Archives

Accounting Chapter 08 1 Compute And Interpret The Fixed Overhead Budget

Appendix 8A Predetermined Overhead Rates and Overhead Analysis in a Standard Costing System Answer Key True / False Questions 1. TRUE AACSB: Reflective Thinking AICPA: BB Critical Thinking AICPA: FN Measurement Accessibility: Keyboard Navigation Blooms: Understand Learning Objective: 08-07 (Appendix […]

Accounting Chapter 08 1 Efficiency Variance For June Would Recorded Aa

Appendix 8B Journal Entries to Record Variances Answer Key True / False Questions 1. FALSE AACSB: Reflective Thinking AICPA: BB Critical Thinking AICPA: FN Measurement Accessibility: Keyboard Navigation Blooms: Understand Learning Objective: 08-08 (Appendix 8B) Prepare journal entries to record […]

Accounting Chapter 08 2 Enwall Corporations Standard Wage Rate 1120

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 31. A. Raw materials $2,000, Debit; materials price variance $250, Credit B. Raw materials $1,750, Debit; materials price variance $250, […]

Accounting Chapter 08 2 Pizzi Inc Had The Following Fixed

App8A-107 29. Semaan Corporation applies manufacturing overhead to products on the basis of standard machine-hours. Budgeted and actual overhead costs for the month appear below: Original Budget Actual Costs Variable overhead costs: Supplies $11,340 $12,850 Indirect labor 15,120 17,080 Fixed […]

Accounting Chapter 08 3 The 17200 hours Worked During The Period Resulted

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Blooms: Apply Learning Objective: 08-03 Prepare a flexible budget with more than one cost driver. Learning Objective: 08-07 (Appendix 8A) […]

Accounting Chapter 08 3 The Standards For Product F28 Call

8-72 Essay Questions Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 8-73 48. Albert Manufacturing Company manufactures a single product. The standard cost of one unit of this […]

Accounting Chapter 08 4 Difficulty Medium topic Area Appendix 8a Predetermined Overhead

App8A-147 SH = 13,000 units × 1.4 machine-hours per unit = 18,200 machine-hours SR = ($10,000) ÷ 20,000 machine-hours = $0.50 per machine-hour Variable overhead efficiency variance = (AH – SH) × SR = (17,000 machine-hours – 18,200 machine-hours) × […]

Accounting Chapter 08 5 Actual Fixed Overhead Budgeted Fixed Overhead Cost

App8A-167 Topic Area: Appendix 8A: Predetermined Overhead Rates and Overhead Analysis in a Standard Costing System 72. A manufacturer of playground equipment uses a standard costing system in which standard machine-hours (MHs) is the measure of activity. Data from the […]

Accounting Chapter 08 6 Odonell Corporation Estimates That Its Variable

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 87. The following data for February has been provided by Gillard Corporation. Denominator level of activity 3,700 machine-hours Budgeted fixed […]

Accounting Chapter 08 7 Littleton Manufacturing Uses Standard Cost System

App8A-207 102. Cajun Corporation manufactures a labor-intensive product. The cost standards developed by Cajun appear below. Manufacturing overhead at Cajun is applied to production on the basis of standard direct labor-hours: Standard quantity per unit Standard cost per ounce or […]

Accounting Chapter 1 1 Difficulty Easy topic Area Traditional And Contribution Format

Chapter 01 Managerial Accounting and Cost Concepts Answer Key True / False Questions 1. TRUE AACSB: Reflective Thinking AICPA: BB Critical Thinking AICPA: FN Measurement Accessibility: Keyboard Navigation Blooms: Remember Learning Objective: 01-02 Identify and give examples of each of […]

Accounting Chapter 1 10 Sobota Corporation Has Provided The Following

1-275 184. Sobota Corporation has provided the following partial listing of costs incurred during August: Marketing salaries $49,000 Property taxes, factory $7,000 Administrative travel $104,000 Sales commissions $49,000 Indirect labor $38,000 Direct materials $138,000 Advertising $76,000 Depreciation of production equipment […]

Accounting Chapter 1 2 Within The Relevant Range Variable Cost

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Learning Objective: 01-04 Understand cost classifications used to predict cost behavior: variable costs, fixed costs, and mixed costs. Level of […]

Accounting Chapter 1 3 Given The Cost Formula 7000 180x

1-140 78. Given the cost formula, Y = $7,000 + $1.80X, total cost for an activity level of 4,000 units would be: A. $7,000 B. $200 C. $7,200 D. $14,200 Y = $7,000 + ($1.80 per unit × X) = […]

Accounting Chapter 1 4 The Following Data Pertains Activity And

1-160 91. The following data pertains to activity and utility cost for two recent periods: Activity level (units) 8,000 5,000 Utility cost $8,000 $6,150 A. Y = $1.00 X B. Y = $1.25 X C. Y = $4,000 + $0.50 […]

Accounting Chapter 1 5 Corcetti Company Manufactures And Sells Prewashed

1-180 Topic Area: Cost Classifications for Manufacturing Companies 110. A partial listing of costs incurred during December at Rooks Corporation appears below: Factory supplies $7,000 Administrative wages and salaries $92,000 Direct materials $176,000 Sales staff salaries $32,000 Factory depreciation $52,000 […]

Accounting Chapter 1 6 Erkkila Inc Reports That Activity Level

1-200 131. A. $12.30 B. $11.79 C. $10.92 D. $12.05 Helpline cost per unit = Total helpline costs ÷ Number of calls = $369,000 ÷ 30,000 calls = $12.30 per call The average helpline cost per call is constant within […]

Accounting Chapter 1 7 Bee Company Honey Wholesaler Income Statement

1-220 145. Baker Corporation has provided the following production and total cost data for two levels of monthly production volume. The company produces a single product. Production volume 6,000 units 7,000 units Direct materials $194,400 $226,800 Direct labor $74,400 $86,800 […]

Accounting Chapter 1 8 Data Concerning Nelson Companys Activity For

1-240 = $36.11 per escrow AACSB: Analytical Thinking AICPA: BB Critical Thinking AICPA: FN Measurement Blooms: Apply Learning Objective: 01-05 Analyze a mixed cost using a scattergraph plot and the high-low method. Level of Difficulty: 2 Medium Topic Area: The […]

Accounting Chapter 1 9 Dechico Corporation Purchased Machine Years Ago

1-260 173. Searls Corporation, a merchandising company, reported the following results for July: Number of units sold 2,700 units Selling price per unit $664 per unit Unit cost of goods sold $405 per unit Variable selling expense per unit $48 […]

Accounting Chapter 1 Lecture Notes Iii The Analysis Mixed

Chapter 01 Lecture Notes 1 that will be discussed in this chapter, namely cost classifications for assigning costs to cost objects, financial reporting, predicting cost behavior, and making business decisions. 2 subunits, etc. For purposes of assigning costs to cost […]

Accounting Chapter 1 Moreover For Planning Purposes The Company Likely

Problem 1-22A (continued) 3. The high-low estimate of fixed costs is $170.90 lower than the estimate provided by least-squares regression. The high-low estimate of the variable cost per unit is $1.82 higher than the estimate provided by least-squares regression. A […]

Accounting Chapter 1 The Cost Gasoline Consumed The Meal son wheels Van

Exercise 1-13 (20 minutes) 1. Traditional income statement The Alpine House, Inc. Traditional Income Statement Sales ………………………………………………………. $150,000 Cost of goods sold ($30,000 + $100,000 – $40,000) ………………… 90,000 Gross margin …………………………………………….. 60,000 Selling and administrative expenses: Selling expenses (($50 […]

Accounting Chapter 1 The Wages The Companys Accountant Administrative Depreciation

Chapter 1 Managerial Accounting and Cost Concepts Solutions to Questions 1-1 The three major elements of product costs in a manufacturing company are direct materials, direct labor, and manufacturing overhead. 1-2 a. Direct materials are an integral part of a […]

Accounting Chapter 10 2 Net operating income would decrease by $77,400 per year.

