Financial Reporting and Analysis (7th Ed.)

Chapter 9 Solutions

Inventories

Exercises

Exercises

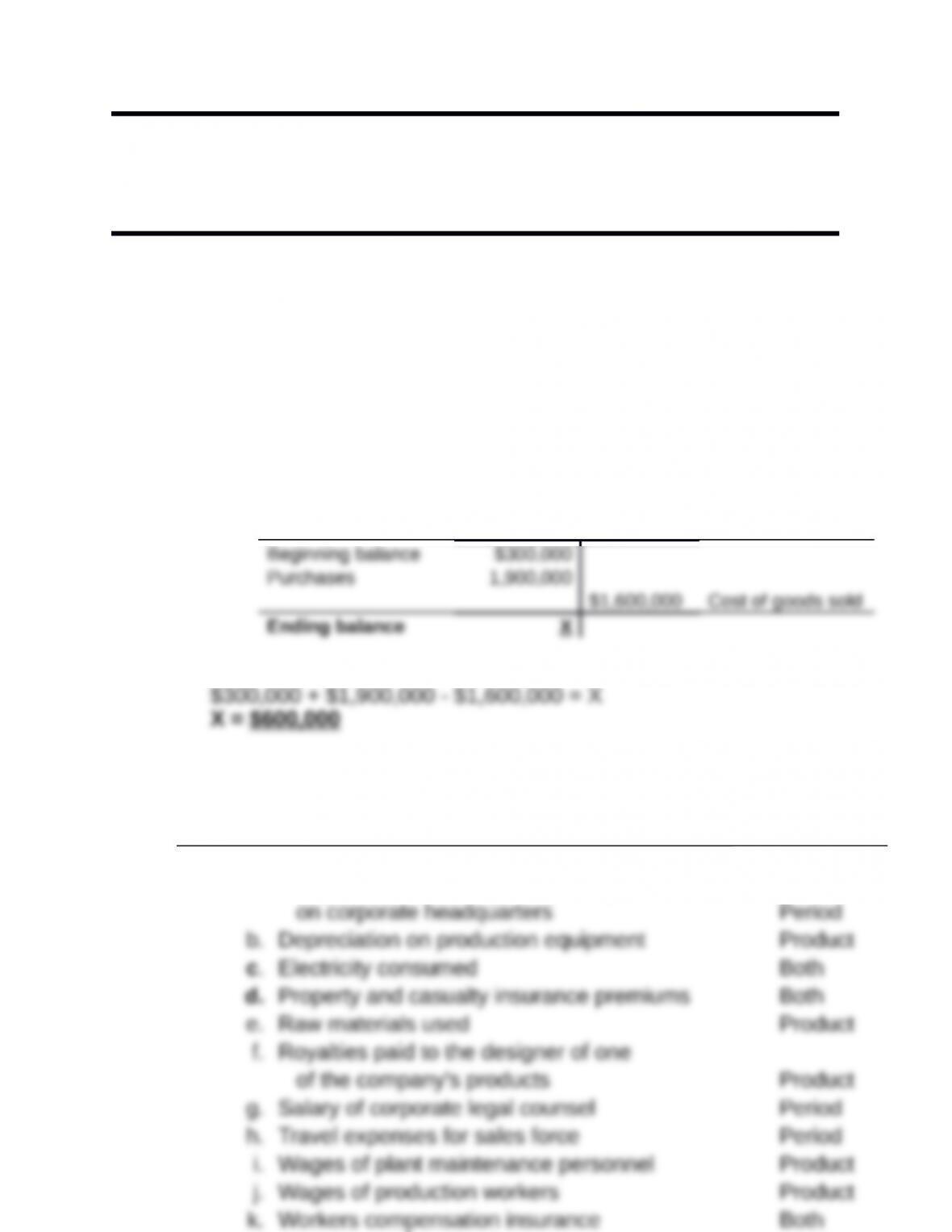

E9-1. Computing inventory amount from income statement data

(LO 1)

(AICPA adapted)

To find merchandise inventory, we first need to find cost of goods

sold. This figure can be computed by using the gross margin

percentage given. If profit is 20% of sales, then cost of goods sold

must be (1-20%) or 80% of sales. So 80% of $2,000,000 is

$1,600,000—cost of goods sold. Now we can look at the T-account

for the answer.

