P11-6. Call options as investments (LO 11-7)

Required entries for 1 through 3:

July 1, 2017:

July 31, 2017:

August 31, 2017:

The unrealized holding gains and losses flow directly to income

each month.

Requirement 4:

The option contracts are “underwater” on July 31, meaning that the

$40 exercise price is above the $38 market price for Selmer stock.

That’s what has happened by August 31. Now the options are “in

Requirement 5:

If Getz exercises the stock options on September 15, he will turn in

September 15, 2017:

Requirement 6:

If the option contracts were allowed to expire on September 15

(presumably because the market price of Selmer stock was below

$40), the entry is:

P11-7. Fair value option and retiring debt early (LO 11-2, LO 11-4, LO

11-5)

Requirement 1: Bond price at issuance

Because the coupon rate and the market rate are the same, the

Market value – tables

Paymen

$3,000,000 = $75,000,000 x 8% ÷ 2.

Requirement 2: Journal entries during 2017

January 1, 2017

To record bond issuance

June 30, 2017

To record interest expense

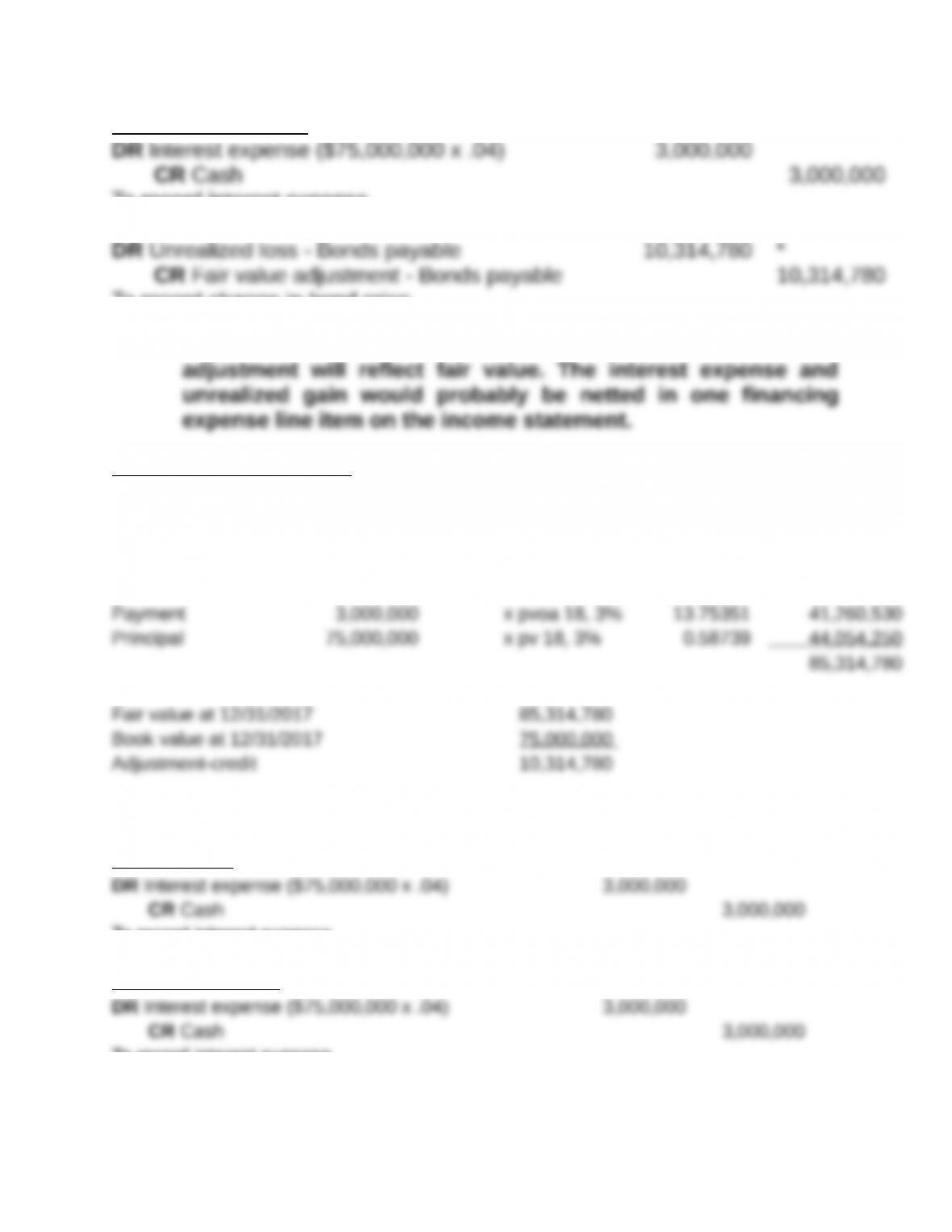

December 31, 2017

To record interest expense

To record change in bond price

After the second journal entry, the bonds payable net of the

*Price adjustment calculation

Remaining periods 18

Market rate 6%

Payments per year 2

Fair value (tables)

Requirement 3: General rates remain at 6% but Tango’s rate is 10%

June 30, 2018

To record interest expense

December 31, 2018

To record interest expense

To record change in bond price

To record change in bond price

a

Price adjustment that effects net income

The fair value changes because there are fewer payments remaining.

Fair value (tables)

This adjustment will decrease the book value of the bond.

b

Price adjustment that affects OCI

Fair value (tables)

Check of bond payable book value

Requirement 4 – Bond retirement on 1/1/2019

DR OCI – Bonds payable gain (credit risk)

17,549,490

To transfer gain from AOCI

Requirement 5 – Bond retirement on 1/1/2019 (no fair value option)

The gain is lower because the debt had not been increased to fair value in prior years.

P11-8. Citigroup and the fair value option (LO 11-4)

Requirement 1:

The bonds were issued on January 1, 2005 at par, so the proceeds

received by Citigroup are equal to the face value ($500 million) of

