Financial Reporting and Analysis (7th Ed.)

Chapter 9 Solutions

Inventories

Cases

Cases

C9-1. Daimler AG: Identifying differences and similarities between

IFRS and GAAP (LO 11)

Similarities

1. As a manufacturer, Daimler reports separate values for raw

2. Daimler uses a cost flow assumption – average cost

3. Costs include all expenditures related to acquisition and bringing

Differences

1. Daimler defines market as net realizable value, but in 2015, U.S.

GAAP defined market as the middle value of replacement cost,

net realizable value, or net realizable value less normal markup.

C9-2. General Electric: Interpreting a LIFO note (LO 5, 6, 7)

Requirement 1:

What are the total tax savings as of 12/31/Year 3 that GE has

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 9-1

Total tax savings $212.1

Requirement 2:

What would GE’s pre-tax earnings have been in Year 3 if they had

been using FIFO?

Requirement 3:

What 12/31/Year 3 balance sheet figures would be different and by

how much if GE had used FIFO?

Difference

Requirement 4:

LIFO liquidation profits in Year 3.

Requirement 5:

LIFO reserve on 1/1/Year 3 $676

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 9-2

So FIFO pre-tax income would have been $70 million lower

C9-3. ExxonMobil: Interpreting a LIFO footnote (LO 5, 6, 7)

Requirement 1:

Change in LIFO reserve (in billions):

Because the LIFO reserve decreased, FIFO income (after-tax) would

Requirement 2:

LIFO reserve (in billions) as reported at

Requirement 3:

Exxon-Mobil paid more in income tax by being under LIFO because of the

decline in prices and the liquidation. The extra tax is computed as follows:

Requirement 4:

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 9-3

To answer this part, we must determine the change in the LIFO reserve

after adding back the reserve decrease because of the LIFO liquidation:

Therefore, the estimated rate of price change for Exxon-Mobil’s inventory in 2014

was:

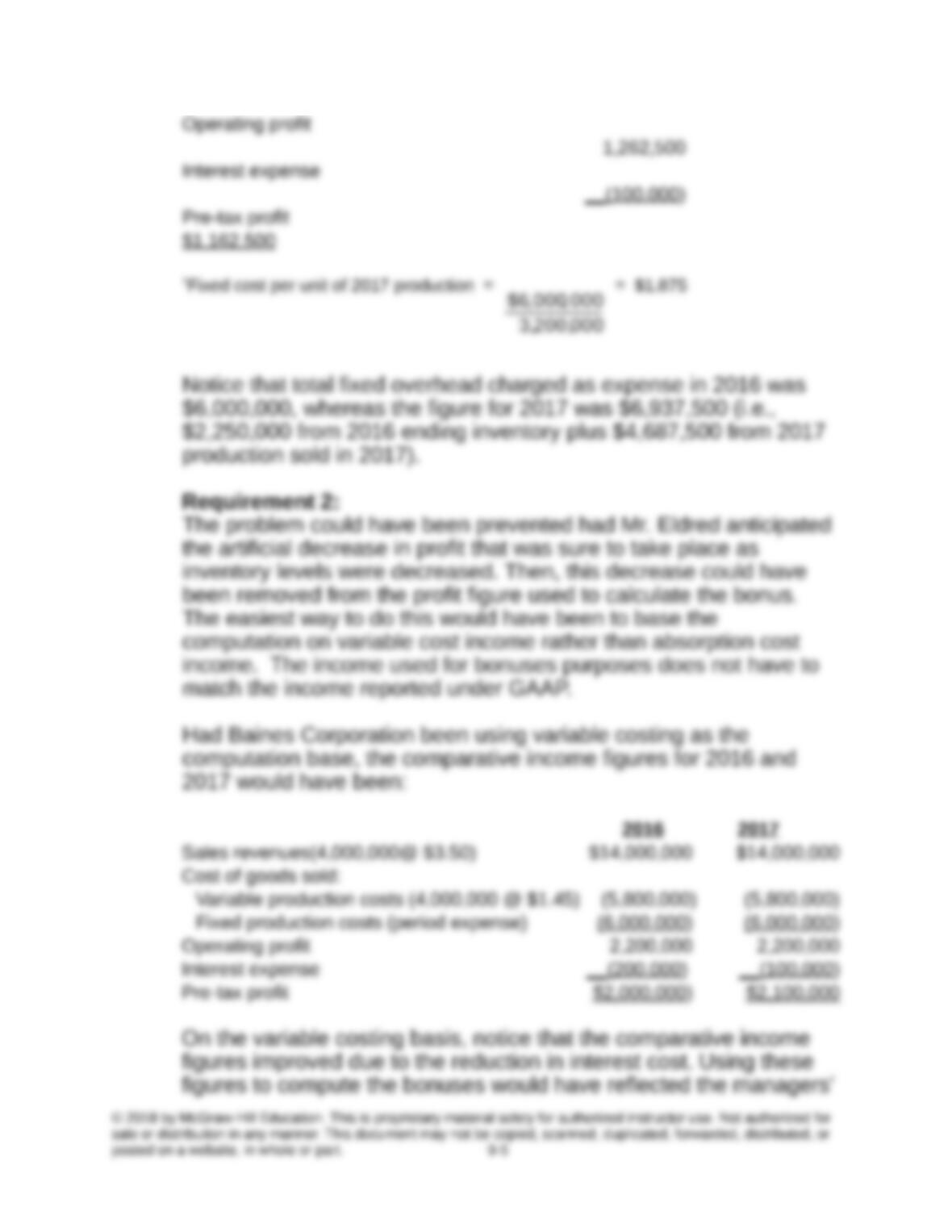

C9-4. Baines Corporation: Using absorption vs. variable costing (LO

12)

Requirement 1:

The mood of the management team undoubtedly changed because

of the considerable decline in 2017 pre-tax profit and, thus, in 2017

bonuses. Since sales and costs remained constant at 2016 levels,

937,500)

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 9-4

excellent efforts in controlling inventories. The compensation

committee could have overridden the bonus formula because of the

A suspicious view might suggest that Mr. Eldred, the president,

knew more about absorption costing than did his management

C9-5. Consequence of IFRS adoption (LO 4, 7, 11)

1. Currently, the LIFO Conformity rule does not allow firms to elect LIFO

for tax reporting unless they use LIFO for financial statement

reporting. IFRS disallows LIFO, so Chevron anticipates it will lose its

2. U.S. Congress has the authority to change tax laws. Therefore, it

could remove the LIFO Conformity rule and thereby allow firms to

report other-than-LIFO for financial statements and retain LIFO for tax

purposes. The SEC does not have the authority to alter tax laws, but

does have the authority to alter the enforcement of financial reporting

C9-6. Caterpillar: Interpreting a LIFO footnote (LO 5, 6, 7)

Requirement 1:

Change in LIFO reserve (in millions):

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 9-6

Requirement 2:

Requirement 3:

Requirement 4:

Requirement 5:

Appendix 9B on Dollar-Value LIFO provides more insights on how price

changes and inventory quantity changes affect the LIFO reserve.

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 9-7