P14-12 Evaluating the effects of unreasonable rate of return

assumptions (LO14-3, LO14-4, LO14-6, LO14-9)

Requirement 1: US GAAP pension expense

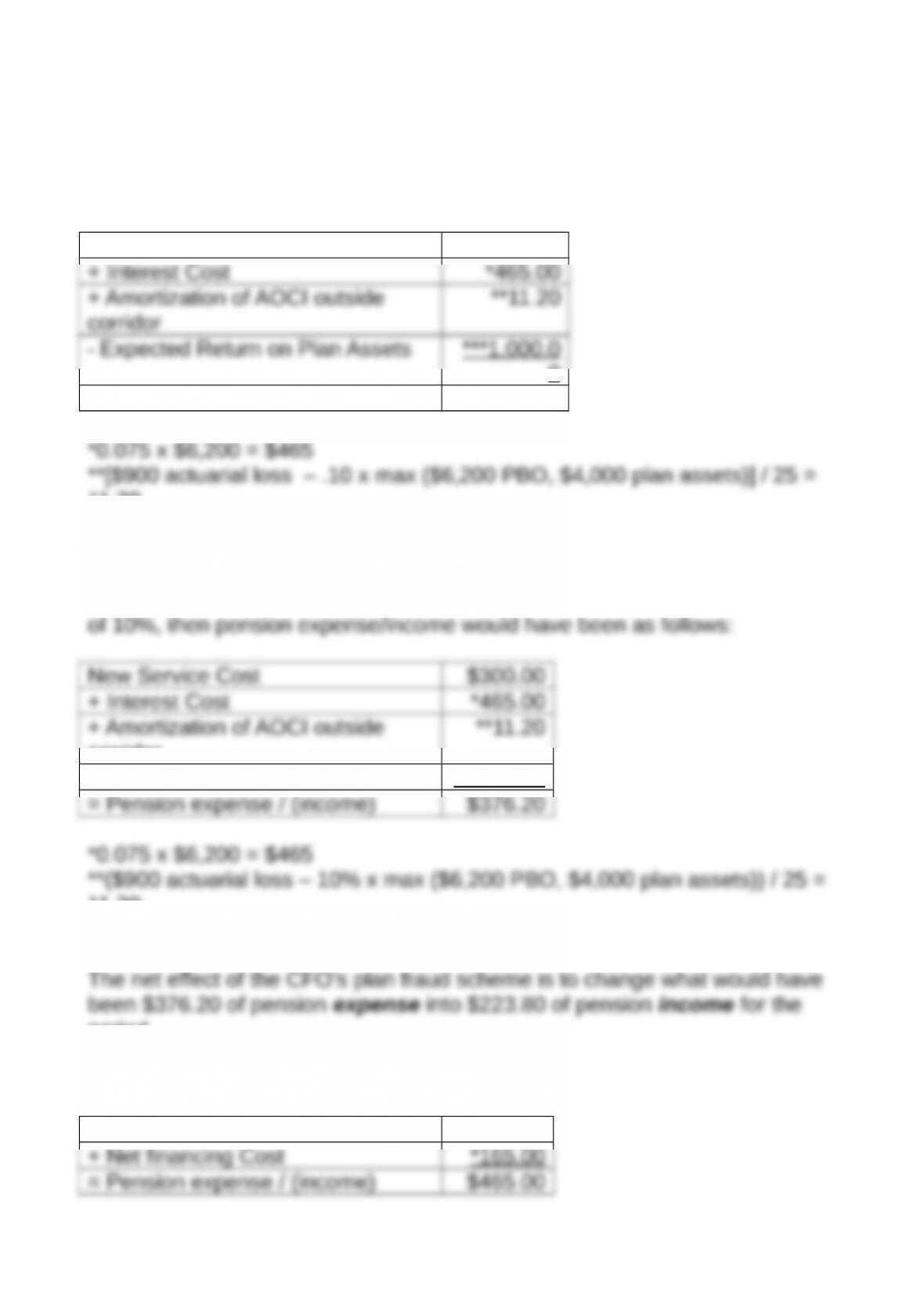

New Service Cost $300.00

0

= Pension expense / (income) ($223.80)

11.20

***0.25 x $4,000 = $1,000

Note that if the CFO had used the traditional expected return on plan assets

corridor

–Expected Return on Plan Assets ***400.00

11.20

***0.10 x $4,000 = $400

period.