Inventory

Solving for X:

E9-2. Distinguishing between product and period costs (LO 3)

Now

we

Cost

Nature of incurred cost Classification

a. Comprehensive liability insurance premiums

PPossible cost allocation approaches for costs that are both product

and period costs:

c. Electricity consumption is metered. Electric bills relating to usage at

production facilities would be considered product costs. Electricity

d. Property and casualty insurance premiums may be allocated

between product and period costs based on the value of the insured

k. Workers compensation insurance pays expenses related to on the

job injuries. This coverage applies to all employees, not just factory

E9-3. Computing ending inventory and cost of goods sold under

different cost flow assumptions (LO 2, 4)

(AICPA adapted)

For all the cost flow assumptions, we first compute Goods available

for sale first. Second, we then compute Ending inventory based on

the appropriate cost flow assumption. Third, we compute Cost of

Goods available for sale:

A physical count yields 200 units, and we also get 200 by

subtracting 350 units sales from the 550 units available.

Requirement 1: FIFO

Under FIFO, the most recent purchases are in ending inventory.

Remaining in ending inventory:

FIFO

By subtracting the ending inventory amount of $3,500 from the

goods available for sale, we compute cost of goods sold as follows:

Requirement 2: LIFO

Under LIFO the earliest purchases are assumed to be in ending

inventory. In this case, all the units come from beginning inventory

Under LIFO, ending inventory is $300 less than it is under FIFO.

We compute cost of goods sold the same way we computed it

under FIFO. However, now we subtract LIFO ending inventory.

Note that LIFO cost of goods sold exceeds FIFO cost of goods sold

Requirement 3: Average cost

For average cost, we divide goods available for sale by the units

available for sale. These totals come from the first table in our

solution. Specifically,

To compute ending inventory we multiply this average unit cost by

the number units in inventory. Specifically,

To compute cost of goods sold, we can multiply the units sold by

this average unit cost as follows:

Alternatively, we can compute it by subtracting ending inventory

from the cost of goods available for sale, as we did for LIFO and

FIFO.

E9-4. Computing cost of goods sold (LO 1)

(AICPA adapted)

We can find cost of goods sold for 2017 by analyzing the inventory

account.

Inventory

Purchases can be found by adding together the disbursements for

We know that the ending balance in inventory is $10,000 less than

E9-5. Computing sales from inventory information (LO 3, 12)

(AICPA adapted)

To find Dumas’ sales for 2017, we need to first look at the inventory

T-account.

Finished Goods Inventory

Since we already know cost of goods manufactured, we do not

need to analyze work in process inventory.

We solve for cost of goods sold as follows:

Now that we know cost of goods sold, we can solve for sales using

this figure and the gross profit amount given. Gross profit is the

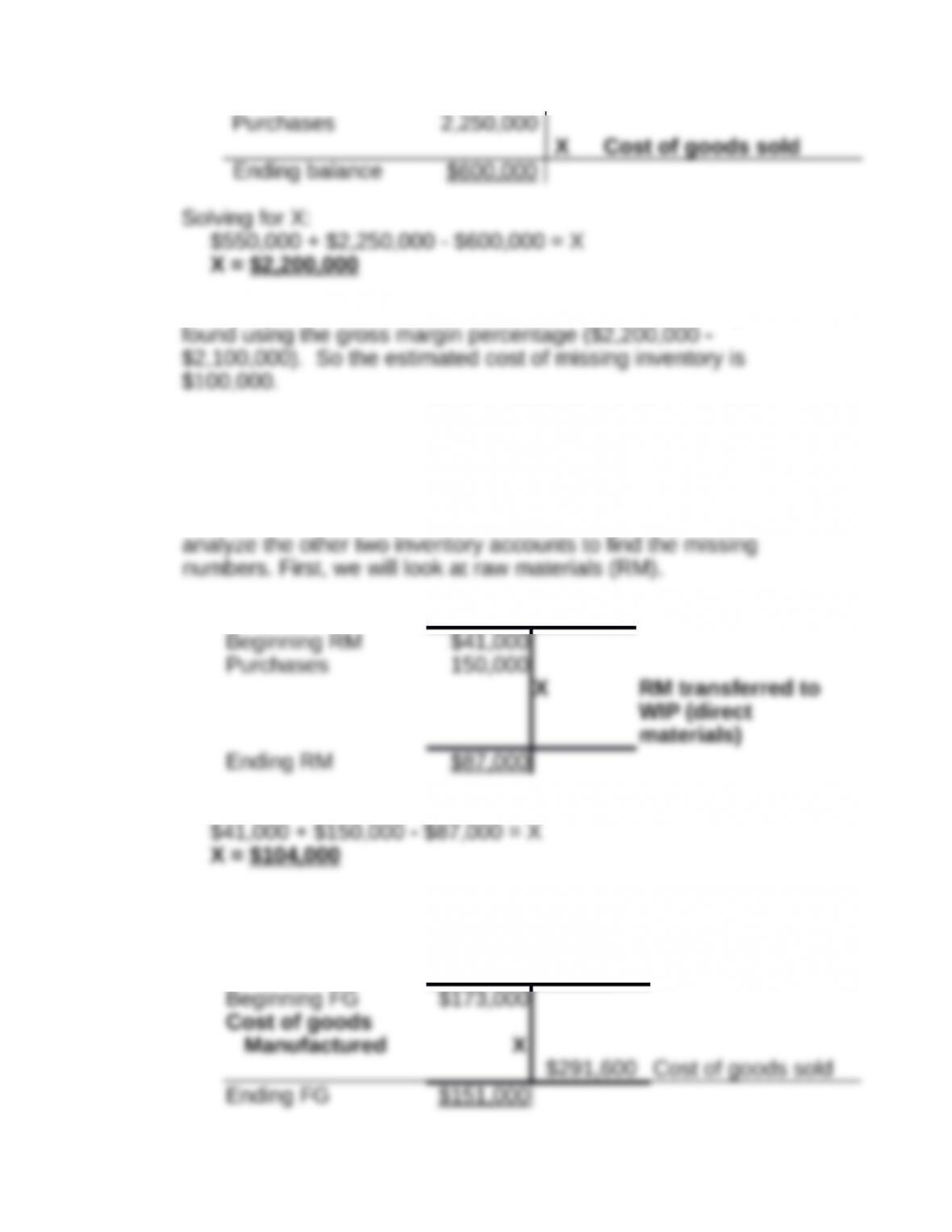

E9-6. Estimating missing inventory (LO 1)

(AICPA adapted)

In this problem, we need to determine the accuracy of the inventory

account. We know that cost of goods sold is 70% of sales [70% of

Inventory

The amount we solved for is $100,000 more than cost of goods sold

E9-7. Computing work-in-process inventory from balance sheet and

income statement information (LO 1, 12)

(AICPA adapted)

To solve for ending work in process inventory (WIP), we need to

Raw Materials

We can now solve for X (direct materials).

Now we have direct materials of $104,000 to plug into WIP. But we

also need to know cost of goods manufactured, so we must analyze

finished goods (FG).

Finished Goods

Now that we have direct materials and cost of goods manufactured,

we can solve for the ending balance of WIP inventory.

Work In Process

Finally, we can now solve for ending Work in Process.

E9-8. Computing inventory under three flow assumptions (LO 4)

(AICPA adapted)

Units and prices for 2017 beginning inventory and purchases are:

Units Price Extended

The table shows that goods available for sale in units is 5,000 and

goods available for sale in dollars is $51,750. The exercise states

that there are 1,600 units in ending inventory. We price these units

Requirement 1: FIFO

Under FIFO, the most recent purchases are in ending inventory.

Remaining in ending inventory:

600 @ $11.00 6,600

Requirement 2: LIFO

Under LIFO the earliest purchases are assumed to be in ending

inventory. In this case, 800 units come from beginning inventory

and the remaining 800 come from the first purchase.

Under LIFO, ending inventory is $2,800 less than it is under FIFO.

We compute cost of goods sold the same way we computed it

under FIFO. However, now we subtract LIFO ending inventory.

Requirement 3: Weighted average

For average cost, we divide goods available for sale by the units

available for sale. These totals come from the first table in our

solution. Specifically,

To compute cost of goods sold, we can multiply the units sold of

Alternatively, we can compute it by subtracting ending inventory

from the cost of goods available for sale, as we did for LIFO and

FIFO.