-3)

(AICPA adapted)

The balance sheet asset liability is the difference between plan

assets and PBO:

PBO on 9/30/2017 $(380,000)

To obtain the $90,000 desired credit balance we must add a credit

The adjustment “plug” is shown in the T-account below.

Pension

asset (liability)

$20,000

$110,000

$90,000

E14-11. Determining postretirement expense (LO14-7)

(AICPA adapted)

Postretirement benefit cost is determined below:

Postretirement benefit cost $290 ,000

E14-12. Determining pension expense (LO14-3)

(AICPA adapted)

Pension expense is calculated as follows:

Pension expense $180 ,000

E14-13. Determining pension expense, fair value of plan assets, and

deferred return on plan assets (LO14-3, LO14-4)

Requirement 1:

Determination of pension expense for Bostonian in 2014:

Service cost $120,000

Pension expense for 2017 $200 ,000

Requirement 2:

Plan assets at December 31, 2017:

Beginning fair value of plan assets $2,000,000

Fair value of plan assets, 12/31/2017 $2 ,300,000

Requirement 3:

Dollar amount that is deferred in 2017:

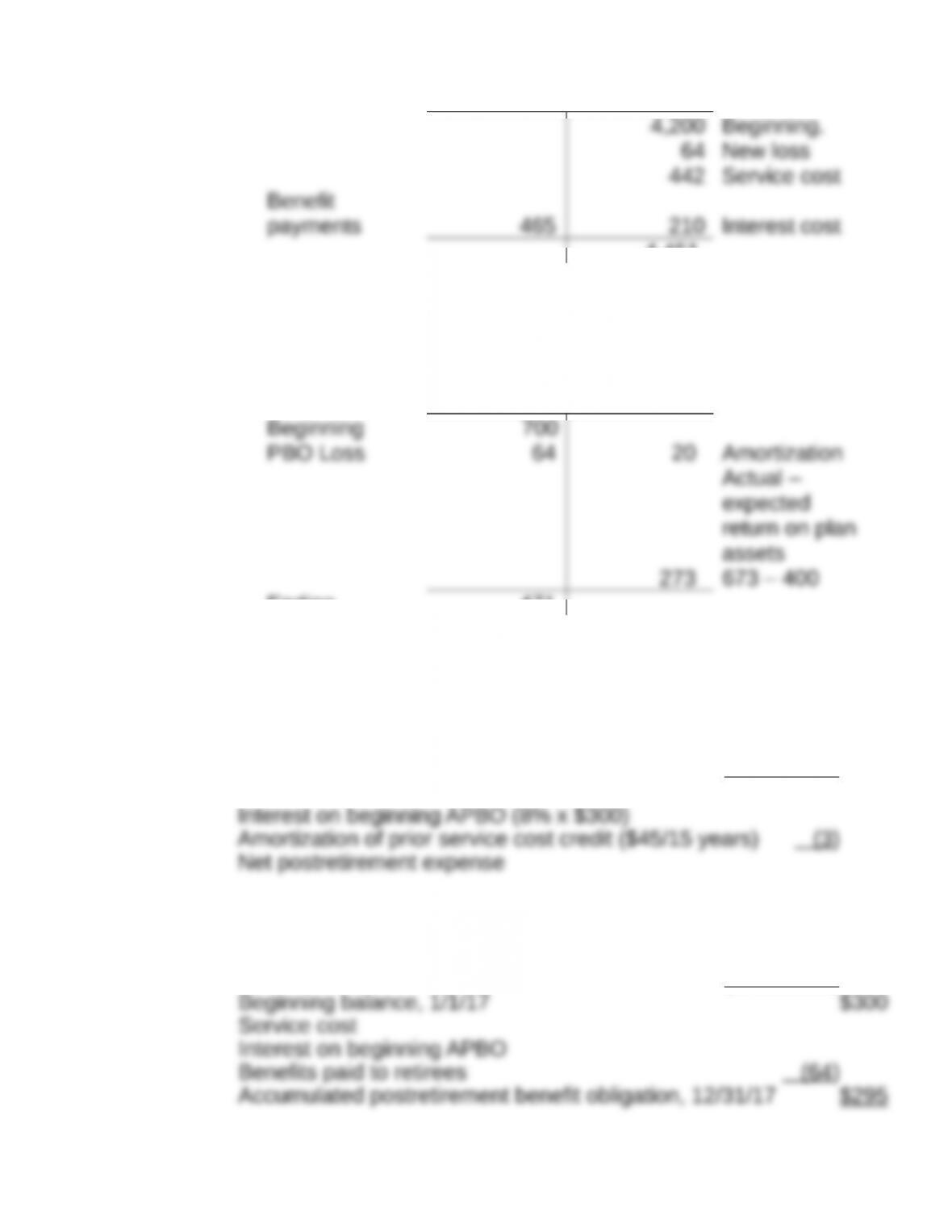

E14-14. Determining pension expense and plan asset, PBO, and AOCI

balances (LO14-3, LO14-4)

Requirement 1: Pension expense

Service Cost $442

Pension cost $322

*Calculation of amortization of actuarial loss:

Amortization 20

Requirement 2: Fair value of plan assets

Plan Assets

Beginning 5,000

Ending 5,458

Requirement 3: Projected benefit obligation

Projected

Benefit Obligation

4,451

Requirement 4: AOCI – Net actuarial (gain) loss

AOCI – Net Actuarial

Loss

Ending 471

E14-15. Determining postretirement (healthcare) benefits expense and

obligation (LO14-7)

Requirement 1:

Determining postretirement expense:

($ millions)

Service cost

Requirement 2:

Determining 12/31/17 balance in accumulated postretirement

benefit obligation account:

($ millions)