C11-2 Tuesday Morning Corporation: Interpreting long-term debt

disclosures

Requirement 1:

Requirement 2:

Requirement 3:

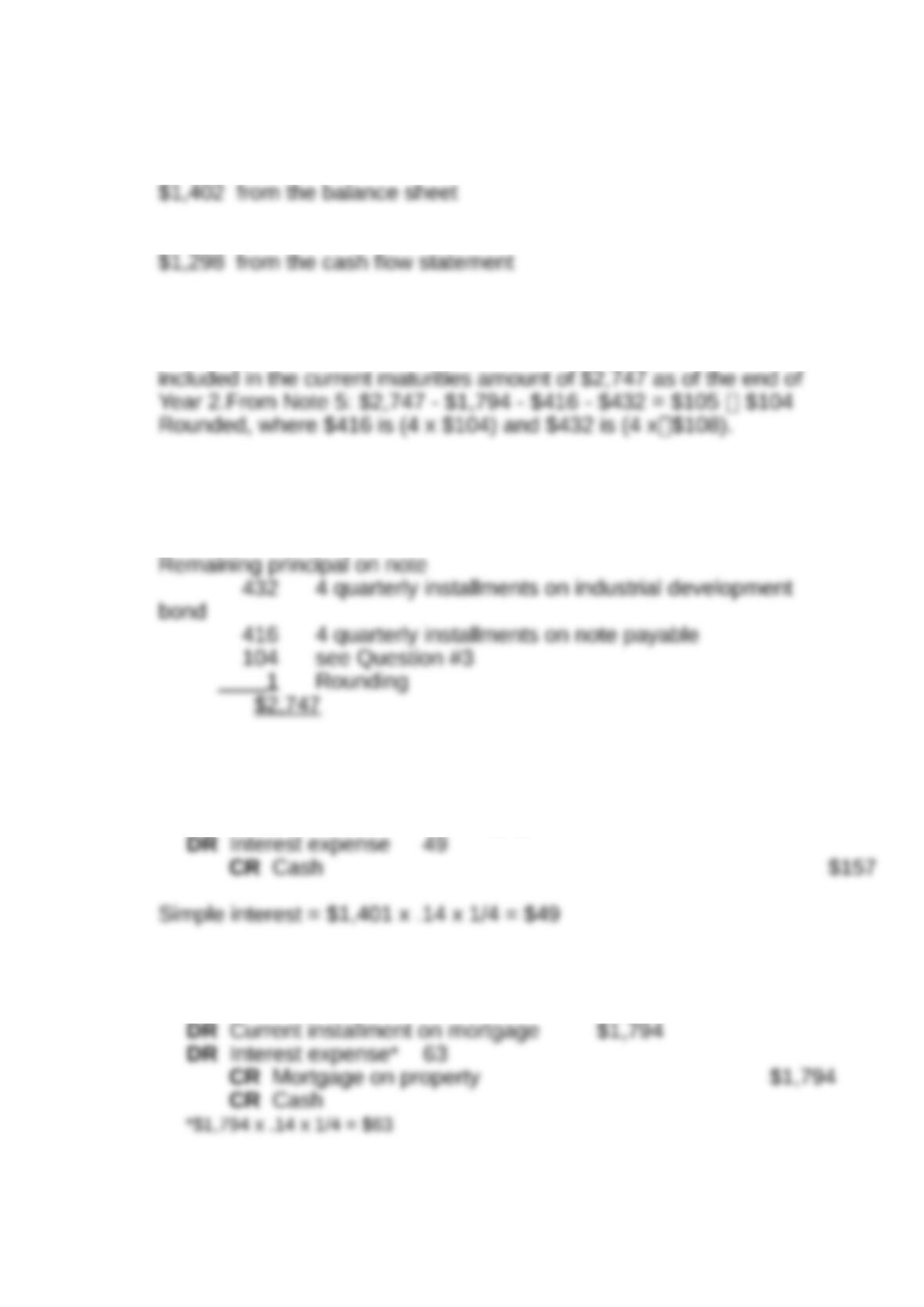

The difference is $104. This appears to suggest that payment on the

note payable in Note 5 was not made during Year 2, but that it is

Requirement 4:

Current portion is $2,747

$1,794

Requirement 5:

Journal entry for March 31:

DR Current installment on mortgage $108

Requirement 6:

Journal entry for April 30:

11-1

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

Requirement 7:

C11-3 Dentsply International: Analyzing long-term debt disclosures (LO

11-1, LO 11-2)

