Archives

Accounting Chapter 1 Purpose to Provide The Student With Opportunity Evaluate

CHAPTER 1 Financial Accounting and Accounting Standards ASSIGNMENT CLASSIFICATION TABLE (By Topic) Topics Questions Concepts for Analysis 1. Subject matter of accounting. 1 4 2. Environment of accounting. 2, 3, 21 6, 7 3. Role of principles, objectives, standards, and […]

Accounting Chapter 1 Rule 203 The Code Professional Ethics Requires

CA 1.10 (Continued) 4. The public accounting profession, through bodies such as the Accounting Principles Board, made rules which business enterprises and individuals “had” to follow. For many years, these businesses and individuals had little say as to what the […]

Accounting Chapter 1 The purpose of the International Accounting Standards

Financial Accounting and Accounting Standards 1 – 13 55. The Financial Accounting Standards Board (FASB) was proposed by the a. American Institute of Certified Public Accountants. b. Accounting Principles Board. c. Study Group on the Objectives of Financial Statements. d. […]

Accounting Chapter 1 Users of financial accounting statements have

CHAPTER 1 FINANCIAL ACCOUNTING AND ACCOUNTING STANDARDS IFRS questions are available at the end of this chapter. TRUE-FALSE—Conceptual Answer No. Description MULTIPLE CHOICE—Conceptual Answer No. Description a 21. Financial accounting. d 22. Users of financial reports. d 23. Identify the […]

Accounting Chapter 10 A motor in one of North Company’s trucks

Acquisition and Disposition of Property, Plant, and Equipment 10 – 41 126. Colt Football Co. had a player contract with Watts that is recorded in its books at $8,400,000 on July 1, 2020. Day Football Co. had a player contract […]

Accounting Chapter 10 Allocation Land And Building Accounts Proportion Appraised

EXERCISE 10.21 (20–25 minutes) (a) Any addition to plant assets is capitalized because a new asset has been created. This addition increases the service potential of the plant. (b) Expenditures that do not increase the service benefits of the asset […]

Accounting Chapter 10 Discount Notes Payable Cash Depreciation

EXERCISE 10.6 (Continued) 2. Equipment ………………………………………………………. 25,000 Cash ………………………………………………………. 2,000 Note Payable …………………………………………………. 23,000 3. Equipment ………………………………………………………. 19,600 Accounts Payable ($20,000 X .98) ……………………. 19,600 4. Land …………………………………………………………………….. 27,000 Contribution Revenue ………………………….. 27,000 5. Buildings ………………………………………………………. 600,000 Cash ………………………………………………………. 600,000 […]

Accounting Chapter 10 Free Cash Flow The Amount Discretionary Cash

CA 10.3 (Continued) Calculations for avoidable interest are more complex. First, interest can be capitalized only on the weighted-average amount of accumulated expenditures. Although total costs amounted to $5,200,000 for the project, an average of only $3,500,000 was outstanding during […]

Accounting Chapter 10 Other Asset For The Longterm Portion The

PROBLEM 10.8 (Continued) 3. Holyfield Corporation Machinery ……………………………………………………… 95,000f Accumulated Depreciation—Machinery …………… 60,000 Loss on Disposal of Machinery ………………………. 8,000a Machinery …………………………..………………….. 160,000 Cash ………………………………………………………. 3,000 Liston Company Machinery ($95,000f – $3,000) ………………………….. 92,000 Accumulated Depreciation—Machinery …………… 75,000 Cash ……………………………………………………………… […]

Accounting Chapter 10 The building was completed and ready for occupancy

Acquisition and Disposition of Property, Plant, and Equipment 10 – 21 74. On May 1, 2020, Goodman Company began construction of a building. Expenditures of $600,000 were incurred monthly for 5 months beginning on May 1. The building was completed […]

Accounting Chapter 10 The Third Class Expenditures Major Overhauls Usually

CHAPTER 10 Acquisition and Disposition of Property, Plant, and Equipment ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Valuation and classification of land, buildings, and equipment. 1, 2, 3, 4, 6, 7, 13, […]

Accounting Chapter 10 which is greater than specific debt incurred

Acquisition and Disposition of Property, Plant, and Equipment 10 – 53 Solution 10-137 PROBLEMS Pr. 10-138—Capitalizing acquisition costs. Gibbs Manufacturing Co. was incorporated on 1/2/20 but was unable to begin manufacturing activities until 8/1/20 because new factory facilities were not […]

Accounting Chapter 11 A plant asset with a five-year estimated

Depreciation, Impairments, and Depletion 11 – 21 81. Orton Corporation, which has a calendar year accounting period, purchased a new machine for $80,000 on April 1, 2016. At that time Orton expected to use the machine for nine years and […]

Accounting Chapter 11 If an observable input requires an adjustment

CODIFICATION RESEARCH CASE (Continued) 35–38 The availability of relevant inputs and their relative subjectivity might affect the selection of appropriate valuation techniques (see paragraph 820-10–35–24). However, the fair value hierarchy prioritizes the inputs to valuation techniques, not the valuation techniques […]

Accounting Chapter 11 If the interest is allocated between the building

(14,000) $(18,550) = 3,000 = 4,800 = 4,000 $19,800 Truck #3: $30,000/5 X 1/2 Truck #4:$24,000/5 Truck #5: $40,000/5 X 1/2 Total 7 16,400 $79,700 (16,400) $(62,600) $18,000 (21,000) $ 3,000 _______ $104,000 Book value of Truck #3 [$30,000 – […]

Accounting Chapter 11 Management first had to determine whether there

EXERCISE 11.6 (Continued) OR 1st full year (.25 X $212,000) = $53,000 2nd full year [.25 X ($212,000 – $53,000)] = $39,750 2020 Depreciation 3/12 X $53,000 = $13,250 2021 Depreciation 9/12 X $53,000 = $39,750 3/12 X $39,750 = […]

Accounting Chapter 11 Management Might Encouraged Expand Believing That The

CHAPTER 11 Depreciation, Impairments, and Depletion ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Depreciation methods; meaning of depreciation; choice of depreciation methods. 1, 2, 3, 4, 5, 6, 10, 14, 20, 21, […]

Accounting Chapter 11 The Schedule Cash Flow Measures Indicates That

CA 11.2 (Continued) ii. The application of depreciation to the whole group tends to average out or offset errors, economic or operating, caused by under-depreciation or over-depreciation. iii. Periodic income is not distorted by gains or losses on disposal of […]

Accounting Chapter 11 These methods are used for depreciating

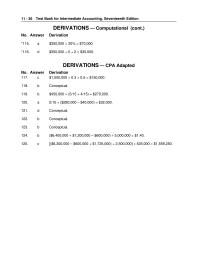

Test Bank for Intermediate Accounting, Seventeenth Edition 11 – 36 DERIVATIONS — Computational (cont.) No. Answer Derivation DERIVATIONS — CPA Adapted No. Answer Derivation 117. c $1,000,000 × 0.3 × 0.5 = $150,000. 118. b Conceptual. 119. b $450,000 × […]

Accounting Chapter 12 Findley Corporation purchased a patent for a new

Intangible Assets 12 – 21 92. ELO Corporation purchased a patent for $135,000 on September 1, 2019. It had a useful life of 10 years. On January 1, 2021, ELO spent $33,000 to successfully defend the patent in a lawsuit. […]

Accounting Chapter 12 It is important that before conducting the goodwill

EXERCISE 12.11 (20–25 minutes) Net assets of Zweifel as reported ($575,000 – $350,000) $225,000 Adjustments to fair value Increase in land value 30,000 Decrease in equipment value (5,000) 25,000 Net assets of Zweifel at fair value 250,000 Selling price 350,000 […]

Accounting Chapter 12 The expected use of the asset by the entity

CHAPTER 12 Intangible Assets ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Intangible assets; concepts, definitions; items comprising intangible assets. 1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12, 13, […]

Accounting Chapter 12 The Term Indefinite Does Not Mean The

Copyright © 2019 WILEY Kieso, Intermediate Accounting, 17/e, Solutions Manual (For Instructor Use Only) 12–39 CA 12.3 (Continued) The high degree of uncertainty about whether research and development expenditures will provide any future benefits, the lack of objectivity in setting […]

Accounting Chapter 12 under IFRS the costs associated with research

Test Bank for Intermediate Accounting, Seventeenth Edition 12 – 40 Solution 12-140 Ex. 12-141 Listed below is a selection of accounts found in the general ledger of Marshall Corporation as of December 31, 2021: Accounts receivable Research & development costs […]

Accounting Chapter 12 Which The Following Not Intangible Asset

CHAPTER 12 INTANGIBLE ASSETS IFRS questions are available at the end of this chapter. TRUE-FALSE—Conceptual Answer No. Description MULTIPLE CHOICE—Conceptual Answer No. Description b 26 Characteristics of intangible assets. c 27 Characteristics of intangible assets. a 28 Characteristics of intangible […]

Accounting Chapter 13 accrue as its share of payroll taxes in its

Current Liabilities and Contingencies 13 – 21 80. An electronics store is running a promotion where for every video game purchased, the customer receives a coupon upon checkout to purchase a second game at a 50% discount. The coupons expire […]

