P6-8. Assigning credit ratings using financial ratios

Requirement 1:

Standard & Poor’s credit analysts would probably assign a credit

Requirement 2:

Requirement 3:

All of the financial ratios for Firm 3 tilt toward the median values for

AAA rated companies when compared to those of Firm 2.

P6-9. Calculating value creation by two companies

Requirement 1:

The abnormal earnings of the two firms for 2013–2017 appear

below.

Company A 2013 2014 2015 2016 2017

Company B

Requirement 2:

Company B created value each year via positive abnormal

Requirement 3:

The return investors earn from a stock depends on the

difference between what must paid to buy the stock—it’s cost

or current market price—and what it will ultimately be worth at

How do these notions apply to company A and B? Company B

has clearly outperformed Company A during the years shown.

Let’s assume that this favorable performance difference is

expected to continue into the future. The performance

differences between A and B are likely to be already reflected

P6-10. Making credit rating changes

Requirement 1:

The company’s credit risk has increased since the first quarter of

Requirement 2:

Standard & Poor’s analysts are likely to assign a credit rating of AA

Requirement 3:

There is a gradual deterioration in credit worthiness throughout

Credit risk deteriorates even further in the second quarter of 2017.

Standard & Poor’s analysts might have concluded that the credit

P6-11. ENRON: Fair value accounting

Requirement 1:

There are several features of the Bravehart structure that were

essential to achieving the fair value accounting profit boost. First,

Enron needed to isolate the Blockbuster contract in a separate

entity (Bravehart partnership) so that the investment bank loan was

not viewed as an Enron obligation and thus as Enron debt. Second,

Enron’s investment in the Bravehart partnership had to be

structured such that consolidation was not required. Back in the

The final piece required for the profit boost involved “monetizing” the

Enron-Blockbuster contract with the aid of an investment bank. The

effectively established the contract’s fair value at $115 million, which

also meant that Bravehart must have a fair value of about $115

million ($115 million for the contract plus $115 million cash from the

Requirement 2:

There are two critical judgments required to estimate the bank

guarantee’s fair value: (1) what is the likelihood that Bravehart will

default on the loan and cause the bank to seek payment directly

from Enron? and (2) how much of the loan balance will be unpaid at

Requirement 3:

Enron’s mark-to-market adjustment to the Bravehart investment

would then have been just $15 million, the difference between

Requirement 4:

This would be an extraordinarily challenging audit task because the

fair value measurement occurs at Level 3, and thus relies on

unobservable inputs. The auditor could turn to independent

estimates of the future net cash flows for the Enron-Blockbuster

contract, but the only third party estimates available would be those

P6-12. Calculating sustainable earnings

Requirement 1:

The original income statements for 2011–2014 appear on the next

page along with the calculation of sustainable earnings for each of

the three years. Except for the transitory revenue of $1 billion in

2014, which was given in the case, all of the adjustments required

Requirement 2:

An interesting conclusion emerges when reported earnings are

compared with sustainable earnings. While the firm’s reported

earnings increased each year from 2011 to 2014, its sustainable

Colonel Electric Inc. (in millions of $) As Reported Earnings Sustainable Earnings Calculation