Requirement 2: IFRS pension expense

New Service Cost $300.00

rate of return to equal the discount rate.

Requirement 3: Effect of overstatement on U.S. GAAP amounts

To compute the incremental effect under U. S. GAAP, we first need to update

computed as follows:

Jan 1 2016 AOCI Balance $900.00

= Dec 31 2016 / Jan 1 2014 AOCI Balance $1578.80

Note that if the CFO had used the traditional estimate for return on plan

Jan 1 2016 AOCI Balance $900.00

= Dec 31 2016 / Jan 1 2017 AOCI Balance $978.8

Therefore, the net effect of the income management efforts is that there is an

of the Fair Value of Plan Assets as follows:

Jan 1 2016 PBO Balance $6,200.00

= Dec 31 2016 / Jan 1 2017 PBO Balance $6,650.00

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale

or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted

on a website, in whole or part.

14-2

Jan 1 2016 FVPA Balance $4,000.00

= Dec 31 2016 / Jan 1 2017 PBO Balance $4,160.00

The corridor is 10% of Maximum $($6,650 PBO, $4,160 plan assets) or

$665.

In 2017, the amortization would be computed as follows:

[$978.80 actuarial loss – $665.00 corridor] / 25 years = $12.55

So, the “cost” of the aggressive accounting scheme is that 2017 pension

expense.

Requirement 4: Effect under IFRS

There is no incremental effect under IFRS because there is no

Financial Reporting and Analysis (7th Ed.)

Chapter 14 Solutions

Pensions and Postretirement Benefits

Cases

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale

or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted

on a website, in whole or part.

14-3

C14-1. GE Corporation: Interpreting OPEB disclosures (LO14-6, LO14-7)

Requirement 1:

(in millions)