Requirement 1: Change in amount and composition of debt

The debt amount declined slightly from 2011 to 2012. Individual

amount changes appear to have occurred because of premium or

Requirement 2: Difference between fair value and book value

At December 31, 2012, the fair value of debt of $1,515.2 million

Requirement 3: Weighted-average interest rate

The weighted-average rate of interest on Dentsply’s long-term debt

is 3.01%. To arrive at this figure, multiply the principal balance of

There are two features of this calculation to notice. First, the

weighted-average interest rate is not simply the average of the

interest rates reported in the financial statement note. Each reported

interest rate is weighted by the dollar amount of debt to which it is

11-2

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

Requirement 4: Interest expense for 2013

Forecasted interest expense for 2013 is $44.296 million. This

Requirement 5: Cash payout on debt

The company is obligated to make 2013 cash payments on debt in

the amount of $295.174 million. This figure is the sum the schedule

Requirement 6: Dentsply’s ability to meet its debt obligations

The note indicates that Dentsply should be able to meet its debt

obligations. The fair value of its debt exceeds the debt book value

Compare this analysis to the one connected with the Chesapeake

Energy Corporation information in Exhibit 11.10. Chesapeake’s debt

C11-4. Groupe Casino: Determining whether it is debt or equity (LO

11-10)

Requirement 1:

International Accounting Standards (IAS) No. 32 states that “[t]he

issuer of a financial instrument shall classify the instrument, or its

component parts, on initial recognition as a financial liability, a

financial asset or an equity instrument in accordance with the

A financial liability is any liability that is: (a) a contractual obligation to deliver

cash or another financial asset to another entity, or a contractual obligation to

11-3

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

exchange financial assets or financial liabilities with another entity under

conditions that are potentially unfavourable to the entity; or (b) a contract that will

or may be settled in the entity’s own equity instruments and is a non-derivative for

An equity instrument is any contract that evidences a residual interest in the

Requirement 2:

Equity treatment seems appropriate in this case. The notes have no

maturity date and the lender cannot force redemption. Moreover,

interest payments can be suspended at any time. Thus Casino does

Requirement 3:

The following entries would be made on the books of Groupe Casino:

To record the issuance of the notes on January 1, 20X5 (in millions of

euros)

To record the interest payment on December 31, 20X5 (in millions of

euros)

The notes themselves would be shown in the equity section of

11-4

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

Requirement 4:

Why would an investor pay a premium (i.e., more than the principal)

for notes where interest payments can be suspended at any time, the

principal is never repaid, and there is no equity conversion privilege?

The notes seem to be characterized by consider cash flow risk to the

C11-5. Kellogg Company’s Organic Corn Hedge (LO 11-7, LO 11-8)

Requirement 1:

Notice that the non-organic corn futures contracts are exactly

“matched” in bushel amount and delivery month to the company’s

anticipated purchases of organic corn. This sort of matching would

Requirement 2:

The eligible market risk being hedged is an overall change in cash

flow arising from the risk of changes in organic corn commodity price

between now and the dates of future planned purchases or organic

corn. Hedge accounting can be used in this situation because:

Requirement 3:

The following entries would be made on March 31, 2015 and April 30th.

