E16-17. Translating foreign currency

(AICPA adapted)

Because the subsidiary’s functional currency is the local currency unit

(LCU), Ward Inc. must use the current rate method to translate the

included in the consolidated income statement would be 400,000 x .44 =

$176,000.

E16-18. Reporting transaction foreign exchange gain/loss

(AICPA adapted)

Lindy Corp. has engaged in a foreign currency transaction. The transaction

or losses go through income in the year that the change occurs.

On November 5, 2017, Lindy would make the following entry (not required):

euros x $1.40 per euro)

In preparing its 2017 financial statements, Lindy would make the following

adjusting entry to reflect the year-end spot rate (not required):

DR Accounts payable $2,000

On January 15, 2018 Lindy would make the following entry (not required):

DR Accounts payable ($140,000- $2,000) $138,000

DR Foreign exchange transaction loss 6,000

16-1

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Thus, a $2,000 foreign exchange gain would be recognized in 2017 and a

$6,000 foreign exchange loss would be recognized in 2018.

E16-19. Adjustments and eliminations for consolidation under acquisition

method

(A) DR Common Stock $1,500,000

DR Retained Earnings 500,000

To eliminate Beta’s stockholders’ equity accounts against Alpha’s

(B) DR Fixed assets $300,000

To allocate the excess of the price paid for Beta’s shares ($2,000,000)

over Alpha’s proportionate interest in the book value of Beta’s net assets

(C) DR Fixed assets $75,000

DR Goodwill-noncontrolling interest 25,000

the consolidated balance sheet.

16-2

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Requirement 2:

Alpha Beta

Eliminations Consolidated

Dr Cr Balance Sheet

Assets

Current assets $ 1,750,000 $ 500,000 $2,250,000

$ 300,000

Common stock 7,000,000

0 1,500,000 A

00

Capital in excess of

par 500,000 0 500,000

Retained Earnings

1,000,00

0 500,000 500,000 A 1,000,000

Noncontrolling interest 400,000 A 500,000

100,000 C

16-3

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

16-4

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

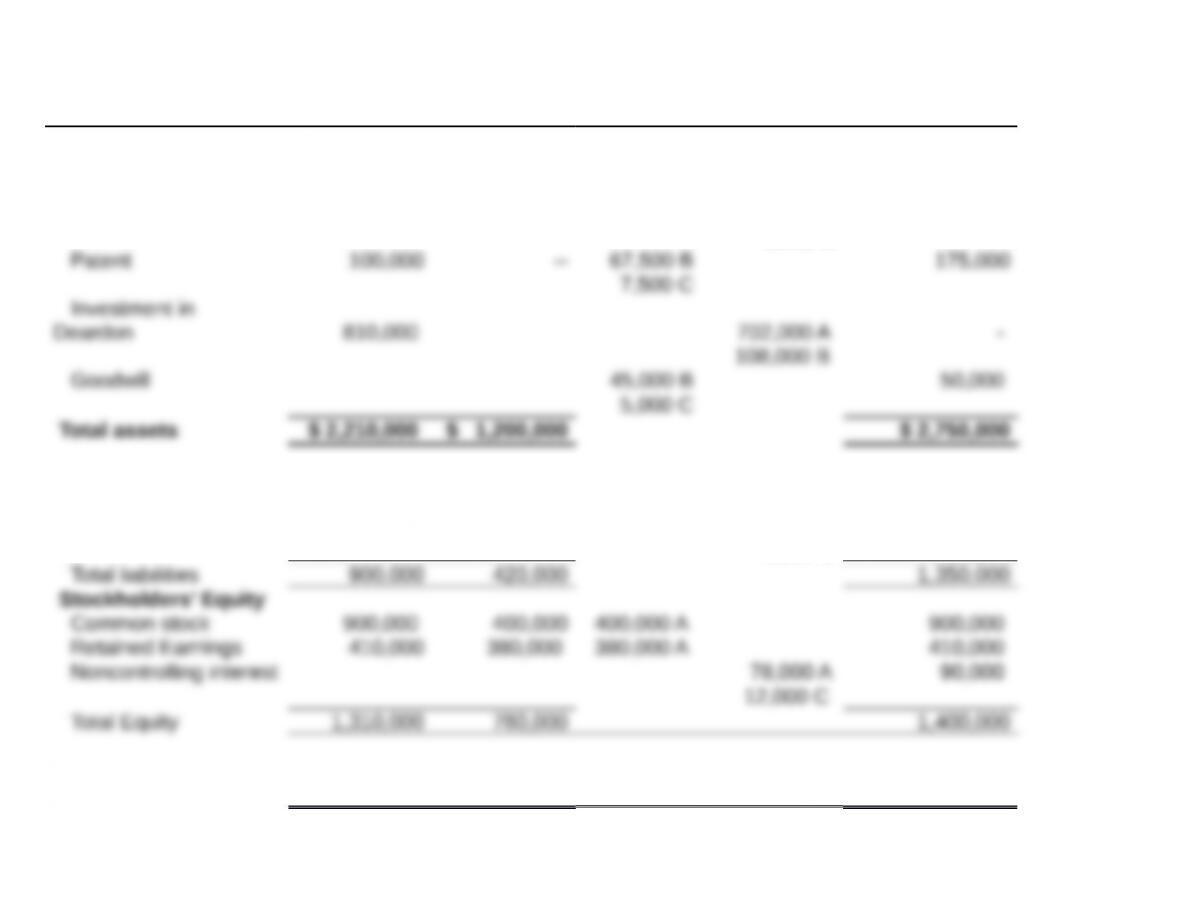

E16-20. Consolidation worksheet and balance sheet under acquisition method

Requirement 1:

The elimination entries that Chesapeake should make in its consolidated

worksheet are given below:

(A) DR Common Stock $ 400,000

To eliminate Deardon’s stockholders’ equity accounts against

Chesapeake’s Investment in Deardon account and set up Noncontrolling

CR Investment in Deardon 108,000

To allocate the excess of the price paid for Deardon’s shares ($810,000)

over Chesapeake’s proportionate interest in the book value of Deardon’s

(C) DR Current assets $5,000

DR Patent 7,500

DR Goodwill 5,000

To adjust the net assets of Deardon to reflect the full fair value at time of

Note that total noncontrolling interest is $90,000 ($78,000 (A) + $12,000

16-5

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Requirement 2:

Chesapeake Deardon

Eliminations Consolidated

Dr Cr Balance Sheet

Assets

Current assets $ 500,000 $ 400,000 $ 45,000 B $950,000

5,000 C

PP&E, net 800,000 800,000 $ 22,500 B 1,575,000

2,500 C

Liabilities

Current liabilities $ 400,000 $ 150,000 $ 550,000

Long term liabilities 500,000 270,000 $ 27,000 B

3,000 C 800,000

Total Liabilities

and Equity $ 2,210,000 $ 1,200,000 $ 955,000 $ 955,000 $ 2,750,000

16-6

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

16-7

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Financial Reporting and Analysis (7th Ed.)

Chapter 16 Solutions

Intercorporate Investments

Problems

Problems

P16-1. Equity method accounting

Requirement 1:

Figland’s equity in Irene’s earnings (40% x $600,000)

$240,000

Requirement 2:

Cost of initial investment $1,800,000

Investment income [see Requirement (1)] 175,000

P16-2. Accounting for trading securities

Requirement 1:

Desired balance in Fair Value adjustment account at

12/31/16:

DR

Previous balance before adjustment 0

16-8

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education.

CR Unrealized holding gain on trading securities

$5,000

Requirement 2:

DR Cash $14,000

DR Fair Value adjustment—trading securities 2,500

adjustment on 12/31/16 was determined as follows:

Cost of Co. B common stock $30,000

Fair value on 12/31/16 (25 ,000)

Fair value adjustment related to Co. B shares sold $2 ,500

Requirement 3:

Desired balance in Fair Value adjustment account:

12/31/17

Cost Fair Value

Co. A Common $50,000 $55,000

on 7/01/17 ($5,000 DR + $2,500 DR) 7 ,500

DR

Required adjustment to Fair Value adjustment account

$2,500

16-9

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education.

Requirement 4:

DR Cash $14,000

DR Realized loss on sale of available-for-sale

securities 1,000

of available for sale securities $2,500

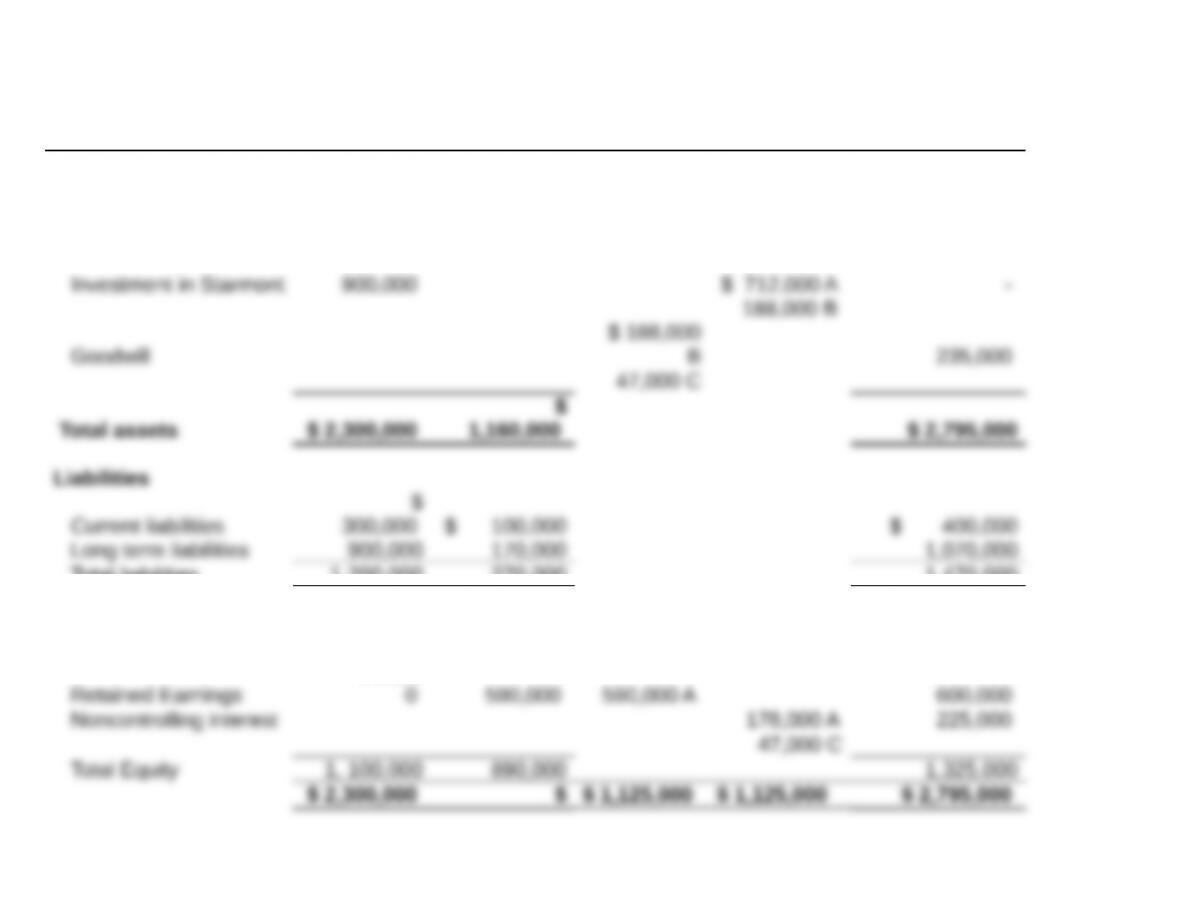

P16-3 Consolidated balance sheet and income statement

under acquisition method.

Requirement 1:

The consolidating balance sheet appears on the

following page.

16-10

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education.

Pate Starmont

Eliminations Consolidated

Dr Cr Balance Sheet

Assets

Current assets $ 400,000 $ 300,000 $700,000

Long term assets 1,000,000 860,000 1,860,000

Total liabilities 1,200,000 270,000 1,470,000

Stockholders’ Equity

Common stock 500,000 300,000 300,000 A 500,000

600,00

16-11

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Total Liabilities

and Equity 1,160,000

16-12

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

(A) To eliminate Starmont’s stockholders’ equity accounts against

$178,000.

(B) To allocate the excess of the price paid for Starmont’s shares

allocate is $188,000.

(C) To reflect the full fair value of goodwill at time of acquisition

Note that total noncontrolling interest is $225,000 ($178,000 (A)

Total goodwill is $235,000 ($188,000 (B) + $47,000 (C)), which

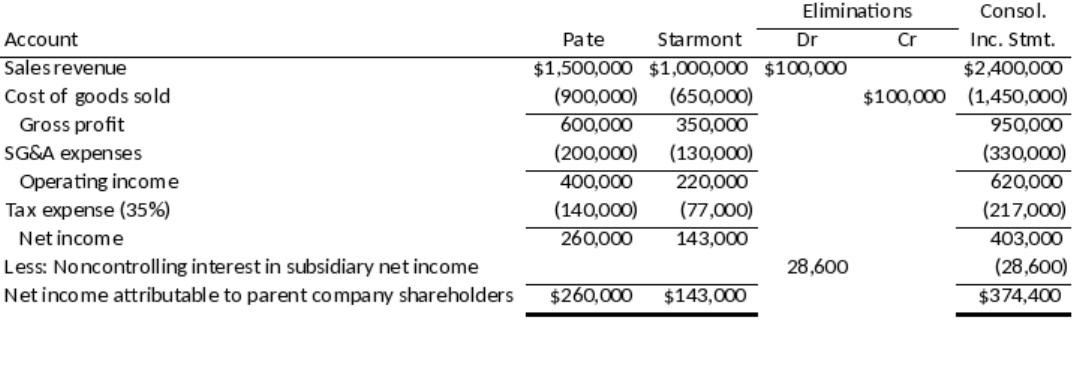

Requirement 2:

Intra-entity Sale:

The intra-entity sale from Pate to Starmont needs to be eliminated to

are eliminated against each other.

Income Allocated to Noncontrolling Interest:

Starmont’s tax expense is .35 x $220,000 = $77,000, so its net

16-13

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

adjustment required to income for the noncontrolling interest share of

Goodwill.

Consolidated Income Statement:

The 2018 consolidated income statement worksheet is as follows:

16-14

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.