Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

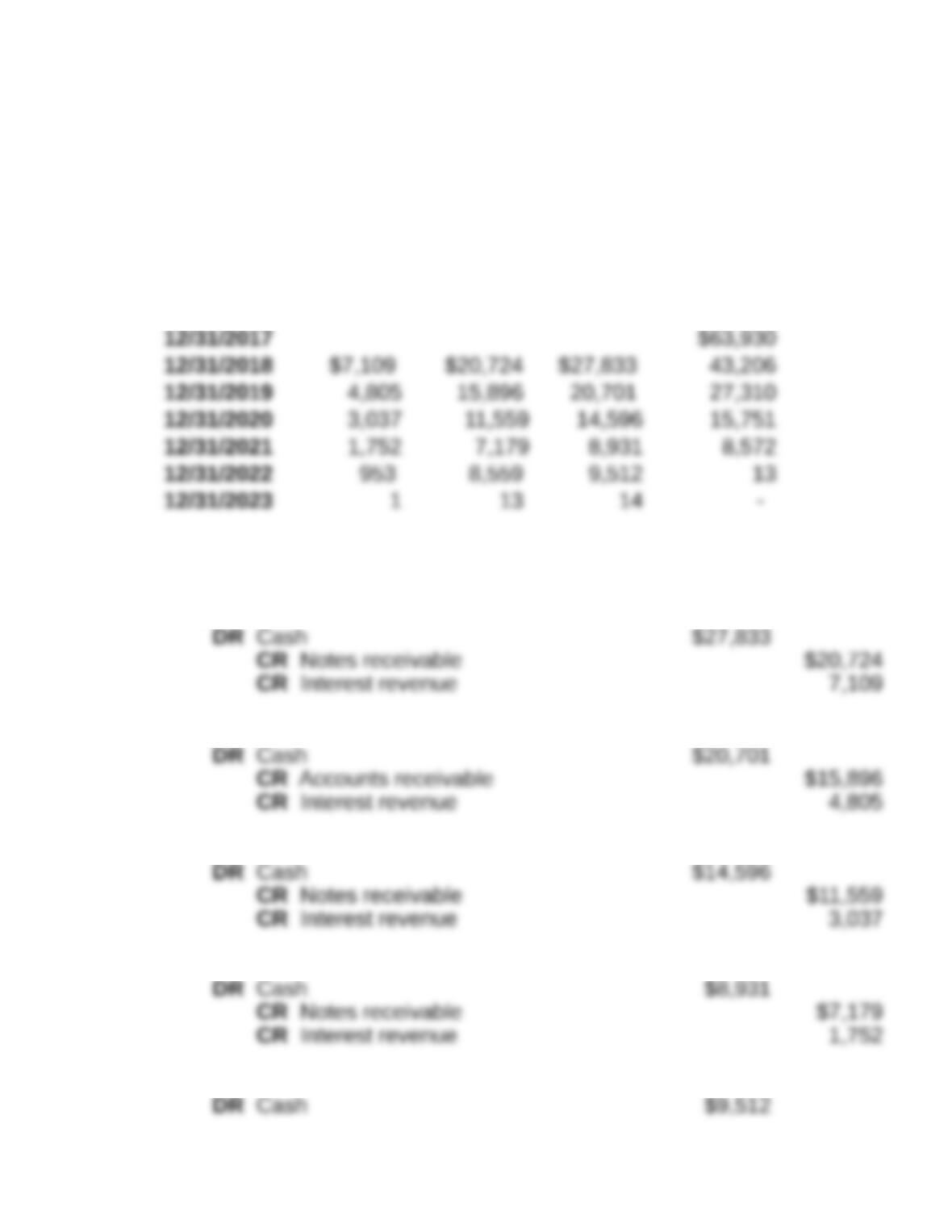

P8-7. Scheduling interest received (LO 8-4)

Effective interest table in 000’s

( a ) ( b ) ( c ) ( d )

Date

Interest

income -

prior (d) x

11.12%)

Note

payment

received

(given)

Total

cash

received

(a) + (b)

Note

receivable -

prior (d)

less (b)

12/31/2018:

12/31/2019:

12/31/2020:

12/31/2021:

12/31/2022:

12/31/2023:

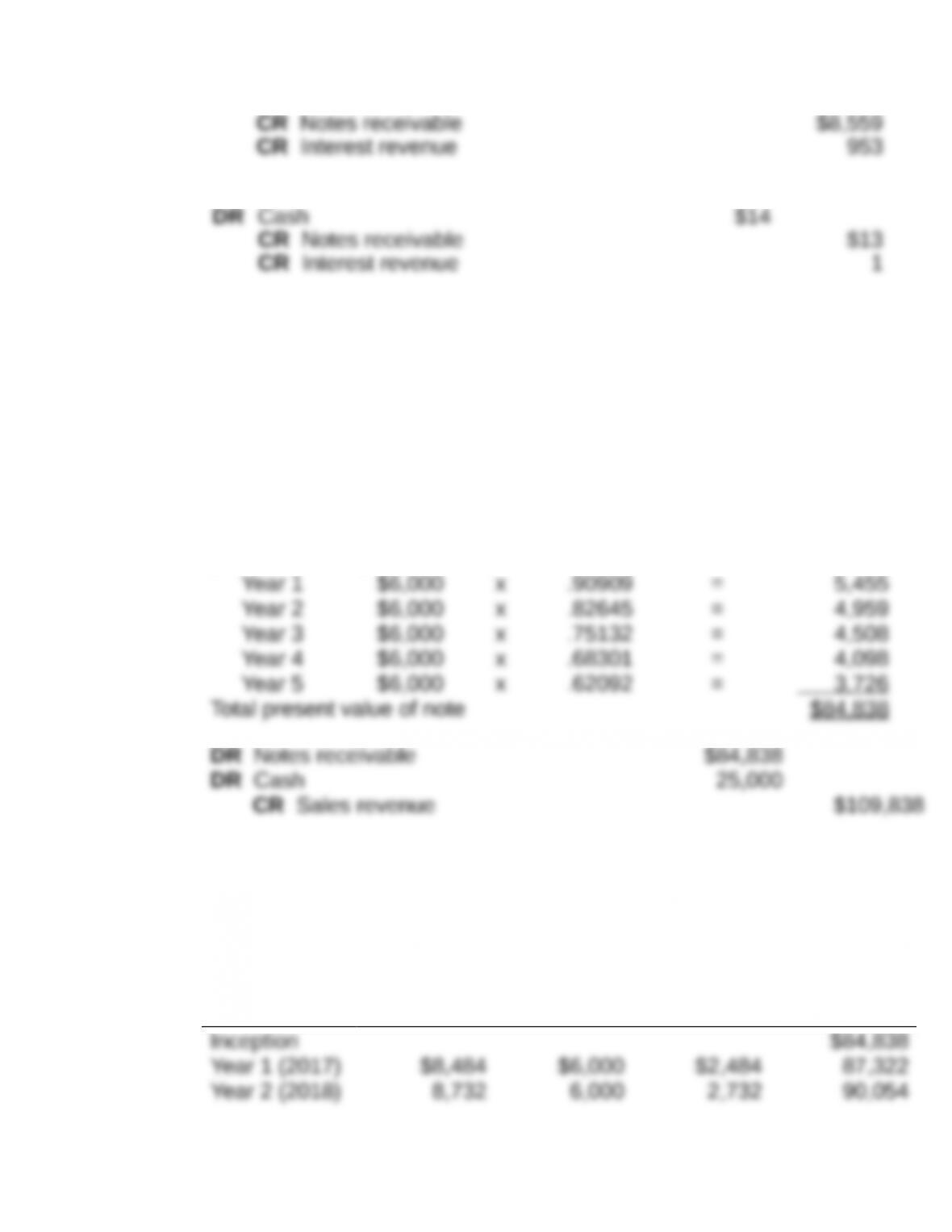

P8-8. Imputing interest on a nominal interest-bearing note and fair

value option (LO 8-4, LO 8-5)

Requirement 1:

Calculation of the present value of Criswell Acre’s note at a 10%

effective rate of interest:

Present value of $100,000 principal repayment in 5 years at 10%

$100,000 x .62092 = $62,092

Present value of five interest payments of $6,000

($100,000 x .06) each at 10%:

Requirement 2:

(a)

Interest

income—

10% of

column (d)

balance for

prior year

(b)

Cash

interest

received

(c)