For Years Ended December 31, 2016 2015 2015 2016

Revenues

Cumulative loss (+ gain) from change in

accounting methods (net of tax) ___(110) 0 _____55 ______0

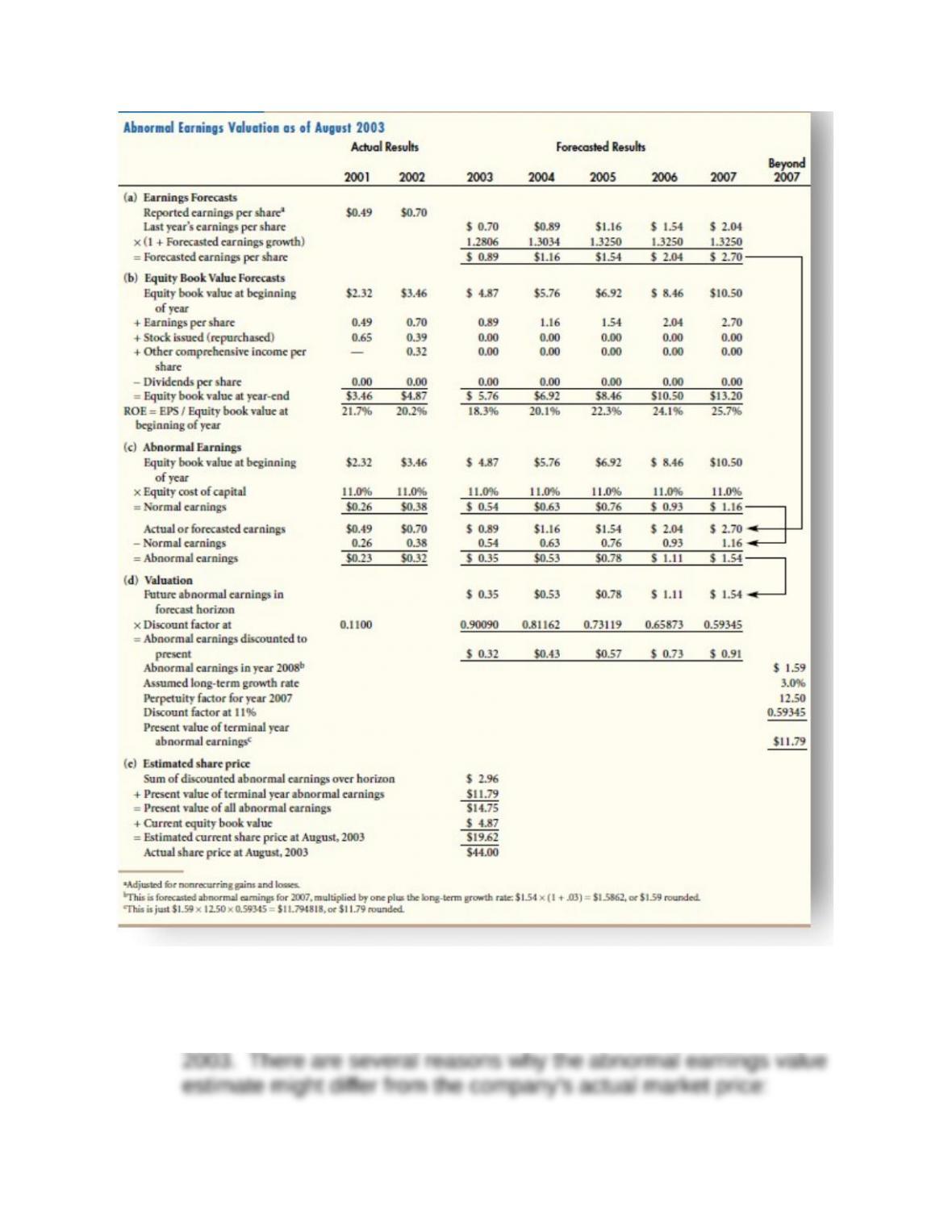

P6-13. Krispy Kreme Doughnuts: Valuing abnormal earnings

Requirement 1:

Requirement 2:

The value estimate from requirement 1 ($19.62 per share) is

substantially below the market price of the stock ($44.00) in August

Investors may be more optimistic about the company’s profit

Investors and analysts may agree about EPS forecasts over the

next five years, but the terminal growth assumption (3.0%) used

We may have assigned the company a cost of equity capital

that is too large. Given the forecasts used in the valuation

model, a 7% cost of capital (discount rate) will yield a value

The most interesting possibility is that the stock is “overvalued”

at $44 per share. Why might this occur? One reason is that

It is interesting to note that 9 months later (May 2004) the stock was

trading at about $20 per share.