11-5

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

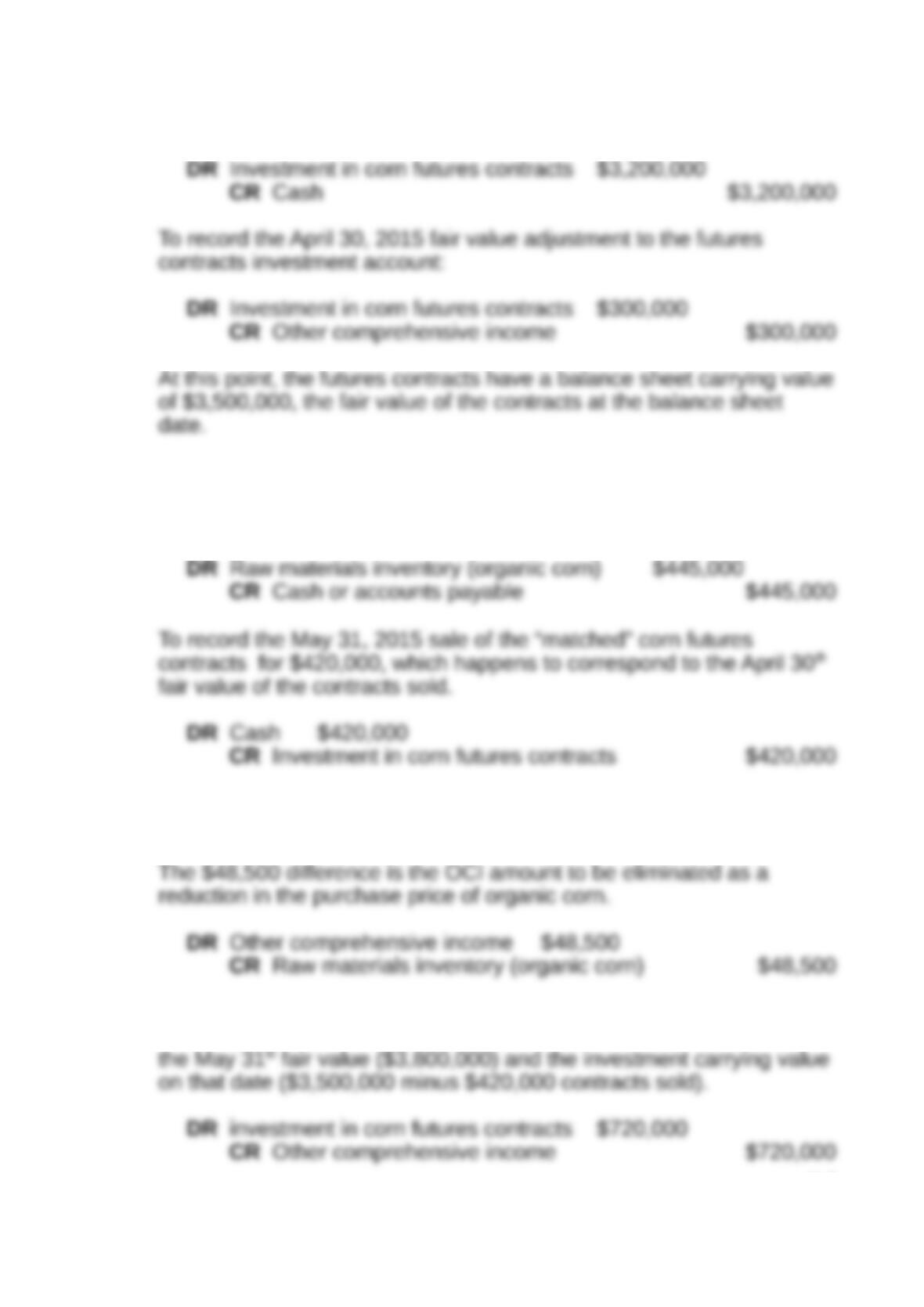

To record the March 31, 2015 purchase of “matched” corn futures

contracts:

Requirement 4:

To record the May 31, 2015 purchase and delivery of organic corn for

use in the production of cereal:

To eliminated the balance in Other comprehensive income that

pertains to the corn futures contracts sold. These contracts were

purchase for $371,500 and had a fair value of $420,000 when sold.

To record the May 31st fair value adjustments to the remaining corn

futures contracts. The adjustment amount is the difference between

11-6

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

Requirement 5:

Corn prices rose substantially during the period from March 31st to

May 31st, as evidenced by the increase in corn futures contracts fair

value. The dollar amount of the price increase is captured by the

cumulative balance of Other comprehensive income ($971,500 =

Requirement 6:

If corn prices had moved in the opposite direction and fallen in value

over this time period, the corn futures contracts themselves would

have lost value. Kellogg would have been able to buy organic corn on

Kellogg benefits from the futures contracts hedge if corn prices rise

because the higher price paid to buy organic corn will be partially

offset by the increased value of the corn futures contracts. Kellogg

C11-5. Southwest Airlines: Interpreting cash flow hedge (LO

11-7, LO 11-8)

All amounts are in millions.