Accounting Chapter 13 Megan Drabek Over Hydraulic Compressor Used Several

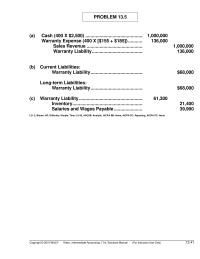

PROBLEM 13.5 (a) Cash (400 X $2,500) ……………………………………………….. 1,000,000 Warranty Expense (400 X [$155 + $185]) ………………….. 136,000 Sales Revenue ………………………………………………. 1,000,000 Warranty Liability …………………………………………… 136,000 (b) Current Liabilities: Warranty Liability …………………………………………… $68,000 Long-term Liabilities: Warranty Liability …………………………………………… $68,000 (c) […]

Accounting Chapter 13 Nolte should record interest expense for 2021

Current Liabilities and Contingencies 13 – 38 b. $15,020. c. $10,220. d. $8,540. 142. Yurman Co. sells major household appliance service contracts for cash. The service contracts are for a one-year, two-year, or three-year period. Cash receipts from contracts are […]

Accounting Chapter 13 Once Have Negotiated The Contracts The Bottlers

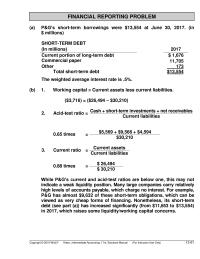

Copyright © 2019 WILEY Kieso, Intermediate Accounting, 17/e, Solutions Manual (For Instructor Use Only) 13–61 FINANCIAL REPORTING PROBLEM (a) P&G’s short-term borrowings were $13,554 at June 30, 2017. (in $ millions) SHORT-TERM DEBT (In millions) 2017 Current portion of long-term […]

Accounting Chapter 13 Unearned revenue is a liability that arises from

CHAPTER 13 Current Liabilities and Contingencies ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Concept of liabilities; definition and classification of current liabilities. 1, 2, 3, 4, 6, 8, 31 1, 16 1, […]

Accounting Chapter 13 Yes The Debt Should Included Current Liabilities

CE13.1 Master Glossary (a) An asset retirement is an obligation associated with the retirement of a tangible long-lived asset. (b) Current liabilities is used principally to designate obligations whose liquidation is reasonably expected to require the use of existing resources […]

Accounting Chapter 13 when some amount within the range of expected

EXERCISE 13.6 (10–15 minutes) Salaries and Wages Expense ………………………………….. 480,000 Withholding Taxes Payable …………………………….. 80,000 FICA Taxes Payable* ………………………………………. 29,900 Union Dues Payable ……………………………………….. 9,000 Cash ……………………………………………………………… 361,100 *[($480,000 – $110,000) X 7.65% = $28,305 $110,000 X 1.45% = $1,595; […]

Accounting Chapter 14 Compute the gain or loss to Mann on the transfer

Long-Term Liabilities 14 – 21 a. $108,000. b. $184,000. c. $92,000. d. $100,000. Ans: C, LO: 1, Bloom: AP, Difficulty: Moderate, Min: 3, AACSB: Analytic, AICPA BB: None, AICPA FN: Measurement, AICPA PC: Problem Solving, IMA: Reporting, IFRS: None Test […]

Accounting Chapter 14 Entries for redemption and issuance of bonds

CHAPTER 14 Long-Term Liabilities ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Long-term liability; classification; definitions. 1, 14 1, 2 10, 11 1, 2 2. Issuance of bonds; types of bonds. 2, 3, […]

Accounting Chapter 14 Fallen’s creditworthiness has improved during

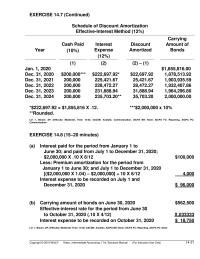

EXERCISE 14.7 (Continued) Schedule of Discount Amortization Effective-Interest Method (12%) Year Cash Paid (10%) Interest Expense (12%) Discount Amortized Carrying Amount of Bonds (1) (2) (2) – (1) Jan. 1, 2020 $1,855,816.00 Dec. 31, 2020 $200,000*** $222,697.92 * $22,697.92 1,878,513.92 […]

Accounting Chapter 14 One method of amortization is the straight-line

PROBLEM 14.9 12/31/19 (a) Machinery ………………………………………………………. 182,485.20 Discount on Notes Payable ………………………….. 27,514.80 Cash ………………………………………………………. 50,000.00 Notes Payable ………………………….. 160,000.00 [To record machinery at the present value of the note plus the immediate cash payment: PV of $40,000 annuity @ […]

Accounting Chapter 14 That Presumption However Must Not Permit The

FINANCIAL REPORTING PROBLEM (Continued) Inventory turnover = Cost of goods sold Average inventory = $32,535 $4,624 + $4,716 2 = 6.97 times (6.79 in 2016) Current cash debt coverage = Net cash provided by operating activities Average current liabilities = […]

Accounting Chapter 14 The Loss Reported Ordinary Loss Note Loss

Copyright © 2019 WILEY Kieso, Intermediate Accounting, 17/e, Solutions Manual (For Instructor Use Only) 14–41 *EXERCISE 14.27 (Continued) December 31, 2021 (see schedule) Cash ……………………………………………………………………… 11,000 Allowance for Doubtful Accounts ………………………….. 12,277 Interest Revenue ……………………………………………. 23,277 December 31, 2022 (see […]

Accounting Chapter 15 Assume common stock is the only class of stock

CHAPTER 15 STOCKHOLDERS’ EQUITY IFRS questions are available at the end of this chapter. TRUE-FALSE—Conceptual Answer No. Description MULTIPLE CHOICE—Conceptual Answer No. Description c 21. Nature of stockholders’ interest. b 22. Preemptive right. a 23. Preemptive right. b S24. Definition […]

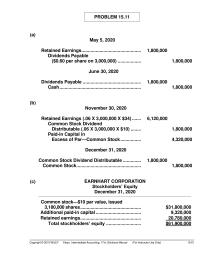

Accounting Chapter 15 Generally Investments Owners Cause Increase Assets Addition

PROBLEM 15.11 (a) May 5, 2020 Retained Earnings ………………………………………. 1,800,000 Dividends Payable ($0.60 per share on 3,000,000) ……………… 1,800,000 June 30, 2020 Dividends Payable ……………………………………… 1,800,000 Cash ……………………………………………………… 1,800,000 (b) November 30, 2020 Retained Earnings (.06 X 3,000,000 X $34) […]

Accounting Chapter 15 How would the declaration and subsequent issuance

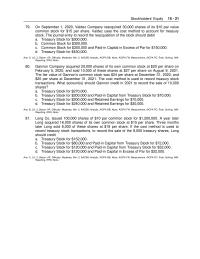

Stockholders’ Equity 15 – 21 79. On September 1, 2020, Valdez Company reacquired 30,000 shares of its $10 par value common stock for $15 per share. Valdez uses the cost method to account for treasury stock. The journal entry to […]

Accounting Chapter 15 including a note to the financial statements setting

Time and Purpose of Problems (Continued) Problem 15.10 (Time 35–45 minutes) Purpose—to provide the student with an understanding of the differences between a stock dividend and a stock split. Acting as a financial advisor to the Board of Directors, the […]

Accounting Chapter 15 Major differences relate to terminology used

Stockholders’ Equity 15 – 39 DERIVATIONS — Computational (cont.) No. Answer Derivation 88. a 15,000 $100 .04 = $60,000 ($110,000 2) – ($60,000 3) = $40,000. 89. a 12,000 $100 .05 = $60,000 $230,000 […]

Accounting Chapter 15 No entry simply a memorandum note indicating

EXERCISE 15.5 (10–15 minutes) (a) Fair Value of Common (500 X $165) $ 82,500 Fair Value of Preferred (100 X $230) 23,000 $105,500 Allocated to Common: $82,500/$105,500 X $100,000 $ 78,199 Allocated to Preferred: $23,000/$105,500 X $100,000 21,801 Total allocation […]

Accounting Chapter 15 One measure of solvency is the ratio of debt

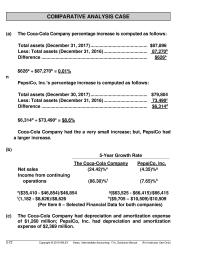

COMPARATIVE ANALYSIS CASE (Continued) During 2017, PepsiCo earned a higher return on its stockholders’ equity. (g) Payout ratios for 2017. Coca-Cola, $5,350 = 75.37% $7,098 PepsiCo, $3,730 = 62.74% $5,946 – $1 LO: 4, Bloom: AN, Difficulty: Moderate, Time: 20-25, […]

Accounting Chapter 15 Preferred stock commonly has preference to dividends

CHAPTER 15 Stockholders’ Equity ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Stockholders’ rights; corporate form. 1, 2, 3 1 2. Stockholders’ equity. 4, 5, 6, 16 3 7, 9, 10, 16, 17, […]

Accounting Chapter 16 A reconciliation of the numerators and the denominators

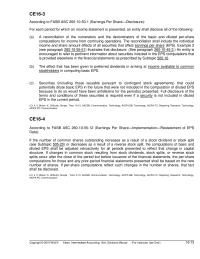

CE16-3 According to FASB ASC 260-10–50-1 (Earnings Per Share—Disclosure): For each period for which an income statement is presented, an entity shall disclose all of the following: (a) A reconciliation of the numerators and the denominators of the basic and […]

