Financial Reporting and Analysis (7th Ed.)

Chapter 8 Solutions

Receivables

Problems

Problems

P8-1. Determining balance sheet presentation and preparing journal

entries for various receivables transactions (LO 8-1, LO 8-4,

LO8-6)

Requirement 1:

Journal entries

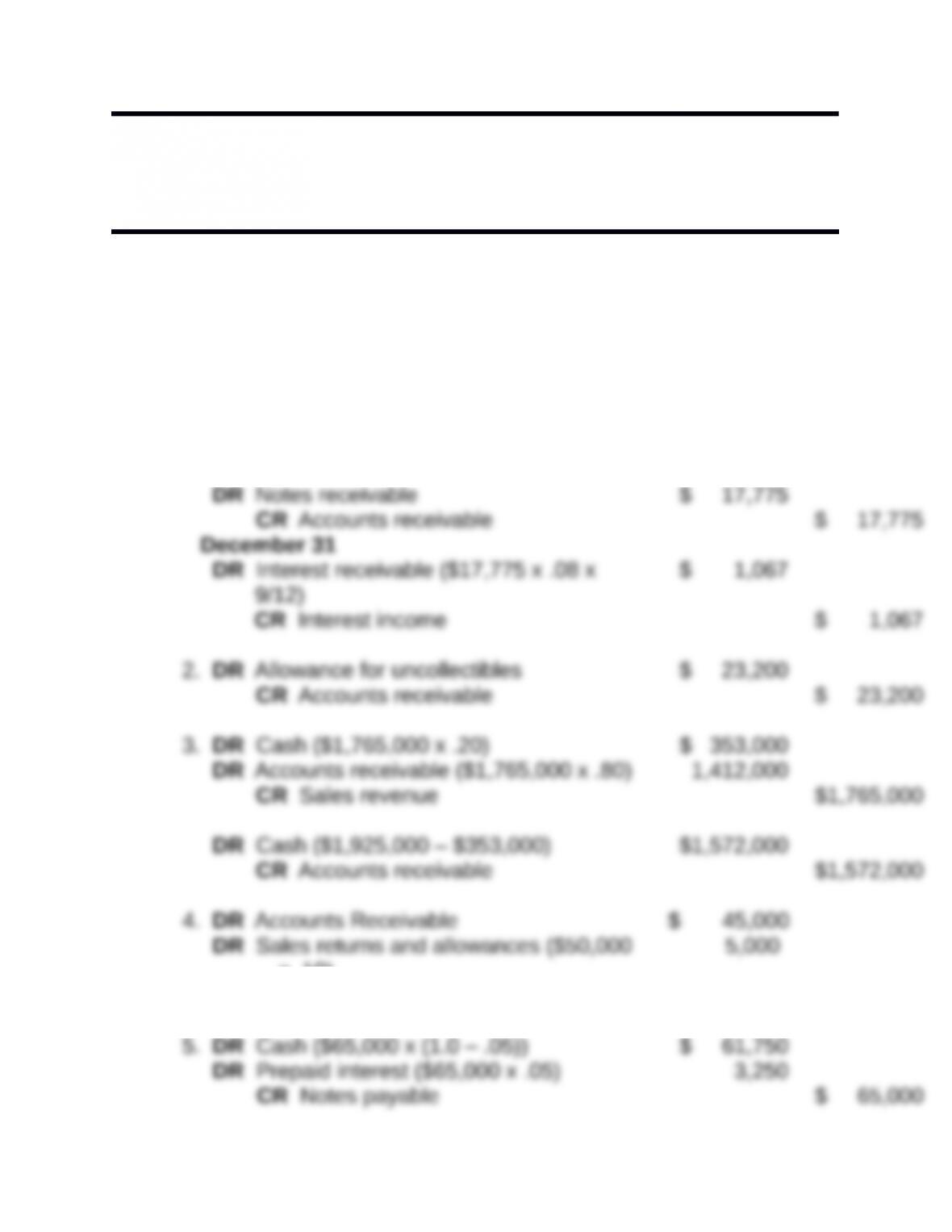

1.

