E14-16. Determining postretirement health care expenses and plan

assets and liabilities balances (LO14-7)

Requirement 1:

Determination of postretirement health care expense for 2017:

Service cost $20,000

Interest on accumulated benefit obligation

Recognized actuarial loss 7 ,000

Postretirement expense $58 ,000

Requirement 2:

Determination of fair value of plan assets:

Ending fair value on 12/31/17 $40 ,000

Requirement 3:

Balance of accumulated postretirement benefit obligation (APBO)

at 12/31/17:

Beginning balance $300,000

E14-17. Determining plan assets, PBO, and AOCI for 2 years (LO14-3,

LO14-4)

2018 2017

Requirement 1 – Change in PBO

Beginning balance $799,400 $750,000

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 14-1

Actuarial loss (gain) (13,000) 4,400

Ending balance $837,364 $799,400

Requirements 2 and 3- Change in

plan assets and funded status

2018 2017

Change in plan

assets

Ending balance $753,400 $680,000

Funded Status $(83,964) $(119,400)

Requirement 4 – AOCI Actuarial losses (gains)

2018 2017

Beginning balance $(25,600) $ 0

Actual less expected return

Ending balance (57,400) $(25

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 14-2

Requirement 5 – OCI

OCI is the change in AOCI for the year. One method is to subtract the beginning

balance from the ending balance as follows:

2018 2017

Another approach is to sum the items giving rise to the loss (gain)

as follows:

2018 2017

$(18,800

All amounts are pretax.