Accounting Chapter 16 Accumulated Depreciation Equipment John Wiley Amp

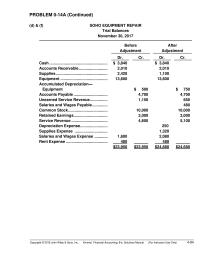

PROBLEM 0-14A (Continued) (d) & (f) SOHO EQUIPMENT REPAIR Trial Balances November 30, 2017 Before Adjustment After Adjustment Dr. Cr. Dr. Cr. Accumulated Depreciation— Equipment Accounts Payable …………………………. Unearned Service Revenue ……………. Salaries and Wages Payable ………….. Common Stock ……………………………… […]

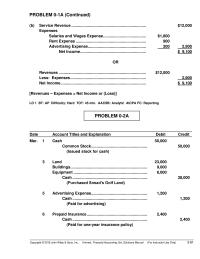

Accounting Chapter 16 Assets, Dividends, and Expenses have debit balances

PROBLEM 0-1A (Continued) (b) Service Revenue ………………………………………………………….. $12,000 Expenses Salaries and Wages Expense ………………………………… $1,800 Rent Expense ………………………………………………………. 900 Advertising Expense …………………………………………….. 200 2,900 Net Income …………………………………………………… $ 9,100 OR Revenues ……………………………………………………………………. $12,000 Less: Expenses …………………………………………………………… 2,900 Net Income …………………………………………………………………… […]

Accounting Chapter 16 Capital Structure Cumulative Preferred Stock 100 Par

Test Bank for Intermediate Accounting, Seventeenth Edition 16 – 52 Solution 16-142 *Ex. 16-143—Stock appreciation rights. On January 1, 2020, Orr Co. established a stock appreciation rights plan for its executives. They could receive cash at any time during the […]

Accounting Chapter 16 Cash received with respect to fees and dues

PROBLEM 0-8A (Continued) (d) PAMPER ME SALON INC. Trial Balance May 31, 2017 Debit Credit Unearned service revenue ……………………………………….. Common stock ……………………………………………………….. Retained earnings …………………………………………………… Service revenue ………………………………………………………. Salaries and wages expense ……………………………………. Rent expense ………………………………………………………….. Supplies expense ……………………………………………………. Advertising […]

Accounting Chapter 16 Houser Company granted some of its executives

Dilutive Securities and Earnings per Share 16 – 21 67. On January 1, 2021, Ritter Company granted stock options to officers and key employees for the purchase of 20,000 shares of the company’s $1 par common stock at $20 per […]

Accounting Chapter 16 Income tax laws impose no restrictions on the exercise

CA 16.3 (Continued) 3. Income tax laws impose no restrictions on the exercise price of warrants issued to purchasers of a company’s bonds. The exercise price may be above, equal to, or below the current market price of the company’s […]

Accounting Chapter 16 Increase in assets and increase in liabilities

CHAPTER 0 Accounting Cycle Review SOLUTIONS TO BRIEF EXERCISES BRIEF EXERCISE 0-1 Assets Liabilities Stockholders’ Equity (b) (c) + – NE NE + – LO 1 BT: C Difficulty: Easy TOT: 2 min. AACSB: None AICPA FC: Reporting (a) + […]

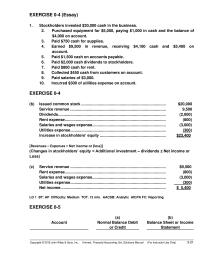

Accounting Chapter 16 Maintenance and Repairs Expense Accounts Payable

EXERCISE 0-4 (Essay) 1. Stockholders invested $20,000 cash in the business. 2. Purchased equipment for $5,000, paying $1,000 in cash and the balance of $4,000 on account. 3. Paid $750 cash for supplies. 4. Earned $9,500 in revenue, receiving $4,100 […]

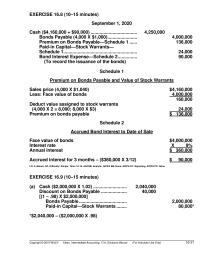

Accounting Chapter 16 Premium on Bonds Payable and Value of Stock

EXERCISE 16.8 (10–15 minutes) September 1, 2020 Cash ($4,160,000 + $90,000) ……………………………… 4,250,000 Bonds Payable (4,000 X $1,000) ………………….. 4,000,000 Premium on Bonds Payable—Schedule 1 …… 136,000 Paid-in Capital—Stock Warrants— Schedule 1 ………………………………………………… 24,000 Bond Interest Expense—Schedule 2 …………… 90,000 […]

Accounting Chapter 16 Stockholders Equity And Expenses The Opposite

EXERCISE 0-21 (a) Revenue recognition principle. (b) Periodicity assumption. (c) No violation. (d) Going concern assumption. (e) Historical cost principle. (f) Economic entity assumption. LO 5 BT: C Difficulty: Medium TOT: 10 min. AACSB: None AICPA FC: Reporting EXERCISE 0-22 […]

Accounting Chapter 16 The Holders These Securities Can Expect Participate

CHAPTER 16 Dilutive Securities and Earnings Per Share ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Convertible debt and preferred stock. 1, 2, 3, 4, 5, 6, 7 1, 2, 3 1, 2, […]

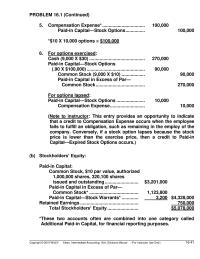

Accounting Chapter 16 This entry provides an opportunity to indicate that

PROBLEM 16.1 (Continued) 5. Compensation Expense* …………………………… 100,000 Paid-in Capital—Stock Options …………… 100,000 *$10 X 10,000 options = $100,000 6. For options exercised: Cash (9,000 X $30) ……………………………………. 270,000 Paid-in Capital—Stock Options (.90 X $100,000) ……………………………………… 90,000 Common Stock (9,000 […]

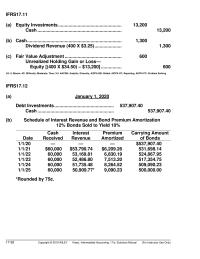

Accounting Chapter 17 Continued Classification Financial Liabilities And Equity

IFRS17.11 (a) Equity Investments …………………………………………. 13,200 Cash ……………………………………………………….. 13,200 (b) Cash ………………………………………………………………. 1,300 Dividend Revenue (400 X $3.25) ………………… 1,300 (c) Fair Value Adjustment …………………………………….. 600 Unrealized Holding Gain or Loss— Equity [(400 X $34.50) – $13,200] ……………. 600 LO: […]

Accounting Chapter 17 Investments in debt securities should be recorded

CHAPTER 17 INVESTMENTS IFRS questions are available at the end of this chapter. TRUE-FALSE—Conceptual Answer No. Description T *20. Disclosure of fair value information. MULTIPLE CHOICE—Conceptual Answer No. Description c 21. Debt securities. b 22. Valuation of debt securities. c […]

Accounting Chapter 17 Journal entries for fair value and equity

CHAPTER 17 Investments ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Debt securities. 1, 2, 3, 13 1 6 (a) Held-to-maturity. 4, 5, 7, 8, 10, 13, 21 1, 3 2, 3, 5 […]

Accounting Chapter 17 No entry necessary at the date of the swap

Copyright © 2019 WILEY Kieso, Intermediate Accounting, 17/e, Solutions Manual (For Instructor Use Only) 17–61 *PROBLEM 17.14 (a) January 7, 2020 Put Option ……………………………………………………… 360 Cash ………………………………………………………… 360 (b) March 31, 2020 Put Option ……………………………………………………… 2,000 Unrealized Holding Gain or […]

Accounting Chapter 17 Patel transferred its investment in security

Investments 17 – 21 76. On November 1, 2021, Horton Company purchased Lopez, Inc., 10-year, 9%, bonds with a face value of $800,000, for $720,000. An additional $24,000 was paid for the accrued interest. Interest is payable semiannually on January […]

Accounting Chapter 17 Similarly Amounts Recognized Accrued Receivables Shall Not

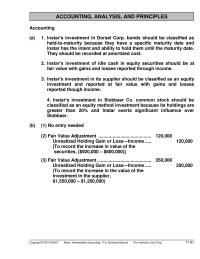

Copyright © 2019 WILEY Kieso, Intermediate Accounting, 17/e, Solutions Manual (For Instructor Use Only) 17–81 ACCOUNTING, ANALYSIS, AND PRINCIPLES Accounting (a) 1. Instar’s investment in Dorsel Corp. bonds should be classified as held-to-maturity because they have a specific maturity date […]

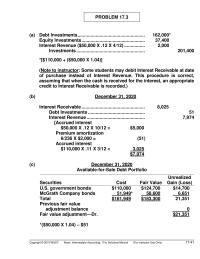

Accounting Chapter 17 Some students may debit Interest Receivable at date

PROBLEM 17.3 (a) Debt Investments ……………………………………………. 162,000* Equity Investments …………………………………………. 37,400 Interest Revenue ($50,000 X .12 X 4/12) ……………. 2,000 Investments …………………………………………….. 201,400 *[$110,000 + ($50,000 X 1.04)] (Note to instructor: Some students may debit Interest Receivable at date of […]

Accounting Chapter 17 The basis for consolidation under IFRS is control

Test Bank for Intermediate Accounting, Seventeenth Edition 17 – 36 Solution 17-117 BE. 17-118—Investments in debt securities. Presented below are unrelated cases involving investments in debt securities. Case I. The fair value of the trading securities at the end of […]