April 1

x .10)

CR Sales $ 50,000

DR Notes payable $ 65,000

CR Cash $ 65,000

DR Interest expense $ 3,250

CR Prepaid interest $ 3,250

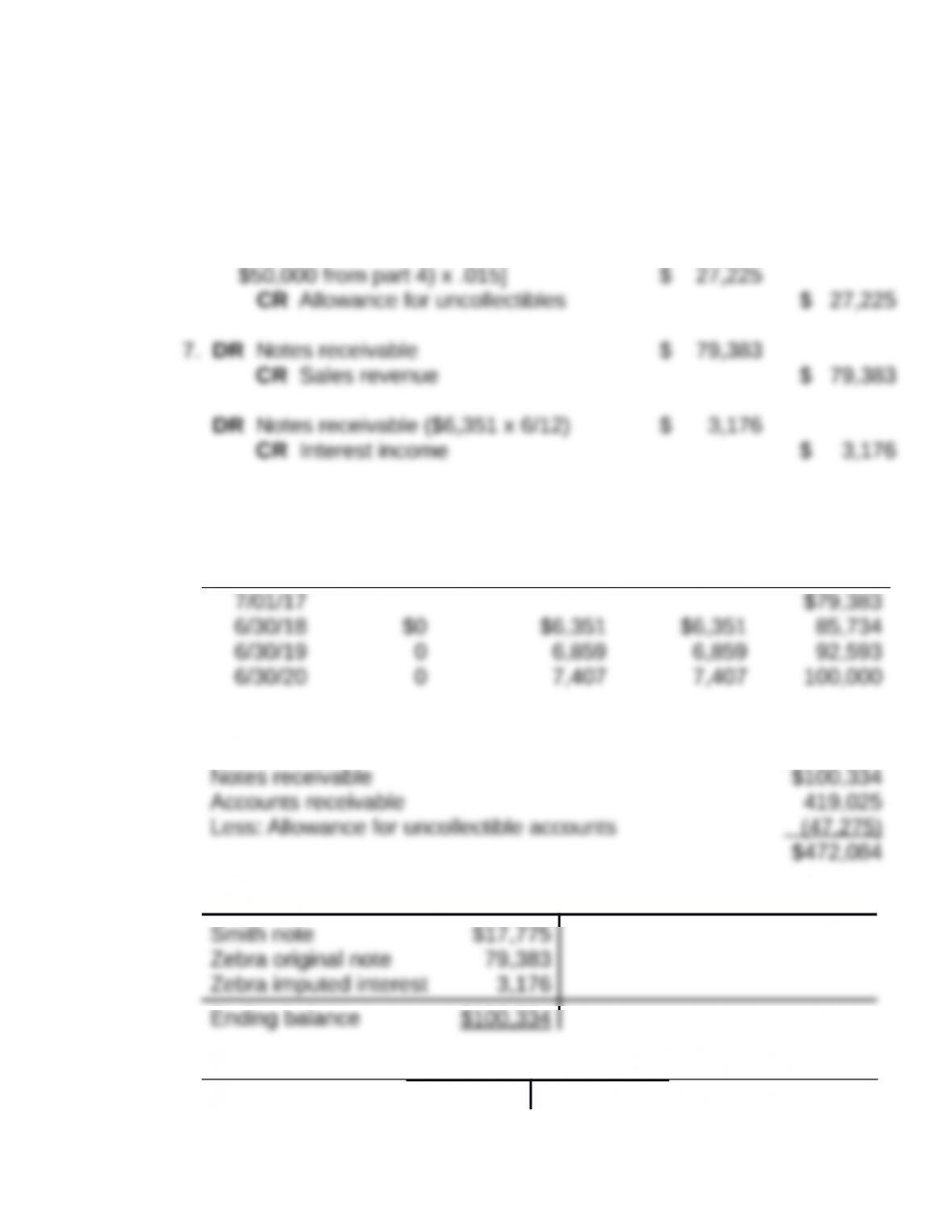

6. DR Bad debt provision [ ($1,765,000 +

Accrued interest over 3-year loan term.