Feedback: Product H58S Sales …………………………………………………………… $490,000 Variable expenses ………………………………………… 221,000 Contribution margin ………………………………………. 269,000 58. Part S00 is used in one of Morsey Corporation’s products. The company makes 6,000 units of this part each year. The company’s Accounting Department reports […]

Accounting Chapter 10 3 Suppose The Special Order For 4000

Nesmith Corporation is considering two alternatives: A and B. Costs associated with the alternatives are listed below: 88. Are the materials costs and processing costs relevant in the choice between alternatives A and B? (Ignore the equipment rental and occupancy […]

Accounting Chapter 10 4 The sale of these defective units will have no effect

121. Suppose the special order is for 6,000 haks this month and thus some regular sales would have to be given up. If this offer is accepted by Molis, the company’s operating income for the month will: A) increase by […]

Accounting Chapter 10 5 Relevant, since costs differ between alternatives

Essay [QUESTION] 154. Nicklin Corporation is considering two alternatives that are code-named M and N. Costs associated with the alternatives are listed below: Alternative M Alternative N Supplies costs ………. $32,000 $58,000 Assembly costs …….. $47,000 $47,000 Power costs ………….. […]

Accounting Chapter 10 6 The normal unit product cost of product Y19 is computed as

170. Tullius Corporation has received a request for a special order of 8,000 units of product C64 for $50.00 each. The normal selling price of this product is $53.25 each, but the units would need to be modified slightly for […]

Accounting Chapter 10 Because the Mike doll has the lowest contribution

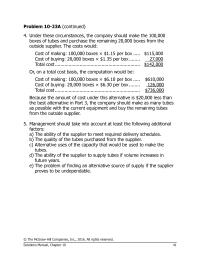

Problem 10-23A (continued) 4. Under these circumstances, the company should make the 100,000 boxes of tubes and purchase the remaining 20,000 boxes from the outside supplier. The costs would: Cost of making: 100,000 boxes × $1.15 per box ….. $115,000 […]

Accounting Chapter 10 A relevant cost is a cost that differs in total

Chapter 10 Differential Analysis: The Key to Decision Making Solutions to Questions 10-1 A relevant cost is a cost that differs in total between the alternatives in a decision. 10-2 An incremental cost (or benefit) is the change in cost […]

Accounting Chapter 11 1 Education topic Area Preference Decisions The Ranking Investment

Chapter 11 Capital Budgeting Decisions Answer Key True / False Questions 1. FALSE AACSB: Reflective Thinking AICPA: BB Critical Thinking AICPA: FN Measurement Accessibility: Keyboard Navigation Blooms: Understand Learning Objective: 11-01 Determine the payback period for an investment. Level of […]

Accounting Chapter 11 1 The annual payment under the lease will be $4,781

Appendix 11A The Concept of Present Value Answer Key True / False Questions 1. TRUE AACSB: Reflective Thinking AICPA: BB Critical Thinking AICPA: FN Measurement Accessibility: Keyboard Navigation Blooms: Understand Learning Objective: 11-05 (Appendix 11A) Understand the present value concepts […]

Accounting Chapter 11 2 Peter Wants Buy Computer Which Expects

11–115 34. Correl Corporation has provided the following data concerning an investment project that it is considering: Initial investment $190,000 Annual cash flow $75,000 per year Salvage value at the end of the project $25,000 A. $38,500 B. $228,500 C. […]

Accounting Chapter 11 3 Crowley Corporation Considering Three Investment Projects

11–135 58. The management of Edelmann Corporation is considering the following three investment projects: Project R Project S Project T Investment required $13,000 $59,000 $79,000 Present value of cash inflows $13,520 $66,080 $87,690 A. T, S, R B. R, T, […]

Accounting Chapter 11 4 Sawyers Discount Rate 12 the Net Present Value

11–155 Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 11–156 78. Carlson Manufacturing has some equipment that needs to be rebuilt or replaced. The following information has been […]

Accounting Chapter 11 5 The Management Keno Corporation Considering Three

11–175 A. ($483,095) B. ($583,095) C. ($596,395) D. ($536,395) AACSB: Analytical Thinking AICPA: BB Critical Thinking AICPA: FN Measurement Blooms: Apply Learning Objective: 11-02 Evaluate the acceptability of an investment project using the net present value method. Level of Difficulty: […]

Accounting Chapter 11 6 Vernon Corporation has been offered a 5-year

11–195 Learning Objective: 11-02 Evaluate the acceptability of an investment project using the net present value method. Level of Difficulty: 1 Easy Topic Area: The Net Present Value Method Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or […]

Accounting Chapter 11 7 The working capital would be released at the end of the project

11–208 112. Annual cash inflows $100,000 Annual cash outflows: Building rent $25,000 Other annual cash outflows 44,000 69,000 Annual net cash inflow $31,000 Year Now 1-6 6 Initial investment ($50,000) Mark Stevens is considering opening a hobby and craft store. […]

Accounting Chapter 11 Cost The New Machine Scrap Value

Problem 11-25A (continued) 2. Considering all three investments together, Linda did not earn a 16% rate of return. The computation is: Net Present Value Common stock ……………………. $ 7,560 Preferred stock ……………………. (8,650) Bonds ……………………………….. (2,743) Overall net present value […]

Accounting Chapter 11 The company would want Casey to invest in

Problem 11-13A (continued) 2. The simple rate of return is computed as follows: Annual incremental net operating income Simple rate of return = Initial investment $400,000 = = 11.4% $3,500,000 3. The company would want Casey to invest in the […]

Accounting Chapter 11 The Net Present Value The Investment Opportunity

Chapter 11 Capital Budgeting Decisions projects that have long-term implications such as the purchase of new equipment and the introduction of new products. This chapter describes three methods for making these types of investment decisions—the payback method, the net present […]

Accounting Chapter 11 A capital budgeting screening decision is concerned

Chapter 11 Capital Budgeting Decisions Solutions to Questions 11-1 A capital budgeting screening decision is concerned with whether a proposed investment project passes a preset hurdle, such as a 15% rate of return. A capital budgeting preference decision is concerned […]

Accounting Chapter 12 1 Appendix 12a The Direct Method Determining The

Appendix 12A The Direct Method of Determining the Net Cash Provided by Operating Activities Answer Key True / False Questions 1. FALSE AACSB: Reflective Thinking AICPA: BB Critical Thinking AICPA: FN Measurement Accessibility: Keyboard Navigation Blooms: Remember Learning Objective: 12-04 […]

Accounting Chapter 12 1 Classify cash inflows and outflows as relating to operating,

Chapter 12 Statement of Cash Flows Answer Key True / False Questions 1. TRUE AACSB: Reflective Thinking AICPA: BB Critical Thinking AICPA: FN Measurement Accessibility: Keyboard Navigation Blooms: Remember Learning Objective: 12-01 Classify cash inflows and outflows as relating to […]

Accounting Chapter 12 10 Prepare a statement of cash flows using the indirect method

12–292 129. Beltram Corporation’s balance sheet and income statement appear below: Comparative Balance Sheet Ending Balance Beginning Balance Assets: Cash and cash equivalents $30 $26 Accounts receivable 37 43 Inventory 67 63 Property, plant and equipment 601 560 Less accumulated […]

Accounting Chapter 12 2 Gross Margin 235 Selling And Administrative Expense

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Gross margin 235 Selling and administrative expense 158 Net operating income 77 Income taxes 23 Net income $54 Cash dividends […]

Accounting Chapter 12 2 Partin Corporations Cash And Cash Equivalents

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 47. A. a net $9,000 increase. B. a net $29,000 decrease. C. a net $38,000 increase. D. a net $38,000 […]

Accounting Chapter 12 3 Furis Corporations Cash And Cash Equivalents

12–161 61. Autry Corporation’s balance sheet and income statement appear below: Comparative Balance Sheet Ending Balance Beginning Balance Assets Current assets: Cash and cash equivalents $33 $26 Accounts receivable 67 68 Inventory 54 65 Total current assets 154 159 Property, […]

Accounting Chapter 12 3 The net cash provided by (used in) financing

12–120 30. Kilduff Corporation’s balance sheet and income statement appear below: Comparative Balance Sheet Ending Balance Beginning Balance Assets: Cash and cash equivalents $36 $38 Accounts receivable 36 32 Inventory 49 55 Property, plant and equipment 707 580 Less accumulated […]

Accounting Chapter 12 4 Last Year Knox Corporation Reported Its

12–140 40. The changes in Northrup Corporation’s balance sheet account balances for last year appear below: Increases (Decreases) Asset and Contra-Asset Accounts: Cash $4,000 Accounts receivable ($4,000) Inventory ($2,000) Prepaid expenses $2,000 Long-term investments $40,000 Property, plant and equipment $25,000 […]

Accounting Chapter 12 4 The Data Given Below Are From

12–181 Level of Difficulty: 2 Medium Topic Area: Organizing the Statement of Cash Flows Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 12–182 73. Degeare Corporation’s balance sheet […]

Accounting Chapter 12 5 Difficulty Medium topic Area Example Statement Cash Flows

12–201 C. $40,000 D. $52,000 Operating activities: Net income $11,000 Adjustments to convert net income to a cash basis: Depreciation ($207,000 – $177,000) $30,000 Increase in accounts receivable ($22,000 – $18,000) (4,000) Decrease in inventory ($66,000 – $70,000) 4,000 Decrease […]

Accounting Chapter 12 5 Use the direct method to determine the net cash provide

12–160 Purchase of property, plant and equipment ($278,000 – $150,000) (128,000) Net cash provided by investing activities (92,500) Financing activities: Repaying principle on bonds payable (15,000) Issuance of bonds payable ($120,000 – $30,000 – $15,000) 105,000 Issuance of common stock […]

Accounting Chapter 12 6 Property, plant, and equipment 374,000354,000 Less accumulated

12–221 B. The change in Prepaid Expenses will be subtracted from net income; The change in Income Taxes Payable will be subtracted from net income C. The change in Prepaid Expenses will be subtracted from net income; The change in […]

Accounting Chapter 12 6 Selling and 270,000 administrative expense

12–175 Gross margin 160,000 Selling and administrative expense 158,000 Net income $2,000 Requirements a through d: Sales (as reported) $350,000 Adjustments to a cash basis: Increase in accounts receivable –5,000 $345,000 The company did not dispose of any property, plant, […]

Accounting Chapter 12 7 It did not dispose of any property, plant, and equipment during the year.

