C13-4. ABC Inc.: Interpreting tax notes and reconciling statutory and

effective rates

Requirement 1:

Tax Amount Tax Rate

The expense at the statutory rate is calculated by multiplying the

earnings before income taxes of $10,891 by 35%. The tax effects of

amortization of goodwill (or cost in excess of net assets of acquired

companies) and state taxes are given in the problem. The effect of

Requirement 2:

The credit to the income tax liability represents the current portion of

the income tax expense. The decrease in the deferred tax asset

Requirement 3:

13-1

The decrease in the deferred tax asset for accounts receivable

The deferred tax asset for inventories is due to additional costs

inventoried for tax purposes and financial statement allowances. It

appears that certain costs that are considered as product costs for tax

purposes are treated as period costs for financial reporting purposes.

In addition, it seems that certain writedown of inventories (financial

statement allowances) are not allowed for tax purposes until the loss

due to writedown of inventories is realized through the sale of

The deferred tax asset for employee benefits suggests that the

company is using the accrual basis for expensing the cost of

employee benefits in the financial statements while using the cash

basis for tax purposes. The decrease in the deferred tax asset for

employee benefits suggests that ABC Inc. paid more of the employee

benefits in cash when compared to the tax expense during 2017.

The reduction in the deferred tax asset for accrual for costs of

restructuring is consistent with the current payment for restructuring

charges that were accrued in the GAAP income statement of the

The deferred tax asset for accrual for disposal of discontinued

operations was created to record the expected tax benefit from the

loss on discontinued operations reported in the GAAP financial

13-2

Since the company reports a deferred tax liability for plant and

equipment, it must mean that ABC Inc. is using a more accelerated

depreciation for tax purposes compared to the financial reporting

depreciation. However, the decrease in the deferred tax liability

C13-5. Understanding tax note disclosures

Requirement 1:

($ in millions)

Requirement 2:

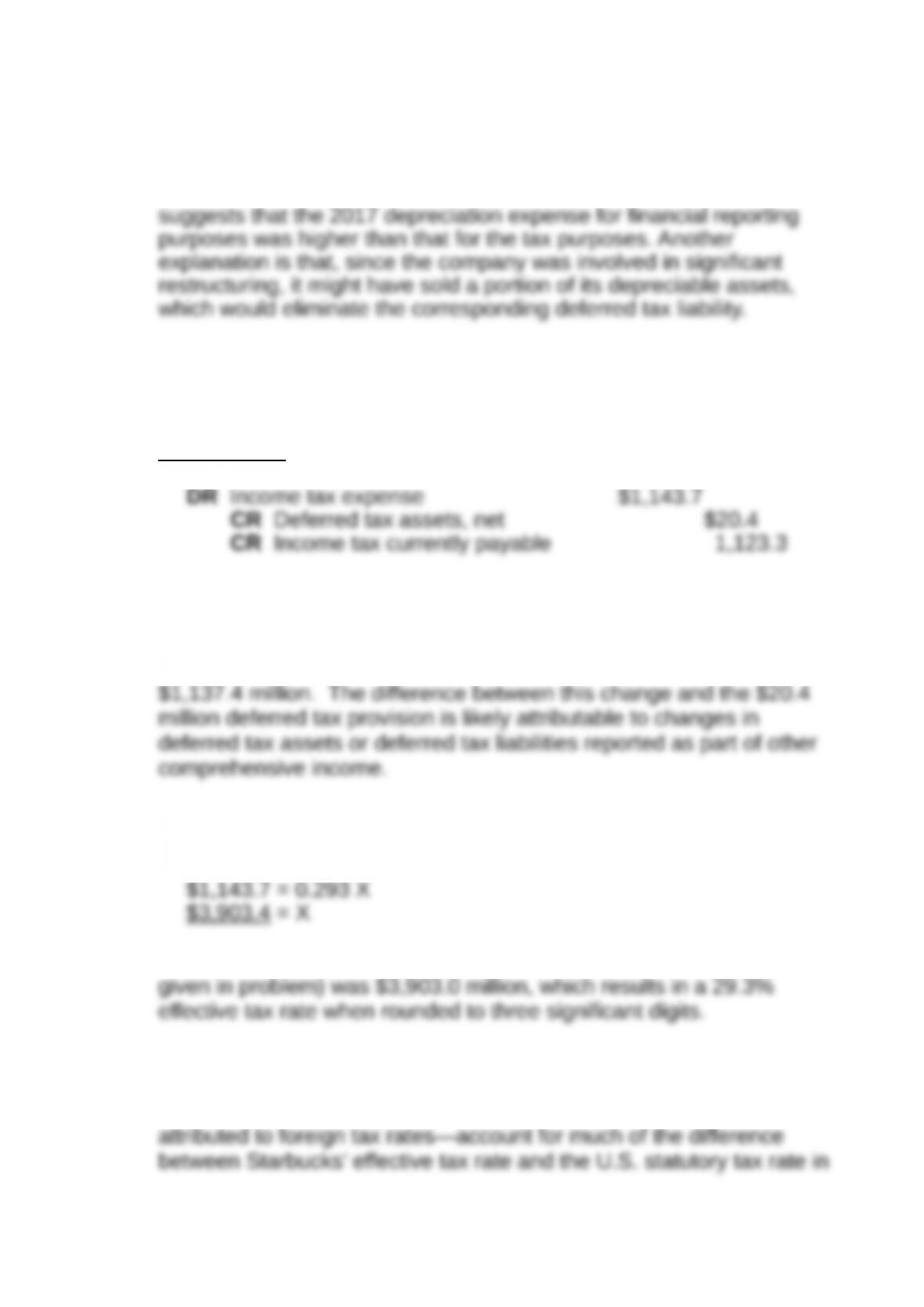

Starbucks deferred $20.4 million in taxes in fiscal 2015. This deferral

resulted in a decrease in net deferred tax assets. Note that net

deferred tax assets declined by $72.2 million, from $1,209.6 million to

Requirement 3:

Let X = earnings before taxes ($ in millions):

Note to the instructor: Starbucks’ actual earnings before taxes (not

Requirement 4:

The tax jurisdictions in which the firm chooses to operate—indicated

by the 2.1 percentage point reduction in the effective tax rate

13-3

The domestic production activities deduction reduces the effective tax

rate for domestic activities deemed to be production, as defined by the

law. Although it may not seem that Starbucks’ products would fall

under this category, which is essentially a manufacturing process, as

Starbucks recorded a gain on the acquisition of a joint venture, under

Requirement 5:

Starbucks’ effective tax rate in the year ended September 27, 2015

was 29.3% However, had it not been for the gain on the joint venture

purchase, the effective tax rate would have been 3.7% higher, or

33.0%, down only slightly from the prior year (34.6%). It is not

Requirement 6:

According to the tax rate reconciliation, the litigation charge reduced

the income tax provision by $1,071.0 million. Further, the effective tax

Note to instructor: The actual pretax litigation charge reported in the

C13-6. Using tax note disclosures to forecast next year’s tax

provision

13-4

Requirement 1:

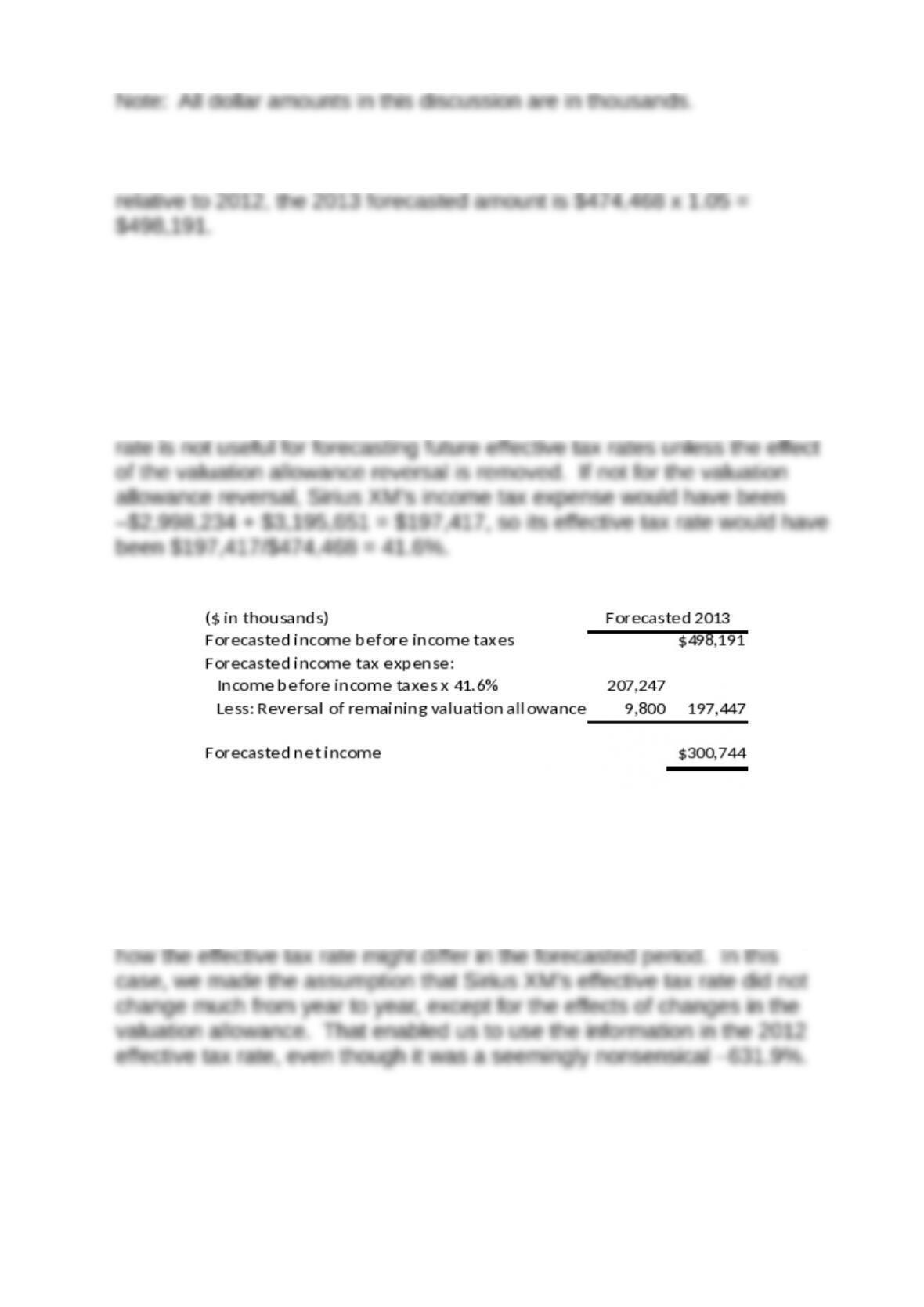

Given an assumption that income before income taxes will grow by 5%

Requirements 2 and 3:

The effective tax rate is income tax expense divided by income before

income taxes. Sirius XM’s 2012 effective tax rate was –$2,998,234 /

$474,468 = –631.9%. This very unusual effective tax rate arises because

of the reversal of the valuation allowance. As a result, this effective tax

Requirements 4 and 5:

Note: Effective tax rates are often stable from one period to the next for a

particular company. However, aberrations may occur that alter the

effective tax rate in a particular year. It is still possible to use the

information in the effective tax rate to forecast subsequent period income

tax expense by undoing the effect of the aberration and also considering

C13-7 Interpreting uncertain tax position disclosures

Requirement 1:

13-5

Requirement 2:

Requirement 3:

The note says the total liability for unrecognized tax benefits is $31.3

million and the table, which excluded interest and penalties, indicates

it is about $28.353 million. $31.3 million minus $28.353 million, or

C13-8: Tax note under IFRS

Requirement 1:

Lufthansa does not report a separate valuation allowance because

valuation allowances are not used under IFRS. Instead, a single-step

Requirement 2:

Lufthansa was not able to capitalize €498 million of deferred tax assets

because management did not deem it likely that those assets would be

Requirement 3:

Lufthansa reported a €135 million decrease (633–498) in the amount of

deferred tax assets it believes will not be realized. This likely indicates

Lufthansa expects relatively larger future taxable profits that will allow it to

13-6

13-7