Date

Annual

Payment

Interest

Income (8%)

Receivable

Increase

Receivable

Balance

Requirement 2:

Balance sheet presentation at December 31, 2017

Notes receivable

Accounts receivable

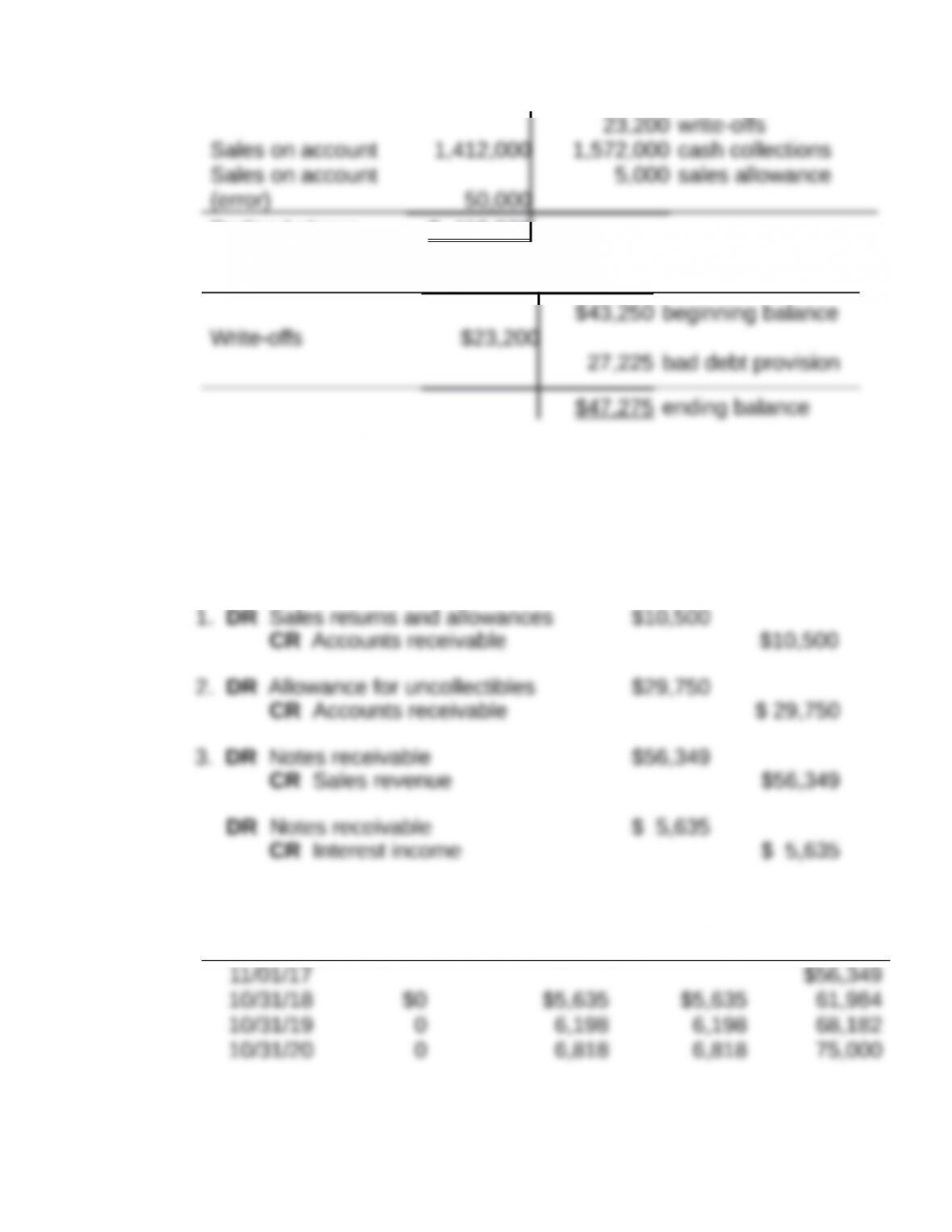

Beginning balance $ 575,000 $ 17,775 exchange for note

Ending balance $ 419 ,025

Allowance for uncollectibles

P8-2. Determining balance sheet presentation and preparing journal

entries for various receivables transactions (LO 8-1, LO 8-4, LO

8-6)

Requirement 1:

Journal entries

Date

Annual

Payment

Interest

Income (10%)