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 14-3

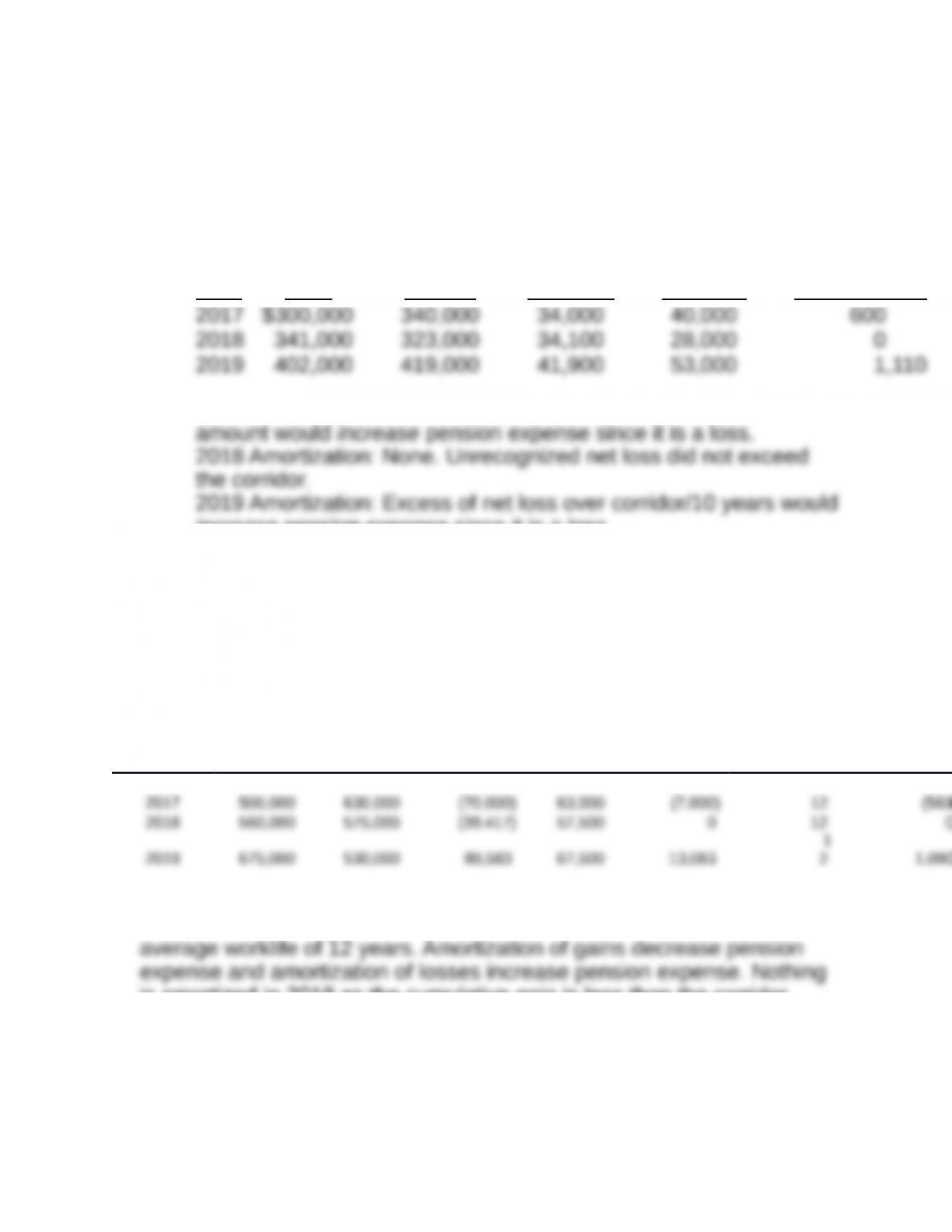

E14-18. Determining actuarial gain or loss amortization using the

corridor approach over three 3 years (LO14-3, LO14-4)

Amortization Net Actuarial (Gains) Losses—Corridor Approach:

Year PBO

Fair Market

Value of Plan

Assets Corridor

AOCI

Net loss Amortization

2017 Amortization: Excess of net loss over corridor/10 years;

increase pension expense since it is a loss.

E14-19. Determining amortization of actuarial gain or loss using the

corridor approach over three years (LO14-3, LO14-4)

Requirement 1: Effect on pension expense

Reporting January 1

January 1

Plan 1/1 AOCI

Increase

(Decrease)

Year PBO Assets (Gain) Loss – Corridor = Excess / Worklife =

To Pension

Expense

The corridor is the 10% of the greater of the 1/1/ plan assets or PBO.

The amount of the gain or loss outside the corridor is divided by the

is amortized in 2018 as the cumulative gain is less than the corridor.

Requirement 2 – AOCI balance

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 14-4

Amortization Current Year Current Year 12/31

Year

To Pension

Expense

Asset (Gain)

Loss

PBO (Gain)

Loss

AOCI (Gain)

Loss

201

6 (70,000)

201

7 583 60,000 (30,000) (39,417)

The AOCI is reduced for amortization and increased or decreased for

loss, and PBO (gain) loss columns.

Requirement 3 – Other comprehensive income

1/1 AOCI 12/31 AOCI

Other

Comprehensiv

e

Year (Gain) Loss (Gain) Loss (Income) Loss

2017 (70,000) (39,417) 30,583

Other comprehensive income is the change in AOCI for the year. It can

summing the middle three columns of the solution for Requirement 2

(see above).

E14-20. Determining pension elements (LO14-3, LO14-4)

Requirement 1:

Determination of fair value of plan assets for George at January 1,

2017:

Determine this from an analysis of changes in the fair value of plan

assets:

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 14-5

– Payments made to employees (204 ,000)

Ending fair value on 12/31/2017 $880 ,000

Fair value of plan assets at 1/1/2017 equals $924,000 to balance.

Requirement 2:

Expected dollar return on plan assets for 2017:

Expected dollar return on plan assets $ 55 ,440

Requirement 3:

Pension expense amount for 2017:

Service cost $196,000

Pension expense for 2017 $309 ,560

Requirement 4:

Actual dollar return $30,000

Requirement 5:

Pension expense $309,560

Pension asset (liability) $130,000

Cash $130,000

To record deferred loss

E14-21. Determining pension elements (LO14-3, LO14-4, LO14-6)

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 14-6

Requirement 1:

Prior Service Cost Amortization

Requirement 2:

Pension Expense for 2017:

Service cost $ 45,000

Pension expense $142 ,500

Requirement 3:

Fair value of plan assets at 12/31/2017:

Fair Value Plan Assets

1/1/2017 balance -0-

12/31/2017 balance 110,000

Requirement 4:

The projected benefit obligation at 12/31/2017:

65 ,000

Projected benefit obligation 12/31/2017

$760 ,000

Requirement 5:

Required pension expense journal entries for 2017:

DR Pension expense $142,500

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 14-7

CR Cash $110,000

Requirement 6:

Pension expense for 2018:

Service cost $ 49,000

Pension expense $147 ,600

Fair value of plan assets at 12/31/2018:

Fair Value Plan Assets

1/1/2018 balance 110,000

12/31/2018 balance $236 ,200

The projected benefit obligation at 12/31/2018:

Projected benefit obligation, 1/1/2018 $760,000

Projected benefit obligation, 12/31/2018 $883 ,000

The pension journal entries for 2018:

DR Pension expense $115,100

DR Pension asset (liability) $125,000

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 14-8

CR Cash $125,000

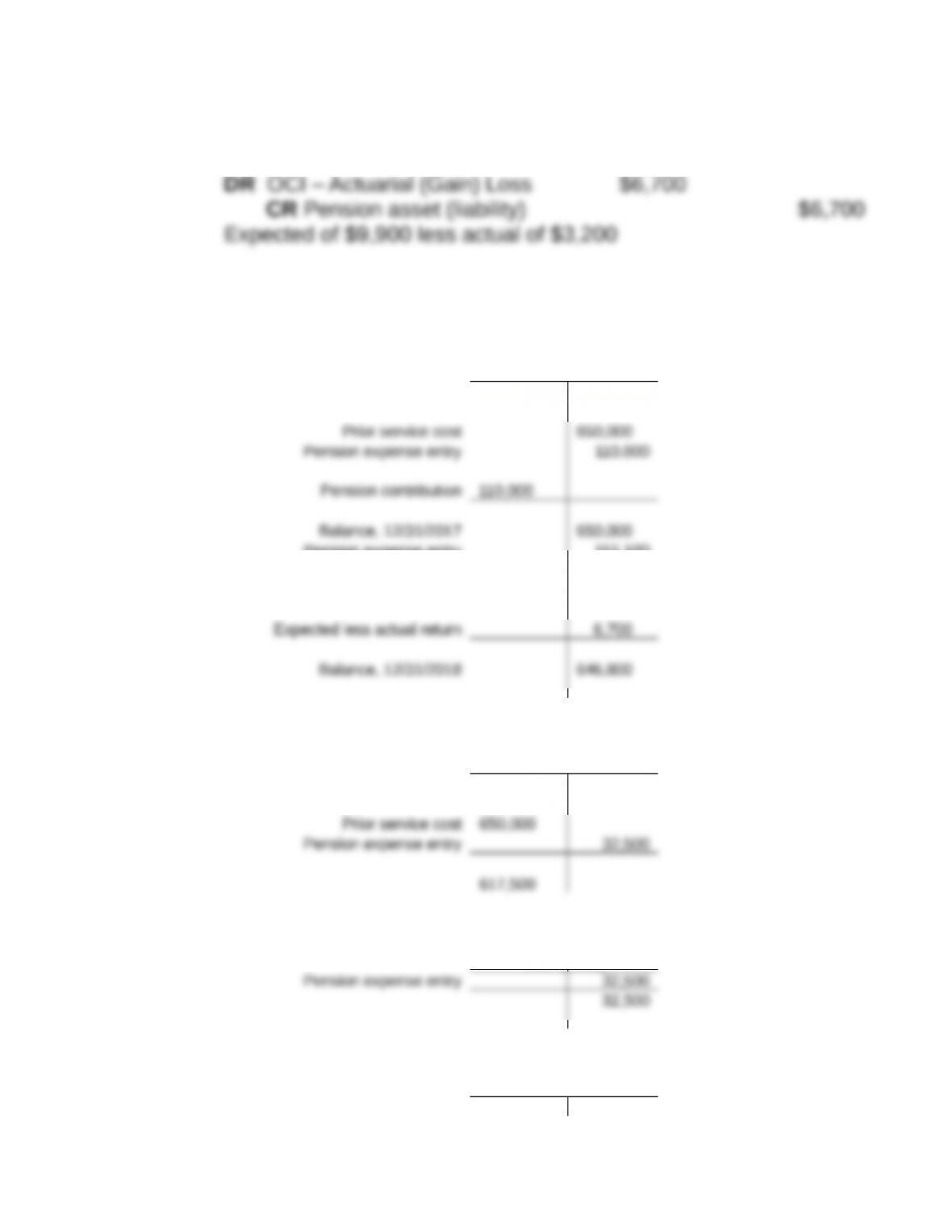

Requirement 7 – t-accounts for pension asset (liability) and AOCI

accounts

Pension

Asset (liability)

Balance, 1/1/2017 –

Pension expense entry 115,100

Pension contribution

125,000

OCI – Prior service

cost (2017)

OCI – Prior service

cost (2018)

OCI – actuarial (gain)

loss (2017)

–

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 14-9

–

Check that funded status equals balance

sheet account

2017 2018

Plan assets 110,000 236,200

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 14-10