Financial Reporting and Analysis (7th Ed.)

Chapter 6 Solutions

The Role of Financial Information in Valuation

and Credit Risk Assessment

Problems/Discussion Questions

Problems

P6-1 Interpreting stock price changes

Requirement 1:

AMD’s announcement differed from analysts’ expectations and

presumably also from the market’s expectations. One would expect

the price to adjust to reflect the new updated information. Note that

the price revision would capture not only how the current period’s

performance differed from expectations, but also any revision in

Requirement 2:

Stock prices change when investors’ beliefs about current or future

performance change. In scenario (a), the reduced revenue was

predictable based on public information available prior to the

announcement. This suggests that at least some of the $200 million

difference was due to the analysts’ forecasts that were available

P6-2. Assessing credit risk using cash flow forecasts

Requirement 1:

If Randall’s cash flow forecasts are accurate, it will be unable to

repay the loan at the end of 2020. At the end of 2017, Randall will

have only $95,000 of cash flow available to make loan interest and

principal payments. This amount grows to $1,815,000 by the end of

Unless Randall has cash available other highly liquid assets that

Requirement 2:

There are several ways Randall could enhance its creditworthiness

and reduce its credit risk. One approach is to focus on generating

more operating cash flow each year by growing sales, reducing

costs, or both. A second approach is to agree contractually not to

pay dividends without bank approval. Curtailment of the company’s

planned dividend payments would add another $400,000 to the

P6-3. Valuing growth opportunities

Requirement 1:

The cost of equity capital for eBay is higher than that of Wal-Mart

because eBay has a riskier cash flow stream than does Wal-Mart.

