Problem 4-15A (45 minutes)

Weighted-Average Method

1.

Equivalent units of production:

Materials

Conversion

Transferred to next department ……………………

160,000

Ending work in process:

Equivalent units of production ……………………..

2.

Cost per Equivalent Unit

Materials

Conversion

Cost of beginning work in process …………….

Cost added during the period …………………..

Total cost (a) ……………………………………….

Equivalent units of production (b) …………….

170,000

Cost per equivalent unit, (a) ÷ (b) ……………

3.

Applying costs to units:

Materials

Conversion

Total

Ending work in process inventory:

Equivalent units of production

40,000

10,000

$15,500

Units completed and transferred out:

160,000

Problem 4-15A (continued)

4.

Cost reconciliation:

Costs to be accounted for:

Costs added to production during the period

Costs accounted for as follows:

Cost of beginning work in process inventory

Problem 4-16A (45 minutes)

Weighted-Average Method

1.

Equivalent units of production

Materials

Conversion

Transferred to next department* ………………….

95,000

95,000

Ending work in process:

Equivalent units of production ……………………..

2.

Cost per equivalent unit

Materials

Conversion

Cost of beginning work in process …………….

Cost added during the period …………………..

Total cost (a) ……………………………………….

Equivalent units of production (b) …………….

98,000

Cost per equivalent unit, (a) ÷ (b) ……………

$1.50

$1.00

3.

Cost of ending work in process inventory and units transferred out

Materials

Conversion

Total

Ending work in process inventory:

Equivalent units of production…

9,000

3,000

Cost per equivalent unit ………..

$1.50

$1.00

$3,000

Units completed and transferred out:

95,000

Cost per equivalent unit ………..

$1.50

$1.00

$95,000

Problem 4-16A (continued)

4.

Cost Reconciliation

Costs to be accounted for:

Costs added to production during the period

Costs accounted for as follows:

Cost of beginning work in process inventory

Problem 4-17A (45 minutes)

Weighted-Average Method

1.

a.

Work in Process—Refining Department ………

495,000

Work in Process—Blending Department ……..

115,000

Raw Materials ………………………………….

610,000

b.

Work in Process—Refining Department ………

72,000

Work in Process—Blending Department ……..

18,000

Salaries and Wages Payable ……………….

Manufacturing Overhead ………………………..

Accounts Payable ……………………………..

225,000

d.

Work in Process—Refining Department ………

181,000

Manufacturing Overhead ……………………

181,000

d.

Work in Process—Blending Department ……..

42,000

Manufacturing Overhead ……………………

42,000

Work in Process—Blending Department ……..

740,000

Work in Process—Refining Department …

740,000

Finished Goods …………………………………….

Work in Process—Blending Department …

950,000

g.

Accounts Receivable ………………………………

Sales ……………………………………………..

Cost of Goods Sold ………………………………..

Finished Goods ………………………………..

900,000

Problem 4-17A (continued)

2.

Accounts Receivable

Raw Materials

(g)

1,500,000

Bal.

618,000

(a)

610,000

Bal.

8,000

Work in Process

Refining Department

Work in Process

Blending Department

(a)

495,000

(a)

(b)

(b)

(d)

181,000

(d)

Bal.

46,000

(e)

Bal.

Finished Goods

Manufacturing Overhead

Bal.

20,000

(g)

900,000

(c)

225,000

(d)

223,000

(f)

950,000

Bal.

2,000

Bal.

70,000

Accounts Payable

(c)

225,000

(b)

(g)

1,500,000

(g)

Problem 4-18A (30 minutes)

Weighted-Average Method

1.

Equivalent units of production

Materials

Conversion

Transferred to next department ……………………

190,000

190,000

Ending work in process:

Equivalent units of production ……………………..

2.

Cost per equivalent unit

Materials

Conversion

Cost of beginning work in process …………….

$ 67,800

$ 30,200

Cost added during the period …………………..

Total cost (a) ……………………………………….

Equivalent units of production (b) …………….

220,000

214,000

Cost per equivalent unit, (a) ÷ (b) ……………

3.

Total units transferred …………………………...

190,000

Less units in the beginning inventory …………

30,000

Units started and completed during April ……

4. No, the manager should not be rewarded for good cost control. The

Mixing Department’s low unit cost for April occurred because the costs

Analytical Thinking (45 minutes)

Weighted-Average Method

1. The revised computations follow:

Equivalent Units of Production:

Transferred

In Costs

Materials

Conversion

Transferred to finished goods ……………………………..

