E9-17. Computing dollar-value LIFO (LO 13)

(AICPA adapted)

To compute ending inventory at base year prices, we need to divide

the year-end prices of each year by the respective price index, then

separate the layers to compute ending inventory at LIFO Cost. Here

are the computations:

Year Ended

December 31,

Inventory at

Respective

Year-End Prices

External

Price Index

(Base Year 2014)

Inventory at

Base Year

(2014) Price

December 31, 2015

33,000

$333 ,000

December 31, 2016

24,000

Notice that the 2016 layer was partially depleted in 2017.

E9-18. Computing dollar-value LIFO (LO 13)

(AICPA adapted)

The computation of dollar value LIFO can be seen below. The first

step is to find the base-year price of ending inventory. We can do

and use the price indices to find ending inventory at LIFO Cost as

is done below.

Ending inventory

Price

Index Base-Year Price

$780,000 1.2 $650,000

Layers at Base-Year Price

Price

Index

Ending Inventory

at LIFO Cost

E9-19. Evaluating inventory costing concepts (LO 4, 9, 10)

(AICPA adapted)

Requirement 1:

Description of fundamental cost flow assumption:

a) It is difficult, if not impossible, to measure the physical flow of

goods and, therefore, to cost items on an average price basis

b) The first-in-first-out (FIFO) method assumes that goods are used

or sold in the order they were purchased, and, therefore, the

c) Last-in-first-out (LIFO) matches the cost of the most recent

Requirement 2:

Reasons for using LIFO in an inflationary environment:

In an inflationary economy, LIFO is a useful tool. When using LIFO,

as prices rise, the company’s cost of goods sold expense also rises

because it is assumed the sale is always the most recent inventory

Requirement 3:

