Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Financial Reporting and Analysis (6th Ed.)

Chapter 10 Solutions

Long-Lived Assets and Depreciation

Problems

Problems

P10-1. Computing depreciation expense – SL, DDB, SYD, and UP (LO

10-7)

(AICPA adapted)

The table below shows the amount of depreciation expense in 2017

under each method. Computations are shown below the schedule.

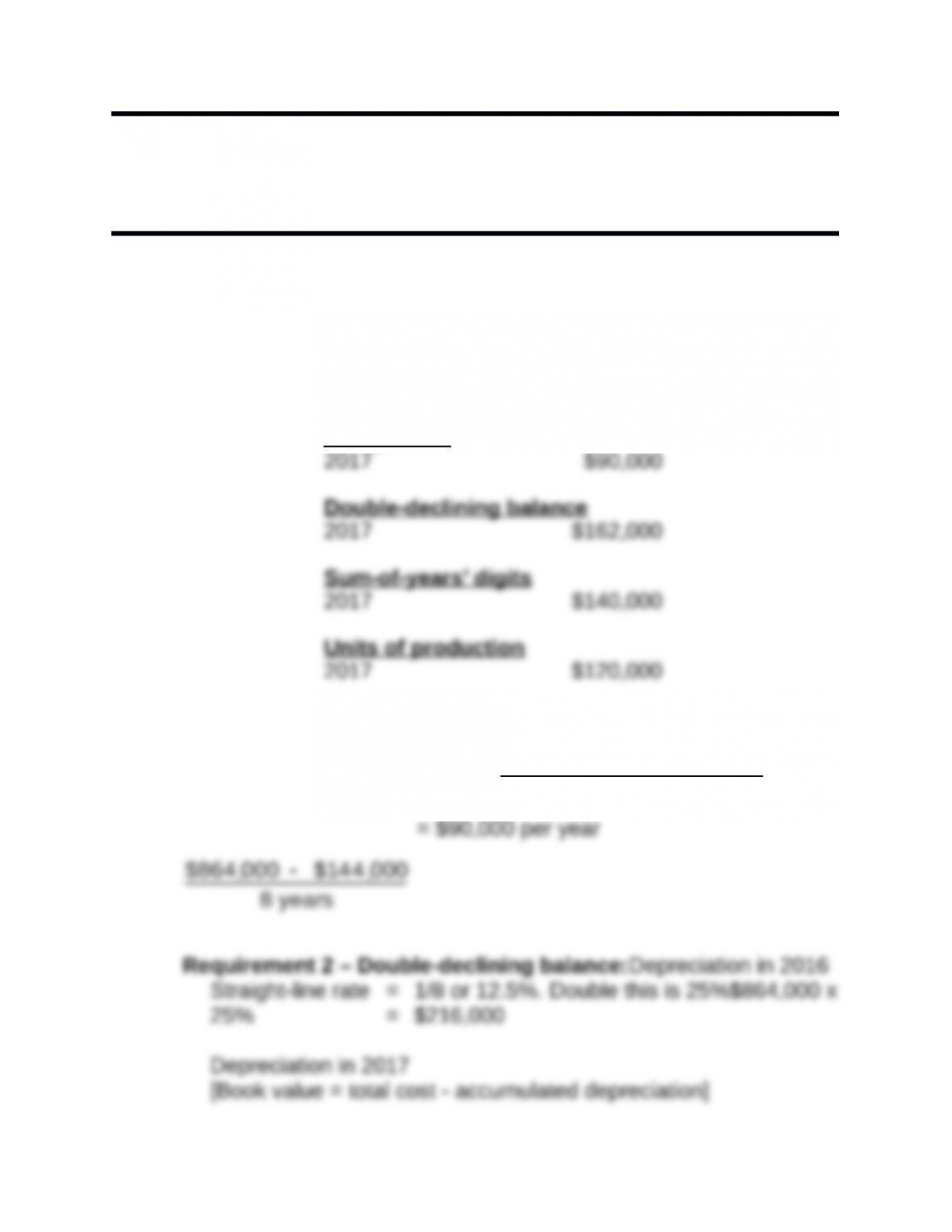

Straight-line

Requirement 1 – Straight-line:

Total cost Salvage value

Estimated useful life

=

Depreciation in 2017

[Book value = total cost - accumulated depreciation]

Requirement 3 – Sum-of-years’ digits: Depreciation in 2016

Requirement 4 – Units of production:

Depreciation = depreciation cost per unit x number of units

P10-2. Recording lump-sum purchases (LO 10-2)

Requirement 1:

Cost of land and building:

Land:

FMV of land/FMV of land and building

$6,300,000/$17,500,000 = 36%

Requirement 2:

Depreciation is not recorded on land. Thus, the higher the amount

P10-3. Determining asset cost when purchased with a note (LO 10-2)

At a discount rate of 10%, the present value of the note is:

Since this is more than the cash price of $250,000, Cayman should

pay cash.