Receivable

Increase

Receivable

Balance

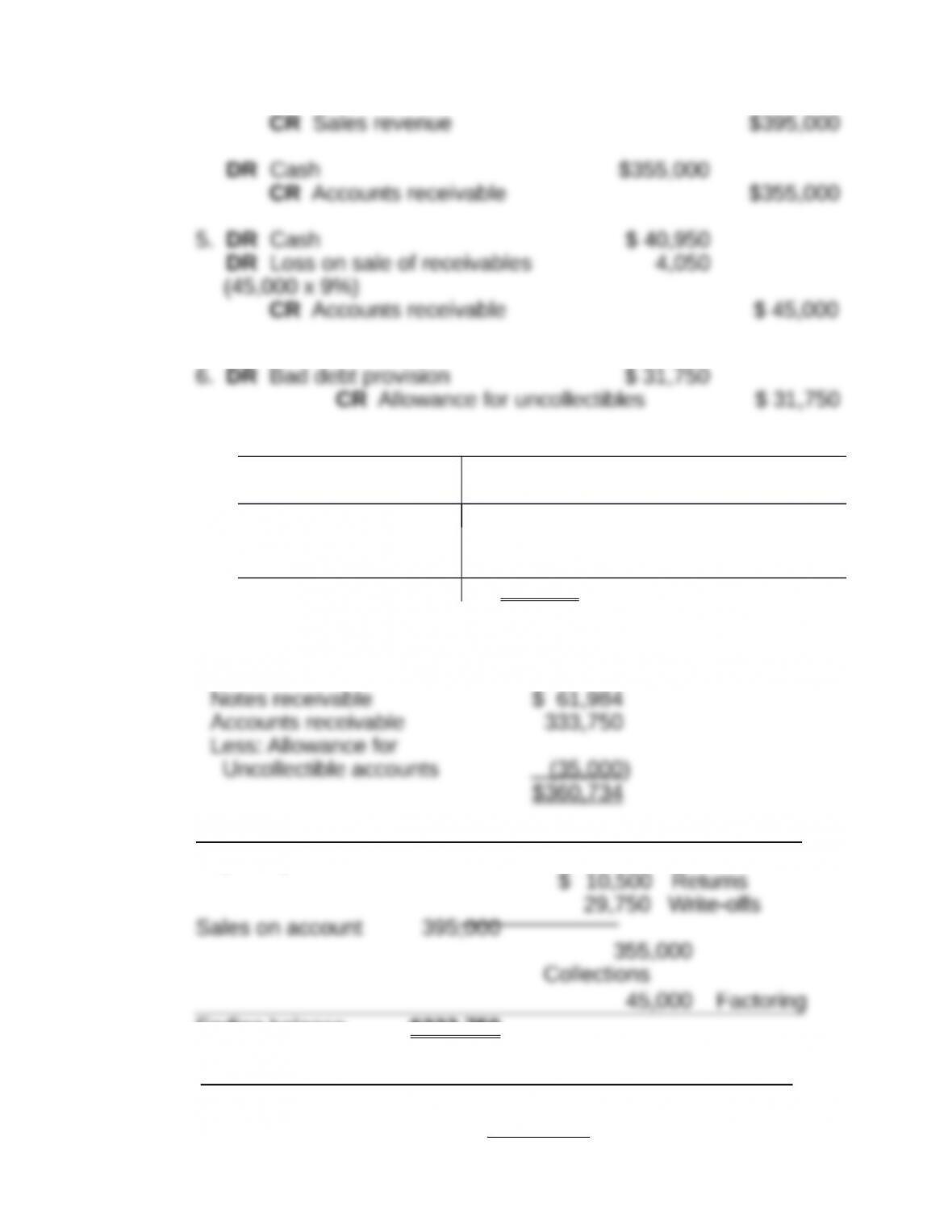

4. DR Accounts receivable $395,000

Allowance for uncollectibles

$33,000 Beginning balance

Write-offs $29,750

3,250

31,750 Required adjustment

(plugged number)

$35 ,000 Required balance

Requirement 2:

Balance sheet presentation at October 31, 2015:

Accounts receivable

Beginning balance $379,000

Ending balance $333,750

Notes receivable

Sale by note $56,349

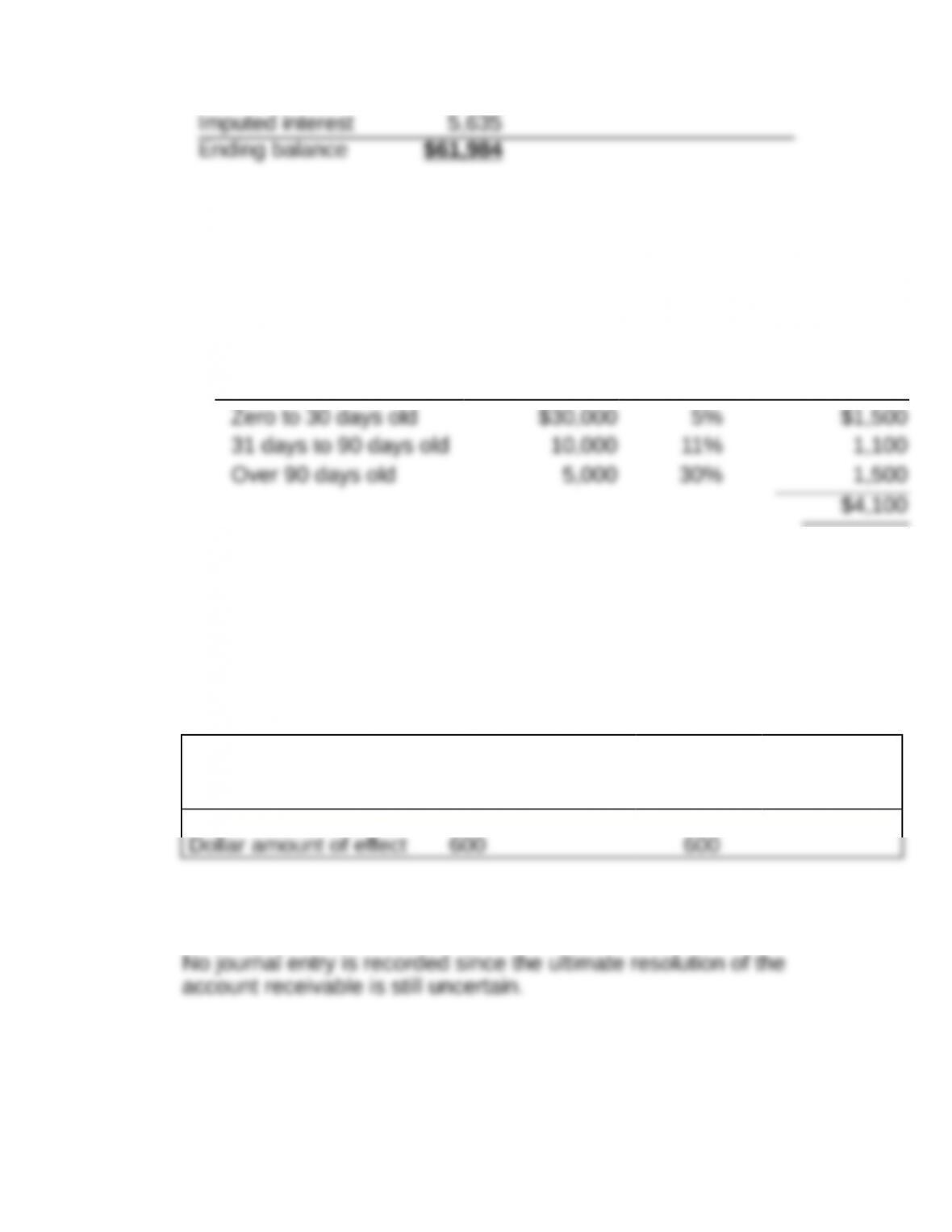

P8-3. Determining allowance for uncollectibles (LO 8-1)

Requirement 1:

Based on the aging schedule, the ending balance in the allowance

for

doubtful accounts is calculated as follows:

Expected Dollar

Age of Receivables

Amount

Bad Debts

Amount

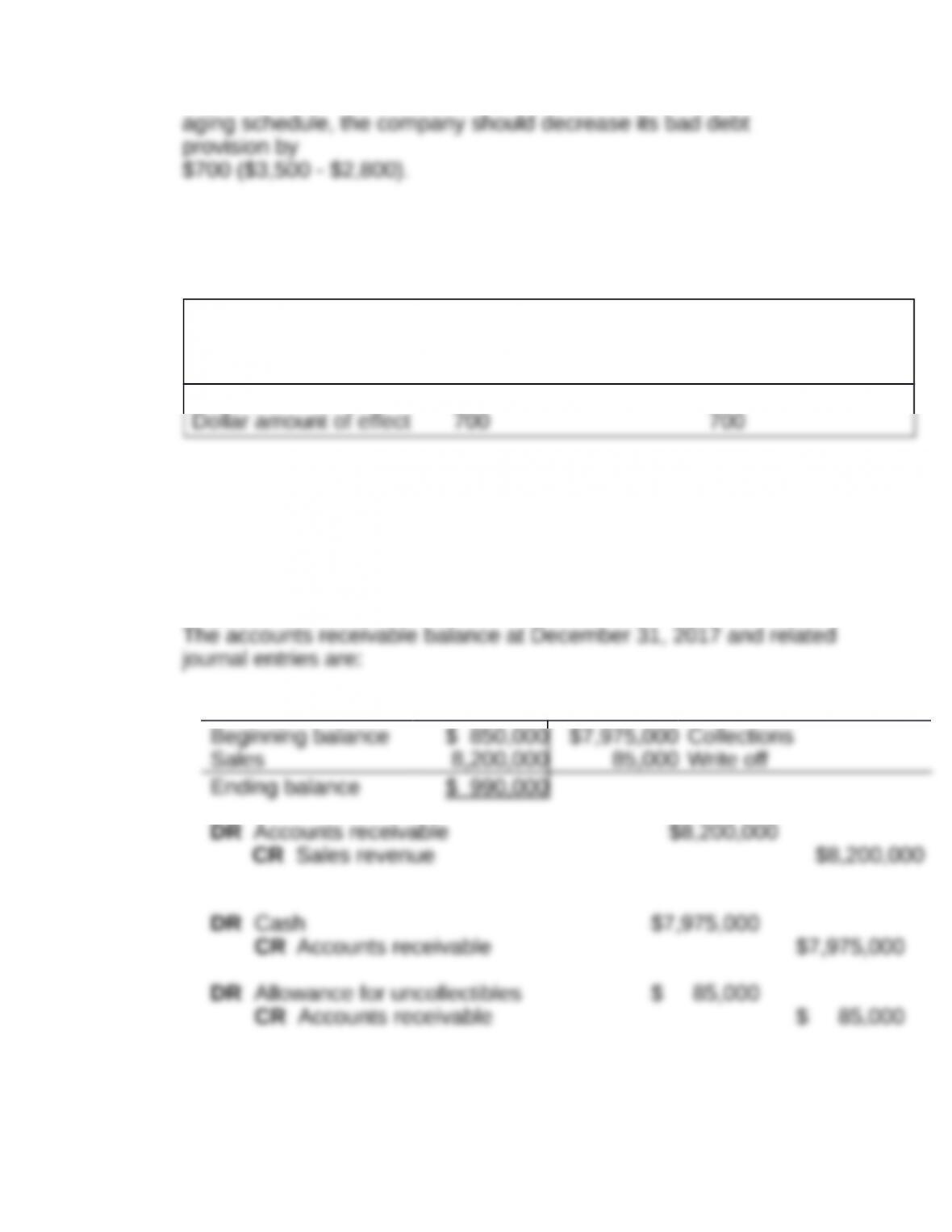

The company needs to record an additional bad debt provision of

$600

($4,100 – $3,500) to increase the allowance balance to $4,100.

December 31, 2017

DR Bad debt provision $600

CR Allowance for uncollectibles

Cash Flow

Net from

Assets Liabilities Income Operations

Direction of effect – NE – NE

The journal entries for the other transactions are provided below:

January 1, 2018

March 1, 2018

DR Allowance for uncollectibles $800

CR Accounts receivable

40% of $2,000 is written-off as uncollectible.

Cash Flow

Net from

Assets Liabilities Income Operations

Direction of effect NE NE NE NE

Dollar amount of effect

May 7, 2018

CR Accounts receivable

$1,200

Cash Flow

Net from

Assets Liabilities Income Operations

Direction of effect NE NE NE +

Dollar amount of effect 1,200

Requirement 2:

Based on the aging schedule, the ending balance in the allowance

for

doubtful accounts is calculated as follows:

Expected

Dollar

Age of Receivables

Amount

Bad Debts

Amount

Since the company has a larger balance than what is required by

the

December 31, 2017

DR Allowance for uncollectibles $700

CR Bad debt provision

Cash Flow

Net From

Assets Liabilities Income Operations

Direction of effect + NE + NE

The other journal entries do not change from Requirement 1.

