P13-15. Financial statement effects of tax rate change

Requirement 1:

Both companies project pretax income of $100 million. Because

there are no permanent differences and no change in cumulative

temporary differences in 2017 for either company, both are also

Requirement 2:

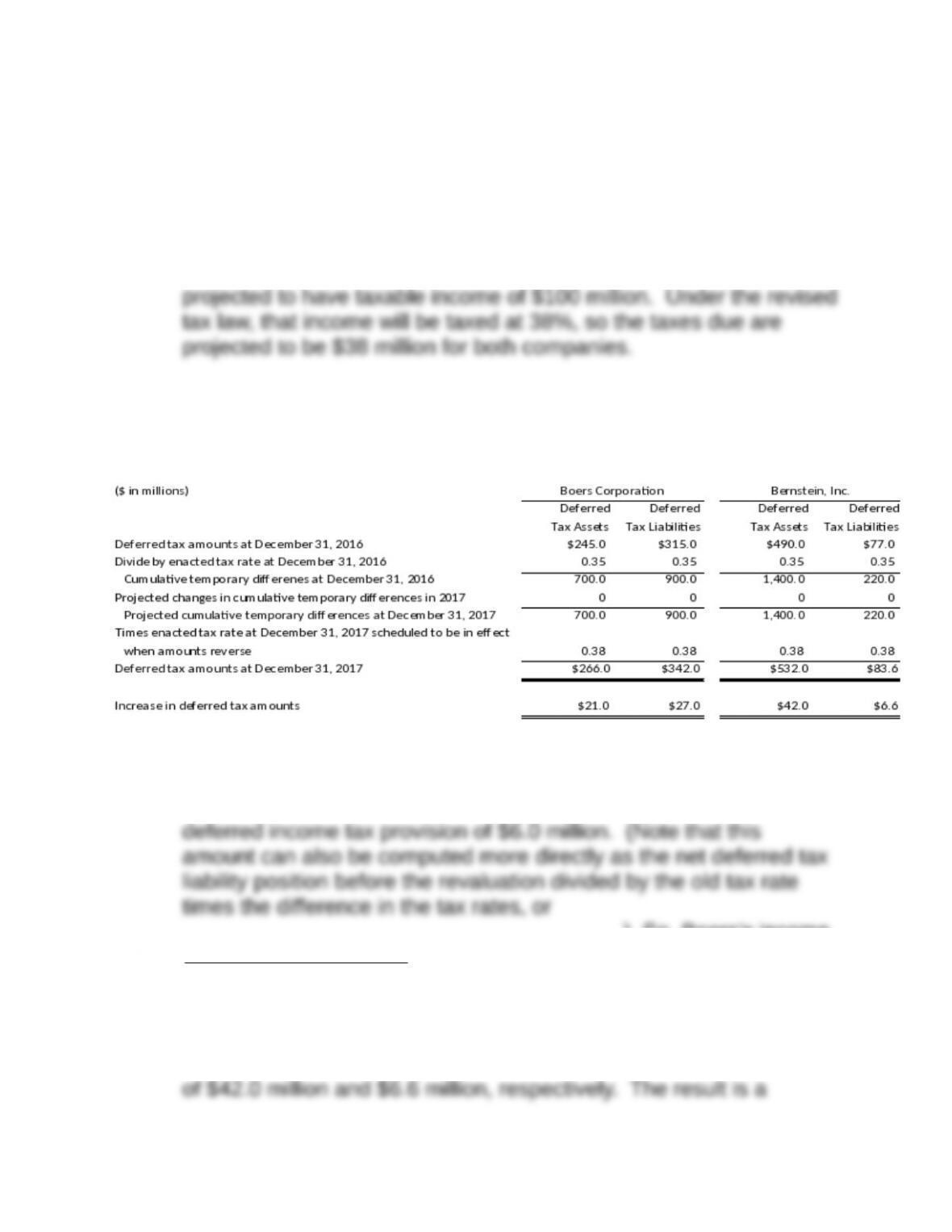

The following analysis shows the changes in the deferred tax assets

and liabilities for each firm during 2017:

Boers will have increases in its deferred tax assets and liabilities of

$21.0 million and $27.0 million, respectively. The result is a

$315 $245 (0.38 0.35) $6

0.35

million million million

–· – =

). So, Boers’s income

tax expense is $38 million + $6 million = $44 million.