1,800

1,800

1,800

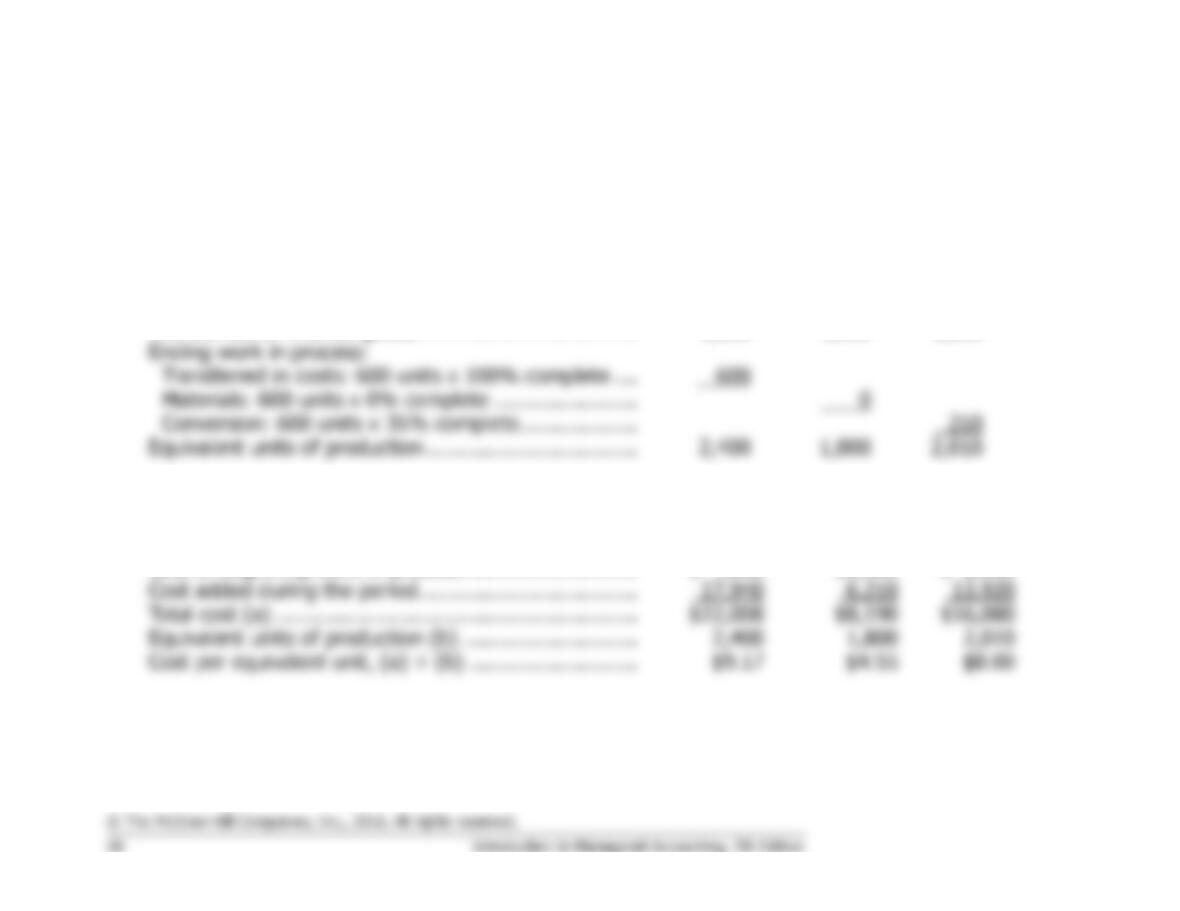

Ending work in process:

Equivalent units of production …………………………….

2,400

1,800

2,010

Cost per Equivalent Unit:

Transferred

In Costs

Materials

Conversion

Cost of beginning work in process ……………………….

$ 4,068

$1,980

$ 2,160

Cost added during the period ……………………………..

Total cost (a) ………………………………………………….

Equivalent units of production (b) ……………………….

Cost per equivalent unit, (a) ÷ (b) ………………………

Analytical Thinking (continued)

Transferred

In Costs

Materials

Conversion

Total

Ending work in process inventory:

2. The unit cost computed above is $21.72 (= $9.17 + $4.55 + $8.00) versus $25.71 on the original

Ethics Challenge (90 minutes)

Because there are no beginning inventories, it makes no difference

1.