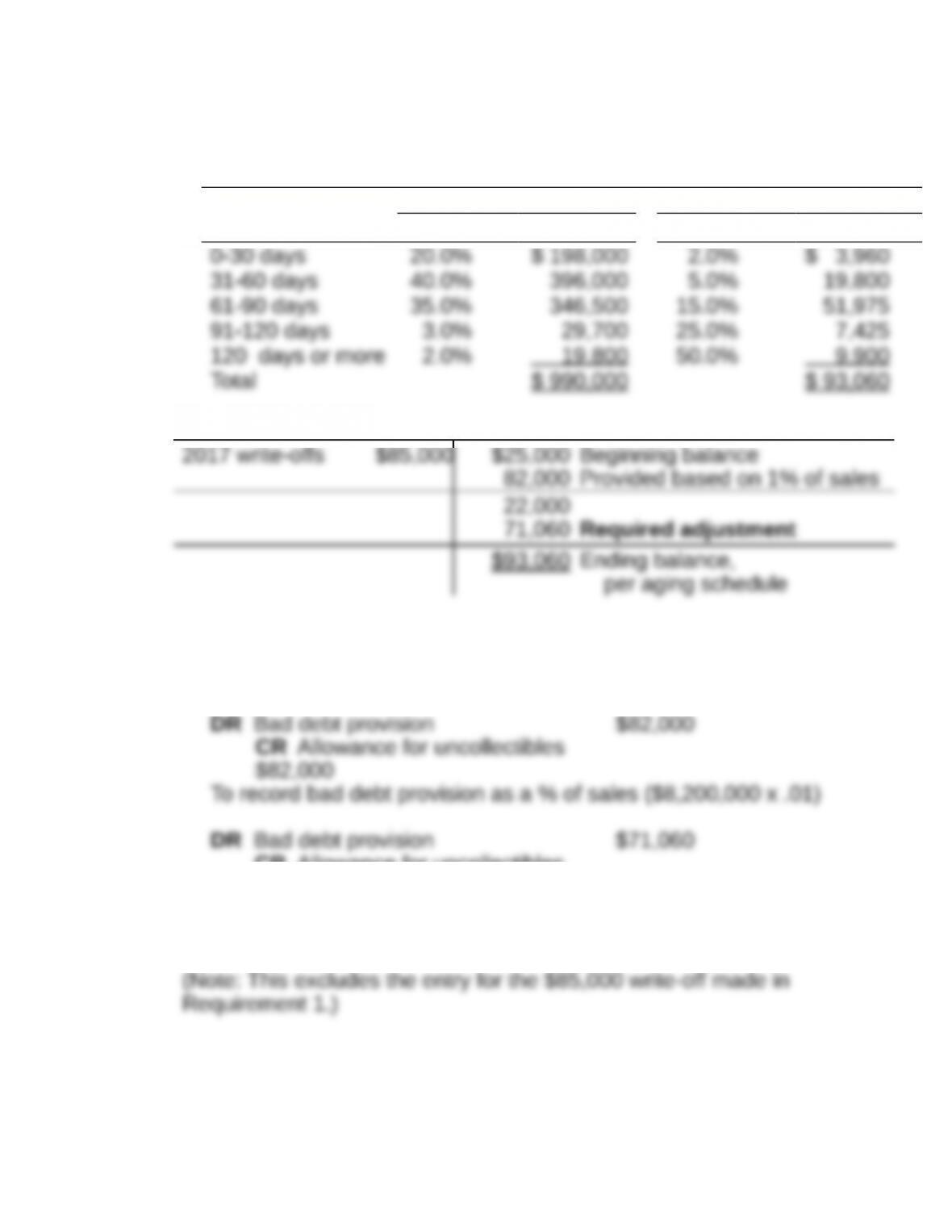

P8-4. Preparing journal entries, aging analysis and balance sheet

presentation (LO 8-1)

Requirement 1:

Accounts receivable

Requirement 2:

Oettinger Corporation

Accounts Receivable Aging Schedule

December 31, 2017

Accounts receivable Uncollectibles

Age Aging % Balance Percentage Amount

Allowance for uncollectibles

Requirement 3:

The journal entries affecting the allowance for uncollectible

accounts are:

CR Allowance for uncollectibles

$71,060

To adjust allowance for uncollectibles to required aging analysis

balance

Requirement 4:

Accounts receivable balance sheet presentation at December 31,

2017:

P8-5. Securitization (LO 8-7)

Requirement 1:

FASB ASC 860-10-40 on the subject of conditions for a sale of

financial assets states that a financial asset should be considered

sold if it is transferred and control is surrendered. Control is

deemed to be surrendered if transferred assets are isolated from

Requirement 2:

Requirement 3:

Assets

Liabilities and shareholders’ equity

securitization.