Bernstein will have increases in its deferred tax assets and liabilities

of $42.0 million and $6.6 million, respectively. The result is a

deferred income tax provision of negative $35.4 million. The

provision is negative because Bernstein is in a net deferred tax

Income Tax Reporting

Cases

Cases

C13-1 Pepsico: Analyzing the tax note

Requirement 1 ($ in millions):

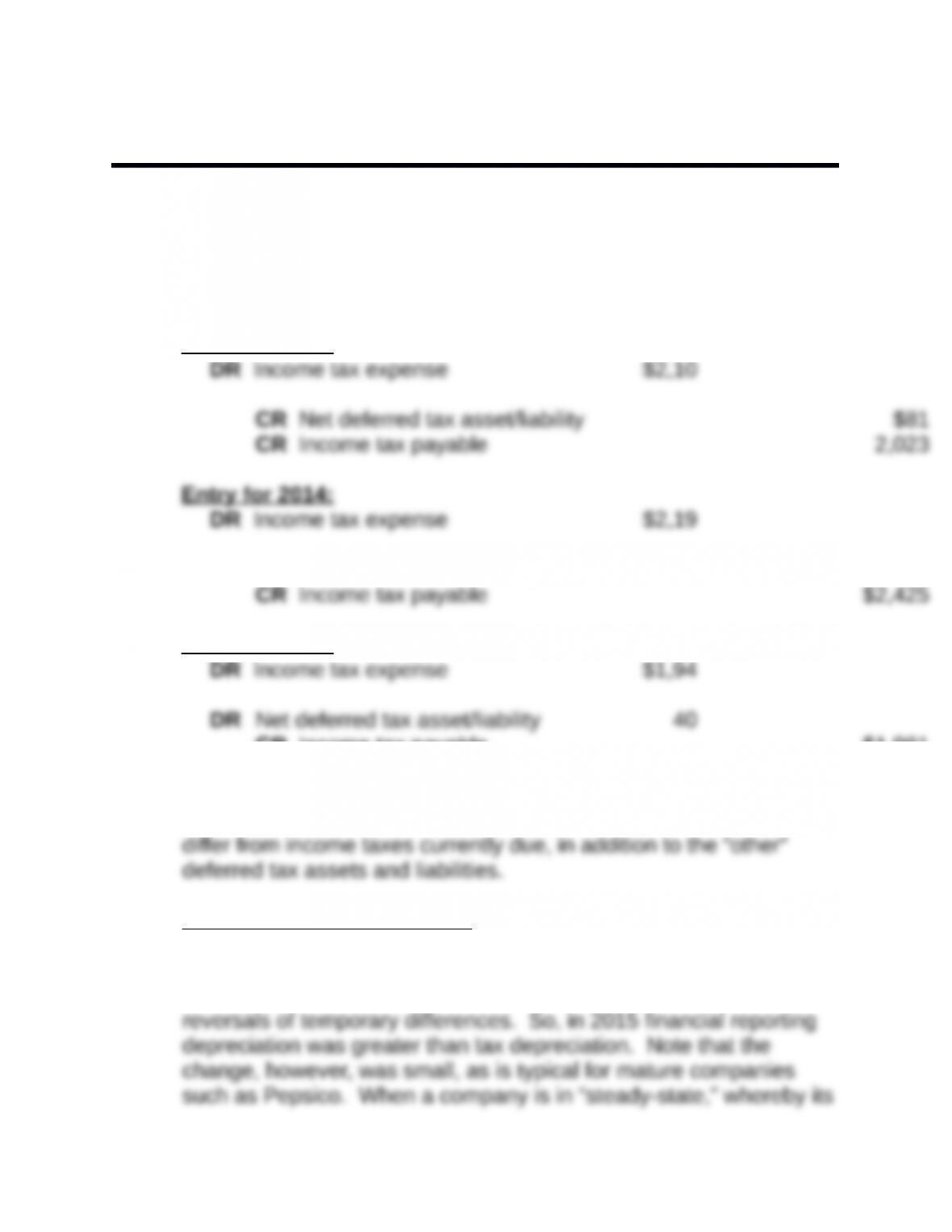

Entry for 2013:

DR Net deferred tax asset/liability

Entry for 2015:

CR Income tax payable $1,981

Requirement 2:

Pepsico identifies several items that cause income tax expense to

Property, plant and equipment: This deferred tax liability arises

when a company uses a more accelerated depreciation method for

tax purposes than in its financial statements. The amount of the

deferred tax liability decreased slightly in 2015, indicating net

Intangible assets other than nondeductible goodwill: This deferred

tax liability arose because amortization is recognized faster for tax

purposes than for financial reporting. The effect is similar to that for

depreciation differences. It is common for intangibles to be

Net carryforwards: This deferred tax asset decreased slightly,

indicating carryforwards incurred in 2015 were less than

carryforwards used. Although Pepsico is profitable overall, it can

still have carryforwards if they pertain to jurisdictions where Pepsico

Stock-based compensation: This deferred tax asset decreased in

2015, indicating a net reversal. Stock-based compensation creates

a deferred tax asset because compensation expense related to

non-qualified stock options is recognized earlier for financial