Increase in

present

value of

note

(a)–(b)

(d)

End of year

present

value of

note

*Rounded

Requirement 3:

Requirement 4:

Calculation of the present value of Criswell Acre’s note at an 8%

effective rate of interest with 3 years until maturity:

Present value of $100,000 principal repayment in 3 years at 10%

Present value of three interest payments of $6,000

($100,000 x .06) each at 10%:

Total fair value of note at December 31, 2018 to be

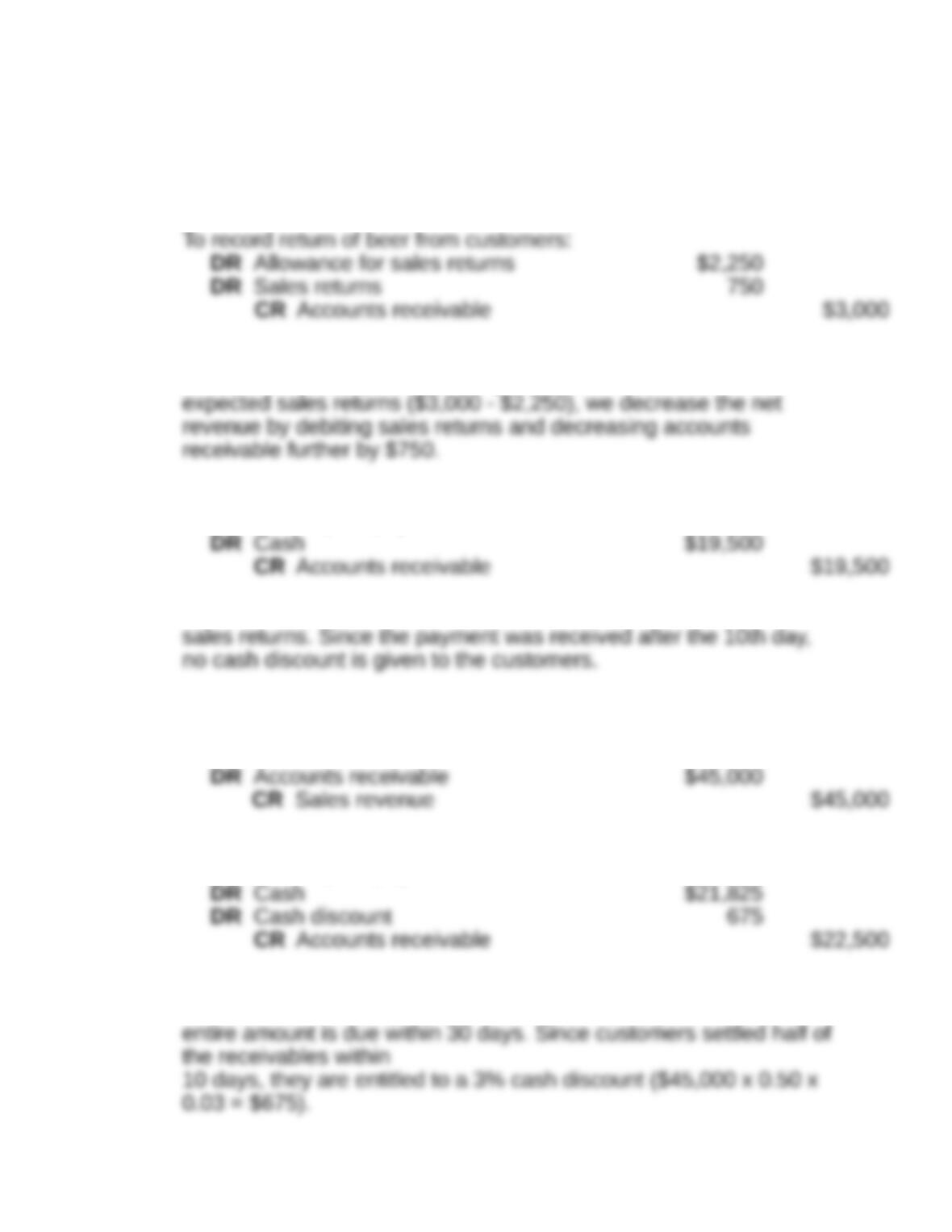

P8-9. Recording cash discounts and sales returns (LO 8-1)

Note to instructor: This problem covers cash discount/credit terms

not discussed in the chapter and, thereby, provides an opportunity

to introduce these issues.