Accounting Chapter 17 Amount reclassified from accumulated other

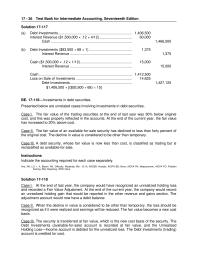

EXERCISE 17.10 (20–25 minutes) (a) STEFFI GRAF, INC. Statement of Comprehensive Income For the Year Ended December 31, 2020 _____________________________________________________________ Net income $120,000 Other comprehensive income Unrealized holding gain 1,100 Comprehensive income $121,100 (b) STEFFI GRAF, INC. Statement of Comprehensive […]

Accounting Chapter 18 At that time the total costs of construction

Revenue Recognition 18 – 21 92. Bella Pool Company sells prefabricated pools that cost $80,000 to customers for $144,000. The sales price includes an installation fee, which is valued at $20,000. The fair value of the pool is $128,000. The […]

Accounting Chapter 18 Celic recognizes warranty expenses associated

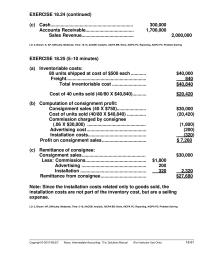

EXERCISE 18.24 (continued) (c) Cash…………………………….…………………………. 300,000 Accounts Receivable.………………………………. 1,700,000 Sales Revenue..………………………….…….. 2,000,000 LO: 3, Bloom: K, AP, Difficulty: Moderate, Time: 10-15, AACSB: Analytic, AICPA BB: None, AICPA FC: Reporting, AICPA PC: Problem Solving EXERCISE 18.25 (5–10 minutes) (a) Inventoriable costs: […]

Accounting Chapter 18 Make the journal entry to record the income

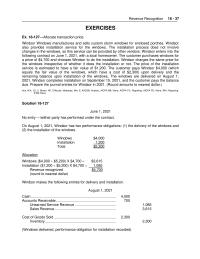

Revenue Recognition 18 – 37 EXERCISES Ex. 18-127—Allocate transaction price. Windsor Windows manufactures and sells custom storm windows for enclosed porches. Windsor also provides installation service for the windows. The installation process does not involve changes in the windows, so […]

Accounting Chapter 18 Progress billings would be accounted for by

*CA 18.9 (a) Widjaja Company should recognize revenue as it performs the work on the contract (the percentage-of-completion method) because it meets the criteria for revenue recognition over time. (b) Progress billings would be accounted for by increasing accounts receivable […]

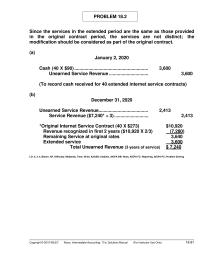

Accounting Chapter 18 Since the services in the extended period

Since the services in the extended period are the same as those provided in the original contract period, the services are not distinct; the modification should be considered as part of the original contract. (a) January 2, 2020 Cash (40 […]

Accounting Chapter 18 The fourth step in the process for revenue

CHAPTER 18 REVENUE RECOGNITION TRUE-FALSE—Conceptual Answer No. Description MULTIPLE CHOICE—Conceptual Answer No. Description d 26. Comprehensive revenue recognition model. c 27. Revenue recognition standard. b 28. First step in revenue recognition process. d 29. Revenue recognition process steps. a 30. […]

Accounting Chapter 18 The Seller Cannot Have The Ability Use

CHAPTER 18 Revenue Recognition ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Current Environment; 5-Step Model. 1, 2, 3, 4, 5, 6 8 1, 2, 3 2. Contracts. 7 1, 2, 3, 4 […]

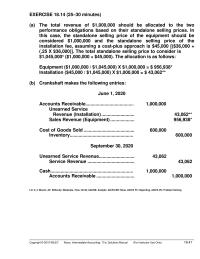

Accounting Chapter 18 The separate performance obligations are the oven

EXERCISE 18.14 (25–30 minutes) (a) The total revenue of $1,000,000 should be allocated to the two performance obligations based on their standalone selling prices. In this case, the standalone selling price of the equipment should be considered $1,000,000 and the […]

Accounting Chapter 18 therefore the task would not need to be

PROBLEM 18.11 (Continued) 2022 Costs to date (12/31/22)……………………..………….. $2,100,000 Estimated costs to complete …………………………. 0 2,100,000 Contract price ………..…………………………………….. 1,900,000 Total loss………..……………………..…………………….. $ 200,000 Total loss………………………………………………….….. Less: Loss recognized in 2021 ……………………… $180,000 $ 200,000 Gross profit recognized in 2020…….……… […]

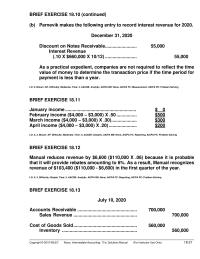

Accounting Chapter 18 This Statement True One The Difficulties The

BRIEF EXERCISE 18.10 (continued) (b) Parnevik makes the following entry to record interest revenue for 2020. December 31, 2020 Discount on Notes Receivable……………………. 55,000 Interest Revenue (.10 X $660,000 X 10/12) ……………………. 55,000 As a practical expedient, companies are not […]

Accounting Chapter 19 Corporation Reported The Following Results For Its

Accounting for Income Taxes 19 – 21 68. Ewing Company sells household furniture. Customers who purchase furniture on the installment basis make payments in equal monthly installments over a two-year period, with no down payment required. Ewing’s gross profit on […]

Accounting Chapter 19 larger of the beginning balances of the projected

CHAPTER 19 ACCOUNTING FOR INCOME TAXES IFRS questions are available at the end of this chapter. TRUE-FALSE—Conceptual Answer No. Description MULTIPLE CHOICE—Conceptual Answer No. Description b 21. Differences between taxable and accounting income. c 22. Differences between taxable and accounting […]

Accounting Chapter 19 Pretax Financial Income Nondeductible Expense Subtotal Taxable

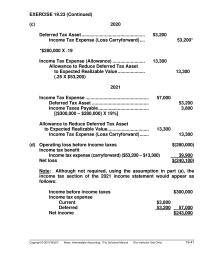

EXERCISE 19.23 (Continued) (c) 2020 Deferred Tax Asset …………………………………………. 53,200 Income Tax Expense (Loss Carryforward) …. 53,200* *$280,000 X .19 Income Tax Expense (Allowance) ……………………. 13,300 Allowance to Reduce Deferred Tax Asset to Expected Realizable Value ………………… 13,300 (.25 X […]

Accounting Chapter 19 Rents Are Taxed The Year They Are

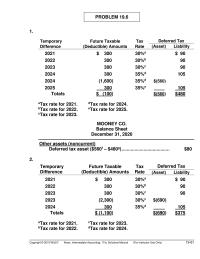

PROBLEM 19.6 1. Temporary Difference Future Taxable (Deductible) Amounts Tax Rate Deferred Tax (Asset) Liability 2021 $ 300 30%a $ 90 2022 300 30%b 90 2023 300 30%c 90 2024 300 35%d 105 2024 (1,600) 35%d $(560) 2025 300 35%e […]

Accounting Chapter 19 Significant Expenses Implement Tax planning Strategy Any Significant

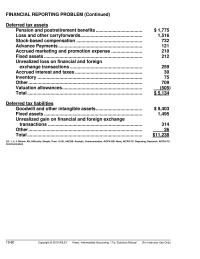

FINANCIAL REPORTING PROBLEM (Continued) Deferred tax assets Pension and postretirement benefits ……………………………… $ 1,775 Loss and other carryforwards………………………………………… 1,516 Stock-based compensation …………………………………………… 732 Advance Payments ……………………………………………………….. 121 Accrued marketing and promotion expense …………………… 210 Fixed assets …………………………………………………………………. 212 Unrealized loss […]

Accounting Chapter 19 Such Positions Give Rise Tax Benefits Either

CHAPTER 19 Accounting for Income Taxes ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Reconcile pretax financial income with taxable income. 1, 14 1, 2, 3, 4, 5, 10, 16, 18, 19 1, […]

Accounting Chapter 19 Temporary Difference Installment Sales Warranty Costs Totals

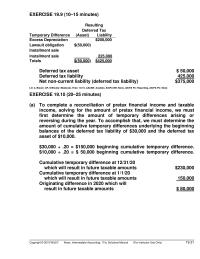

EXERCISE 19.9 (10–15 minutes) Resulting Deferred Tax Temporary Difference (Asset) Liability Excess Depreciation $200,000 Lawsuit obligation $(50,000) Installment sale Installment sale 225,000 Totals $(50,000) $425,000 Deferred tax asset $ 50,000 Deferred tax liability 425,000 Net non-current liability (deferred tax liability) […]

Accounting Chapter 19 When a change in the tax rate is enacted

Accounting for Income Taxes 19 – 37 BRIEF EXERCISES BE. 19–105—Computation of taxable income. The records for Bosch Co. show this data for 2021: • Gross profit on installment sales recorded on the books was $480,000. Gross profit from collections […]

Accounting Chapter 2 Comprehensive Income Defined The Change Equity Net

COMPARATIVE ANALYSIS CASE (Continued) (d) Change in accounting policy Coke Recently Issued Accounting Guidance for Revenue In May 2014, the Financial Accounting Standards Board (“FASB”) issued Accounting Standards Update (“ASU”) 2014-09, Revenue from Contracts with Customers, which will replace most […]

