Requirement 1: Annual pension expense

Assumptions: Discount rate = 8% and rate of return on plan assets = 10%

End of

Year

1

Annual

Salary

2

Cumulative

Salary

3

Total Vested

Pension

4

Vested

During the

Year

5

Discount

Period

6

PV Factor

7

PV of

Total Vested

Pension

8

2017 $50,000 $ 50,000 $12,500 $12,500 4 0.73503 $ 9,187.87

*Rounded

Note that the pension fund investments and earnings will be identical

earnings is not reported again.

Service Interest Return on Pension

Year Cost Cost Plan Assets Expense

2017 $ 9,187.87 – – $ 9,187.87

$52 ,475.74

Requirement 2: Funded status under 8% discount rate

End of Year 2017 2018 2019 2020

Projected benefit obligation $9,187.87 $21,830.39 $38,580.25 $60,185.19*

*Rounded

Pension Liability

(Asset) at Year-End 2017 2018 2019 2020 2021

Beginning balance – $ 712.87 $ 1,507.89 $ 1,225.50 $1,094.96

Ending balance $ 712.87 $ 1 ,507.89 $ 1 ,225.50 $ 1 ,094.96 ($ 0.00 )

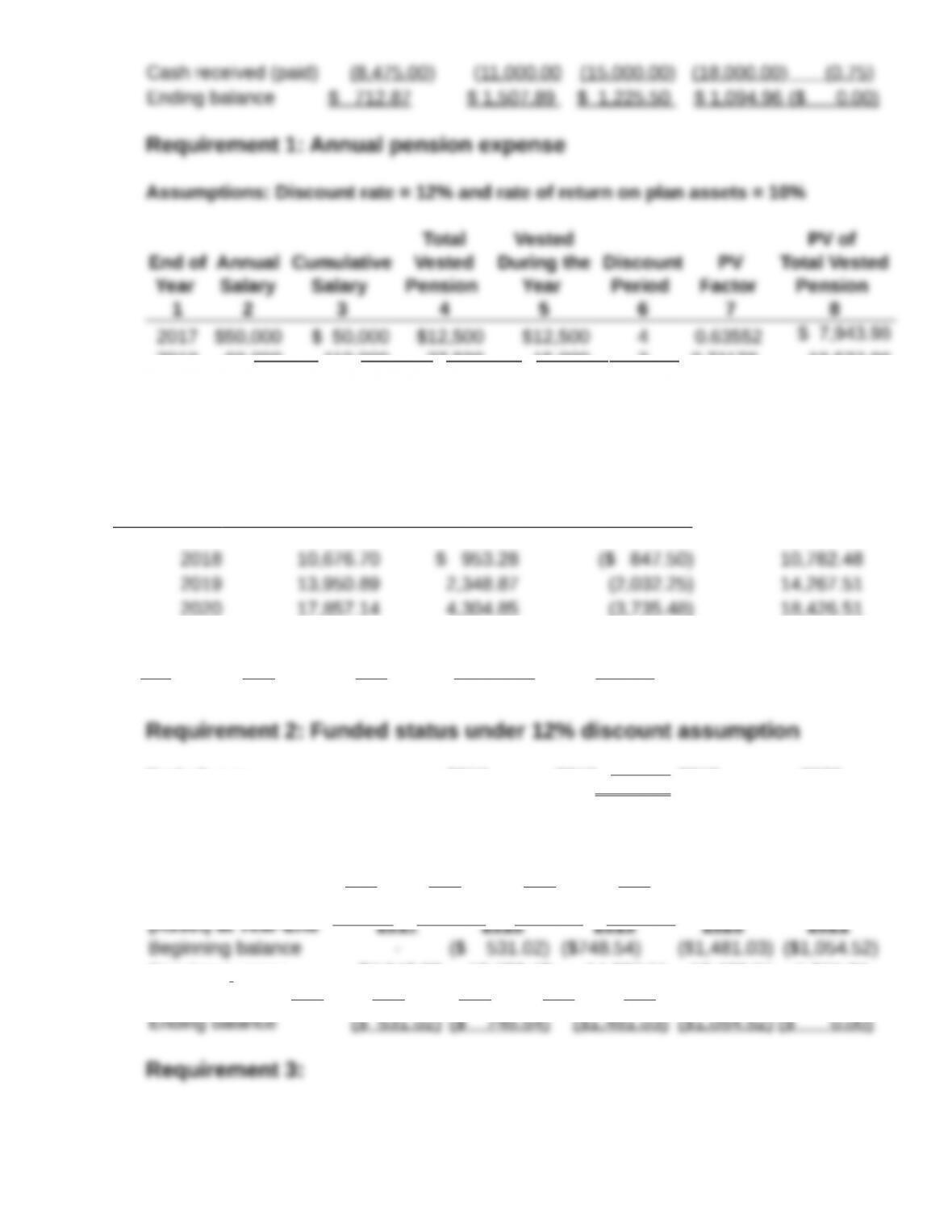

Requirement 1: Annual pension expense

Assumptions: Discount rate = 12% and rate of return on plan assets = 10%

End of

Year

1

Annual

Salary

2

Cumulative

Salary

3

Total

Vested

Pension

4

Vested

During the

Year

5

Discount

Period

6

PV

Factor

7

PV of

Total Vested

Pension

8

2017 $50,000 $ 50,000 $12,500 $12,500 4 0.63552 $ 7,943.98

2021 – 260,000 65,000 – 0 1.00000 65,000.00

Service Interest Return on Pension Pension

Year Cost Cost Plan Assets Expense

2017 $ 7,943.98 – – $ 7,943.98

2021 – 6,964.29 (5,909.02) __1,055.27

$52,475.75

Requirement 2: Funded status under 12% discount assumption

End of year 2017 2018 2019 2020