Computation of the Cost of Goods Sold:

Transferred In

Conversion

Units completed and sold …………………..

200,000

200,000

Ending work in process:

Equivalent units of production …………….

210,000

203,000

Transferred In

Conversion

Cost of beginning work in process ……….

Cost added during the period ……………..

Total cost (a) ………………………………….

Equivalent units of production (b) ……….

Cost per equivalent unit, (a) ÷ (b) ………

2. The estimate of the percentage completion of ending work in process

inventories affects the unit costs of finished goods and therefore the

3. Increasing the percentage of completion can increase net operating

income by reducing the cost of goods sold. To increase net operating

Ethics Challenge (continued)

The percentage of completion, X, affects the cost of goods sold by its

effect on the unit cost, which can be determined as follows:

Because the cost of goods sold must be reduced down to $57,800,000,

the unit cost must be $289.00 ($57,800,000 ÷ 200,000 units). Thus, the

required percentage completion, X, to obtain the $200,000 reduction in

cost of goods sold can be found by solving the following equation:

$20,807,500

$187.50 + = $289.00

200,000 + 10,000X

Ethics Challenge (continued)

3. (continued)

Computation of the Cost of Goods Sold:

Transferred In

Conversion

Units completed and sold …………………..

200,000

200,000

Ending work in process:

Equivalent units of production …………….

210,000

205,000

Transferred In

Conversion

Cost of beginning work in process ……….

Cost added during the period ……………..

Equivalent units of production (b) ……….

Cost per equivalent unit, (a) ÷ (b) ………

4. Mary is in a very difficult position. Collaborating with Gary Stevens in

subverting the integrity of the accounting system is unethical by almost

any standard. To put the situation in its starkest light, Stevens is

Ethics Challenge (continued)

From a broader perspective, if the net profit figures reported by the

managers in a division cannot be trusted, then the company would be

foolish to base bonuses on the net profit figures. A bonus system based

on divisional net profits presupposes the integrity of the accounting

system.

The company should perhaps reconsider how it determines the bonus. It

Chapter 4

Take Two Solutions

Exercise 4-2 (10 minutes)

Weighted-Average Method

Equivalent Units

Materials

Conversion

Units transferred out ………………….

190,000

190,000

Exercise 4-3 (10 minutes)

Weighted-Average Method

1.

Materials

Labor

Overhead

Cost added during the period ……..

Total cost (a) ………………………….

Equivalent units of production (b) .

Cost per equivalent unit (a) ÷ (b) .

Cost of beginning work in process

2.

Cost per equivalent unit for materials …..

$ 7.34

Cost per equivalent unit for labor ………..

Cost per equivalent unit for overhead …..

13.00

Exercise 4-4 (10 minutes)

Materials

Conversion

Total

Ending work in process inventory:

Equivalent units of production ……

2,000

800

Cost per equivalent unit ……………

Units completed and transferred out:

Cost per equivalent unit ……………

Cost of units transferred out ………

$278,586

Exercise 4-5 (10 minutes)

Baking Department

Cost Reconciliation

Costs to be accounted for:

*

*The cost of units completed and transferred out can be deduced as

follows:

Cost of beginning Costs added Cost of ending Cost of units

Exercise 4-6 (10 minutes)

Weighted-Average Method

1.

Tons of Pulp

Work in process, June 1 ……………………………………

20,000

Started into production during the month ……………..

Total tons in process ………………………………………..

Deduct work in process, June 30 …………………………

Completed and transferred out during the month ……

2.

Equivalent Units

Materials

Labor and

Overhead

Units transferred out …………………………..

Work in process, ending:

Equivalent units of production ……………….

Exercise 4-9 (15 minutes)

Weighted-Average Method

1.

Materials

Labor

Overhead

Units transferred to the next

department ………………………………..

41,000

41,000

41,000

Work in process, ending:

Equivalent units of production ………….

2.

Materials

Labor

Overhead

Cost of beginning work in process ….

$ 4,320

$ 1,040

$ 1,790

Cost added during the period ………..

Total cost (a) …………………………….

$57,120

$22,540

$34,040

Equivalent units of production (b) ….

Cost per equivalent unit (a) ÷ (b) …..