At a discount rate of 13%, the present value of the note is:

In this case, since the present value of the note is less than the

cash price of $250,000, Cayman should issue the note to the seller

rather than paying cash.

P10-4. Allocating acquisition costs among asset accounts and

interest capitalization (LO 10-2)

Relative assessed values of the land and building at the time of

purchase:

Initial allocation of cost:

Allocation of subsequent costs:

Land:

Warehouse:

Department store:

Land improvements:

The $725,000 would be recorded in the land improvements account

rather than the land account because the parking lot, lighting,

P10-5. Exchanging assets (LO 10-9)

Requirement 1:

Hoyle’s entry to record the exchange:

Requirement 2:

Patterson’s entry to record the exchange:

P10-6. Capitalizing or expensing various costs (LO 10-2)

Requirement 1:

1) Since the new engines increase the future service potential of

2) Since there is no increase in useful life, future service potential,

or efficiency, the amount should be charged to expense in the

3) Since the repairs are routine (i.e., recurring), the amount should

4) The noise abatement equipment is mandated and is, thus, an

5) Since the new systems increase the future service potential of

6) Again, some might argue that this is another gray area. Since the

objective of the expenditure is to increase business, it might warrant

7) Since the overhauls increase the efficiency of the engines, the

Requirement 2:

Perhaps the easiest way for a firm like Fly-by-Night to use some of

the above expenditures to manage earnings upward is to capitalize

a portion of those that might otherwise be treated as expenses of

the period. Other ways Fly-by-Night could manage earnings is to

P10-7. Determining asset impairment (LO 10-5)

Requirement 1:

Book value:

Requirement 2:

Yes, the asset is impaired.

Impairment loss to be reported in the income statement:

Requirement 3:

The balance sheet amount at the end of year 4 is $9,500,000, the

P10-8. Determining asset impairment (LO 10-5)

Requirement 1:

Assets should be tested for impairment whenever events or

circumstances indicate that the asset’s carrying value might be

impaired. In this case, due to the economic downturn and concerns

Requirement 2:

depreciation

The equipment is impaired since its undiscounted net future cash

flow is below its carrying value.

An asset’s impairment is measured by reference to its fair value.

Requirement 3:

Requirement 4:

The company might revise the asset’s estimated useful life or its

Requirement 5:

Under U.S. GAAP, impairment losses cannot be reversed.

P10-9. Determining asset impairment under IFRS (LO 10-5, LO 10-10)

Requirement 2:

The following impairment test indicates that Yachting in Paradise’s

yacht is impaired:

Book value:

IFRS dictates than an asset should not be carried at more than

its recoverable value, defined as the higher of an asset’s fair

value less costs to sell and its value in use. The latter is defined

The yacht is impaired since its recoverable value is below its

carrying value.

An asset’s impairment is measured by reference to its recoverable

value (see requirement 2).

Requirement 3:

Requirement 4:

Under IFRS, if the estimates used to determine an asset’s

recoverable value have changed, a previously recognized

impairment loss shall be reversed, but the reversal shall not yield a

Requirement 5:

See the answer in requirement 4, noting that the carrying value in

early 2019 after reversing any impairment loss cannot exceed $8.6

million).

P10-10. Accounting for computer software costs (LO 10-4)

Requirement 1:

Until the technological feasibility of the product is proven, all costs

are expensed as R&D. After technological feasibility is proven, the

costs are supposed to be capitalized up to the point the product is

Requirement 2:

This amount cannot be determined from the information given.

While we can determine the costs incurred after technological

feasibility has been shown (see Requirement 3), we cannot know

how much IBM expended up to the point that technological

feasibility was reached on the various projects.

Requirement 3:

Requirement 4:

X = $3,058, where X is the gross amount of software-related costs

that were written off in Year 2. (The offsetting DR was to

accumulated amortization.) So:

Y = $3,541, where Y is the credit to accumulated amortization. The

Requirement 5:

Total capitalized software at the end of Year 2/software

amortization for Year 2:

Requirement 6:

Earnings can be managed by judicious selection of the point in

time when technological feasibility has been reached. For

example, a firm that wants to

boost income in a given year would declare that technological