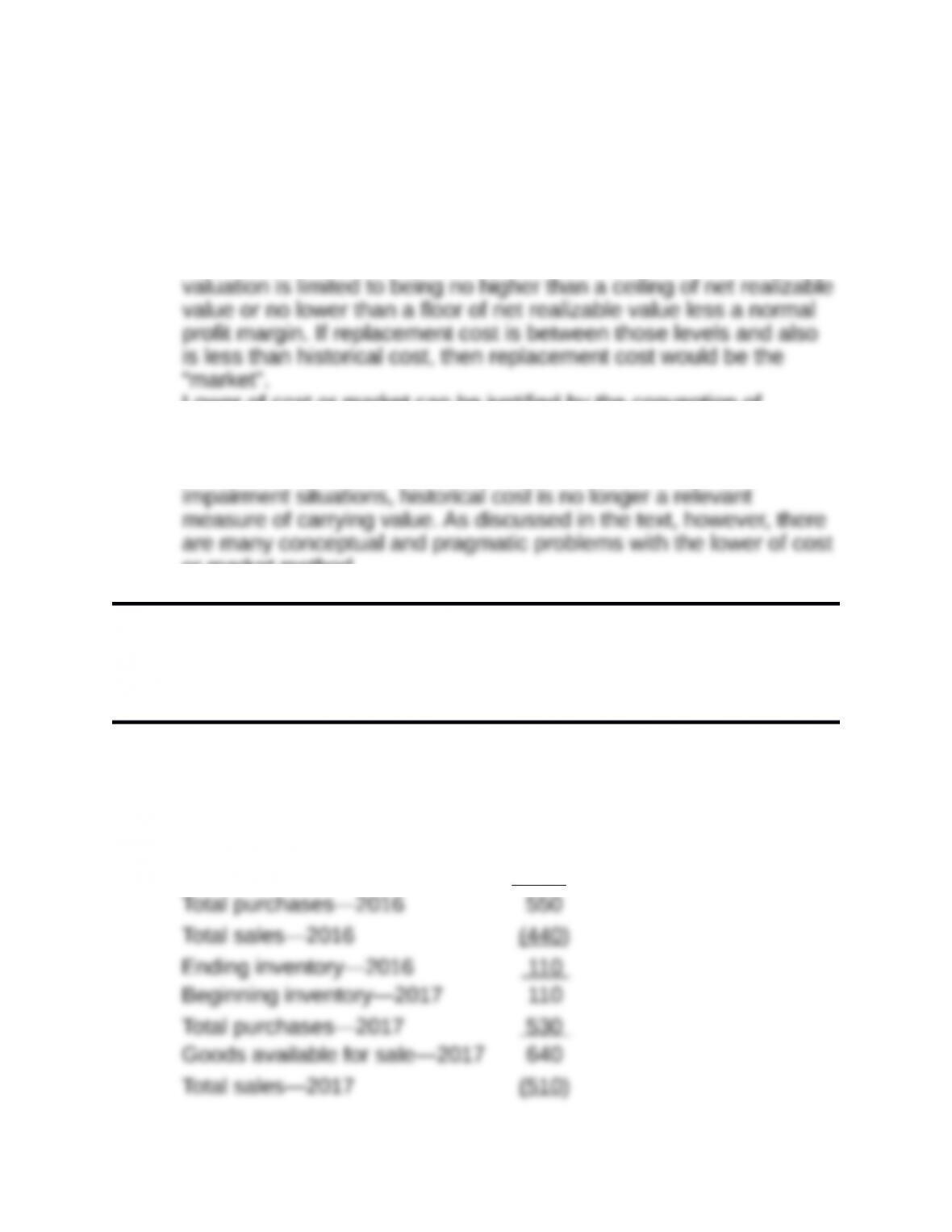

Proper accounting treatment when utility of goods is below cost:

The prevailing accounting treatment in this case is to value the

inventory at the lower of cost or market. For the average cost and

FIFO methods, “market” is defined as net realizable value. For

LIFO, the accounting treatment is “market” where the inventory

Lower of cost or market can be justified by the convention of

conservatism. Accountants tend to prefer conservative asset

measures. Relevance can also be used to defend the lower of cost

or market convention. Accountants generally believe that, in asset

or market method.

Financial Reporting and Analysis (7th Ed.)

Chapter 9 Solutions

Inventories

Problems/Discussion Questions

Problems

P9-1. Calculating amounts and ratios under FIFO and LIFO (LO 2, 4)