Projected benefit obligation $7,943.98 $19,573.96 $35,873.72 $58,035.71

– Fair value of plan assets (8 ,475.00) (20 ,322.50) (37,354.75) (59,090.23)

Pension Liability

(Asset) at Year-End 2017 2018 2019 2020 2021

Beginning balance – ($ 531.02) ($748.54) ($1,481.03) ($1,054.52)

Requirement 3:

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

14-2

The most (least) conservative approach for the purposes of income

determination is when the discount rate is less (more) than the rate of return

on the plan assets. Let us compare the pension under the three scenarios:

Pension Expense under Various

Discount Rate Assumptions

Year 8% 10% 12%

2017 $ 9,187.87 $ 8,537.67 $ 7,943.98

$52 ,475.74 $52 ,475.76 $52 ,475.75

In the first three years, the pension expense is the highest (lowest) when the

discount rate is 8% (12%). However, in the last two years, the situation

the pension fund are unaffected by the discount rate assumption used for

financial reporting purposes.) For instance, if the pension was completely

on pension plan assets are fixed in the problem, the choice of the discount

rate cannot affect the total pension expense. To see this, let us examine the

total contributions to the pension fund:

2017 2018 2019 2020 2021 Total

had been different, then the final shortfall would have been different, resulting

in a different total expense for pensions.

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

14-3

discount rates lead to more (less) conservative income figures.

P14-9. Interpreting OPEB disclosures and making journal entries (LO14-3,

LO14-6, LO14-7)

Requirement 1:

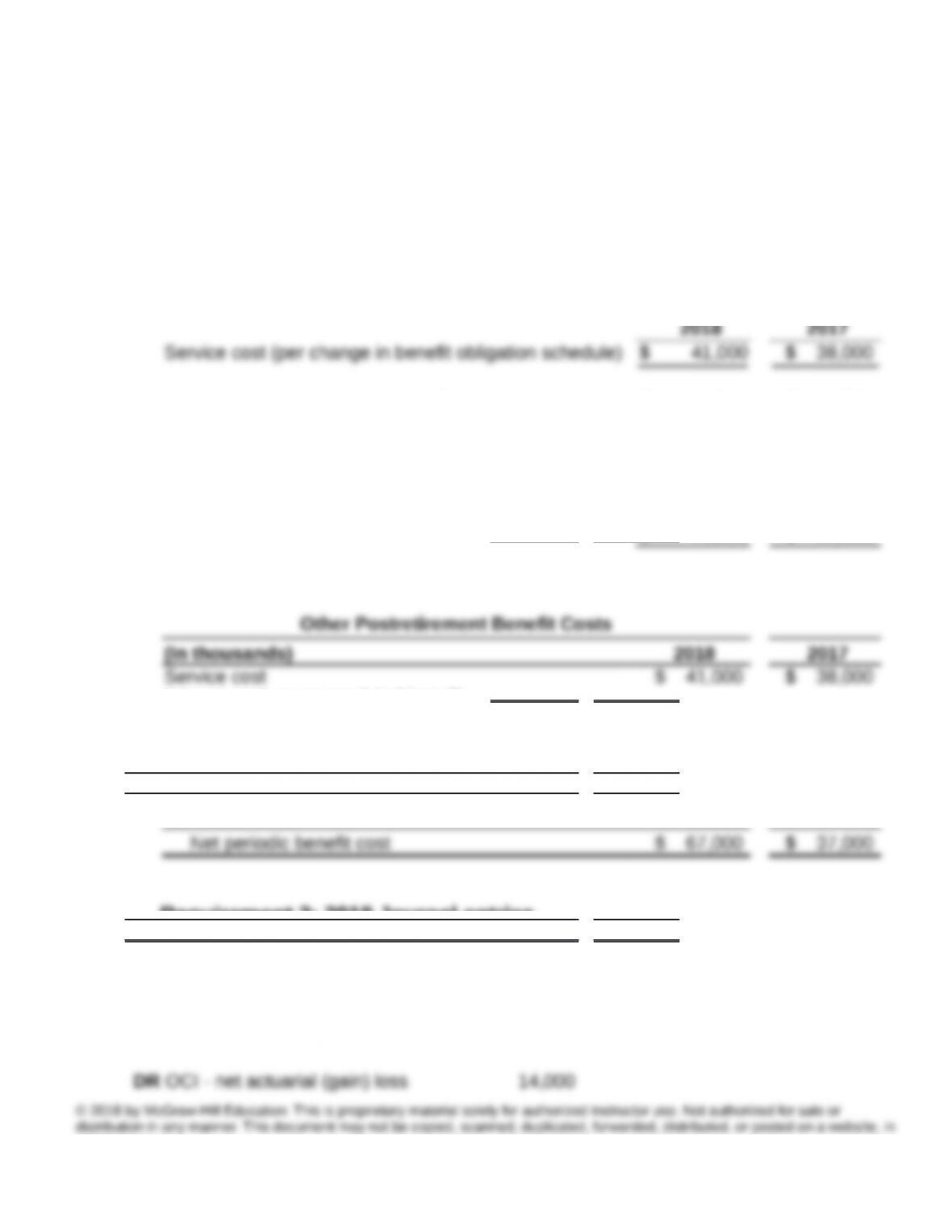

Determining missing costs and net periodic benefit cost:

2018 2017

Rounded to nearest million $ 76,000 $ 69,000

Other Postretirement Benefit Costs

(In thousands) 2018 2017

Service cost $ 41,000 $ 38,000

Interest cost on accumulated benefit

Curtailment loss 30,000 0

Net periodic benefit cost $ 67,000 $ 37,000

Requirement 2: 2018 Journal entries

DR Benefit expense $74,000

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

14-4

CR OCI – prior service costs

DR Retirement benefit asset (liability) $29,000

DR Retirement benefit asset (liability)

$188,00

0

Requirement 3: Balance sheet account

Beginning balance $(371,000)