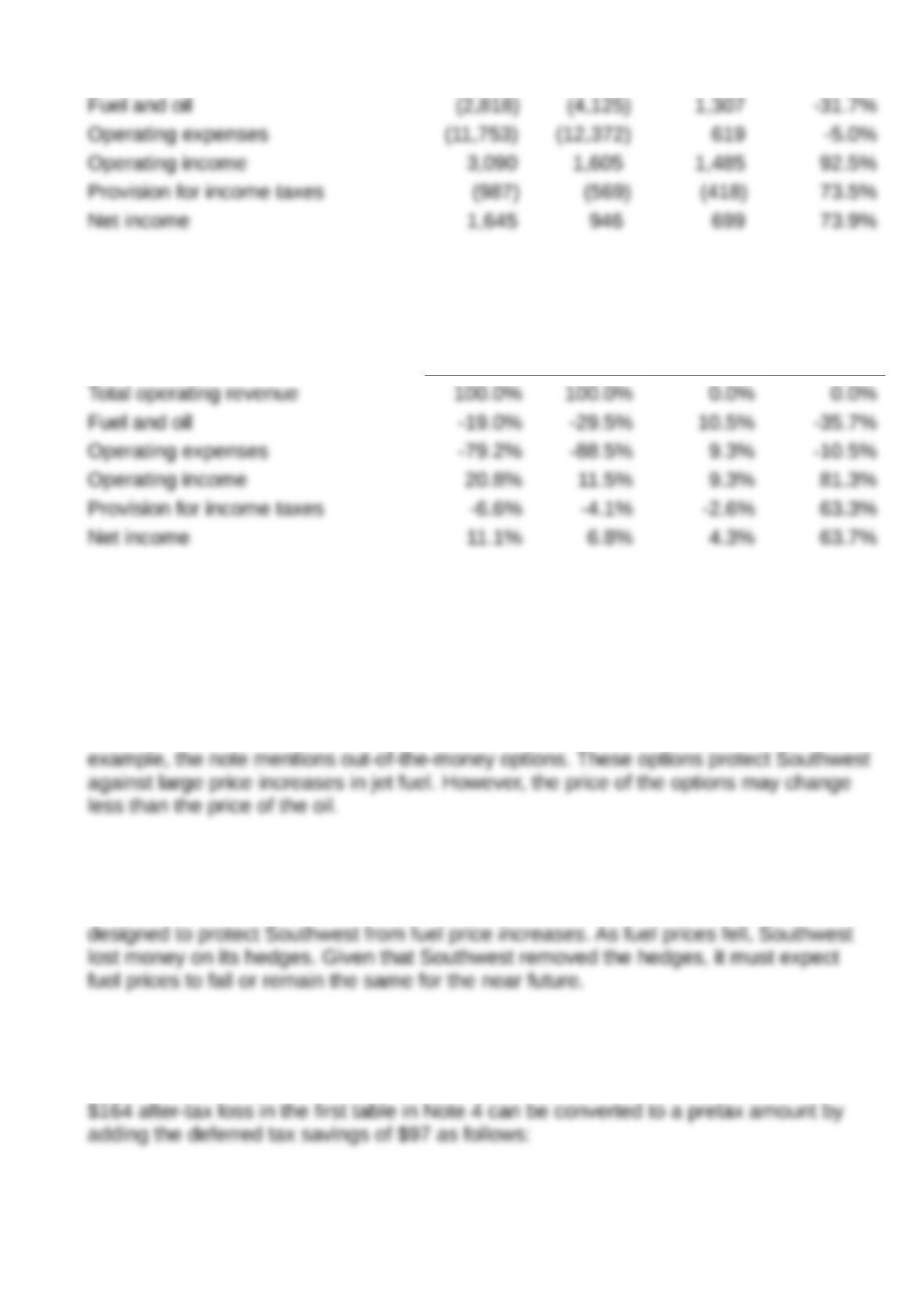

Requirement 1 – Reason for increase in 2015 net income

Selected income statement items

a b a – b (a – b) / b

2015 2014

Change

from 2014

% change

from 2014

11-7

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

Common size (amounts as a percent of total revenue)

a b a – b (a – b) / b

2015 2014

Change

from 2014

% change

from 2014

Both the raw analysis and the common size analysis indicate that lower fuel and oil

expense was the main reason for the higher net income.

Requirement 2 – Economic hedge versus accounting hedge

Under U.S. GAAP, price changes in the hedge must be highly correlated with the

hedged item. The economic hedges may not meet the threshold of high correlation. For

Requirement 3 – Reason for eliminating hedges

Note 3 indicates that Southwest experienced losses on its derivatives, which were

Requirement 4 – Losses in OCI

No. This is the net after-tax new losses and losses recycled to operating income. The

11-8

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

Unrealized loss on fuel derivatives (164)

Deferred taxes (97)

(261)

The $525 represents the actual amount of new pretax losses occurring in 2015. Note

Requirement 5 – Fuel and oil expense without hedging

The third table of Note 4 shows that $264 in pretax losses were transferred to Fuel

and oil expense. If not for hedging, the Fuel and oil expense would have been $264

lower. It is important to note that losses and gains on cash flow hedges affect the item

Requirement 6 – Timing of derivative payments

Note 5 shows that Accrued liabilities (a current liability) includes $541 for Derivative

contracts, which indicates that $541 will be paid within the next 12 months. Southwest

also has Derivative contracts of $265 in Other noncurrent liabilities that will be paid

11-9

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.