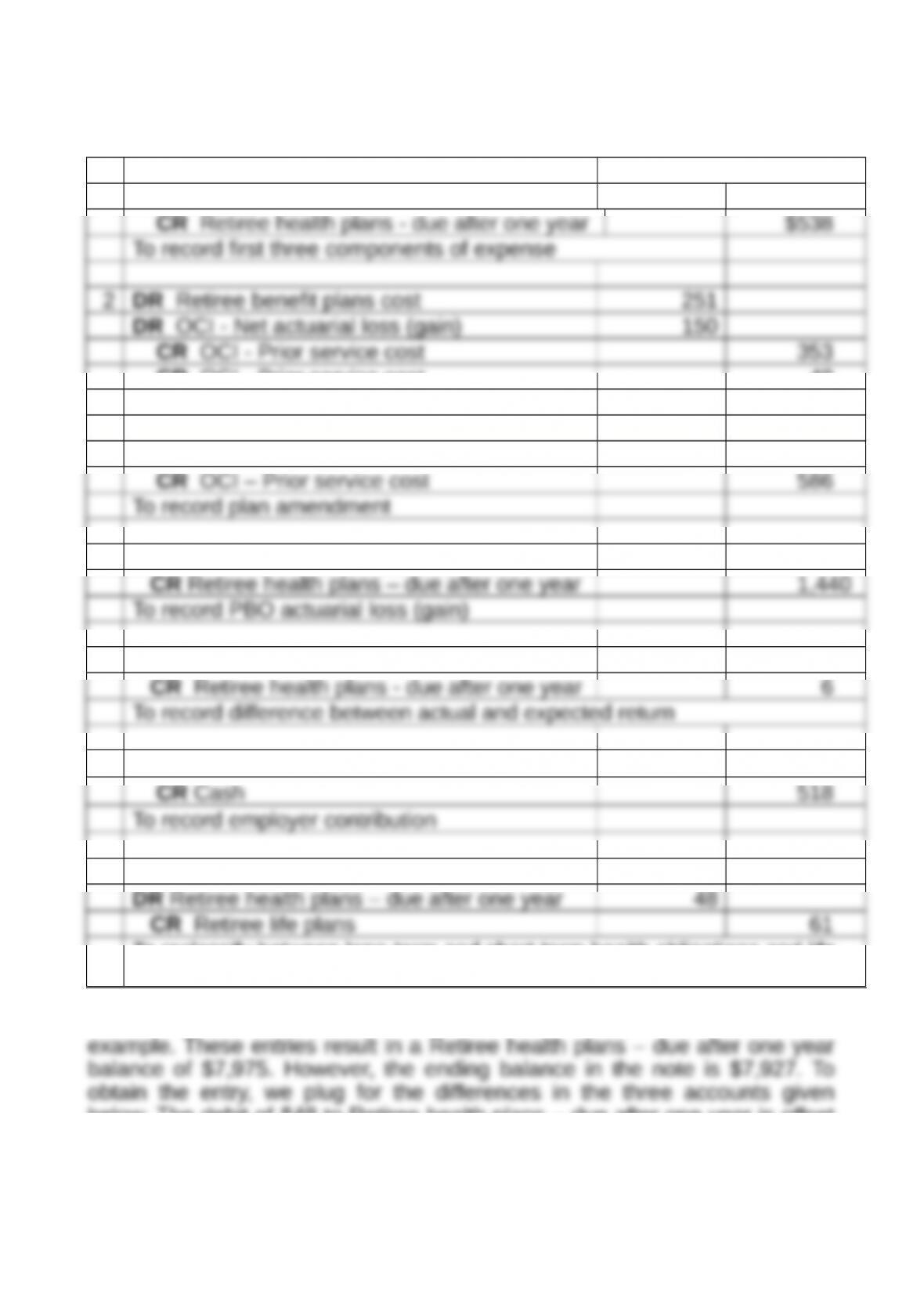

1DR Retiree benefit plans cost $538

CR OCI – Prior service cost 48

To record amortization components

3DR Retiree health plans – due after one year 586

4DR OCI – Net actuarial loss (gain) 1,440

5DR OCI – Net actuarial loss (gain) 6

6DR Retiree health plans – due after one year 518

7DR Retiree health plans – due within one year 13

To reclassify between long-term and short-term health obligations and life

insurance obligations

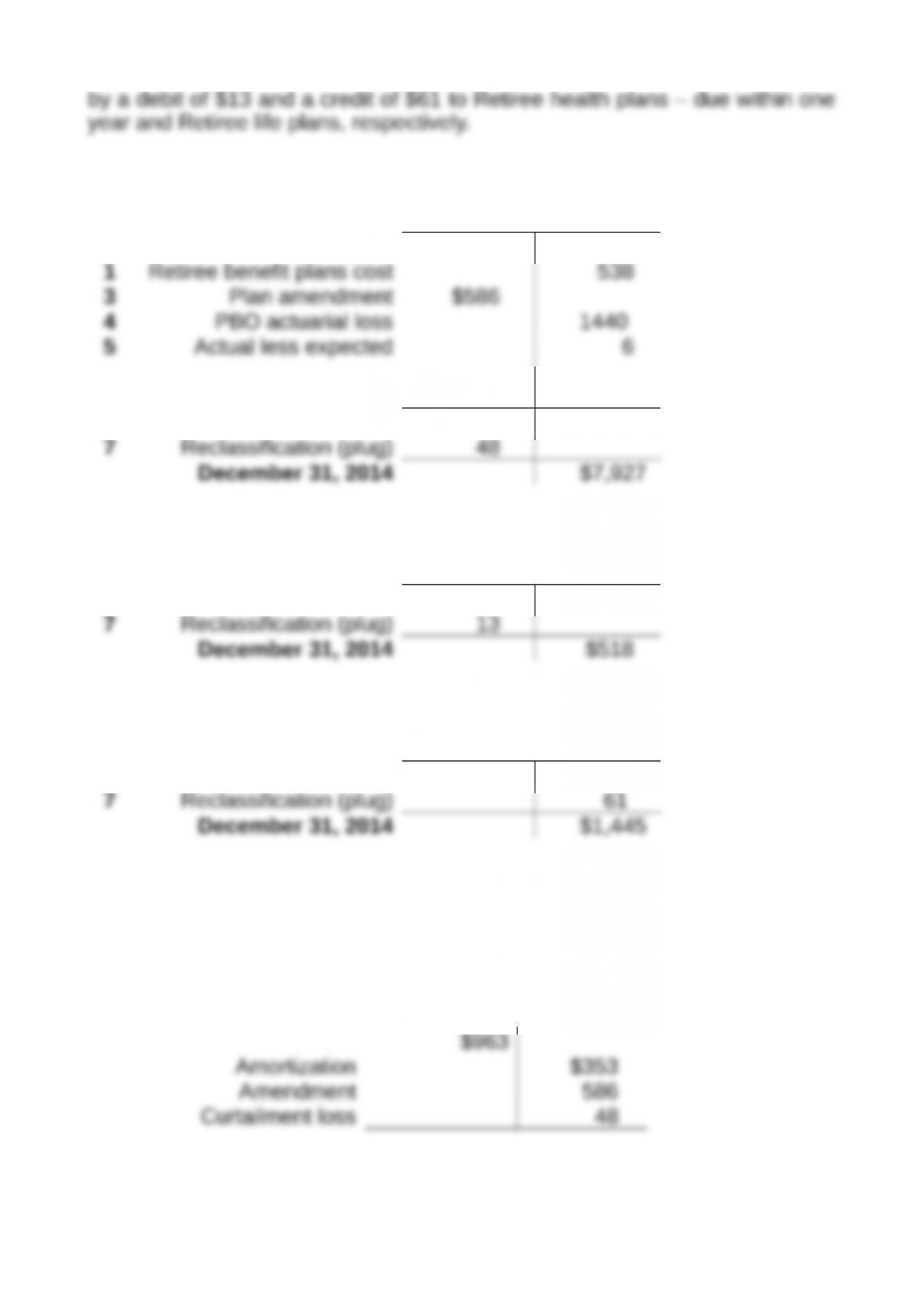

The first six entries are very similar to the ones made for the GE pension

below. The debit of $48 to Retiree health plans – due after one year is offset

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale

or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted

on a website, in whole or part.

14-4

Retiree health plans –

due after one year

January 1, 2014 $7,095

6Employer contribution 518

$7,975

Retiree health plans –

due within one year

January 1, 2014 $531

Retiree life plans

January 1, 2014 $1,384

Requirement 2:

Presented below are t-accounts for AOCI – prior service cost and

AOCI – actuarial (gain) loss.

AOCI –

prior service cost

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale

or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted

on a website, in whole or part.

14-5

$24

AOCI –

actuarial (gain) loss

$1,667

$71

The credits to OCI – prior service cost decreases GE’s AOCI – prior

service cost from a $963 debit balance to a $24 credit balance. The credits

ending $71 credit balance and the beginning $1,667 credit balance, or a

negative $1,596.

Note that the $353 prior service cost amortization and the $48 curtailment

represent new losses that increase the retiree benefit liability and the Net

actuarial loss.

in the statement of comprehensive income and balance sheet.

C 14-2. Novartis: Interpreting IFRS pension accounting (LO14-3, LO14-6,

LO14-9)

Requirement 1:

The adoption of IAS 19 (R) increased Novartis’ annual pension expense in

Requirement 2:

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale

or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted

on a website, in whole or part.

14-6

IAS 19 (R) required firms to adjust the prior year’s reporting to help with

instead chosen to expense through net income all at one time.