Wal-Mart has a long history of predictable earnings and operating

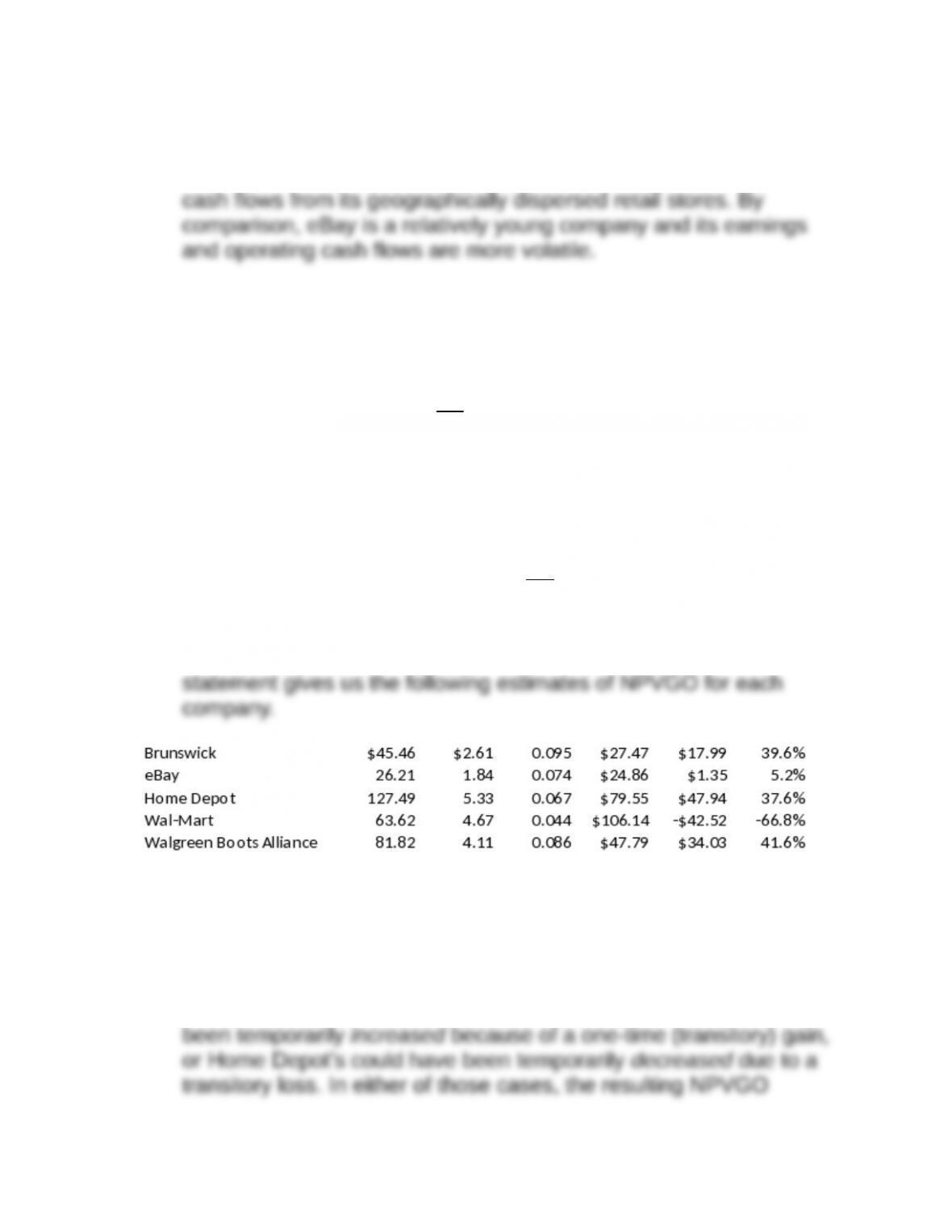

Requirements 2 and 3:

To find the NPVGO for each company, you need to solve for

NPVGO in the following expression:

P

0

= X0

r + NPVGO

where P is the current stock price, X is current reported earnings

per share for the year, and r is the estimated cost of equity capital.

Rearranging terms gives us:

0

0

–

X

NPVGO P r

=

Using this expression and the data provided in the problem

Requirement 4:

The NPVGO at Home Depot is greater as a percent of share price

than that for eBay because investors believe that Home Depot has

better growth opportunities—a higher rate of growth and more

profitable growth. Alternatively, eBay’s earnings per share may have

Requirement 5:

On its face, a negative NPVGO suggests and expected earnings

growth rate that is negative. However, the result could also be due

P6-4. Predicting future cash flow

Requirement 1:

If, as the problem statement indicates, credit customers pay 30 days

after the sale, the month-end accounts receivable balance will be

Note that January cash collections ($510) are equal to the previous

December’s outstanding accounts receivable ($500) plus cash

sales in January ($10 = $620 Sales minus $610 month-end balance

Requirement 2:

March cash collections ($640) are equal to February’s outstanding

Requirement 3:

An analysis of the inventory account reveals that March purchases

Requirement 4:

If, as the problem statement indicates, suppliers are paid 60 days

after health care products are purchased, the March cash payment

Requirement 5:

Visual inspection of the data suggests that current month’s gross

profit is a better predictor of next month’s net cash flow than is

current month net cash flow. This intuition is confirmed statistically

Requirement 6:

In general, accrual earnings smoothes out the period-to-period

lumpiness that sometimes arise in operating cash flows. This

lumpiness is produced by period-to-period variations in business

P6-5. Tail O’ the Dog: Fair value measurement

Requirement 1:

The least relevant measure for purposes of fair value determination

is the parking lot’s 1962 historical cost ($12,000). The price paid 50

Here’s another example to illustrate why historical cost is irrelevant

to fair value determination. In 1626, Peter Minuit bought Manhattan

island from the local Indians for a load of cloth, beads, hatchets, and

Requirement 2:

Quoted prices from an active market for identical assets (Level 1 fair

value measurement) are not available in this setting, but observable

inputs (Level 2) are available. In particular, there are recent quoted

Requirement 3:

Level 2 fair value measurements include quoted market prices for

similar assets. There are two Level 2 observable inputs present in

this fact pattern: the recent (market) price paid for the parking lot

($500,000) and for the residential beach front lot ($1.2 million).

Requirement 4:

Auditors are especially challenged by Level 3 fair value

measurements because it is difficult (if not impossible) to verify the

accuracy and precision of the forecasted income stream that forms

P6-6. Sonic Solutions: Discounted cash flow valuation

Requirement 1:

Free cash flow is defined in the spreadsheet as EBITDA minus

capital expenditures and cash taxes, where EBITDA refers to

earnings before interest, taxes, depreciation and amortization. This

spreadsheet definition differs in several ways from how accountants

and auditors define free cash flow. In particular, it ignores: (1) other

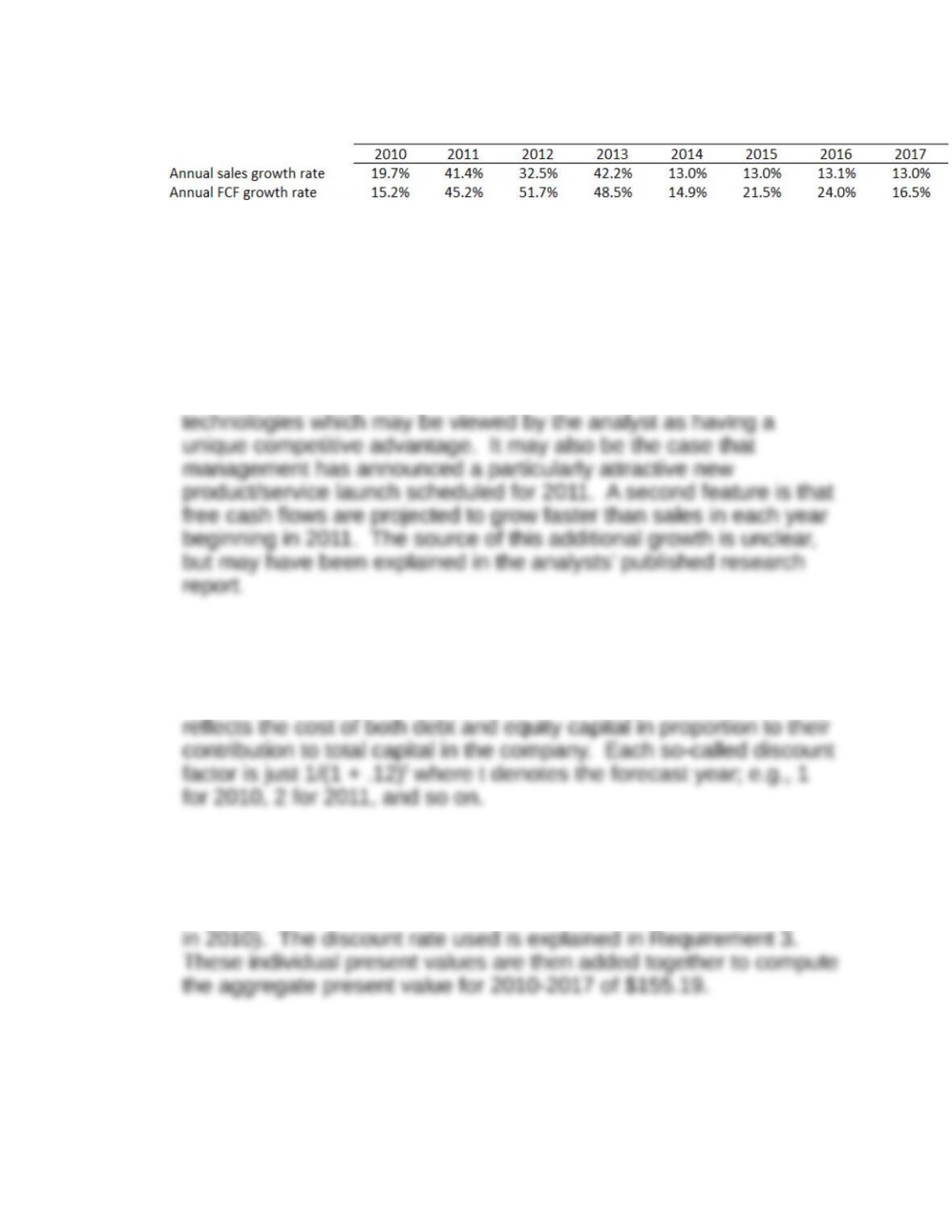

Requirement 2:

The annual percentage rates of sales growth and free cash flow

growth are:

Several features of these growth rates are noteworthy. First, the

analyst is projecting rather high levels of sales growth in 2011

through 2013, which would be quite unusual for an established

company operating in a mature product market. However, Sonic

Solutions develops digital media products, services and

Requirement 3:

The 12% weighted-average cost of capital (WACC) serves as the

discount rate used in computing the present values shown in the

spreadsheet. WACC represents a blended discount rate that

Requirement 4:

Each forecasted free cash flow amount (e.g., $4.6 in 2010) is

multiplied by a corresponding discount factor (e.g., 0.89286 in 2010)

to arrive at a present value of the future free cash flow (e.g., $4.11

Requirement 5:

This figure represents the present value of free cash flows occurring

beyond 2017. Analysts typically calculate this terminal present

value as follows:

TPV =FreeCash FlowT

(

WACC −growth

)

x discount factorT

where T denotes the spreadsheet terminal year (2017). If you insert

$79.8 as the terminal-year free cash flow forecast (from the

spreadsheet), 0.40388 as the discount factor, and 0.12 as the

Requirement 6:

Notice that free cash flow is defined for spreadsheet purposes as a

“before interest” figure, and that the discount rate is a

weighted-average cost of capital (WACC). Both spreadsheet

Requirement 7:

If equivalent assumptions are used, the share value estimate

calculated using an abnormal earnings approach will be identical to

Requirement 8:

The share value estimate would have been $19.43 (= $672.11 /

As you might have already guessed, an analyst covering Sonic

Solutions did indeed mistakenly use the wrong share count (34.60

million) in a research report published in June 2010. The initial

report, the analyst discovered the error and issued a revised report

which used the correct share count (51.69 million) but also

concluded that the stock was worth $13 per share. How was this

conclusion supported? The analyst altered the free cash flow

Requirement 9:

It is difficult to discern any large stock price reactions, suggesting

Rovi investors viewed the price as fair. Rovi stock was up 1.0% on

the December 22 announcement date versus 0.3% for the S&P 500.

