P3-11. Right of return

Berger applies the variable consideration analysis, which indicates that

$200,000 – $10,000 – $2,000 = $188,000 is its best estimate of the amount it

will be entitled to receive related to 2019 sales. First Berger records the initial

sale of $200,000, allowing for $12,000 in returns:

Berger records cost of goods sold related to the sales revenue it recognized.

Because Berger has not recognized sales revenue on the $12,000 of sales it

expects to be returned, it does not recognize cost of goods sold related to it.

CR Inventory

When the $10,000 of returns are made, Berger records the following entry:

CR Cash

Berger also reinstates the inventory that is returned, eliminating a portion of the

Inventory recovery asset. The inventory that was returned had a cost of

CR Inventory recovery asset

3-1

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

P3-12. Determining distinct performance obligations

Requirement 1:

The transaction price is $425,000, the consideration to which Sapra expects

to be entitled.

Requirement 2:

There are two performance obligations. The issue here is whether Gao can

benefit from each of the machines independently of the other. If so, there are

two distinct performance obligations. Because the machines are used

Requirement 3:

Because the two machines are distinct performance obligations, Sapra

determines when it is appropriate to recognize revenue for each of them

P3-13. Bill-and-hold

Revenue may be recognized under a bill-and-hold arrangement only if all of the

following criteria are met:

The reason for the arrangement is substantive.

3-2

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

In scenario 1, the product is not separately identified as belonging to

In scenario 2, although the product has been labeled for Christiansen,

Gallemore is able to sell the product to another customer and replace

In scenario 3, all of the above criteria are met, so Gallemore may recognize

revenue, even before physically transferring the product. In this case, it is clear

P3-14. Gift cards with breakage

Requirement 1:

Maffett expects the gift cards to be used eventually to make purchases totaling

$250,000 x 99% = $247,500. In 2019, they were used to make purchases of

Note that Breakage revenue may be recognized only to the extent it is probable

a reversal will not be necessary.

Requirement 2:

If state law requires unused gift card proceeds to be remitted to the state under

escheat laws, breakage revenue is not recognized. Instead, Maffett would

make the following entries:

3-3

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

When the gift cards expire, there will still be a balance in the liability. The

P3-15. Contract acquisition costs

Requirement 1:

Installation of the satellite dish is not a distinct performance obligation. The

customer cannot benefit from the installation of the dish without also

subscribing to the service. That interrelationship indicates there is a single

Requirement 2:

The cost of installing the dish is a contract acquisition cost – it is an

incremental cost incurred to secure the contract. The cost is amortized over the

P3-16. Customer options

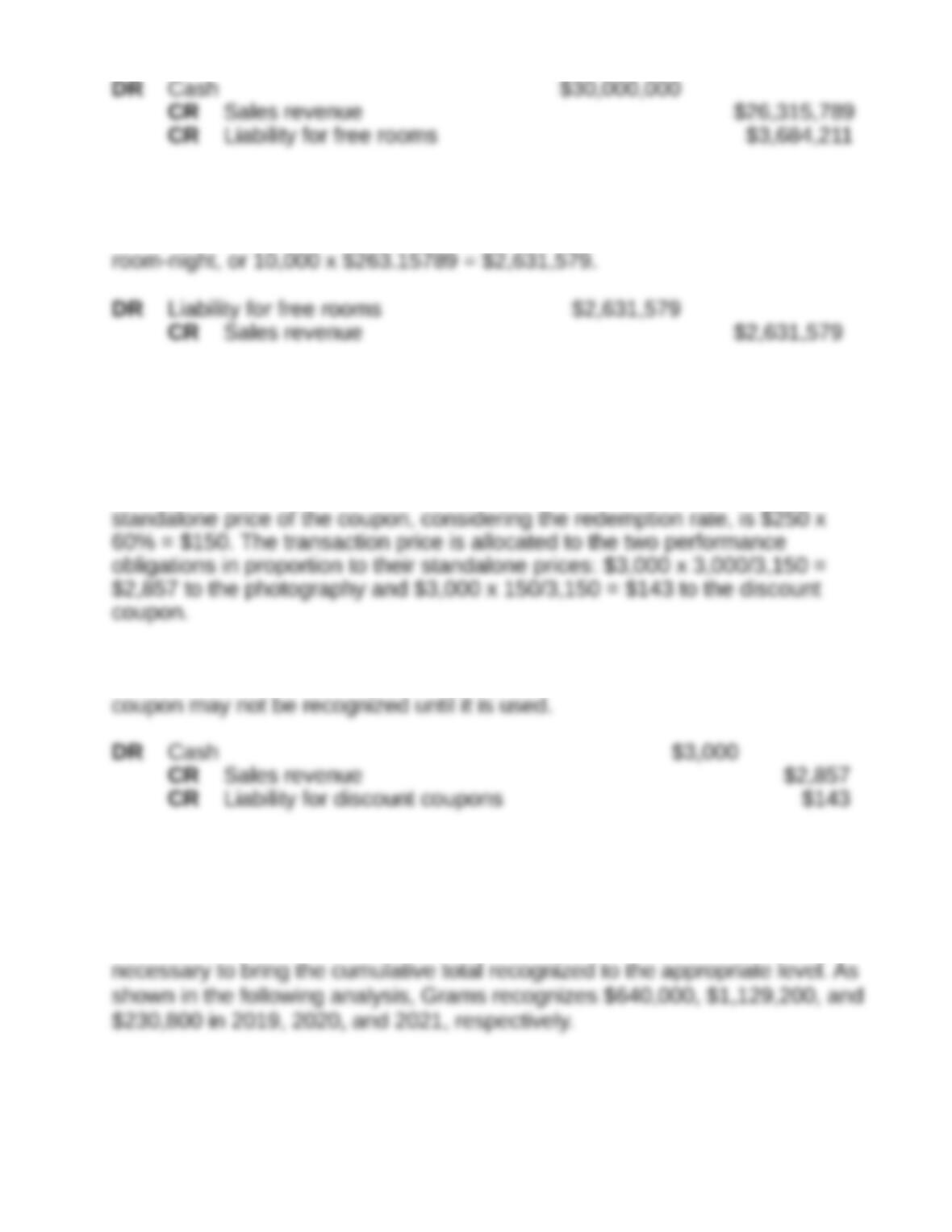

The 100,000 paid nights generate an expected number of free nights of

100,000 / 5 x 70% = 14,000. So, the room purchases customers made in 2019

constitute two performance obligations – 100,000 paid nights and 14,000 free

nights. Each room-night has a standalone price of $300, so the aggregate

standalone prices are $30 million for the 100,000 paid nights and $300 x

Revenue may be recognized immediately on the paid nights. The journal entry

to record the 2019 purchases is as follows:

3-4

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

During 2019, 10,000 free room nights were redeemed. Revenue may be

recognized on those rooms and the related liability is relieved. The amount of

revenue recognized is 10,000 times the amount associated with each

P3-17. Customer options

There are two performance obligations – the photographing of the wedding and

the printing of images. For $3,000 the customer gets the wedding

photographed, with a standalone price of $3,000 and a discount coupon. The

The revenue related to photographing the wedding may be recognized when

the service is provided to the customer, but revenue related to the discount

P3-18. Revenue recognition over time

At the end of each year, Grams must determine the cumulative amount of

revenue that may be recognized and recognize the amount in the current year

3-5

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

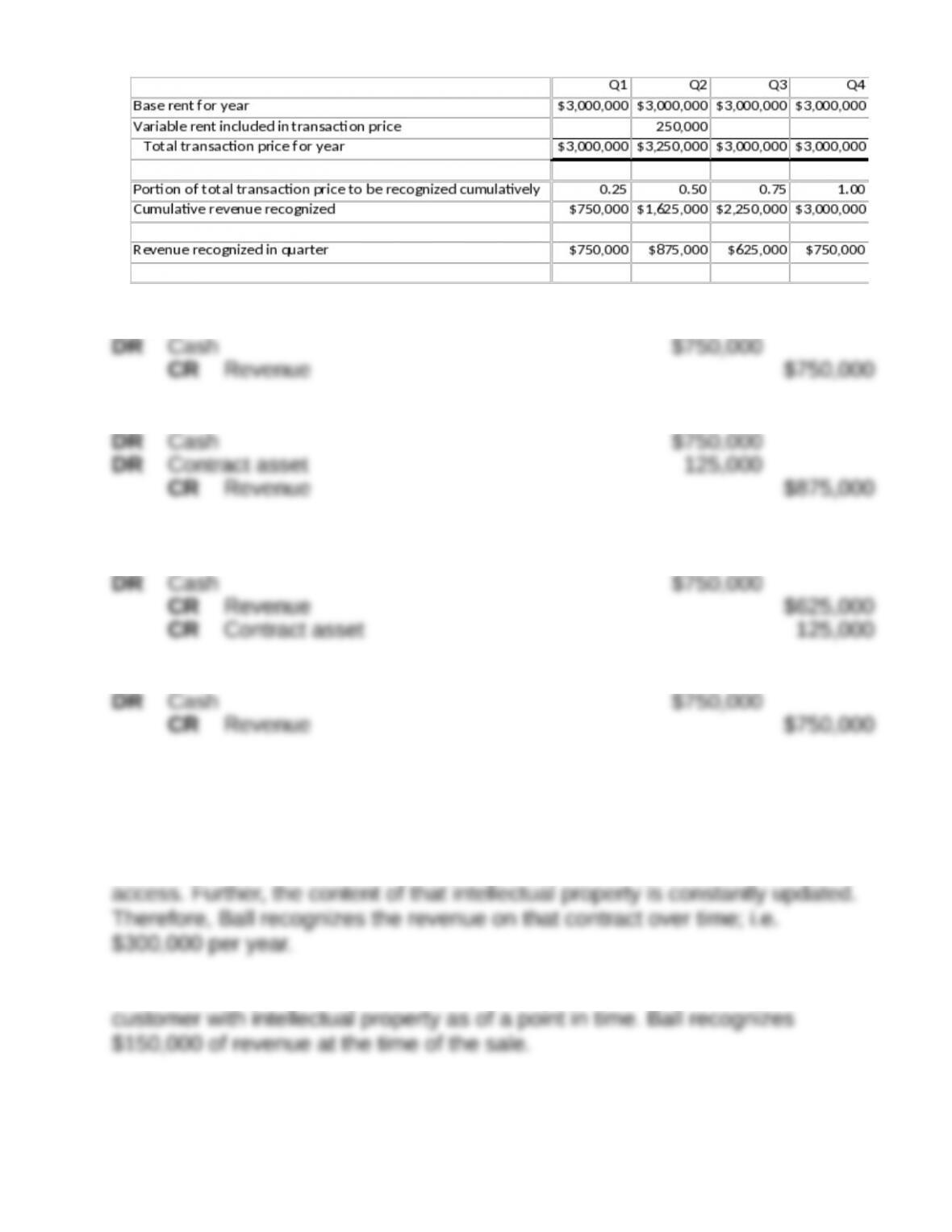

P3-19. Variable revenue

At the end of each quarter, Skinner must assess the variable consideration to

determine the transaction price. As circumstances change, the transaction

price may be adjusted.

At the end of the first quarter, there were two outcomes for the variable portion

of the revenue, with a 40% chance of receiving an additional $250,000 and a

At the end of the second quarter, there was a 90% probability of receiving the

At the end of the third and fourth quarters, there was a zero probability of

3-6

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Quarter 1:

Quarter 2:

Quarter 3:

Quarter 4:

P3-20. Revenue recognition at a point in time and over time

In the first situation, where Ball sells access to a real-time data base, Ball has

granted the right to access its intellectual property as it exists at the time of

In the second situation, where Ball sells historical data, it has provided the

P3-21. Payments to customers

3-7

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Because the in-store advertising has no readily determinable market value, the