Accounting Chapter 2 Conceptual Framework Underlying Financial Accounting

CHAPTER 2 CONCEPTUAL FRAMEWORK FOR FINANCIAL REPORTING IFRS questions are available at the end of this chapter. TRUE-FALSE—Conceptual Answer No. Description MULTIPLE CHOICE—Conceptual Answer No. Description c 21. GAAP defined. d 22. Purpose of conceptual framework. c 23. Conceptual framework. […]

Accounting Chapter 2 Examples Systematic And Rational Allocation Asset Cost

EXERCISE 2.10 (Continued) (c) Assets should be recorded at the fair value of what is given up or the fair market value of what is received, whichever is more clearly evident. It should be emphasized that it is not a […]

Accounting Chapter 2 Information Provided The Notes The Financial Statements

CHAPTER 2 Conceptual Framework for Financial Reporting ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Concepts for Analysis 1. Conceptual framework– general. 1 1, 2 1, 2 2. Objective of financial reporting. 2, 7 1, 2 3 3. […]

Accounting Chapter 2 Recognizing expenses not when a company pays wages

Test Bank for Intermediate Accounting, Seventeenth Edition 2 – 20 89. The measurement principle includes the a. fair value principle only. b. historical cost principle only. c. revenue recognition principle and expense recognition principle. d. historical cost principle and the […]

Accounting Chapter 20 Amortization of any prior service cost or credit

CE20.3 According to FASB ASC 715-30–35-4 (Defined-Benefit Plans – Pension – Components of Net Periodic Cost): All of the following components shall be included in the net pension cost recognized for a period by an employer sponsoring a defined-benefit pension […]

Accounting Chapter 20 Pension expense for 2020 consisted only of the service

*EXERCISE 20.23 (15–20 minutes) 20–40 Copyright © 2019 WILEY Kieso, Intermediate Accounting, 17/e, Solutions Manual (For Instructor Use Only) ENGLEHART CO. Postretirement Benefit Worksheet—2020 General Journal Entries Memo Record Items Annual Postretirement Expense Cash OCI—Prior Service Cost Postretirement Asset/Liability APBO […]

Accounting Chapter 20 Postretirement benefit expense computation

CHAPTER 20 Accounting for Pensions and Postretirement Benefits ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Basic definitions and concepts related to pension plans. 1, 2, 3, 4, 5, 6, 7, 8, 9, […]

Accounting Chapter 20 The Expected Return Plan Assets And the Settlement

Accounting for Pensions and Postretirement Benefits 20–41 Solution 20-115 Ex. 20-116—Pension plan calculations and journal entry. On January 1, 2021, McGee Co. had the following balances: Projected benefit obligation $7,800,000 Fair value of plan assets 7,800,000 Other data related to […]

Accounting Chapter 20 the pension worksheet on the next page could be

EXERCISE 20.8 (20–25 minutes) Corridor and Minimum Loss Amortization Year Projected Benefit Obligation (a) Plan Assets 10% Corridor Accumulated OCI (G/L) (a) Minimum Amortization of Loss 2019 $2,000,000 $1,900,000 $200,000 $ 0 $ 0 2020 2,400,000 2,500,000 250,000 280,000 3,000(b) […]

Accounting Chapter 20 This case is quite thought-provoking and should stimulate

PROBLEM 20.7 Copyright © 2019 WILEY Kieso, Intermediate Accounting, 17/e, Solutions Manual (For Instructor Use Only) 20-59 HANSON CORP. Pension Worksheet—2020 General Journal Entries Memo Record Items Annual Pension Expense Cash OCI—Prior Service Cost OCI— Gain/Loss Pension Asset/Liability Projected Benefit […]

Accounting Chapter 20 Us Employees And Certain Employees International Locations

Copyright © 2019 WILEY Kieso, Intermediate Accounting, 17/e, Solutions Manual (For Instructor Use Only) 20–79 CA 20.5 1. This situation can exist because companies vary as to which assumption they are using when interest rates are disclosed. In the implicit […]

Accounting Chapter 20 Which measure requires the use of future

Accounting for Pensions and Postretirement Benefits 20–21 The service cost component of pension expense for 2021 is $1,040,000 and the amortization of prior service cost due to an increase in benefits is $210,000. The settlement rate is 10% and the […]

Accounting Chapter 20 What is the amount of Pension Asset

Test Bank for Intermediate Accounting, Sixteenth Edition 20–48 Pr. 20-123 (cont.) Instructions (a) Determine the missing amounts in the 2021 pension worksheet, indicating whether the amounts are debits or credits. (b) Prepare the journal entry to record 2021 pension expense […]

Accounting Chapter 21 End The Year Lease Receivable Interest

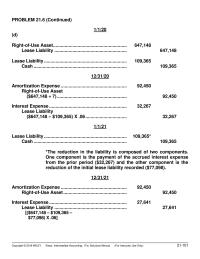

PROBLEM 21.6 (Continued) 1/1/20 (d) Right-of–Use Asset ………………………………………………… 647,148 Lease Liability ……………………………………………….. 647,148 Lease Liability ………………………………………………………. 109,365 Cash ……………………………………………………………… 109,365 12/31/20 Amortization Expense …………………………………………… 92,450 Right-of–Use Asset ($647,148 ÷ 7) ……………………………………………… 92,450 Interest Expense …………………………………………………… 32,267 Lease Liability ($647,148 – […]

Accounting Chapter 21 From The Information Provided This Lease Finance

PROBLEM 21.13 (a) 1. $ 20,027 Interest expense (See amortization schedule) $ 52,174 Amortization expense ($313,043 ÷ 6 = $52,174) 2. Current liabilities: $ 62,700 Lease liability Long-term liabilities: $207,670 Lease liability Non-current assets: $260,869 Right-of-Use asset ($313,043 – $52,174) […]

Accounting Chapter 21 Salaur Expected Purchase The Computers The End

Finally, this vehicle must be amortized over its lease term, using the straight-line method. I computed annual amortization of $2,889 (the initial right–of-use asset, $5,778, divided by the 2-year lease term). The client was advised to make the following entry […]

Accounting Chapter 21 Sands The Lease For 10 year Period The

Accounting for Leases 21 – 21 (a) The term of the noncancelable lease is 3 years with no renewal option. Payments of $574,864 are due on January 1 of each year. (b) The fair value of the machine on January […]

Accounting Chapter 21 The Lease Contains Bargain purchase Option The Lease

CHAPTER 21 Accounting for Leases ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Rationale for leasing. 1, 2, 3 2. Concepts, classification, and measurement of leases. 4, 5, 6, 7, 8, 10, 11, […]

Accounting Chapter 21 The modification grants the lessee an additional

CE21.4 According to FASB ASC 842–30–35-1 > Sales-Type and Direct Financing Leases After the commencement date, a lessor shall measure the net investment in the lease by doing both of the following: a. Increasing the carrying amount to reflect the […]

Accounting Chapter 21 The real estate broker’s fee should be capitalized

EXERCISE 21.15 (Continued) 12/31/20 Interest Expense ……………………………………………. 2,376.60 Lease Liability ………………………………………….. 2,376.60 Amortization Expense ……………………………………. 24,364.99 Right-of–Use Asset ……………………………………. 24,364.99 ($73,094.98 ÷ 3) 1/1/21 Lease Liability ($23,186.36 + $2,376.60) …………… 25,562.96 Cash ………………………………………………………… 25,562.96 12/31/21 Interest Expense ……………………………………………. 1,217.30 Lease […]

Accounting Chapter 21 The Sales Price Less The Present Value

CHAPTER 21 ACCOUNTING FOR LEASES IFRS questions are available at the end of this chapter. TRUE-FALSE—Conceptual Answer No. Description MULTIPLE CHOICE—Conceptual Answer No. Description d 21. Advantages of leasing. d 22. Captive leasing companies. b 23. Basic principle of lease […]

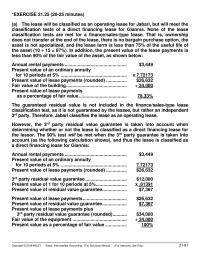

Accounting Chapter 21 The Student Required Identify The Type Lease

*EXERCISE 21.25 (20-25 minutes) (a) The lease will be classified as an operating lease for Jabari, but will meet the classification tests of a direct financing lease for Giannis. None of the lease classification tests are met for a finance/sales-type […]

Accounting Chapter 21 when determining whether or not the lease is classified

Accounting for Leases 21 – 39 DERIVATIONS — Computational (cont.) No. Answer Derivation DERIVATIONS — CPA Adapted No. Answer Derivation 100. c Conceptual. 101. a ($300,000 × 4.7908) – $300,000 = $1,137,240. 102. d $8,756,727 – $2,100,000 = $6,656,727 (2021). […]

Accounting Chapter 21 as they do not transfer a separate good

EXERCISE 21.4 (Continued) Schedule 1 KIMBERLY-CLARK CORP. Lease Amortization Schedule (partial) (Lessee) Date Annual Lease Payment Interest (8%) on Liability Reduction of Lease Liability Lease Liability 12/31/19 $521,934 12/31/19 $71,830 $ 0 $71,830 450,104 12/31/20 71,830 36,008 35,822 414,282 12/31/21 […]

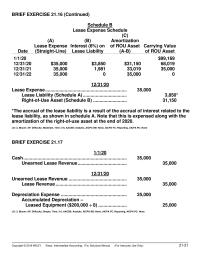

Accounting Chapter 21 Note that this is expensed along with the amortization

BRIEF EXERCISE 21.16 (Continued) Schedule B Lease Expense Schedule Date (A) Lease Expense (Straight-Line) (B) Interest (6%) on Lease Liability (C) Amortization of ROU Asset (A–B) Carrying Value of ROU Asset 1/1/20 $99,169 12/31/20 $35,000 $3,850 $31,150 68,019 12/31/21 35,000 […]