12–241 D. ($15) Investing activities: Purchase of property, plant, and equipment ($386 – $360) ($26) Net cash provided by (used in) investing activities ($26) AACSB: Analytical Thinking AICPA: BB Critical Thinking AICPA: FN Measurement Blooms: Apply Learning Objective: 12-01 Classify […]

Accounting Chapter 12 8 For All Other Items Indicate Whether The

12–261 C. The change in Accounts Receivable will be added to net income; The change in Inventory will be added to net income D. The change in Accounts Receivable will be subtracted from net income; The change in Inventory will […]

Accounting Chapter 12 9 The company did not dispose of any property, plant, and equipment, sell any

12–281 125. Thunder Corporation’s balance sheet and income statement appear below: Comparative Balance Sheet Ending Balance Beginning Balance Assets: Cash and cash equivalents $28 $31 Accounts receivable 60 65 Inventory 41 42 Property, plant, and equipment 454 380 Less accumulated […]

Accounting Chapter 12 Current Liabilities Accounts Payable Accrued Liabilities

Chapter 12 Statement of Cash Flows Solutions to Questions 12-1 The statement of cash flows highlights the major activities that impact cash flows and hence affect the overall cash balance. 12-2 Cash equivalents are short-term, highly liquid investments such as […]

Accounting Chapter 12 Lets Assume That The Company Reported The

2. Can we pay our debts? 3. Can we pay dividends? 4. Will we have to borrow money to make needed investments? 5. Why is there a difference between net income and net cash flow? 3 in all noncash balance […]

Accounting Chapter 12 Paid suppliers for inventory purchases

Problem 12-8A (20 minutes) Transaction Operating Investing Financing Cash Inflow Cash Outflow a. Paid suppliers for inventory purchases ….. X X b. Bought equipment for cash ……………….. X X c. Paid cash to repurchase its own stock ….. X X […]

Accounting Chapter 12 Proceeds from sale of long-term investments

Problem 12-13A (continued) The decrease in the long-term investments account ($20,000) equals the cost of the long-term investment sold; therefore, Rusco did not purchase any long-term investments during the year. The proceeds from the sale of the long-term investment ($30,000) […]

Accounting Chapter 13 1 Compute and interpret financial ratios that managers

Chapter 13 Financial Statement Analysis Answer Key True / False Questions 1. TRUE AACSB: Reflective Thinking AICPA: BB Critical Thinking AICPA: FN Measurement Accessibility: Keyboard Navigation Blooms: Remember Learning Objective: 13-01 Prepare and interpret financial statements in comparative and common-size […]

Accounting Chapter 13 10 Compute and interpret financial ratios that managers use for asset management

13–465 Sales (all on account) $1,370,000 Cost of goods sold 850,000 Gross margin 520,000 Operating expenses 482,692 Net operating income 37,308 Interest expense 21,000 Net income before taxes 16,308 Income taxes (35%) 5,708 Net income $10,600 A. 10.17 B. 0.10 […]

Accounting Chapter 13 11 Dollars Thousands Sales All Account 1770 Cost

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. (dollars in thousands) Sales (all on account) $1,770 Cost of goods sold 1,230 Gross margin 540 Selling and administrative expense […]

Accounting Chapter 13 12 Year And 1520000 At the End Year Its

13–505 AACSB: Analytical Thinking AICPA: BB Critical Thinking AICPA: FN Measurement Blooms: Apply Learning Objective: 13-04 Compute and interpret financial ratios that managers use for debt management purposes. Level of Difficulty: 2 Medium Topic Area: Ratio Analysis – Profitability Copyright […]

Accounting Chapter 13 13 Common Stock Par Value 240000 Per Share

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Net operating income 51,308 Interest expense 19,000 Net income before taxes 32,308 Income taxes (35%) 11,308 Net income $21,000 Dividends […]

Accounting Chapter 13 14 Year Totaled 2500 The Market Price Common stock

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 234. Sperle Corporation has provided the following data concerning its stockholders’ equity accounts: Year 2 Year 1 Stockholders’ equity: Common […]

Accounting Chapter 13 15 Marketable Securities Accounts Receivable Short-term Notes receivable 160

13–565 248. Data from Yochem Corporation’s most recent balance sheet appear below: Cash $16,000 Marketable securities $24,000 Accounts receivables $39,000 Inventory $53,000 Prepaid expenses $11,000 Current liabilities $109,000 Acid-test ratio = Quick assets* ÷ Current liabilities = $79,000 ÷ $109,000 […]

Accounting Chapter 13 16 Return Equity Net Income Average Total Stockholders

13–585 Level of Difficulty: 3 Hard Source: CMA, adapted Topic Area: Ratio Analysis – Asset Management Topic Area: Ratio Analysis – Debt Management Topic Area: Ratio Analysis – Profitability Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or […]

Accounting Chapter 13 17 Wyand Corporations Net Operating Income Last

13–605 = £180 ÷ £900 = 20% Current ratio = Current assets* ÷ Current liabilities = £221 ÷ £147 = 1.5 *Current assets = £5 + £120 + £96 = £221 Inventory turnover = Cost of goods sold ÷ Average […]

Accounting Chapter 13 18 Common Dividends Common Shares See Above 2100

13–625 271. Sidell Corporation’s most recent balance sheet and income statement appear below: Balance Sheet December 31, Year 2 and Year 1 (in thousands of dollars) Assets Year 2 Year 1 Current assets: Cash $180 $100 Accounts receivable 220 200 […]

Accounting Chapter 13 19 Year 2e What The Companys Price earnings Ratio

13–645 k. Dividend yield ratio = Dividends per share* ÷ Market price per share = $0.02 ÷ $1.49 = 1.34% (rounded) *Dividends per share = Common dividends ÷ Common shares (see above) = $2,000 ÷ 100,000 shares = $0.02 per […]

Accounting Chapter 13 2 The Gross Margin Percentage Equal To

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 55. The gross margin percentage is equal to: A. (Net operating income + Selling and administrative expenses)/Sales B. Net operating […]

Accounting Chapter 13 20 What is the company’s return on equity for Year 2?

13–661 284. Degollado Corporation’s most recent income statement appears below: Sales (all on account) $140,000 Cost of goods sold 60,000 Gross margin 80,000 Selling and administrative expense 30,000 Net operating income 50,000 Interest expense 10,000 Net income before taxes 40,000 […]

Accounting Chapter 13 3 Last Year Truro Corporation Purchased 800000

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. AICPA: FN Measurement Blooms: Apply Learning Objective: 13-03 Compute and interpret financial ratios that managers use for asset management purposes. […]

Accounting Chapter 13 4 Crosswhite Corporations Sales Last Year Were

13–345 102. Crosswhite Corporation’s sales last year were $1,270,000, its gross margin was $400,000, its net operating income was $53,769, and its net income was $26,500. The company’s net profit margin percentage is closest to: A. 31.5% B. 3.2% C. […]

Accounting Chapter 13 5 All Rights Reserved Reproduction Distribution Without The

13–365 122. Hernande Corporation has provided the following data: Year 2 Year 1 Common stock, $4 par value $400,000 $400,000 Net operating income $75,429 Net income before taxes $61,429 Net income $43,000 A. $4.25 per share B. $0.43 per share […]

Accounting Chapter 13 6 Excerpts from Colter Corporation’s most recent balance sheet appear

13–385 137. Mayfield Corporation has provided the following financial data: Assets Current assets: Cash $223,000 Accounts receivable 236,000 Inventory 202,000 Prepaid expenses 10,000 Total current assets 671,000 Plant and equipment, net 665,000 Total assets $1,336,000 Liabilities and Stockholders’ Equity Current […]

Accounting Chapter 13 7 Data from Dunshee Corporation’s most recent balance sheet appear

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. stockholders’ equity Income Statement For the Year Ended December 31, Year 2 (in thousands of dollars) Sales (all on account) […]

Accounting Chapter 13 8 The acid-test ratio at the end of Year 2 is closest

13–425 Blooms: Apply Learning Objective: 13-03 Compute and interpret financial ratios that managers use for asset management purposes. Level of Difficulty: 2 Medium Topic Area: Ratio Analysis – Debt Management Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction […]

Accounting Chapter 13 9 Year Totaled 1600 The Market Price Common stock

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 171. Ribaudo Corporation has provided the following financial data from its balance sheet and income statement: Year 2 Year 1 […]

Accounting Chapter 13 A sale of inventory on account will increase

Problem 13-13A (45 minutes) Effect on Ratio Reason for Increase, Decrease, or No Effect 1. Decrease but have no effect on current assets. Therefore, the current ratio will decrease. Declaring a cash dividend will increase current liabilities, 2. Increase but […]

Accounting Chapter 13 Calculation Inventory Turnover Inventory Turnover Cost Goods

Chapter 13 Financial Statement Analysis Solutions to Questions 13-1 Horizontal analysis examines how a particular item on a financial statement such as sales or cost of goods sold behaves over time. Vertical analysis involves analysis of items on an income […]