Requirement 4:

Assets

Liabilities and shareholders’ equity

Notes payable [$50 +

If the securitization did not qualify for “sale accounting,” it would be

treated as a collateralized borrowing, thus Eva’s reported debt

would increase:

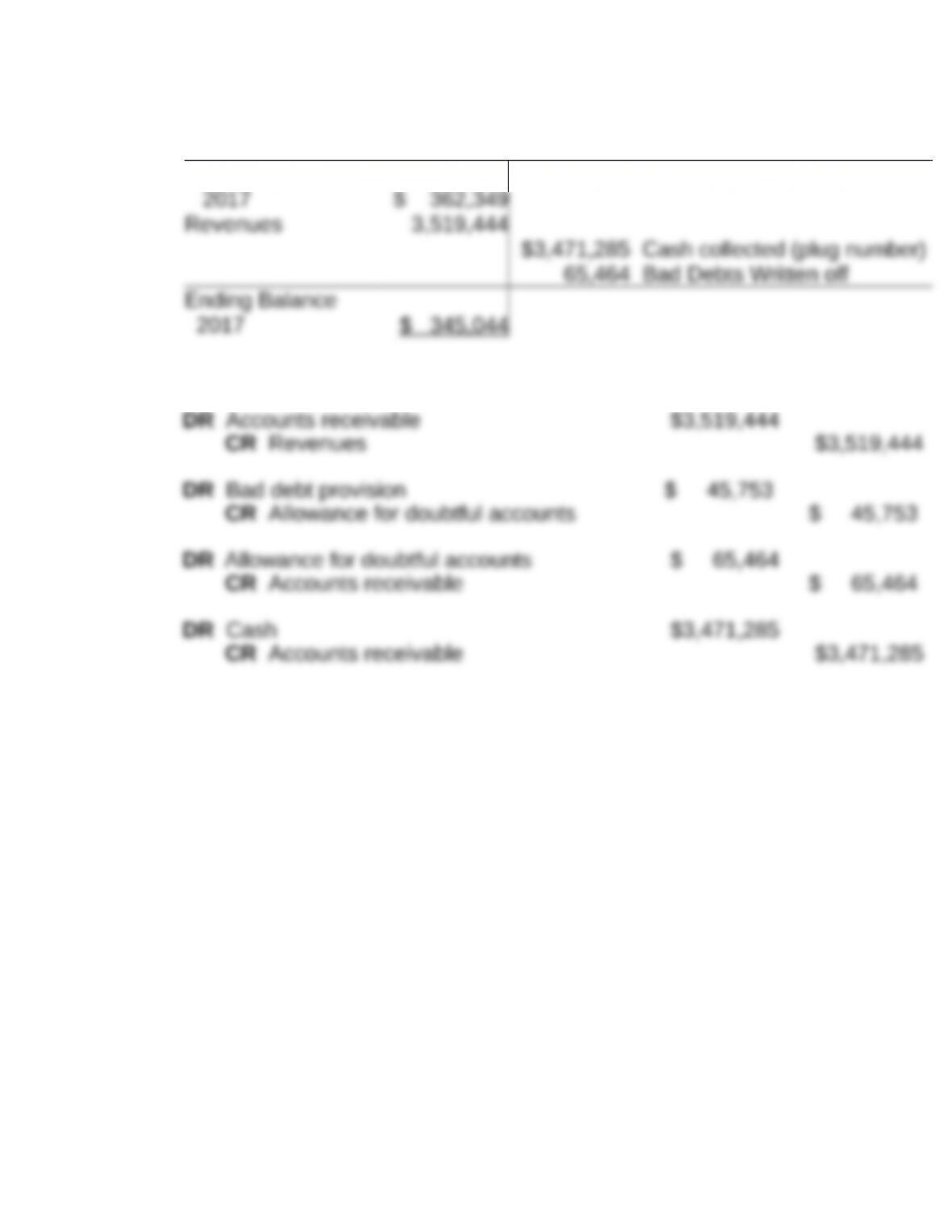

P8-6. Analyzing accounts receivable (LO 8-2)

Allowance for doubtful accounts

Gross accounts receivable

Beginning balance

Journal entries for 2017