P6-7. Determining abnormal earnings: Some simple examples

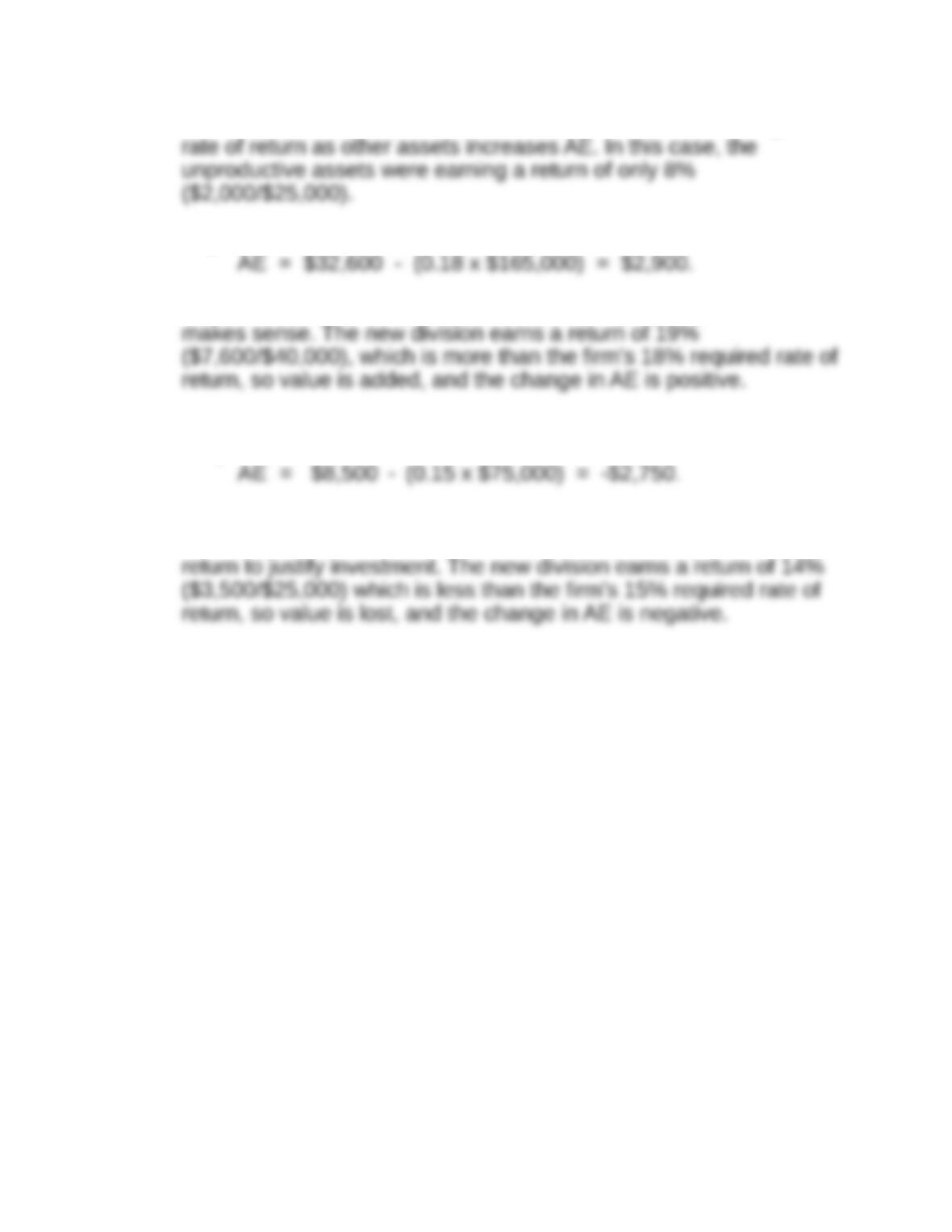

Abnormal earnings (AE) = NOPAT – (r x BVt-1).

Requirement 1:

Requirement 2:

Requirement 3:

NOTE: Higher NOPAT without additional investment (i.e., the same

BVt-1) increases AE.

Requirement 4:

NOTE: Eliminating unproductive assets that do not earn as high a

Requirement 5:

AE increases by $400 (from $2,500 to $2,900). Adding the division

Requirement 6:

AE falls by $250. Adding the new division does not make sense. In

essence, the new division does not earn a high enough rate of