Accounting Chapter 13 The drain on the cash account seems to be a result

Problem 13-18A (continued) b. Sabin Electronics Common-Size Income Statements This Year Last Year Sales …………………………………………….. 100.0 % 100.0 % Cost of goods sold ……………………………. 77.5 79.3 Gross margin ………………………………….. 22.5 20.7 Selling and administrative expenses …….. 13.1 12.6 Net operating […]

Accounting Chapter 2 1 When completed goods are sold, the transaction is recorded as a debit

Chapter 02 Job-Order Costing Answer Key True / False Questions 1. FALSE AACSB: Reflective Thinking AICPA: BB Critical Thinking AICPA: FN Measurement Accessibility: Keyboard Navigation Blooms: Understand Learning Objective: 02-01 Compute a predetermined overhead rate. Level of Difficulty: 3 Hard […]

Accounting Chapter 2 2 The Work Process Inventory Account Manufacturing

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 33. The Work in Process inventory account of a manufacturing Corporation shows a balance of $18,000 at the end of […]

Accounting Chapter 2 3 Epolito Corporation Incurred 87000 Actual Manufacturing

2-135 AICPA: BB Critical Thinking AICPA: FN Measurement Blooms: Apply Learning Objective: 02-04 Understand the flow of costs in a job-order costing system and prepare appropriate journal entries to record costs. Level of Difficulty: 1 Easy Topic Area: Computing Predetermined […]

Accounting Chapter 2 4 Cerrone Inc Has Provided The Following

2-155 67. A. $196,000 B. $184,000 C. $180,000 D. $188,000 Manufacturing overhead underapplied (overapplied) = Actual manufacturing overhead incurred – Manufacturing overhead applied = $71,000 – $67,000 = $4,000 underapplied Adjusted cost of goods sold = Beginning finished goods inventory […]

Accounting Chapter 2 5 The Direct Labor Rate For Brent

2-175 AICPA: BB Critical Thinking AICPA: FN Measurement Blooms: Apply Learning Objective: 02-02 Apply overhead cost to jobs using a predetermined overhead rate. Learning Objective: 02-04 Understand the flow of costs in a job-order costing system and prepare appropriate journal […]

Accounting Chapter 2 6 Echo Corporation Uses Joborder Costing System

2-195 106. A. $0 B. $63,000 C. $69,000 D. $6,000 There were no credits to the Manufacturing overhead account in August, only debits. AACSB: Analytical Thinking AICPA: BB Critical Thinking AICPA: FN Measurement Accessibility: Keyboard Navigation Blooms: Apply Learning Objective: […]

Accounting Chapter 2 7 Underapplied 700 Underapplied 400 Overapplied 3200

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. A. $1,900 underapplied B. $700 underapplied C. $400 overapplied D. $3,200 overapplied Manufacturing Overhead 2,600 6,800 3,000 1,900 Underapplied manufacturing […]

Accounting Chapter 2 8 Parker Company Uses Joborder Costing System

2-235 128. Estimated total manufacturing overhead = $624,520 + ($3.40 per machine-hour × 52,000 machine-hours) = $801,320 Predetermined overhead rate = $801,320 ÷ 52,000 machine-hours = $15.41 per machine- hour AACSB: Analytical Thinking AICPA: BB Critical Thinking AICPA: FN Measurement […]

Accounting Chapter 2 The completed schedule of costs in Work in Process

Problem 2-25A (continued) 5. The amount of overhead cost in Work in Process was: $24,000 direct materials cost × 160% = $38,400 The amount of direct labor cost in Work in Process is: Total ending work in process …………… $70,000 […]

Accounting Chapter 2 The first step is to estimate the total

Chapter 2 Job-Order Costing Solutions to Questions 2-1 By definition, manufacturing overhead consists of costs that cannot be practically traced to jobs. Therefore, if these costs are to be as- signed to jobs, they must be allocated rather than traced. […]

Accounting Chapter 2 The predetermined overhead rate and overhead

Teamwork in Action 1. The types of transactions that are posted to the accounts may be sum- marized in T-account form as follows: Raw Materials Beginning balance Purchases Direct materials used (to Work in Process) Accounts Payable Beginning balance Payments […]

Accounting Chapter 2 The types of transactions that are posted to the accounts

Exercise 2-14 (20 minutes) 1. The estimated total manufacturing overhead cost is computed as fol- lows: Y = $650,000 + ($3.00 per MH)(100,000 MHs) Estimated fixed manufacturing overhead ………………. $650,000 Estimated variable manufacturing overhead: $3.00 per MH × 100,000 MHs […]

Accounting Chapter 3 1 Facility-level activities are activities that

Chapter 03 Activity-Based Costing Answer Key True / False Questions 1. TRUE AACSB: Reflective Thinking AICPA: BB Critical Thinking AICPA: FN Measurement Accessibility: Keyboard Navigation Blooms: Remember Learning Objective: 03-01 Understand the basic approach in activity-based costing and how it […]

Accounting Chapter 3 10 Computation Activity Rates A B Estimated Total

3-483 Computation of activity rates: Activity Cost Pools (a) Estimated Overhead Cost (b) Total Expected Activity (a) ÷ (b) Activity Rate Labor-related $315,588 7,800 DLHs $40.46 per DLH Production orders $26,761 700 orders $38.23 per order General factory $630,800 9,500 […]

Accounting Chapter 3 11 The Direct Materials Cost Per Unit

3-503 A. $41.81 per DLH B. $15.23 per DLH C. $20.42 per DLH D. $29.00 per DLH Predetermined overhead rate = Estimated total overhead ÷ Total direct labor-hours = $238,331 ÷ 5,700 DLHs = $41.81 per DLH (rounded) AACSB: Analytical […]

Accounting Chapter 3 12 product o8 direct materials $298.90 direct labor

3-523 A. $949.18 per unit B. $1,415.62 per unit C. $1,343.14 per unit D. $1,176.22 per unit Predetermined overhead rate = Estimated total overhead ÷ Total direct labor-hours = $928,274 ÷ 12,900 DLHs = $71.96 per DLH (rounded) Computation of […]

Accounting Chapter 3 13 Computing Product Costs topic Area Shifting Overhead Cost topic

3-543 Unit product cost $1,951.54 AACSB: Analytical Thinking AICPA: BB Critical Thinking AICPA: FN Measurement Blooms: Apply Learning Objective: 03-02 Compute activity rates for an activity-based costing system. Learning Objective: 03-03 Compute product costs using activity-based costing. Level of Difficulty: […]

Accounting Chapter 3 14 The company is considering adopting an activity-based

3-563 145. Punches, Inc., manufactures and sells two products: Product H7 and Product Y2. Data concerning the expected production of each product and the expected total direct labor- hours (DLHs) required to produce that output appear below: Expected Production Direct […]

Accounting Chapter 3 15 The Unit Product Cost Product Under Traditional

3-583 153. Boutet, Inc., manufactures and sells two products: Product G5 and Product U1. Data concerning the expected production of each product and the expected total direct labor- hours (DLHs) required to produce that output appear below: Expected Production Direct […]

Accounting Chapter 3 16 estimated total activity overhead expected activity cost pools rate

3-603 A. $706.26 per unit B. $777.96 per unit C. $492.80 per unit D. $544.57 per unit Computation of activity rates: Activity Cost Pools (a) Estimated Overhead Cost (b) Total Expected Activity (a) ÷ (b) Activity Rate Labor-related $121,548 4,200 […]

Accounting Chapter 3 17 Product Activity Cost Pools And Activity Rates

3-623 Product S4 Activity Cost Pools and Activity Rates Expected Activity Amount Labor-related, at $32.69 per DLH 600 $19,614 Machine setups, at $67.85 per setup 500 33,925 General factory, $12.11 per MH 3,900 47,229 Total overhead costs assigned (a) $100,768 […]

Accounting Chapter 3 18 Product Would Closest To 48285 Per Unit

3-643 D. $81.50 per MH Activity rate = Estimated overhead cost ÷ Total expected activity = $709,050 ÷ 8,700 MHs = $81.50 per MH AACSB: Analytical Thinking AICPA: BB Critical Thinking AICPA: FN Measurement Blooms: Apply Learning Objective: 03-02 Compute […]

Accounting Chapter 3 19 Costs Topic Area Shifting Overhead Cost 3671

3-663 184. Mellencamp, Inc., manufactures and sells two products: Product A3 and Product Y6. Data concerning the expected production of each product and the expected total direct labor- hours (DLHs) required to produce that output appear below: Expected Production Direct […]

Accounting Chapter 3 2 Gerula, Inc., manufactures and sells two products

3-323 AICPA: BB Critical Thinking AICPA: FN Measurement Blooms: Apply Learning Objective: 03-02 Compute activity rates for an activity-based costing system. Level of Difficulty: 1 Easy Topic Area: Using Activity-Based Costing Copyright © 2016 McGraw-Hill Education. All rights reserved. No […]

Accounting Chapter 3 20 Costs Topic Area Using Activity based Costing 3693

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. c. Determine the unit product cost of each product under the activity-based costing method. 3-683 a. Computation of activity rates: […]

Accounting Chapter 3 21 The Company Considering Adopting Activity based Costing System

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Determine the unit product cost of each product under the activity-based costing method. Computation of activity rates: (a) (b) 3-703 […]