Requirement 3:

There are likely no cash flow implications (ignoring potential tax

projected benefit obligation or of the fair value of the plan assets.

C 14-3. ExxonMobil: Interpreting pension and OPEB footnote

disclosures (LO14-3, LO14-6, LO14-7)

Using the Excel template will save students considerable time

because they will not have to enter all of the amounts.

All amounts are in millions.

Requirement 1 – Assets or liabilities on the balance sheet

Funded status equals a liability of $8,598. It is computed as the December

ExxonMobil’s balance sheet.

Requirement 2 – Analysis of AOCI – Actuarial (Gains) Losses for U.S

pensions

Accumulated Other

Comprehensive Income –

Actuarial (Gains) Losses

(U.S. Pension Plans)

Beginning $ 6,589

Amortization from curtailment $ 499

(-307-830)

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale

or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted

on a website, in whole or part.

14-7

Requirement 3 – Expense for subsequent year

Service cost should be lower because of the increase in discount rate from

4.00% to 4.25%.

Interest cost will be similar to the 2015 amount. The increase in discount rate

reduced the December 31, 2015 PBO, as demonstrated by the PBO actuarial

indicates that the payments are for both unfunded and funded plans, while

note 1 under plan assets indicates that the payments are for only funded

plans.

Expected return will be 15% less because pension plan assets declined 15%

Based on the answer to part 2, there is a net decline in Actuarial losses

subject to amortization of $451 (ending balance of $6,138 less beginning

addition, we would not expect to see the curtailment loss amortization of

$499.

Given the lower amortization expense more than offsets the decline in

Requirement 4 – Short-term risk ratios

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale

or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted

on a website, in whole or part.

14-8

The U.S. and non-U.S. pension amounts should summed to obtain the values

below. Using the Excel template facilitates substantially these calculations.

Market Cap = Stock price of $77.95 x 4,156 million shares

= $323,960

Mkt Cap

$323,960

Mkt Cap

$323,96

0

Requirement 5 – Long-term risk ratios

The U.S. and non-U.S. pension amounts should summed to obtain the values

below. Using the Excel template facilitates substantially these calculations.

LT Pension PBO

=

$44,700

=

0.138

Requirement 6 – Interpretation of risk ratios

From the chapter, we see that the median short-term pension ratio is 0.02

exceeds the median but is below the 75th percentile. Its short-term OPEB ratio

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale

or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted

on a website, in whole or part.

14-9

of 0.024 is within the range of most OPEB ratios. Based on these ratios, we

would conclude that ExxonMobil has medium short-term retiree benefit risk.

The median long-term pension ratio 0.13, and the 75th percentile is 0.29, and

on these ratios, we would conclude that ExxonMobil has medium long-term

retiree benefit risk.

C 14-4. ExxonMobil: Comparing U.S. GAAP and IFRS pension and OPEB

accounting (LO14-9)

Note to Instructor: This solution focuses on ExxonMobil’s U.S. pension

Requirement – Comparison to IAS 19 (Revised 2011)

All referenced amounts are in millions.

1. ExxonMobil would still recognize its actuarial losses in OCI/AOCI and

return would by recognized in OCI in 2015, but they would not be

amortized in subsequent periods.

2. The effects of new amendments would be recognized as an increase or

costs are recognized immediately, pension and OPEB expense would

exclude amortization.

3. The expected return would be computed using the discount rate. If the

contributions and payments were made evenly during the year, then the

net income is $301 (interest cost of $785 less the recalculated expected

return of $484). The difference between the actual return of $(307) and

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale

or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted

on a website, in whole or part.

14-10

the recomputed expected return of $484 equals $791. This amount

financing cost of $301 (interest cost of $785 less the recomputed

expected return of $484) would be included as a financing component.

The amortization components would no longer be part of pension

between the expected and actual return would be recognized in OCI

without subsequent amortization.

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale

or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted

on a website, in whole or part.

14-11