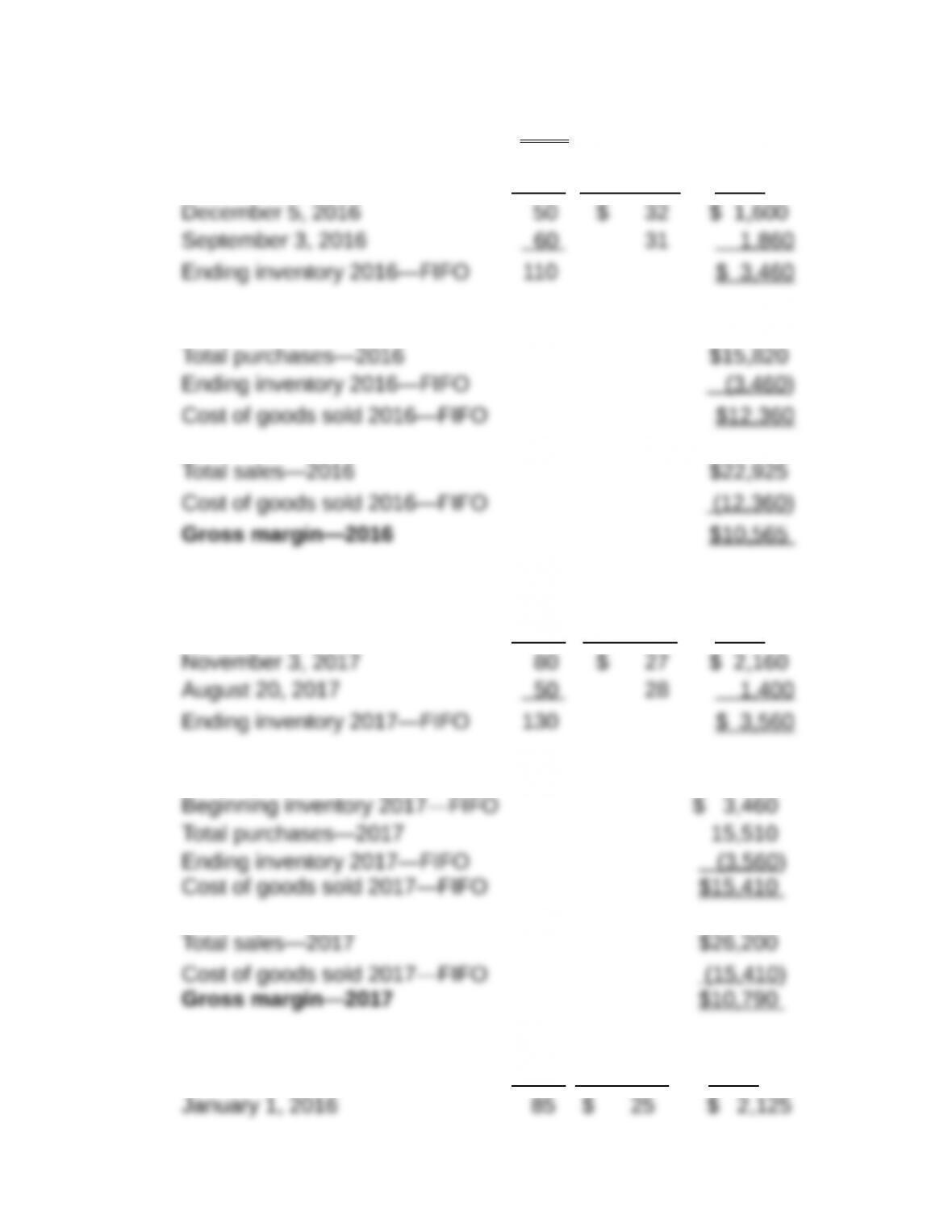

Requirement 1:

Units

Ending inventory—2017 130

Ending inventory 2016—FIFO: Units Cost/unit Total

Cost of goods sold 2016—FIFO:

Ending inventory 2017—FIFO: Units Cost/unit Total

Cost of goods sold 2017—FIFO:

Requirement 2:

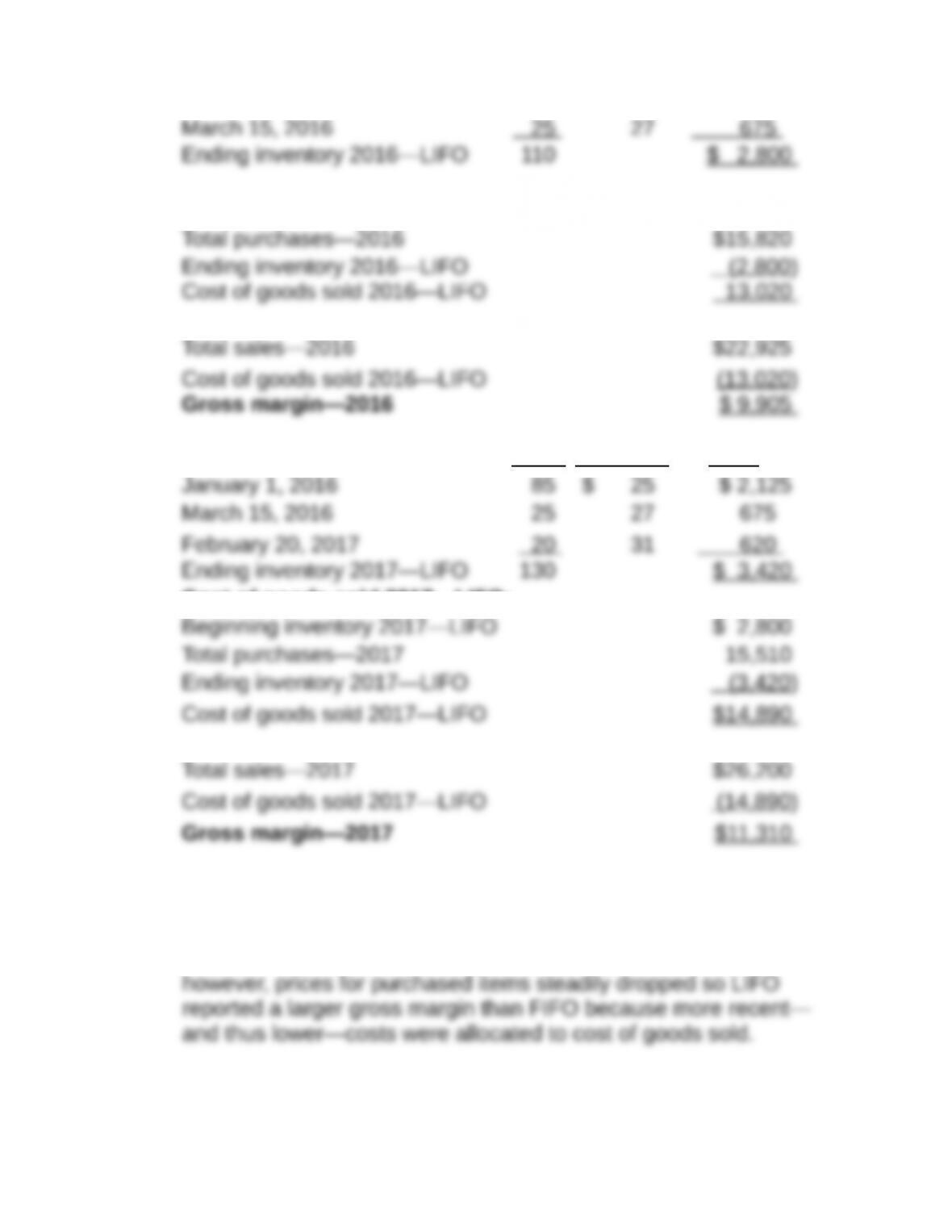

Ending inventory 2016—LIFO: Units Cost/unit Total

Cost of goods sold 2016—LIFO:

Ending inventory 2017—LIFO: Units Cost/unit Total

Cost of goods sold 2017—LIFO:

Requirement 3:

In 2016, when prices paid for purchased goods were rising, FIFO

produced a higher gross margin than LIFO because it allocated the

older, lower cost purchases to cost of goods sold. During 2017,

P9-2. Determining income statement amounts for a manufacturer (LO

1,3, 12)

Requirement 1:

Computation of cost of raw materials used:

Requirement 2:

Computation of cost of goods manufactured/completed:

Cost of goods manufactured = Beginning balance in work in

process inventory + Raw materials used + Wages to factory

Requirement 3:

Computation of cost of goods sold:

Cost of goods sold = Beginning balance in finished goods

Requirement 4:

Computation of gross margin:

Requirement 5:

Computation of net income:

Net income = Gross margin – Salary to selling and administration

P9-3. Determining cost of sales under different flow assumptions —

comprehensive (LO 2, 4, 5)

Requirement 1:

The ending inventory is computed based on the cost flow

assumption, which is then subtracted from goods available for sale

Cost of Ending Inventory Cost of Goods Sold

Weighted

Unit cost:

Requirement 2:

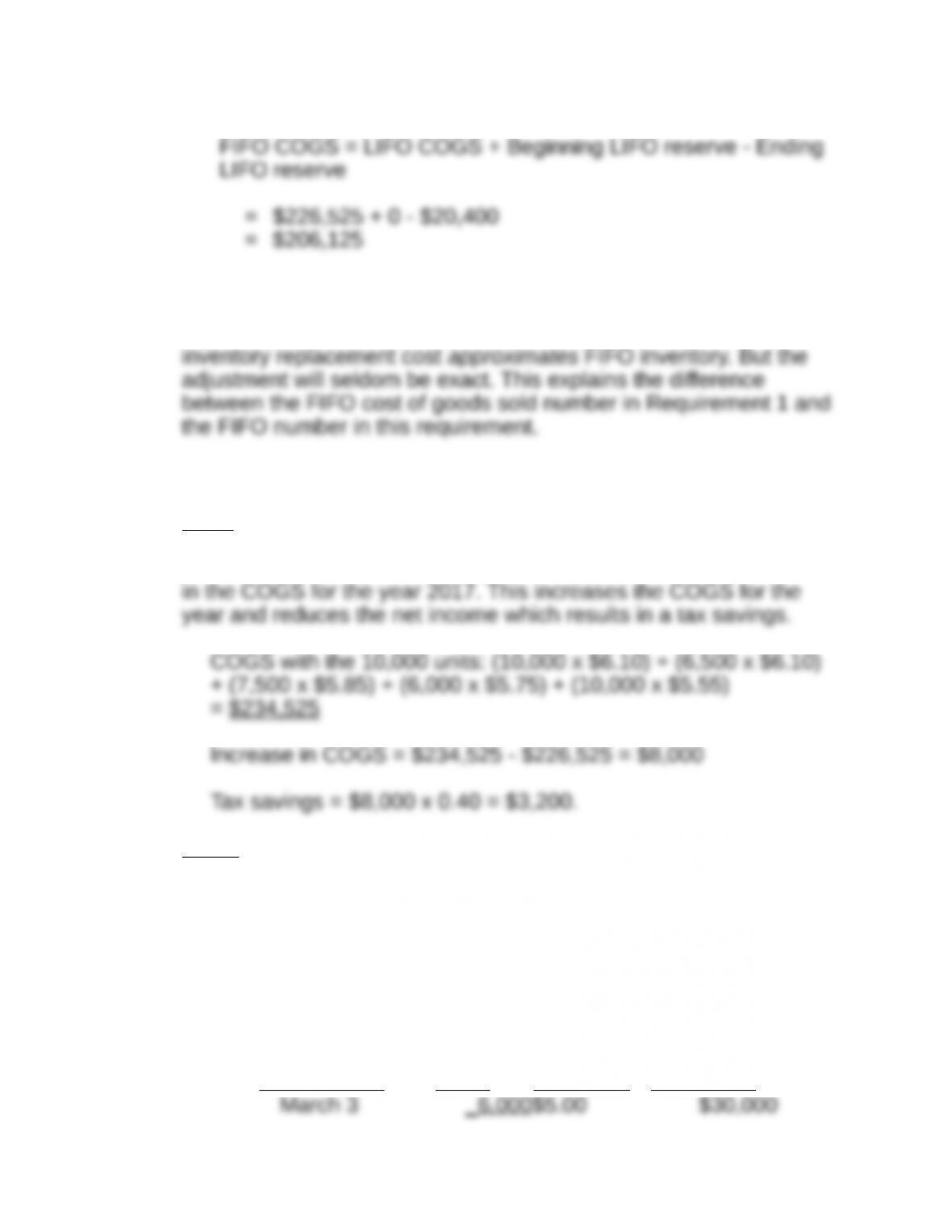

Replacement cost of ending inventory and LIFO reserve.

a) Replacement cost of the ending inventory = 20,000 x $6.10

$122,000

b) Cost of goods sold under FIFO (periodic).

As discussed in the text, the reconciliation procedure is an

approximation. Adding the LIFO reserve to the LIFO inventory

equals replacement cost. If the inventory turns quickly, then

c) Pros and cons of the accountant’s suggestions.

Pros:

Under periodic LIFO, COGS is computed at 12/31/17, i.e., year-end.

Therefore, the 10,000 units acquired on 12/31/17 would be included

Cons:

Inventory carrying cost is higher, and the company is exposed to the

risk of an unexpected fall in demand.

Requirement 3 a:

This will be the same as the periodic FIFO method.

Proof:

Cost of Goods Sold under Perpetual FIFO

Date of Sale Units Cost/Unit Total Cost

Regardless of whether periodic or perpetual inventory procedure is

used, the cost of goods sold and ending inventory values will be the

same under FIFO cost flow assumption. However, the answers will

typically be different under LIFO. Under FIFO, the units purchased

on January 1 will be assigned to cost of goods sold first, irrespective

of when cost of goods sold is calculated. On the other hand,

identifying the most recent units purchased depends on when the

calculations are performed. For instance, if LIFO cost of goods sold

Requirement 3 b:

Quantity Unit cost

0 0

Cost of goods sold under perpetual weighted average = $30,000 +