Accounting Chapter 3 22 Product Direct 23160 13280 Materials Direct

3-723 General factory,85.77 per MH 4,600 394,542 4,900 420,273 Total overhead costs assigned (a) $413,218 $443,345 Number of units produced (b) 100 200 Overhead cost per unit (a) ÷ (b) $4,132.18 $2,216.73 Computation of unit product costs under activity-based costing. […]

Accounting Chapter 3 23 Hours 080 Hour Unit Direct Materials

3-743 a. Predetermined overhead rate = Estimated total overhead ÷ Total direct labor-hours = $1,050,899 ÷ 11,800 DLHs = $89.06 per DLH (rounded) Computation of overhead applied to each product: Product S3 Product K2 Manufacturing overhead: Product S3: (8.0 DLHs […]

Accounting Chapter 3 24 Data concerning the expected production of each product and the expected

3-763 a. Predetermined overhead rate = Estimated total overhead ÷ Total direct labor-hours = $491,888 ÷ 4,800 DLHs = $102.48 per DLH (rounded) b. Computation of overhead applied to each product: Product P0 Product L5 Manufacturing overhead: Product P0: (6.0 […]

Accounting Chapter 3 25 Relative to the activity-based costing system, would Job

3-783 a. Predetermined overhead rate = Estimated total overhead ÷ Total direct labor-hours = $662,351 ÷ 5,200 DLHs = $127.38 per DLH (rounded) b. Computation of overhead applied to each product: Product M8 Product L9 Manufacturing overhead: In all computations […]

Accounting Chapter 3 26 the unit product cost of product i5 under traditional costing is less

3-800 Manufacturing overhead: Product W7: (5.0 DLHs ×168.64 per DLH) 843.20 Product I5: (2.0 DLHs ×168.64 per DLH) 337.28 Unit product cost $1,211.80 $601.38 Computation of activity rates: Activity Cost Pools (a) Estimated Overhead Cost (b) Total Expected Activity (a) […]

Accounting Chapter 3 3 Paparo Corporation Has Provided The Following

3-343 Product V9 Direct materials $176.90 Direct labor (5.0 DLHs × $27.40 per DLH) 137.00 Overhead 303.18 Unit product cost $617.08 AACSB: Analytical Thinking AICPA: BB Critical Thinking AICPA: FN Measurement Blooms: Apply Learning Objective: 03-02 Compute activity rates for […]

Accounting Chapter 3 4 Estimated Total A B Activity Cost Pools

3-363 Activity Cost Pools Estimated Overhead Cost Total Expected Activity (a) ÷ (b) Activity Rate Assembly $846,040 52,000 machine-hours $16.27 per machine-hour Processing orders $64,056 1,700 orders $37.68 per order Inspection $102,408 1,360 inspection-hours $75.30 per inspection-hour The overhead cost […]

Accounting Chapter 3 5 Hane Corporation Uses The Following Activity

3-383 A. The unit product cost of Product A8 under traditional costing is greater than its unit product under activity-based costing by $159.00. B. The unit product cost of Product A8 under traditional costing is greater than its unit product […]

Accounting Chapter 3 6 Contrast The Product Costs Computed Under Activity based

3-403 C. $457.83 per unit D. $772.56 per unit Predetermined overhead rate = Estimated total overhead ÷ Total direct labor-hours = $457,860 ÷ 9,000 DLHs = $50.87 per DLH (rounded) Product J9: 9.0 DLHs × $50.87 per DLH = $457.83 […]

Accounting Chapter 3 7 The activity rate for the Production Orders activity cost pool under

3-423 AACSB: Analytical Thinking AICPA: BB Critical Thinking AICPA: FN Measurement Blooms: Apply Learning Objective: 03-02 Compute activity rates for an activity-based costing system. Learning Objective: 03-03 Compute product costs using activity-based costing. Level of Difficulty: 2 Medium Topic Area: […]

Accounting Chapter 3 8 Angara Corporation Uses Activity based Costing Determine

3-443 93. Kamerling, Inc., manufactures and sells two products: Product H0 and Product Q8. Data concerning the expected production of each product and the expected total direct labor- hours (DLHs) required to produce that output appear below: Expected Production Direct […]

Accounting Chapter 3 9 Computation of unit product costs under activity-based costing

3-463 Level of Difficulty: 2 Medium Topic Area: Using Activity-Based Costing Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 3-464 103. Pachero, Inc., manufactures and sells two products: […]

Accounting Chapter 3 Activity Center A Estimated Overhead Costs Purchasing

Problem 3-18A (30 minutes) 1. The activity rates are computed as follows: Activity Cost Pool (a) Estimated Overhead Cost (b) Expected Activity (a) ÷ (b) Activity Rate Labor related ……… $35,000 7,000 DLHs $5 per DLH Production orders … $4,000 […]

Accounting Chapter 3 The Average Cost Per Diner Differs From

Exercise 3-9 (continued) 2. Activity costs are assigned to the two hospitals as follows: City General: Activity Cost Pool (a) Activity Rate (b) Activity (a) × (b) ABC Cost Customer deliveries …………. $80.00 per delivery 10 deliveries $ 800 Manual […]

Accounting Chapter 3 The president was probably correct in being concerned

Analytical Thinking (continued) 2. The unit product cost of each product under activity-based costing is given below. For comparison, the costs computed by the company’s accounting department using conventional costing are also provided. Activity-Based Costing Direct Labor-Hour Base Standard Specialty […]

Accounting Chapter 4 1 Compute the equivalent units of production using the weighted-average

Chapter 04 Process Costing Answer Key True / False Questions 1. TRUE AACSB: Reflective Thinking AICPA: BB Critical Thinking AICPA: FN Measurement Accessibility: Keyboard Navigation Blooms: Remember Learning Objective: 04-01 Record the flow of materials, labor, and overhead through a […]

Accounting Chapter 4 10 Conversion Units Completed And Transferred Out Units

4-272 Conversion Units completed and transferred out: Units transferred to the next department (a) 140,000 Cost per equivalent unit (b) $1.45 Cost of units completed and transferred out (a) × (b) $203,000 AACSB: Analytical Thinking AICPA: BB Critical Thinking AICPA: […]

Accounting Chapter 4 2 Jimmy Corporation Uses The Weightedaverage Method

4-116 33. A. $4.176 B. $4.600 C. $3.375 D. $4.421 Weighted-average method Conversion Units transferred to the next department 61,000 Ending work in process: Conversion: 14,000 units × 10% 1,400 Equivalent units of production 62,400 Conversion Cost of beginning work […]

Accounting Chapter 4 3 Arizaga Corporation Manufactures Canoes Two Departments

4-136 46. A. 6,160 B. 6,380 C. 6,920 D. 7,240 Weighted-average method Equivalent units of production = Units transferred to the next department or to finished goods + Equivalent units in ending work in process inventory = 6,700 + 1.00 […]

Accounting Chapter 4 4 Lumb Corporation Uses The Weighted average Method

4-156 57. Ibarra Corporation uses the weighted-average method in its process costing system. Data concerning the first processing department for the most recent month are listed below: Beginning work in process inventory: Units in beginning work in process inventory 800 […]

Accounting Chapter 4 5 units in process 30,000 percent complete with respect to materials

4-176 67. Lumb Corporation uses the weighted-average method in its process costing system. Data concerning the first processing department for the most recent month are listed below: Beginning work in process inventory: Units in beginning work in process inventory 200 […]

Accounting Chapter 4 6 What are the equivalent units for conversion costs for the

4-196 77. Guo Corporation uses the weighted-average method in its process costing system. This month, the beginning inventory in the first processing department consisted of 500 units. The costs and percentage completion of these units in beginning inventory were: Cost […]

Accounting Chapter 4 7 Ending Work Process Materials 1500 Units 50

4-216 Ending work in process: Materials: 1,500 units × 50% 750 Conversion: 1,500 units × 30% 450 Equivalent units of production 5,150 4,850 Materials Conversion Cost of beginning work in process inventory $8,000 $7,800 Costs added during the period 90,300 […]

Accounting Chapter 4 8 Units Transferred The Next Department 8700 8700

4-236 Units transferred to the next department 8,700 8,700 Ending work in process: Materials: 700 units × 85% 595 Conversion: 700 units × 20% 140 Equivalent units of production 9,295 8,840 Materials Conversion Cost of beginning work in process inventory […]

Accounting Chapter 4 9 Determine The Cost Per Equivalent Unit For

4-256 108. Carver Inc. uses the weighted-average method in its process costing system. The following data concern the operations of the company’s first processing department for a recent month. Work in process, beginning: Units in process 700 Percent complete with […]

Accounting Chapter 4 Computation Equivalent Units Required Complete The Beginning

Exercise 4-10 (10 minutes) Weighted-Average Method Materials Labor & Overhead during July* ……………………………………………… 377,000 377,000 Work in process, July 31: Materials: 25,000 pounds × 100% complete ……. 25,000 Labor and overhead: 25,000 pounds × 60% complete …………………. 15,000 Equivalent units […]

Accounting Chapter 4 Gary Stevens Would Like The Estimated Percentage

Problem 4-15A (45 minutes) Weighted-Average Method 1. Equivalent units of production: Materials Conversion Transferred to next department …………………… 160,000 160,000 Ending work in process: Materials: 40,000 units x 100% complete ……. 40,000 Conversion: 40,000 units x 25% complete …… 10,000 […]