payment for it is considered a price discount on the sale of goods. Therefore,

P3-22. Revenue recognition over time

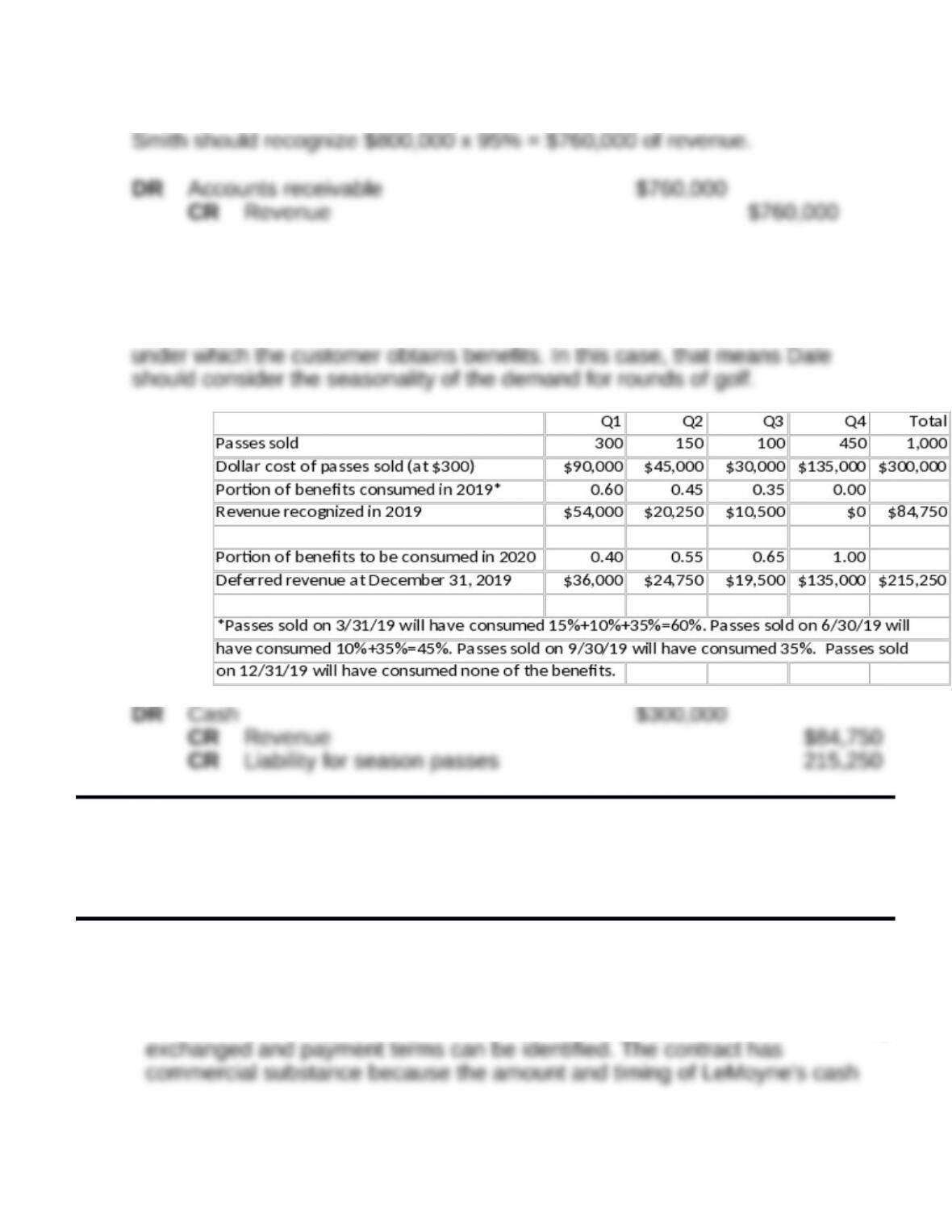

In recognizing revenue over time, Dale should take into account the pattern

Financial Reporting and Analysis (7th Edition)

Chapter 3 Solutions

Revenue Recognition

Cases

C3-1. Applying the 5-step model

Step 1: Identify the contract(s) with a customer.

Both parties are legally obligated to perform their obligations. The items being

3-8

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Step 2: Identify the performance obligations in the contract.

There is a single performance obligation. Franklin will not benefit from

Step 3: Determine the transaction price.

The contract has a variable consideration component. LeMoyne must

consider the probability that it will be entitled to the additional $100,000. As

there are two possibilities (it will or it will not be entitled to the $100,000), it

Step 4: Allocate the transaction price.

Step 5: Recognize revenue when (or as) the entity satisfies a

performance obligation.

LeMoyne must determine whether revenue is to be recognized at a point in

time or over time. To recognize revenue over time, one of the following criteria

must be true:

The customer simultaneously receives and consumes the goods and

The first two criteria are not met. The customer does not benefit from the

work as it is done. The building is of no use until it is complete. Further, the

C3-2. Analyzing the reason for a practical expedient

It would be difficult, if not impossible, for firms to determine what their

estimates would have been for variable consideration at various dates. And,

even if those estimates could be replicated, they are just that – estimates –

3-9

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

and certainly not as precise as using the actual consideration that resulted

Not including the practical expedient would have made the retroactive

C3-3. The meaning of control

The controller’s interpretation of control is more consistent with the meaning

of control under ASC paragraph 606-20-25-25. One of the criteria for having

In addition, Wilson has none of the other characteristics described in ASC

paragraph 606-20-25-25 as indicating control. Wilson may not use the asset

C3-4. Existence of a contract

ASC Topic 606 applies to contracts with customers, and it defines a customer

as “(a) party that has contracted with an entity to obtain goods or services

When multiple products are the output of a production process, one or more

of the outputs might be considered a by-product, or they might be considered

3-10

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

The metal shavings are likely to be considered a by-product. That is,

Robertson is not in the business of producing metal shavings. Rather, it is in

3-11

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.