Requirement 1:

1/1/17:

To record sale of beer:

DR Cash discount 675

Note: The credit terms “3/10, n/30” means that the customer gets a

3% cash discount for payment made within 10 days. However, the

1/15/17:

To record return of beer from customers:

Note: This reflects the actual return of goods that was anticipated

earlier.

1/28/17:

To record receipt of payment:

Note: Recall that expected sales returns of $2,250 were recorded

on January 1, 2017. However, since the actual sales returns were

only $2,000, we reverse the 1/1/17 journal entry to the extent of

$250.

Requirement 2:

Journal entries prior to January 15, 2017 are unaffected.

1/15/17:

Note: This reflects the actual return of goods to the extent it was

anticipated earlier ($2,250). For goods returned in excess of

1/28/17:

To record receipt of payment:

Note: Balance due is $22,500 ($45,000 x 0.50) minus $3,000 of

Requirement 3:

1/1/17:

To record sale of beer:

1/9/17:

To record receipt of payment:

Note: The credit terms “3/10, n/30” mean that the customer gets a

3% cash discount for payment made within 10 days. However, the

1/15/17:

To record return of beer from the customers:

Note: Since expected sales returns were not recorded, actual

returns decrease net revenue by a debit to sales returns.

1/28/17:

To record receipt of payment:

sales returns. Since the payment was received after the 10th day,

Requirement 4:

Assuming the company uses the calendar year as its fiscal year, all

transactions pertaining to the sale of beer took place within one

accounting period (sale of goods, return of goods, and collection of

cash). However, if sales revenue is recorded in one accounting

period and actual sales returns are recorded in the following period,

then the matching principle is likely to be violated. This problem is

Requirement 5:

If the customer decides to take advantage of the cash discount, the

optimal time to do this is on the tenth day (i.e., the customer does

30th day. (Once again, the customer does not obtain any benefit by

paying any sooner.) Consequently, to take

Given that its incremental borrowing rate is 18%, the customer

could borrow $21,825 and pay interest for 20 days (i.e., $21,825 x

18% x 20/365 = $215)—i.e., it has to pay $22,040 ($21,825 + $215)

on the borrowing. However, if it had waited for the entire credit

Another way to answer the question is to view the cash discount

($675) as the return on investment in accounts receivable ($21,825)

P8-10. Balance sheet effects of collateralized borrowing (LO 8-6)

Requirement 1:

Required journal entries

August 1:

(($260,000 - 160,000) x .005)

September 30:

(($260,000 - 160,000 - 80,000) x .005)

Less:

Requirement 2:

August 31 balance sheet

Note to instructor: This amount comprises the initial balance of

of $500.

Requirement 3:

August

1:

August 31:

September 30:

(($260,000 - 160,000 - 80,000) x .005)

Note to instructor: Subsequent cash remittances from the factor

will reduce the due from factor balance. Any remaining balance in

P8-11. Factoring receivables (LO 8-6)

Requirement 1:

To record the sale of receivables to the factor:

Calculation of the proceeds from the factor

Since the factor is responsible for all the bad debts on the factored

receivables, the allowance for uncollectibles with respect to these

In essence, the loss on sale of receivables represents several

different income statement items. While there is loss of information

Note that the entire Interest expense has been recorded at the time

of sale as part of the loss amount. However, for long-term

Effect on statement of cash flows: The $176,000 received from the

factor will also show up as part of operating cash flows. Since the

An alternative approach is to separately show the three components

included in the loss on sale of receivables as follows:

The debit to the allowance for uncollectibles and the credit to the

bad debt provision represent the reversal of the journal entry for bad

debt provision on the $200,000 of the factored receivables. The

The loss on sale of receivables in the original journal entry is now

decomposed into two debits (to interest expense and factoring fee)

Requirement 2:

To record return of $3,000 of merchandise:

Requirement 3:

To record receipt of payment from the factor:

The actual bad debts incurred by the factor were $7,500.

Atherton will not record a journal entry to record this event. Recall

that the receivables were sold without recourse for bad debts, in

which case, the factor is responsible for all the bad debts. In the

given scenario, the actual bad debts of $7,500 were more than the