Accounting Chapter 4 Job-order costing and process costing have

Chapter 4 Process Costing Solutions to Questions 4-1 A process costing system should be used in situations where a homogeneous product is produced on a continuous basis in large quantities. 4-2 Job-order and processing costing are similar in the following […]

Accounting Chapter 4 The Second Step Record The Cost Per

to illustrate the weighted-average method. 1. Assume the following activity, as shown on the slide, is reported in the Assembly Department for the month of June. 4 Chapter 4 Process Costing I. Supplement: FIFO method (slide 1: title slide) A. […]

Accounting Chapter 4s 1 Fifo Method level Difficulty Medium topic Area Equivalent Units

Chapter 04 Supplement: Process Costing Using the FIFO Method Answer Key True / False Questions 1. FALSE AACSB: Reflective Thinking AICPA: BB Critical Thinking AICPA: FN Measurement Accessibility: Keyboard Navigation Blooms: Understand Learning Objective: 04-02 Compute the equivalent units of […]

Accounting Chapter 4s 2 Williams Corporation Uses The Fifo Method

4S-87 21. Qart Corporation uses the FIFO method in its process costing system. Operating data for the Cutting Department for the month of March appear below: Units Percent Complete with Respect to Conversion Beginning work in process inventory 4,500 20% […]

Accounting Chapter 4s 3 Conversion to Complete Beginning Work Process Inventory materials 9000

4S-107 Equivalent units of production 119,100 AACSB: Analytical Thinking AICPA: BB Critical Thinking AICPA: FN Measurement Blooms: Apply Learning Objective: 04-02 Compute the equivalent units of production using the weighted-average method. Level of Difficulty: 1 Easy Topic Area: Compute and […]

Accounting Chapter 4s 4 Reid Corporation Uses Process Costing System

4S-127 Conversion: 5,000 units 70% 3,500 Equivalent units of production 48,000 50,500 AACSB: Analytical Thinking AICPA: BB Critical Thinking AICPA: FN Measurement Blooms: Apply Learning Objective: 04S-06 Compute the equivalent units of production using the FIFO method. Level of […]

Accounting Chapter 4s 5 Data concerning the first processing department for the most recent

4S-147 52. Quilling Corporation uses the FIFO method in its process costing system. Data concerning the first processing department for the most recent month are listed below: Beginning work in process inventory: Units in beginning work in process inventory 600 […]

Accounting Chapter 4s 6 April One The Processing Departments Salatino

4S-167 Units in beginning work in process inventory = 4,800 – 300 = 4,500 Materials Conversion To complete beginning work in process: Materials: 300 units (100% – 85%) 45 Conversion: 300 units (100% – 20%) 240 Units started […]

Accounting Chapter 4s 7 determine the equivalent units of production

4S-187 71. The following data pertain to the Milling Department of Vario Corporation for July. The company uses the FIFO method in its process costing. Percent Complete Units Materials Conversion Work in process, July 1 800 60% 25% Units started […]

Accounting Chapter 4s 8 Rauls Corporation Uses The Fifo Method

4S-200 Topic Area: Equivalent Units – FIFO Method Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution […]

Accounting Chapter 5 1 Education25garth Corporation Sells Single Product The Selling

Chapter 05 Cost-Volume-Profit Relationships Answer Key True / False Questions 1. TRUE AACSB: Analytical Thinking AICPA: BB Critical Thinking AICPA: FN Measurement Accessibility: Keyboard Navigation Blooms: Understand Learning Objective: 05-01 Explain how changes in activity affect contribution margin and net […]

Accounting Chapter 5 10 Gauani Corporation Produces And Sells Single

5-282 175. Gauani Corporation produces and sells a single product. Data concerning that product appear below: Selling price per unit $150.00 Variable expense per unit $42.00 Fixed expense per month $421,200 Required: a. Assume the company’s monthly target profit is […]

Accounting Chapter 5 2 Maack Corporations Contribution Margin Ratio 16

5-126 38. A. $207,160 B. $3,840 C. $255,000 D. $47,840 Profit = (CM ratio × Sales) – Fixed expenses = (0.16 × $299,000) – $44,000 = $47,840 – $44,000 = $3,840 AACSB: Analytical Thinking AICPA: BB Critical Thinking AICPA: FN […]

Accounting Chapter 5 3 Data Concerning Bunck Corporations Single Product

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 54. Data concerning Bunck Corporation’s single product appear below: Per Unit Percent of Sales Selling price $170 100% Variable expenses […]

Accounting Chapter 5 4 Palomo Corporation Sells Product For 170

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 75. A. 6,000 units B. 3,750 units C. 15,000 units D. 10,000 units Unit sales to attain a target profit […]

Accounting Chapter 5 5 Grisham Corporation Produces And Sells Single

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 96. Grisham Corporation produces and sells a single product. The company has provided its contribution format income statement for February. […]

Accounting Chapter 5 6 This question is to be considered independently of all other questions relating

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 113. A manufacturer of tiling grout has supplied the following data: Kilograms produced and sold 300,000 Sales revenue $1,950,000 Variable […]

Accounting Chapter 5 7 Moccio Enterprises Inc Produces And Sells

5-226 AICPA: FN Measurement Blooms: Apply Learning Objective: 05-04 Show the effects on net operating income of changes in variable costs, fixed costs, selling price, and volume. Level of Difficulty: 1 Easy Topic Area: CVP Relationships in Graphic Form Copyright […]

Accounting Chapter 5 8 The July Contribution Format Income Statement

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 143. Mcallister Corporation has provided the following data concerning its only product: Selling price $150 per unit Current sales 39,900 […]

Accounting Chapter 5 9 The marketing manager has proposed a commission of $20 per unit

5-266 162. Data concerning Ulwelling Corporation’s single product appear below: Per Unit Percent of Sales Selling price $170 100% Variable expenses 51 30% Contribution margin $119 70% New contribution margin ($119 per unit – $11 per unit) $108 New unit […]

Accounting Chapter 5 Decrease Line Breakeven Point Have Flatter

Problem 5-28A (continued) 2. The sales mix has shifted over the last year from Standard sets to Deluxe sets. This shift has caused a decrease in the company’s overall CM ratio from 54.2% in April to 47.1% in May. For […]

Accounting Chapter 5 It would be natural for managers to interpret

Analytical Thinking (continued) Allocation of common fixed expenses on the basis of sales revenue: Velcro Metal Nylon Total Sales …………………………….. $165,000 $300,000 $340,000 $805,000 Percentage of total sales …… 20.497% 37.267% 42.236% 100.0% Allocated common fixed expense* …………………….. $49,193 $ […]

Accounting Chapter 5 This problem illustrates the difficulty faced

Problem 5-20A (continued) c. This problem illustrates the difficulty faced by some companies. When variable labor costs increase, it is often difficult to pass these cost increases along to customers in the form of higher prices. Thus, companies are forced […]

Accounting Chapter 5 Incremental analysis focuses on the changes

Chapter 5 Cost-Volume-Profit Relationships Solutions to Questions 5-1 The contribution margin (CM) ratio is the ratio of the total contribution margin to total sales revenue. It can also be expressed as the ratio of the contribution margin per unit to […]

Accounting Chapter 6 1 Which The Following Statements Not correct a Under Variable

Chapter 06 Variable Costing and Segment Reporting: Tools for Management Answer Key True / False Questions 1. TRUE AACSB: Reflective Thinking AICPA: BB Critical Thinking AICPA: FN Measurement Accessibility: Keyboard Navigation Blooms: Remember Learning Objective: 06-01 Explain how variable costing […]

Accounting Chapter 6 10 The Following Data Were Provided Rider

6-359 Learning Objective: 06-03 Reconcile variable costing and absorption costing net operating incomes and explain why the two amounts differ. Level of Difficulty: 3 Hard Topic Area: Overview of Variable and Absorption Costing Topic Area: Segmented Income Statements and the […]

Accounting Chapter 6 11 Kosco Corporation Produces Single Product The

6-379 150. Kosco Corporation produces a single product. The company’s absorption costing income statement for March follows: Kosco Corporation Income Statement For the Month Ended March 31 Sales (2,400 units) $48,000 Cost of goods sold 24,000 Gross margin 24,000 Selling […]

Accounting Chapter 6 12 Education 173 one ill Incorporated’s Segmented Income Statement For The

6-399 166. Higgins Corporation sells three products, Product A, Product B, and Product C. Data concerning the company’s most recent month of operations, June, appear below: Products Total Company A B C Sales $1,500,000 $750,000 $450,000 $300,000 Variable expenses $450,000 […]

Accounting Chapter 6 13 Western Divisions Breakeven Sales Closest Toa 266255b

6-419 Blooms: Apply Learning Objective: 06-04 Prepare a segmented income statement that differentiates traceable fixed costs from common fixed costs and use it to make decisions. Level of Difficulty: 1 Easy Topic Area: Segmented Income Statements: Break-Even Analysis 180. Data […]