Accounting Chapter 22 A change that has the effect of adjusting the

ACCOUNTING, ANALYSIS, AND PRINCIPLES (Continued) Analysis Inventory turnover: 2020 2019 LIFO N/A LIFO information not available $300 ÷ $490 = 0.61 FIFO $330 ÷ $570 = 0.58 $290 ÷ $545 = 0.53 Inventory turnover is lower under FIFO, which leads […]

Accounting Chapter 22 Corrections Errors Are Recorded The Year Discovered

Test Bank for Intermediate Accounting, Seventeenth Edition 22 – 20 purposes. The change will result in a $3,500,000 increase in the beginning inventory at January 1, 2021. Assume a 20% income tax rate. The cumulative effect of this accounting change […]

Accounting Chapter 22 Discount Bonds Payable Interest Expense

CHAPTER 22 Accounting Changes and Error Analysis ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Differences between change in principle, change in estimate, change in entity, errors. 2, 4, 6, 7, 8, 9, […]

Accounting Chapter 22 The Amendments Include New Alternatives For Measuring

standard will be dependent on the specific facts and circumstances of future individual impairments, if any. In March 2017, the FASB issued ASU 2017-07, “Compensation-Retirement Benefits: Improving the Presentation of Net Periodic Pension Cost and Net Periodic Postretirement Benefit Cost […]

Accounting Chapter 22 The omission in inventory over the two-year period will

PROBLEM 22.6 (Continued) (b) MADRASA INC. Comparative Retained Earnings Statements For the Years Ended 2020 2019 Retained earnings, January 1, as previously reported $200,000 Add: Error in recording equipment (Asset C) 112,000* Retained earnings, January 1, as adjusted $666,000 312,000 […]

Accounting Chapter 22 The student must analyze the effects of errors

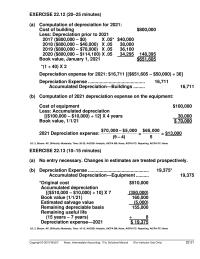

EXERCISE 22.12 (20–25 minutes) (a) Computation of depreciation for 2021: Cost of building $800,000 Less: Depreciation prior to 2021 2017 ($800,000 – $0) X .05* $40,000 2018 ($800,000 – $40,000) X .05 38,000 2019 ($800,000 – $78,000) X .05 36,100 […]

Accounting Chapter 23 A major difference is that in certain situations

Statement of Cash Flows 23 – 59 Ex. 23-124—Preparation of statement of cash flows (format provided). The balance sheets for Kinder Company showed the following information. Additional information concerning transactions and events during 2021 are presented below. Kinder Company Balance […]

Accounting Chapter 23 Harlan Mining Co Has Recently Decided

CHAPTER 23 STATEMENT OF CASH FLOWS IFRS questions are available at the end of this chapter. TRUE-FALSE—Conceptual Answer No. Description MULTIPLE CHOICE—Conceptual Answer No. Description c 21. Objective of the statement of cash flows. c 22. Primary purpose of the […]

Accounting Chapter 23 obtaining cash from creditors and repaying the amounts

CHAPTER 23 Statement of Cash Flows ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Format, objectives purpose, and source of statement. 1, 2, 7, 8, 12 1, 2, 5, 6 2. Classifying investing, […]

Accounting Chapter 23 Operating add Net Income Financing Activity Investing Activity

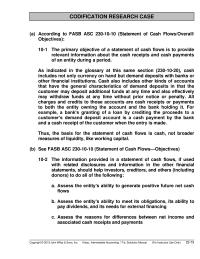

Copyright © 2019 John Wiley & Sons, Inc. Kieso, Intermediate Accounting, 17/e, Solutions Manual (For Instructor Use Only) 23–73 CODIFICATION RESEARCH CASE (a) According to FASB ASC 230-10–10 (Statement of Cash Flows/Overall/ Objectives): 10-1 The primary objective of a statement […]

Accounting Chapter 23 Pepsi co Use The Indirect Method Computing And

CA 23.1 (Continued) 6. The details of changes in long-term debt should be shown separately. Payments should not be netted against increases in long-term borrowings. The long-term borrowing of $620,000 should be shown as cash provided and the retirement of […]

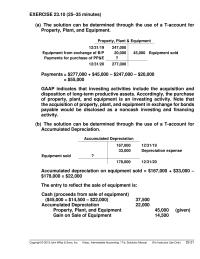

Accounting Chapter 23 to compute net cash provided by operating activities

EXERCISE 23.10 (25–35 minutes) (a) The solution can be determined through the use of a T-account for Property, Plant, and Equipment. Property, Plant & Equipment 12/31/19 247,000 Equipment from exchange of B/P 20,000 45,000 Equipment sold Payments for purchase of […]

Accounting Chapter 23 What is the amount of cash provided by operating

Statement of Cash Flows 23 – 21 63. Financial statements for Kiner Company are given below: Kiner Company Balance Sheet January 1, 2021 Assets Equities Cash $ 960,000 Accounts payable $ 456,000 Accounts receivable 864,000 Buildings and equipment 3,600,000 Accumulated […]

Accounting Chapter 23 What should be the net cash provided by

Statement of Cash Flows 23 – 41 102. A flood damaged a building and contents. The receipts from insurance companies totaled $600,000, which was $180,000 less than the book values. The tax rate is 20%. On the statement of cash […]

Accounting Chapter 23 net income on the accrual basis is adjusted to the cash

PROBLEM 23.3 MORTONSON COMPANY Statement of Cash Flows For the Year Ended December 31, 2020 ($000 Omitted) Cash flows from operating activities Cash receipts from customers …………………. $3,520 (a) Cash payments for: Payments for merchandise ………………….. $1,270 (b) Salaries and […]

Accounting Chapter 24 As reporting for an integral part of an annual

CHAPTER 24 FULL DISCLOSURE IN FINANCIAL REPORTING IFRS questions are available at the end of this chapter. TRUE-FALSE—Conceptual Answer No. Description MULTIPLE CHOICE—Conceptual Answer No. Description d 21. Disclosure of significant accounting policies. c 22. Disclosure of inventory accounting policy. […]

Accounting Chapter 24 Entities For Which Investments Their Equity Securities

CA 24.11 (a) The controller notes that the financial vice president is misrepresenting the financial condition of the company by suggesting that the company has become more efficient when, in fact, the improved ratio is gained through manipulation of estimates. […]

Accounting Chapter 24 Finas Income Statement For The Quarter Ended march

Full Disclosure in Financial Reporting 24 – 21 The following data are provided: December 31 2021 2020 Cash $ 1,500,000 $ 1,000,000 Accounts receivable (net) 1,600,000 1,200,000 Inventories 2,600,000 2,200,000 Plant assets (net) 7,000,000 6,500,000 Accounts payable 1,100,000 800,000 Income […]

Accounting Chapter 24 It further has been suggested that the CPA

Test Bank for Intermediate Accounting, Seventeenth Edition 24 – 34 Solution 24-87 (cont.) (c) The prediction models are probably unsuccessful because accountants have not treated the problem of seasonality correctly in their interim reports. The problem with the conventional approach […]

Accounting Chapter 24 Salaries and wages payable is included as a liability

PROBLEM 24.1 (Continued) Additional comments: 1. The information related to the competitor should be disclosed because this innovation may have a significant effect on the company. The value of the inventory is overstated because of the need to reduce selling […]

Accounting Chapter 24 Understand The Nature And Limitations Accounting

CHAPTER 24 Full Disclosure in Financial Reporting ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis * 1. The disclosure principle; type of disclosure. 2, 3 1, 2, 3 * 2. Role of notes that […]

Accounting Chapter 3 A ledger is where a company first records transactions

CHAPTER 3 THE ACCOUNTING INFORMATION SYSTEM IFRS questions are available at the end of this chapter. TRUE/FALSE Answer No. Description MULTIPLE CHOICE—Conceptual Answer No. Description d 21. Factors shaping an accounting system. d 22. Definition of posting. d 23. DefiNitioN […]

Accounting Chapter 3 Cooke Company Worksheet For The Year Ended

PROBLEM 3.10 (a), (b), (c) Cash Accounts Receivable Allow. for Doubtful Accts. Bal. 18,500 Bal. 32,000 Bal. 700 Adj. 1,400 2,100 Inventory Equipment Accum. Depr.—Equipment Bal. 80,000 Bal. 84,000 Bal. 35,000 Adj. 12,000 47,000 Prepaid Insurance Notes Payable Interest Expense […]

Accounting Chapter 3 If the amount in Supplies Expense is the January

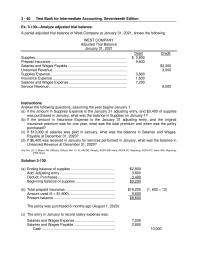

Test Bank for Intermediate Accounting, Seventeenth Edition 3 – 40 Ex. 3-130—Analyze adjusted trial balance. A partial adjusted trial balance of West Company at January 31, 2021, shows the following. WEST COMPANY Adjusted Trial Balance January 31, 2021 Debit Credit […]