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

14-5

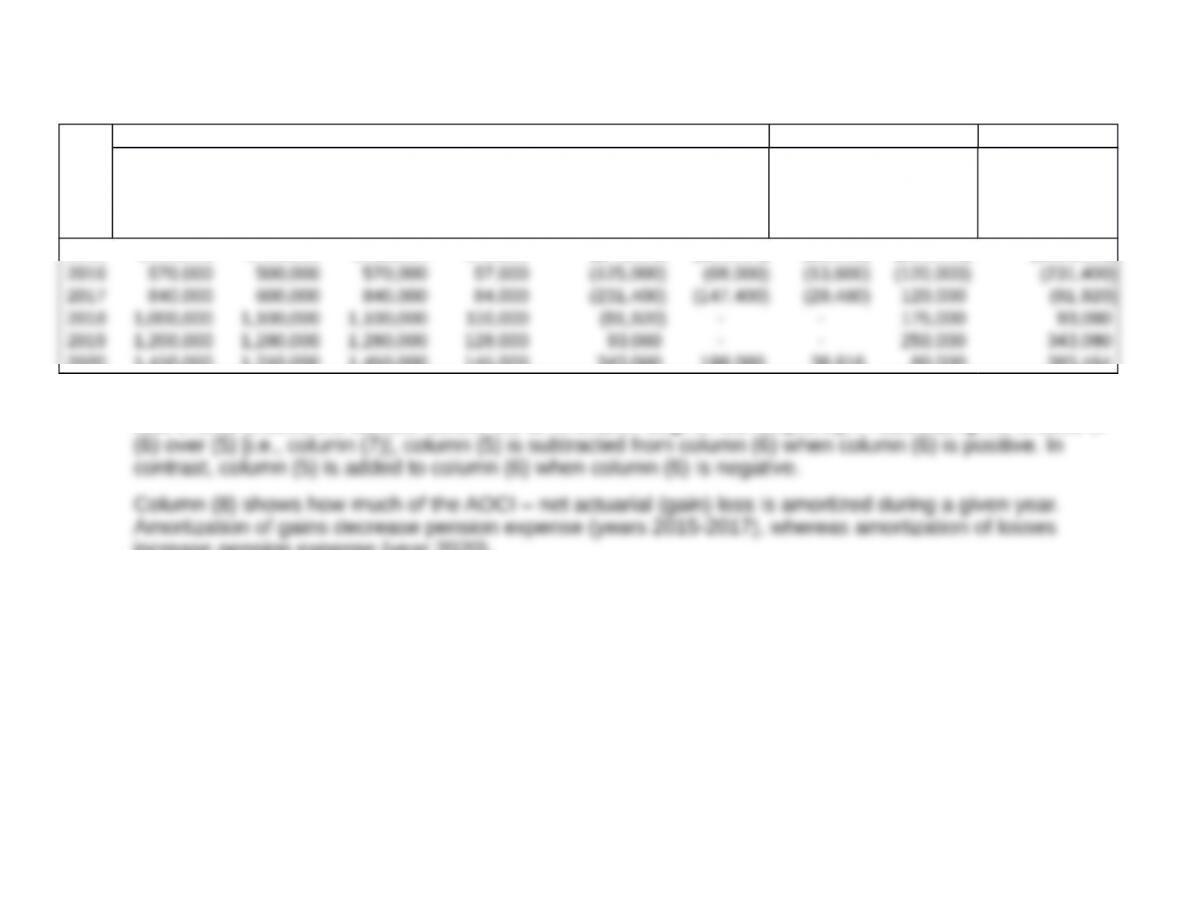

P14-10. Amortizating actuarial (gains) losses (LO14-3, LO14-4)

Beginning of the Year For the Year End of the Year

Projected Fair Value AOCI AOCI

Benefit of Pension Higher of Corridor Net Actuarial Excess of Amortized Excess Net Actuarial

Year Obligation Plan Assets (2) or (3) 10% of (4) (Gain) Loss (6) over (5) (Gain)loss (Gain)loss (Gain) Loss

(1) (2) (3) (4) (5) (6) (7) (8) (9) (6) – (8) + (9)

2015 $450,000 $410,000 $450,000 $45,000 ($70,000) ($25,000) ($5,000) ($60,000) ($125,000)

2020 1,450,000 1,310,000 1,450,000 145,000 343,080 198,080 39,616 80,000 383,464

Note that column (5) is unsigned in the sense that the magnitude of the cumulative unrecognized gain or

loss should exceed the corridor before the amortization begins. Consequently, in calculating the excess of

increase pension expense (year 2020).

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be

copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

14-6

P14-11. Interpreting pension disclosures (LO14-2, LO14-3, LO14-4,

LO14-6)