Accounting Chapter 6 14 Redstone Corporation Produces Single Product And

6-439 199. Criblez Corporation has two divisions: Blue Division and Gold Division. The following report is for the most recent operating period: Total Company Blue Division Gold Division Sales $431,000 $106,000 $325,000 Variable expenses 154,810 54,060 100,750 Contribution margin 276,190 […]

Accounting Chapter 6 15 Italia Espresso Machina Inc Produces Single

6-459 Variable costing income statement Sales ($108 per unit × 900 units) $97,200 Variable expenses: Variable cost of goods sold ($65 per unit × 900 units) $58,500 Variable selling and administrative ($11 per unit × 900 units) 9,900 68,400 Contribution […]

Accounting Chapter 6 16 Hanks Corporation Produces Single Product Operating

6-479 Direct materials $190.00 Direct labor 40.00 Variable manufacturing overhead 25.00 Fixed manufacturing overhead ($250,000 ÷ 20,000 units) 12.50 Total cost per unit $267.50 Cost per unit under variable costing: Direct materials $190.00 Direct labor 40.00 Variable manufacturing overhead 25.00 […]

Accounting Chapter 6 17 Prepare a segmented income statement that differentiates

6-496 Level of Difficulty: 1 Easy Topic Area: Segmented Income Statements: Break-Even Analysis 228. Data for March concerning Mauger Corporation’s two major business segments-Fibers and Feedstocks-appear below: Sales revenues, Fibers $560,000 Sales revenues, Feedstocks $810,000 Variable expenses, Fibers $235,000 Variable […]

Accounting Chapter 6 2 Manufacturing Company That Produces Single Product

6-199 Level of Difficulty: 1 Easy Topic Area: Variable Costing Contribution Format Income Statement costs. 45. Sharron Inc., which produces a single product, has provided the following data for its most recent month of operations: Number of units produced 3,000 […]

Accounting Chapter 6 3 Rede Inc Manufactures Single Product Variable

6-219 Variable costing unit product cost $68 Variable costing income statement Sales (3,000 units sold × $126 per unit) $378,000 Variable expenses: Variable cost of goods sold (3,000 units sold × $68 per unit) $204,000 Variable selling and administrative (3,000 […]

Accounting Chapter 6 4 Insider Corporation Has Two Divisions And

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 71. Insider Corporation has two divisions, J and K. During March, the contribution margin in Division J was $30,000. The […]

Accounting Chapter 6 5 Delvin Corporation Which Has Only One

6-259 AICPA: FN Measurement Blooms: Apply Learning Objective: 06-05 Compute companywide and segment break-even points for a company with traceable fixed costs. Level of Difficulty: 1 Easy Topic Area: Variable Costing Contribution Format Income Statement Copyright © 2016 McGraw-Hill Education. […]

Accounting Chapter 6 6 Peterson Corporation Produces Single Product Data

6-279 = ($3 per unit × Units in ending inventory) – ($3 per unit × Units in beginning inventory) = $3 per unit × (Units in ending inventory – Units in beginning inventory) = $3 per unit × (15,000 units […]

Accounting Chapter 6 7 Hatfield Corporation Which Has Only One

6-299 106. Hatfield Corporation, which has only one product, has provided the following data concerning its most recent month of operations: Selling price $123 Units in beginning inventory 0 Units produced 6,400 Units sold 6,100 Units in ending inventory 300 […]

Accounting Chapter 6 8 Aaker Corporation Which Has Only One

6-319 116. Aaker Corporation, which has only one product, has provided the following data concerning its most recent month of operations: Selling price $99 Units in beginning inventory 0 Units produced 6,300 Units sold 6,000 Units in ending inventory 300 […]

Accounting Chapter 6 9 Elliot Corporation Which Has Only One

6-339 126. Elliot Corporation, which has only one product, has provided the following data concerning its most recent month of operations: Selling price $112 Units in beginning inventory 0 Units produced 4,900 Units sold 4,500 Units in ending inventory 400 […]

Accounting Chapter 6 The Finished Goods inventory account should be

Exercise 6-11 (20 minutes) 1. Division Total Company East Central West Sales ………………………… $1,000,000 $250,000 $400,000 $350,000 Variable expenses ……….. 390,000 130,000 120,000 140,000 Contribution margin …….. 610,000 120,000 280,000 210,000 Traceable fixed expenses . 535,000 160,000 200,000 175,000 Divisional […]

Accounting Chapter 6 The intern’s decision to use the absorption format

Problem 6-23A (60 minutes) 1. a. Absorption costing unit product cost is: Direct materials ……………………………. $ 3.50 Direct labor …………………………………. 12.00 Variable manufacturing overhead …….. 1.00 Fixed manufacturing overhead ($300,000 ÷ 30,000 units) …………… 10.00 Absorption costing unit product cost […]

Accounting Chapter 6 Absorption and variable costing differ in how

Chapter 6 Variable Costing and Segment Reporting: Tools for Management Solutions to Questions 6-1 Absorption and variable costing differ in how they handle fixed manufacturing overhead. Under absorption costing, fixed manufacturing overhead is treated as a product cost and hence […]

Accounting Chapter 6 The correct treatment of the occupancy

Analytical Thinking (continued) 2. a. No, the cookbook line should not be eliminated. The cookbook is covering all of its own costs and is generating an $18,000 segment margin toward covering the company’s common costs and toward profits. (Note: Problems […]

Accounting Chapter 7 1 The Following Are Considered Benefits Participative

Chapter 07 Master Budgeting Answer Key True / False Questions 1. FALSE AACSB: Reflective Thinking AICPA: BB Critical Thinking AICPA: FN Measurement Accessibility: Keyboard Navigation Blooms: Remember Learning Objective: 07-01 Understand why organizations budget and the processes they use to […]

Accounting Chapter 7 2 Mutskic Corporation Produces And Sells Product

7-101 47. A. 28,500 B. 31,500 C. 30,000 D. 36,500 November Budgeted unit sales 30,000 Add desired ending finished goods inventory 6,500 Total needs 36,500 Less beginning finished goods inventory 8,000 Required production in units 28,500 AACSB: Analytical Thinking AICPA: […]

Accounting Chapter 7 3 Vandel Inc Bases Its Selling And

7-121 68. A. $191,400 B. $118,800 C. $64,020 D. $182,820 Selling and Administrative Expense Budget: December Budgeted unit sales 6,600 Variable selling and administrative expense per unit $9.70 Variable selling and administrative expense $64,020 Fixed selling and administrative expense 127,380 […]

Accounting Chapter 7 4 The Following Are Budgeted Data For

7-141 86. Dilbert Farm Supply is located in a small town in the rural west. Data regarding the store’s operations follow: o Sales are budgeted at $260,000 for November, $230,000 for December, and $210,000 for January. o Collections are expected […]

Accounting Chapter 7 5 Sarter Corporation The Process Preparing Its

7-161 100. May Corporation, a merchandising firm, has budgeted sales as follows for the third quarter of the year: July $80,000 August $90,000 September $70,000 A. $52,000 B. $63,050 C. $47,450 D. $91,050 Merchandise Purchases Budget: July Budgeted cost of […]

Accounting Chapter 7 6 if the total budgeted selling and administrative expense for October

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. AICPA: BB Critical Thinking AICPA: FN Measurement Accessibility: Keyboard Navigation Blooms: Apply Learning Objective: 07-05 Prepare a direct labor budget. […]

Accounting Chapter 7 7 Carter Lumber Sells Lumber And General

7-201 145. A. $18,000 B. $0 C. $50,000 D. $82,000 Beginning cash balance $40,000 Add cash receipts 150,000 Total cash available 190,000 Less cash disbursements 158,000 Excess (deficiency) of cash available over disbursements 32,000 Financing (plug figure) 18,000 Ending cash […]

Accounting Chapter 7 8 Chow Corporation Manufactures Childrens Chairs Made

7-221 Liabilities and Stockholders’ Equity Accounts payable $235,300 Common stock 640,000 Retained earnings 554,600 Total liabilities and stockholders’ equity $1,429,900 AACSB: Analytical Thinking AICPA: BB Critical Thinking AICPA: FN Measurement Blooms: Apply Learning Objective: 07-02 Prepare a sales budget, including […]

Accounting Chapter 7 Case Continued Earrings Unlimited Budgeted Balance Sheet

Ethics Challenge (continued) It would take tremendous courage for Keri to take the problem all the way up to Stokes himself—particularly in view of his less-than-humane treatment of subordinates. And going to the Board of Directors is unlikely to work […]

Accounting Chapter 7 December Cash Sales Collections Account October

Exercise 7-13 (30 minutes) 1. Schedule of expected cash collections: Month July August September Quarter From accounts receivable . $136,000 $136,000 From July sales: 45% × 210,000 ………… 94,500 94,500 55% × 210,000 ………… $115,500 115,500 From August sales: 45% […]

Accounting Chapter 7 Employees are able to blend personal and organizational

Problem 7-24A (45 minutes) 1. a. The reasons that Marge Atkins and Pete Granger use budgetary slack include the following: • These employees are hedging against the unexpected (reducing uncertainty/risk). • The use of budgetary slack allows employees to exceed […]

Accounting Chapter 7 The Cash Budget Detailed Plan Showing How

Chapter 7 Lecture Notes 1 Chapter 7 Lecture Notes Chapter theme: This chapter describes how organizations define their financial goals by preparing numerous budgets I. The basic framework of budgeting Learning Objective 7-1: Understand why organizations budget and the processes […]