Accounting Chapter 3 Interest The Note Payable The First Day

The Accounting Information System 3 – 21 Multiple Choice Answers—Conceptual Item Ans. Item Ans. Item Ans. Item Ans. Item Ans. Item Ans. 21. d 32. a 43. c 54. a 65. c 76. c 22. d 33. a 44. d […]

Accounting Chapter 3 Salaries and Wages Payable Unearned Dues Revenue

PROBLEM 3.3 1. Dec. 31 Salaries and Wages Expense ………………………….. 2,120 Salaries and Wages Payable ………………………….. 2,120 (5 X $700 X 2/5) = $1,400 (3 X $600 X 2/5) = 720 Total accrued salaries $2,120 2. 31 Unearned Rent Revenue […]

Accounting Chapter 3 The Related Terms Realized And Unrealized Therefore

COMPARATIVE ANALYSIS CASE (a) The Coca-Cola Company percentage increase is computed as follows: Total assets (December 31, 2017) ……………………………………………. $87,896 Less: Total assets (December 31, 2016) …………………………………… 87,270b Difference ……………………………………………………………………………… $626a $626a ÷ $87,270b = 0.01% n PepsiCo, Inc.’s percentage […]

Accounting Chapter 3 Total Current Liabilities Stockholders Equity Common

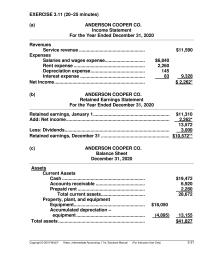

EXERCISE 3.11 (20–25 minutes) (a) ANDERSON COOPER CO. Income Statement For the Year Ended December 31, 2020 Revenues Service revenue ……………………………………………… $11,590 Expenses Salaries and wages expense ………………………….. $6,840 Rent expense …………………………..…………………….. 2,260 Depreciation expense ……………………………………… 145 Interest expense …………………………………………….. […]

Accounting Chapter 3 Differentiate the cash basis of accounting

CHAPTER 3 The Accounting Information System ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems 1. Transaction identification. 1, 2, 3, 5 1, 2 1, 2, 3, 4, 17 1 2. Nominal accounts. 4, 7 3. Trial balance. […]

Accounting Chapter 4 An alternative income statement format is to

EXERCISE 4.3 (Continued) (c) Income attributed to controlling stockholders = (Net income – allocation to noncontrolling interest): Net income [from (b)] $37,300 Allocation to noncontrolling interest 17,000 Income attributable to controlling interest $20,300 LO: 2, 4, Bloom: AP, Difficulty: Simple, […]

Accounting Chapter 4 Both companies use the multiple-step format

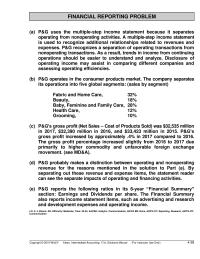

FINANCIAL REPORTING PROBLEM (a) P&G uses the multiple-step income statement because it separates operating from nonoperating activities. A multiple-step income statement is used to recognize additional relationships related to revenues and expenses. P&G recognizes a separation of operating transactions from […]

Accounting Chapter 4 Discontinued Operation Occurs When A Company Eliminates

Income Statement and Related Information 4 – 21 74. Lantos Company had a 20 percent tax rate. Given the following pre-tax amounts, what would be the income tax expense reported on the face of the income statement? Sales revenue $ […]

Accounting Chapter 4 Dividends declared on common and preferred stock

CHAPTER 4 INCOME STATEMENT AND RELATED INFORMATION IFRS questions are available at the end of this chapter. TRUE-FALSE—Conceptual Answer No. Description MULTIPLE CHOICE—Conceptual Answer No. Description c 21. Decreasing current net income. d 22. Usefulness of the income statement. b […]

Accounting Chapter 4 Income from continuing operations before

SOLUTIONS TO PROBLEMS PROBLEM 4.1 DICKINSON COMPANY Income Statement For the Year Ended December 31, 2020 Sales revenue ………………………………………………………. $25,000,000 Cost of goods sold …………………………………………………. 16,000,000 Gross profit ……………………………………………………………. 9,000,000 Selling and administrative expenses ……………………….. 4,700,000 Income from operations………………………………………….. 4,300,000 […]

Accounting Chapter 4 The corporation disposed of its sporting goods

Income Statement and Related Information 4 – 41 Solution 105 (cont.) Ex. 4-106—Income statement classifications. Indicate the major section or subsection of a multiple-step income statement in which each of the following items would usually appear: a. Advertising b. Depletion […]

Accounting Chapter 4 Accounting changes discontinued operations prior

CHAPTER 4 Income Statement and Related Information ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Income measurement concepts. 1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 18, 22, 23, 30, 33, […]

Accounting Chapter 5 Net cash provided by operating activities

EXERCISE 5.5 (Continued) Liabilities and Stockholders’ Equity Current liabilities Notes payable (due 2021) …………………. $ 125,000 Accounts payable …………………………….. 135,000 Rent payable ……………………………………. 49,000 Total current liabilities ………………… $309,000 Long-term liabilities Bonds payable …………………………………. $500,000 Add: Premium on bonds payable […]

Accounting Chapter 5 only investments with original maturities of three

CODIFICATION EXERCISES CE5.1 (a) Current assets is used to designate cash and other assets or resources commonly identified as those that are reasonably expected to be realized in cash or sold or consumed during the normal operating cycle of the […]

Accounting Chapter 5 Similarly Cash Payment That Results Decrease Existing

CHAPTER 5 Balance Sheet and Statement of Cash Flows ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Disclosure principles, uses of the balance sheet, financial flexibility. 1, 2, 3, 4, 5, 6, 7, […]

Accounting Chapter 5 The basis for classifying assets as current

CHAPTER 5 BALANCE SHEET AND STATEMENT OF CASH FLOWS IFRS questions are available at the end of this chapter. TRUE-FALSE—Conceptual Answer No. Description MULTIPLE CHOICE—Conceptual Answer No. Description d 21. Limitation of the balance sheet. c 22. Uses of the […]

Accounting Chapter 5 The ethical issues involved are integrity and honesty

CA 5.4 (a). The ethical issues involved are integrity and honesty in financial reporting, full disclosure, transparency, and the accountant’s professionalism. (b). While presenting property, plant, and equipment net of depreciation on the balance sheet may be acceptable under GAAP, […]

Accounting Chapter 5 The Net Accounts Receivable Balance Includes A

Balance Sheet and Statement of Cash Flows 5 – 39 Solution 5-116 Ex. 5-117—Statement of cash flows. For each event listed below, select the appropriate category which describes the effect of the event on a statement of cash flows: a. […]

Accounting Chapter 5 What Are Intangible Assets What Are Current

Balance Sheet and Statement of Cash Flows 5 – 21 83. For Randolph Company, the following information is available: Capitalized leases $560,000 Copyrights 240,000 Long-term receivables 210,000 In Randolph’s balance sheet, intangible assets should be reported at a. $240,000. b. […]

Accounting Chapter 5 Emphasis is given in this problem to additional

TIME AND PURPOSE OF PROBLEMS Problem 5.1 (Time 30–35 minutes) Purpose—to provide the student with the opportunity to prepare a balance sheet, given a set of accounts. No monetary amounts are to be reported. Problem 5.2 (Time 35–40 minutes) Purpose—to […]

Accounting Chapter 6 Bid A should be accepted since its present value

PROBLEM 6.3 Time diagram (Bid A): i = 9% $69,000 PV – OA = R = ? 3,000 3,000 3,000 3,000 69,000 3,000 3,000 3,000 3,000 0 0 1 2 3 4 5 6 7 8 9 10 n = […]

Accounting Chapter 6 Fund requirements after 15 years of deposits

PROBLEM 6.10 (Continued) Present value of net purchase costs: Down payment ………………………………………………. $ 400,000 Installments …………………………………………………… 1,326,777 Property taxes and other costs ……………………….. 381,567 Insurance ………………………………………………………. 202,367 Total costs …………………………………………………….. 2,310,711 Less: Salvage value ………………………………………. 159,315 Net costs ……………………………………………………….. $2,151,396 […]

Accounting Chapter 6 July And January The Bonds Were Sold to

Test Bank for Intermediate Accounting, Seventeenth Edition 6 – 36 DERIVATIONS — Computational (cont.) No. Answer Derivation 86. c $20,000 × .73503 = $14,701. 87. c $4,000,000 × .09722 = $388,880. 88. d ($40,000 × 6.71008) + ($600,000 × .46319) […]

Accounting Chapter 6 The recommended method of payment would be the

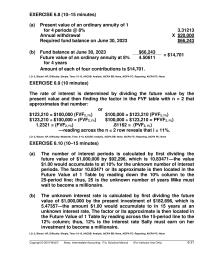

EXERCISE 6.8 (10–15 minutes) (a) Present value of an ordinary annuity of 1 for 4 periods @ 8% 3.31213 Annual withdrawal X $20,000 Required fund balance on June 30, 2023 $66,243 (b) Fund balance at June 30, 2023 $66,243 = […]

Accounting Chapter 6 Trade receivables include notes receivable and

Accounting and the Time Value of Money 6 – 21 77. Barber Company will receive $1,500,000 in 7 years. If the appropriate interest rate is 10%, the present value of the $1,500,000 receipt is a. $765,000. b. $769,740. c. $2,265,000. […]