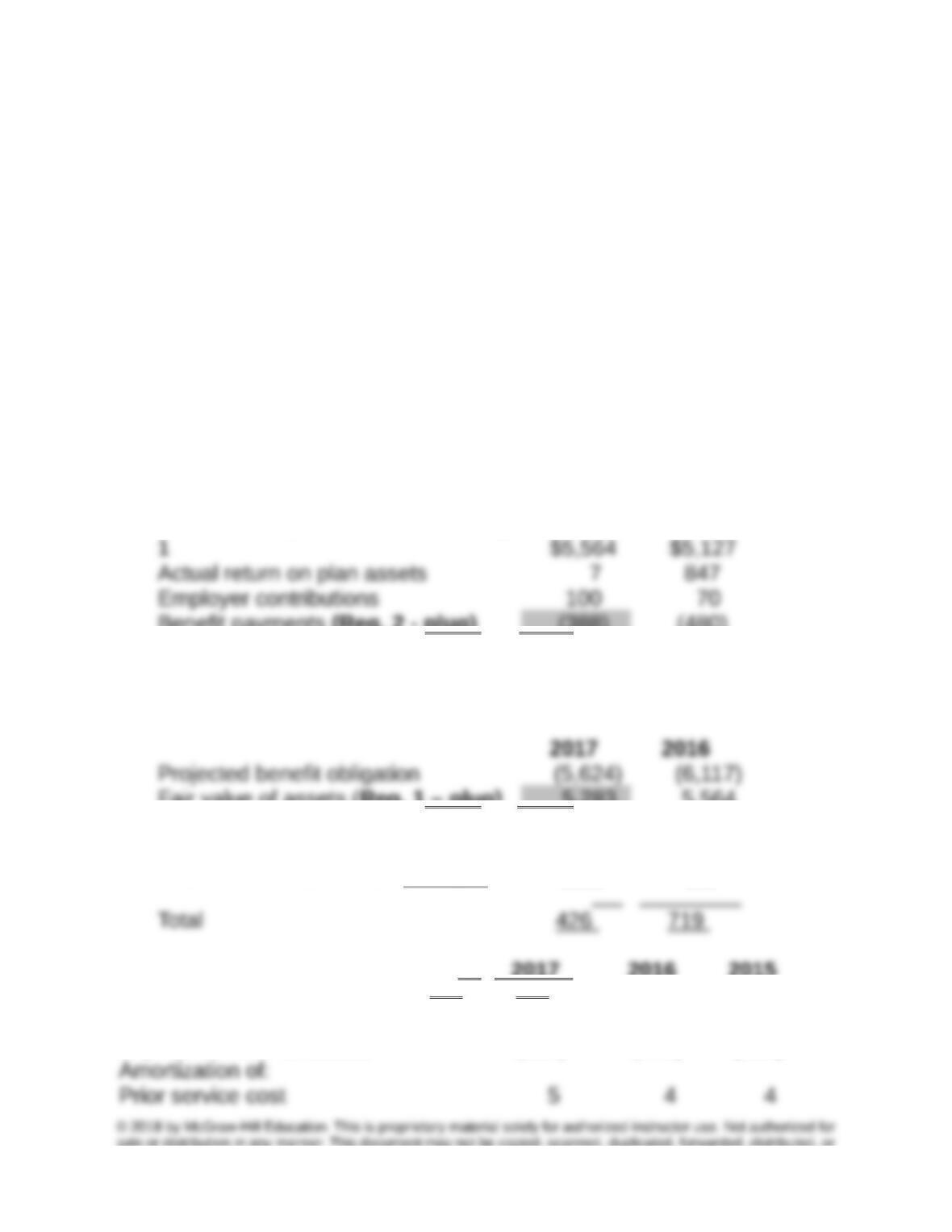

Requirements 1 and 2 – Fair value of assets and benefit

payments

($ in millions) 2017 2016

Obligation at January 1 $6,117 $5,666

Service cost 236 213

Obligation at December 31 $5 ,624 $6 ,117

Fair value of plan assets at January

1 $5,564 $5,127

Actual return on plan assets 7 847

December 31 $5 ,283 $5 ,564

2017 2016

Projected benefit obligation (5,624) (6,117)

Total

426

719

2017 2016 2015

Service cost 236 213 179

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 14-7

Unrecognized loss 21 22 26

Net periodic benefit cost 181 185 181

Requirement 3 – Plan amendments

AOCI – Prior Service Cost

Beginning 68

Ending 138

Requirement 4 – Actuarial (gain) loss on PBO

AOCI – Actuarial (gain)

loss

Beginning 651

Ending

288

Requirement 5 – Effect of increasing the discount rate

The increase in discount rate decreased PBO. This increase was probably

Requirement 6 – Journal Entries

Pension expense 155

Pension expense 26

expense

Pension asset (liability) 100

To record plan amendment

AOCI – actuarial (gain) loss 507

To record deferred gain on PBO

Requirement 7 – Verification of balance sheet account

Pension

Asset (liability)

Balance, 1/1/2017 553

PBO actuarial gain 849

Balance, 12/31/2017 341

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 14-9