Accounting Chapter 7 Total liabilities and stockholders’ equity

Exercise 7-5 (15 minutes) 1. Yuvwell Corporation Manufacturing Overhead Budget 1st Quarter 2nd Quarter 3rd Quarter 4th Quarter Year Budgeted direct labor-hours ………………………….. 8,000 8,200 8,500 7,800 32,500 Variable manufacturing overhead rate …………….. × $2.00 × $2.00 × $2.00 × […]

Accounting Chapter 7 Budgets force managers to think about and plan

Chapter 7 Master Budgeting Solutions to Questions 7-1 A budget is a detailed quantitative plan for the acquisition and use of financial and other resources over a given time period. Budgetary control involves using budgets to increase the likelihood that […]

Accounting Chapter 7 Tell the students that the inventory purchases

Chapter 7 Lecture Notes 12 4. The fourth step is to calculate the materials to be purchased for May (221,500 pounds). Notice: a. April’s desired ending inventory becomes May’s beginning inventory. 5. The fifth step is to calculate the materials […]

Accounting Chapter 8 1 Quantity Standard Indicates How Much Output

Chapter 08 Flexible Budgets, Standard Costs, and Variance Analysis Answer Key True / False Questions 1. FALSE AACSB: Reflective Thinking AICPA: BB Critical Thinking AICPA: FN Measurement Accessibility: Keyboard Navigation Blooms: Remember Learning Objective: 08-01 Prepare a flexible budget. Level […]

Accounting Chapter 8 10 For The Month July The Company Planned

8-621 151. Letts Corporation manufactures and sells a single product. The company uses units as the measure of activity in its budgets and performance reports. During January, the company budgeted for 7,000 units, but its actual level of activity was […]

Accounting Chapter 8 11 Tabeling Corporation manufactures and sells a single product

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. A. $22,144 B. $21,104 C. $22,140 D. $21,049 Cost = Fixed cost + (Variable cost per unit × q) = […]

Accounting Chapter 8 12 The kennel has provided the following data concerning the formulas

8-661 178. Juenemann Kennel uses tenant-days as its measure of activity; an animal housed in the kennel for one day is counted as one tenant-day. During December, the kennel budgeted for 3,800 tenant-days, but its actual level of activity was […]

Accounting Chapter 8 13 Selling and administrative expenses 21,2000.80

8-681 188. Linscott Corporation manufactures and sells a single product. The company uses units as the measure of activity in its budgets and performance reports. During July, the company budgeted for 5,400 units, but its actual level of activity was […]

Accounting Chapter 8 14 Kari Kennel Uses Tenant days Its Measure Activity

8-701 198. Perla Kennel uses tenant-days as its measure of activity; an animal housed in the kennel for one day is counted as one tenant-day. During March, the kennel budgeted for 2,200 tenant-days, but its actual level of activity was […]

Accounting Chapter 8 15 Coderre Corporation manufactures and sells a single product.

8-721 208. Wesolick Clinic uses client-visits as its measure of activity. During August, the clinic budgeted for 2,900 client-visits, but its actual level of activity was 2,870 client-visits. The clinic has provided the following data concerning the formulas used in […]

Accounting Chapter 8 16 Privett Hospital bases its budgets on patient-visits.

8-741 218. Smithj Kennel uses tenant-days as its measure of activity; an animal housed in the kennel for one day is counted as one tenant-day. During February, the kennel budgeted for 3,500 tenant-days, but its actual level of activity was […]

Accounting Chapter 8 17 Difficulty Easy topic Area Flexible Budgets With Multiple

8-761 228. Hagel Clinic uses client-visits as its measure of activity. During July, the clinic budgeted for 2,300 client-visits, but its actual level of activity was 2,320 client-visits. The clinic has provided the following data concerning the formulas used in […]

Accounting Chapter 8 18 Blaster Inc Manufactures Portable Radios Each

8-781 243. Canevari Corporation makes a product that uses a material with the following standards: Standard quantity 3.0 kilos per unit Standard price $2.00 per kilo Standard cost $6.00 per unit A. $360 F B. $410 U C. $410 F […]

Accounting Chapter 8 19 Variable overhead is assigned to blood tests on the basis

Copyright © 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 259. A. $22,960 Unfavorable B. $22,400 Unfavorable C. $9,600 Unfavorable D. $9,840 Unfavorable SQ = 6,000 units × 4.0 gallons […]

Accounting Chapter 8 2 Dehnert Midwifery’s Cost Formula For Its

8-461 43. Akey Hospital bases its budgets on patient-visits. The hospital’s static budget for March appears below: Budgeted number of patient-visits 2,700 Budgeted variable overhead costs: Supplies (@ $3.90 per patient-visit) $10,530 Laundry (@ $9.70 per patient-visit) 26,190 Total variable […]

Accounting Chapter 8 20 Standard Quantity or Hours Standard Price or Rate Direct materials 7.9

8-821 AICPA: FN Measurement Blooms: Apply Learning Objective: 08-05 Compute the direct labor rate and efficiency variances and explain their significance. Level of Difficulty: 1 Easy Topic Area: Using Standard Costs – Direct Labor Variances Copyright © 2014 McGraw-Hill Education. […]

Accounting Chapter 8 21 Variable manufacturing overhead costs are applied to products on

8-841 = $1,000 U AACSB: Analytical Thinking AICPA: BB Critical Thinking AICPA: FN Measurement Blooms: Apply Learning Objective: 08-04 Compute the direct materials price and quantity variances and explain their significance. Level of Difficulty: 1 Easy Topic Area: Using Standard […]

Accounting Chapter 8 22 The direct materials purchases variance is computed

8-861 293. Galla Corporation makes a product with the following standard costs: Standard Quantity or Hours Standard Price or Rate Standard Cost Per Unit Direct materials 8.2 pounds $7.00 per pound $57.40 Direct labor 0.4 hours $20.00 per hour $8.00 […]

Accounting Chapter 8 23 A total of 8,000 pounds of material were purchased

8-881 Blooms: Apply Learning Objective: 08-05 Compute the direct labor rate and efficiency variances and explain their significance. Level of Difficulty: 1 Easy Topic Area: Using Standard Costs – Direct Labor Variances 306. Epley Corporation makes a product with the […]

Accounting Chapter 8 24 Raw materials used in 12,820 ounces production Actual direct

8-901 AICPA: BB Critical Thinking AICPA: FN Measurement Blooms: Apply Learning Objective: 08-04 Compute the direct materials price and quantity variances and explain their significance. Level of Difficulty: 2 Medium Topic Area: Using Standard Costs – Direct Materials Variances Copyright […]

Accounting Chapter 8 25 The labor rate variance for May is $225

8-921 A. $316 F B. $294 F C. $316 U D. $294 U Variable overhead rate variance = AH × (AR − SR) = 3,160 hours × ($5.10 per hour − $5.00 per hour) = 3,160 hours × ($0.10 per […]

Accounting Chapter 8 26 What is the variable overhead efficiency variance for the month?

8-941 345. A manufacturing company that has only one product has established the following standards for its variable manufacturing overhead. Variable manufacturing overhead standards are based on machine-hours. Standard hours per unit of output 8.1 machine- hours Standard variable overhead […]

Accounting Chapter 8 27 Education 366 during July Heron Corporation Plans Serve 23000

8-961 359. Sinopoli Corporation bases its budgets on machine-hours. The company’s static planning budget for September appears below: Budgeted number of machine-hours 8,500 Budgeted variable costs: Supplies (@ $1.50 per machine-hour) $12,750 Power (@ $3.30 per machine-hour) 28,050 Budgeted fixed […]

Accounting Chapter 8 28 During May, Cockrel Corporation plans to serve 34,000

8-981 Level of Difficulty: 1 Easy Topic Area: Flexible Budgets 373. Oshell Clinic Flexible Budget For the Month Ended February 28 Actual patient-visits (q) 3,200 Revenue ($28.80q) $92,160 Expenses: Personnel expenses ($22,500 + $9.90q) 54,180 Medical supplies ($1,200 + $4.70q) […]

Accounting Chapter 8 29 Prepare Report Showing Revenue And Spending Variances level

8-1001 383. Halm Urban Diner is a charity supported by donations that provides free meals to the homeless. The diner’s budget for August was based on 3,000 meals. The diner’s director has provided the following cost data to use in […]

Accounting Chapter 8 3 Gershon Air Uses Two Measures Activity

8-481 63. A. $312 F B. $312 U C. $43 F D. $43 U Actual results $5,830 Flexible budget [$210 + ($86 × 28) + ($15 × 217)] 5,873 Spending variance $43 Because the actual expense is less than the […]

Accounting Chapter 8 30 Cosme Tech Revenue and Spending Variances For the Month

8-1021 Occupancy expenses ($9,500 + $2.40q) 14,470 14,300 170 U Administrative expenses ($3,800 + $0.10q) 3,960 4,000 40 F Total expense 95,280 96,500 1,220 F Net operating income $1,350 $900 $450 F AACSB: Analytical Thinking AICPA: BB Critical Thinking AICPA: […]