Accounting Chapter 6 What Time Value Money Concept Appropriate for This

CHAPTER 6 ACCOUNTING AND THE TIME VALUE OF MONEY TRUE-FALSE—Conceptual Answer No. Description MULTIPLE CHOICE—Conceptual Answer No. Description a 21. Appropriate use of an annuity due table. d 22. Time value of money. b 23. Present value situations. a 24. […]

Accounting Chapter 6 Solve present value problems related to deferred

CHAPTER 6 Accounting and the Time Value of Money ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems 1. Present value concepts. 1, 2, 3, 4, 5, 9, 17 2. Use of tables. 13, 14 8 1 3. […]

Accounting Chapter 7 However Maturities Differ Only The Party With

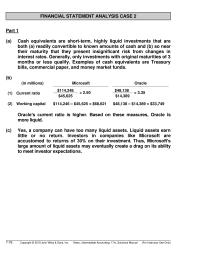

FINANCIAL STATEMENT ANALYSIS CASE 2 Part 1 (a) Cash equivalents are short-term, highly liquid investments that are both (a) readily convertible to known amounts of cash and (b) so near their maturity that they present insignificant risk from changes in […]

Accounting Chapter 7 Lester Company received a seven-year zero

Cash and Receivables 7 – 21 87. Steinert Company has the following items at year-end: Cash in bank $45,000 Petty cash 500 Short-term paper with maturity of 2 months 8,200 Postdated checks 2,100 Steinert should report cash and cash equivalents […]

Accounting Chapter 7 Prepare Schedule Note Discount Amortization For Green

Cash and Receivables 7 – 39 DERIVATIONS — Computational (cont.) No. Answer Derivation 92. a $15,000 ×.02 = $300. 93. c $16,000 ×.01 = $160. 94. b $250,000 − $125,000 = $125,000 95. c 96. d $1,000,000 − [($1,000,000 × […]

Accounting Chapter 7 Recoveries of receivables and write-offs are the types

TIME AND PURPOSE OF PROBLEMS Problem 7.1 (Time 20–25 minutes) Purpose—to provide the student with an understanding of the balance sheet effect that occurs when the cash book is left open. In addition, the student is asked to adjust the […]

Accounting Chapter 7 The Board Believes That Fair Value Measurement

CHAPTER 7 Cash and Receivables ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Accounting for cash. 1, 2, 3, 4, 23 1 1, 2 1 2. Accounting for accounts receivable, bad debts, other […]

Accounting Chapter 7 The company plans to make five annual deposits

CHAPTER 7 CASH AND RECEIVABLES IFRS questions are available at the end of this chapter. TRUE-FALSE—Conceptual Answer No. Description MULTIPLE CHOICE—Conceptual Answer No. Description d 26. Identification of cash items. b 27. Identification of cash items. d 28. Classification of […]

Accounting Chapter 7 The note can be considered to be impaired only

*PROBLEM 7.14 (Continued) (b) November 30 Cash ………………………………………………………………… 1,400.00 Interest Revenue ………………………………………. 1,400.00 November 30 Office Expense (bank charges) ………………………….. 27.40 Cash ………………………………………………………… 27.40 November 30 Accounts Receivable ………………………………………… 372.13 Cash ………………………………………………………… 372.13 LO: 6, Bloom: AP, Difficulty: Moderate, Time: […]

Accounting Chapter 7 The Transferor Does Not Maintain Effective Control

EXERCISE 7.4 (Continued) Selling price = 1.4 (Cost of goods sold) = 1.4 ($230,000*) = $322,000 Sales on account $322,000 Less: Collections 198,000 Uncollected balance 124,000 Balance per ledger 82,000 Apparent shortage $ 42,000 —Enough for a new car LO: […]

Accounting Chapter 8 A modified perpetual inventory system provides

CHAPTER 8 VALUATION OF INVENTORIES: A COST-BASIS APPROACH TRUE-FALSE—Conceptual Answer No. Description MULTIPLE CHOICE—Conceptual Answer No. Description c 21. Identify manufacturer inventory similar to merchandise inventory. d 22. Sales with buyback agreement. a 23. Sales with high rates of return. […]

Accounting Chapter 8 Aber Company manufactures one product

Valuation of Inventories: A Cost-Basis Approach 8 – 39 145. Keck Co. had 300 units of product A on hand at January 1, 2020, costing $21 each. Purchases of product A during January were as follows: Date Units Unit Cost […]

Accounting Chapter 8 Chess Top uses the periodic inventory system

Valuation of Inventories: A Cost-Basis Approach 8 – 21 Multiple Choice Answers—Conceptual MULTIPLE CHOICE—Computational 84. Morgan Manufacturing Company has the following account balances at year end: Office supplies $ 4,000 Raw materials 27,000 Work-in-process 59,000 Finished goods 97,000 Prepaid insurance […]

Accounting Chapter 8 Lifo Inventory After Converting The Closing Inventory

CHAPTER 8 Valuation of Inventories: A Cost-Basis Approach ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Inventory accounts; determining quantities, costs, and items to be included in inventory; the inventory equation; balance sheet […]

Accounting Chapter 8 Noven should consider first whether the inventory

FINANCIAL STATEMENT ANALYSIS CASE 2 (a) The most likely physical flow of goods for a pharmaceutical manufac– turer would be FIFO; that is, the first goods manufactured would be the first goods sold. This is because pharmaceutical goods have an […]

Accounting Chapter 8 Purchase Discounts Lost treat as financial expense

PROBLEM 8.3 (Continued) 8/15 Purchases ……………………………………………………… 15,840 Accounts Payable ($16,000 X .99) ……………. 15,840 8/25 Purchases ……………………………………………………… 19,600 Accounts Payable ($20,000 X .98) ……………. 19,600 8/28 Accounts Payable ………………………………………….. 15,840 Purchase Discounts Lost ……………………………….. 160 Cash ……………………………………………………… 16,000 2. 8/31 […]

Accounting Chapter 8 title passes to the buyer when the seller delivers

Time and Purposes of Concepts for Analysis (Continued) CA 8.10 (Time 30–35 minutes) Purpose—to provide the student with an opportunity to analyze the effect of changing from the FIFO method to the LIFO method on items such as ending inventory, […]

Accounting Chapter 8 which are the higher prices in this case

EXERCISE 8.10 (15–20 minutes) (a) Units in ending inventory Beginning balance 300 Purchase 1,300 (800 + 500) Goods available 1,600 Sales (1,000) (200 + 500 + 300) Ending balance 600 Cost of Goods Sold Ending Inventory (1) LIFO 500 @ […]

Accounting Chapter 9 A departure from cost is justified on the basis

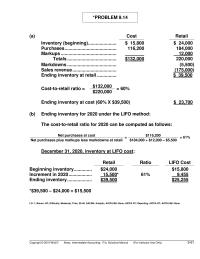

*PROBLEM 9.14 (a) Cost Retail Inventory (beginning) …………………. $ 15,800 $ 24,000 Purchases …………………………………. 116,200 184,000 Markups ……………………………………. 12,000 Totals ……………………………….. $132,000 220,000 Markdowns ……………………………….. (5,500) Sales revenue ……………………………. (175,000) Ending inventory at retail …………… $ 39,500 Cost-to-retail ratio = […]

Accounting Chapter 9 April Merchandise Shipments Paid Unrecorded Purchases

SOLUTIONS TO PROBLEMS PROBLEM 9.1 Item Cost Net Realizable Value* Lower-of– Cost-or–NRV A $470 $ 450 $450 B 450 430 430 C 830 640 640 D 960 1,000 960 *Net Realizable Value = 2021 catalog selling price less estimated costs […]

Accounting Chapter 9 Henke Co. uses the retail inventory method

Inventories: Additional Valuation Issues 9 – 41 135. Keen Company’s accounting records indicated the following information: Inventory, 1/1/20 $ 1,800,000 Purchases during 2020 9,000,000 Sales during 2020 11,400,000 A physical inventory taken on December 31, 2020, resulted in an ending […]

Accounting Chapter 9 How would a comparison of these methods

Inventories: Additional Valuation Issues 9 – 53 Solution 9-147 PROBLEMS Pr. 9-148—Gross profit method. On December 31, 2021 Felt Company’s inventory burned. Sales and purchases for the year had been $1,500,000 and $980,000, respectively. The beginning inventory (Jan. 1, 2021) […]

Accounting Chapter 9 Net Markdowns Sales Price Goods Available Deduct

Copyright © 2019 WILEY Kieso, Intermediate Accounting, 17/e, Solutions Manual (For Instructor Use Only) 9-21 EXERCISE 9.9 (15–20 minutes) 15 – 7 = 8 17 – 2 = 15 LO: 3, Bloom: AP, Difficulty: Simple, Time: 15-20, AACSB: Analytic, AICPA […]

Accounting Chapter 9 The Complement The Markup Percent Determined Then

CHAPTER 9 Inventories: Additional Valuation Issues ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1 Lower-of-cost-or-net realizable value 1, 2, 3, 4, 5 1, 2, 3 1, 2, 3, 4, 5, 6 1, 2, […]

Accounting Chapter 9 This Definition Inventories Excludes Longterm Assets Subject

ACCOUNTING, ANALYSIS, AND PRINCIPLES (Continued) (b) Inventory at cost = $245,000 + $500,000 = $745,000 NRV = $275,000 + $450,000 = $725,000 $725,000 < $745,000, therefore write inventory down to $725,000 Total amount of inventory reported on March 31 balance […]