Retiree medical benefits, Other employee-related benefits: In both

of these cases, there is a deferred tax asset because expense is

recognized earlier than a tax deduction is permitted. Accrual

accounting causes the costs of providing benefits to be accrued as

Pension benefits: Pension benefits, like other benefits, are accrued

over an employee’s working years for financial statement purposes.

However, pension plans generally create an income tax deduction

when contributions are made to the plan. The firm does not have to

wait until the benefit payment is made to take the tax deduction. As

Requirement 3:

The information in the income tax note about the income tax

provision pertains only to income taxes related to continuing

operations. That is, the $1,941 million shown for 2015 in the

Provision for income taxes section of the note is equal to the

amount shown in the income statement as income tax expense.

C13-2. Alphabet, Inc.: Analyzing tax notes

Requirement 1:

($ in millions)

Requirement 2:

Let X = pre-tax book income ($ in millions):

Expected tax provision at federal statutory tax rate =

Requirement 3:

Requirement 4:

The deferred tax liability related to depreciation and amortization

Let Z = difference between taxable income and book pre-tax income

($ in millions)

Requirement 5:

The foreign rate differential item in the tax rate reconciliation is

negative in all three years, indicating that the income tax provision is

lower than it would be if all pretax income had an associated 35%

income tax provision. Therefore, the income tax rate on foreign

income is, on average, lower than the 35% U.S. rate. Although the

Requirement 6:

The tax rate reconciliation includes any item that causes the income

tax provision to deviate from 35% of pretax income. A tax credit

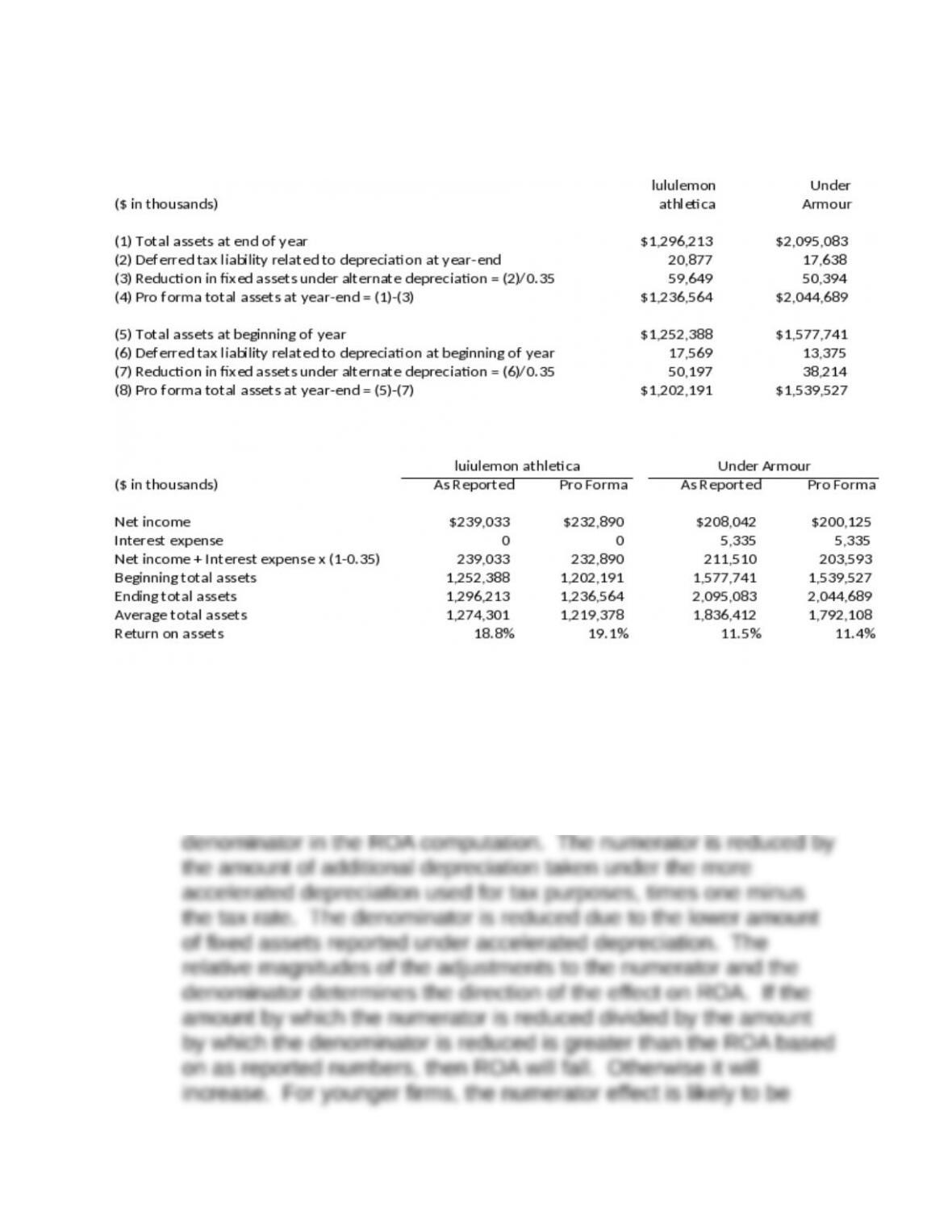

C13-3. lululemon athletica vs. UnderArmour: Adjusting for

depreciation differences

Requirement 1:

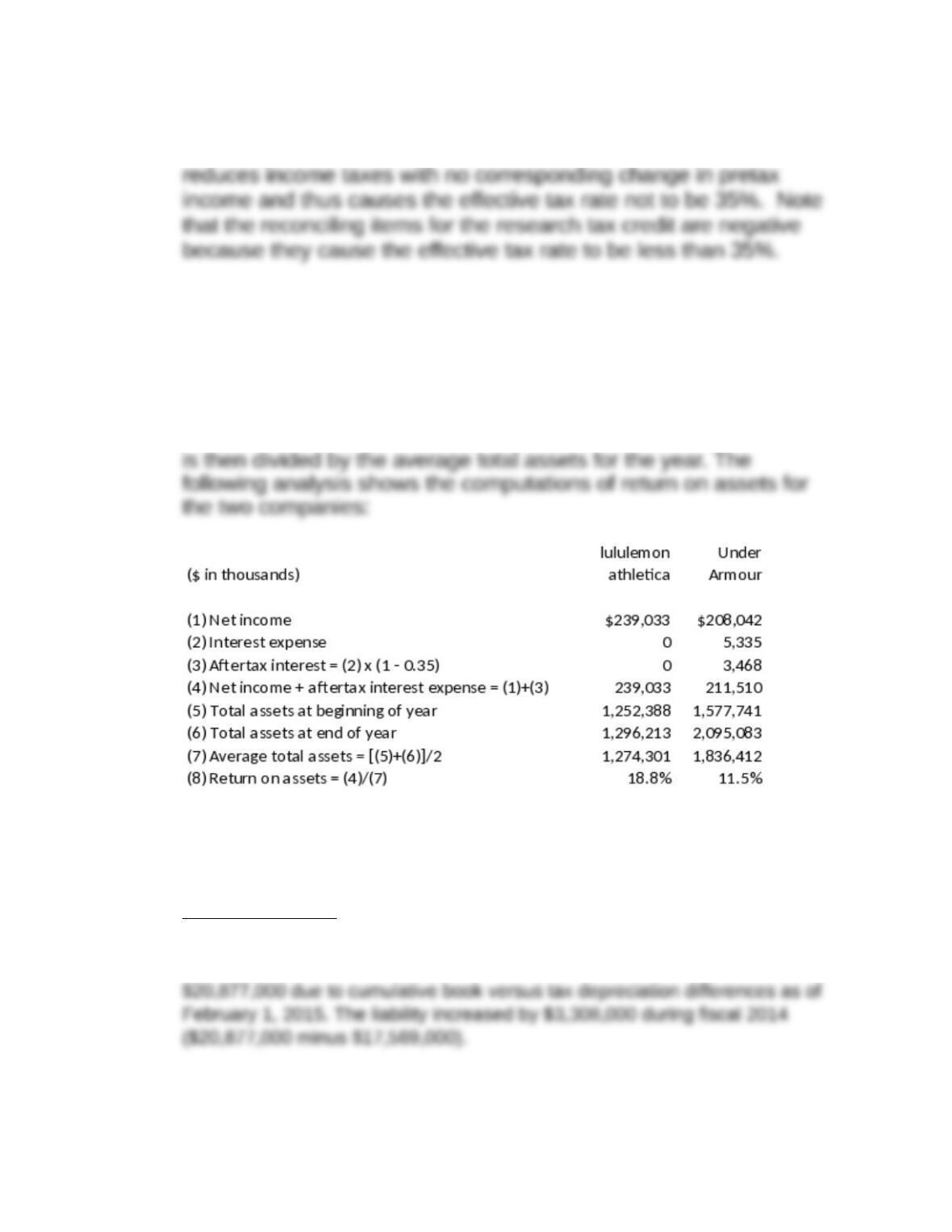

To compute return on assets, we add back interest expense times

one minus the marginal income tax rate to net income. This amount

Requirement 2:

lululemon athletica

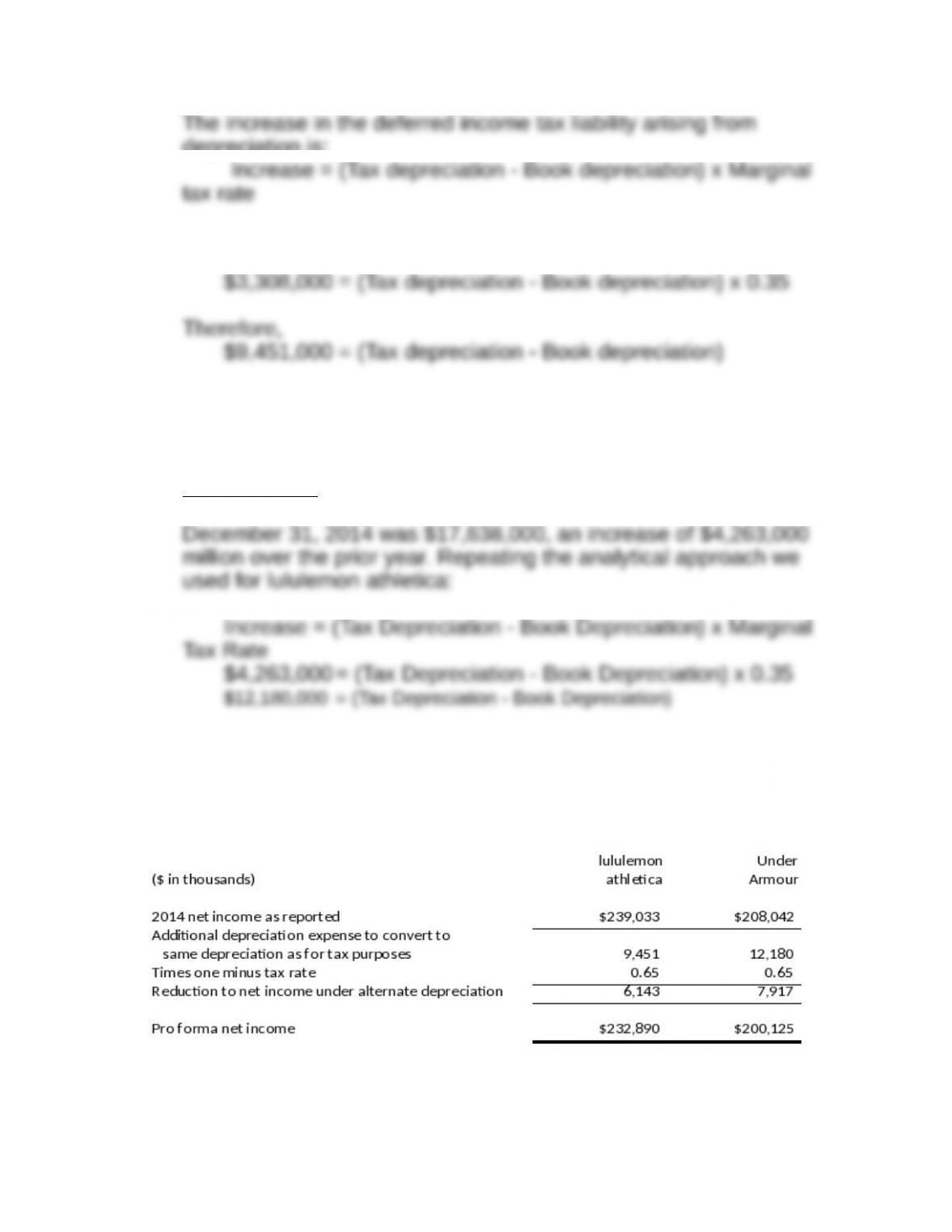

Begin by looking at the data for fiscal 2014 (year ended February 1, 2015) for

lululemon athletica. The deferred tax liability related to depreciation is

depreciation is:

Assuming the company’s marginal tax rate is the 35% statutory rate, we get:

Because lululemon athletica’s book depreciation was $58,364,000, tax

depreciation must have been $58,364,000 + $9,451,000 = $67,815,000.

Under Armour

Under Armour’s depreciation-related deferred income tax liability at

Under Armour’s book depreciation was $72,093,000, so tax depreciation must

have been $72,093,000 + $12,180,000 = $84,273,000.

Requirement 3:

Requirement 4:

Requirement 5:

The adjustment process affects the two companies’ return on assets

figures in the opposite direction, albeit not by significant amounts.

In lululemon athletica’s case, return on assets increased with the

adjustment, from 18.8% to 19.1%. For Under Armour, ROA fell from

11.5% to 11.4%. The reason the effect can be in either direction is

because the adjustment affects both the numerator and the

Requirement 6:

The adjusted figures are not affected by variations in depreciation reporting choices

across firms. So, the operating results of the two companies can be compared more