Requirement 2:

Using a market interest rate of 12%, the market value of the bonds

Requirement 3:

Let’s illustrate the effect of escalating credit risk using the results in

Requirements 1 and 2. Investors who believe on January 1, 2005

that Citigroup’s credit risk is accurately captured by the 6% stated

interest rate will be willing to pay par value ($500 million) for the

Now, let’s jump forward in time. If investors still believed on January

1, 2009 that Citigroup’s credit risk is accurately captured by the 6%

stated interest rate, they will continue to price the bonds at par value

($500 million). [You should verify this fact.] On the other hand, if

Requirement 4:

Citigroup elected to use the fair value option in accounting for its

debt, and thus recorded the following journal entry:

The fair value adjustment reduces the balance sheet carrying value

Requirement 5:

Opponents of the fair value accounting option for debt point to the

counter-intuitive financial statement result: as a company’s credit

risk increases and the slow march toward bankruptcy ensues, it

reports higher earnings because of the fair value accounting

P11-9. Chalk Hill: Using an interest-rate swap as a speculative

investment

(LO 11-7, LO 11-8)

Because the swap contract does not qualify for special hedge

accounting rules, two aspects of the solution in Exhibit 11.11 will

change: (1) interest expense on the company’s variable rate debt

January 1, 2017:

December 31, 2017:

December 31, 2018:

December 31, 2019:

P11-10. Hedging raw material price swings (LO 11-7, LO 11-8)

Requirement 1:

Pulp-paper futures contracts can be used to “lock in” a specific

price for anticipated future inventory purchases. However, the

Requirement 2:

If commodity prices fall, the value of Brosnan’s pulp-paper futures

contracts will also decline. At the same time, Brosnan will be

paying less for its anticipated paper purchases. Some or all of the

Requirement 3:

By executing a forward contract for ink with a supplier, Brosnan

can again “lock in” its inventory purchase price. The upside

potential for Brosnan is that the supplier (and Brosnan) may agree

Requirement 4:

There’s downside risk as well: Brosnan and the supplier may

agree to a contract price that is above the actual future price of ink.