Chapter 1

Managerial Accounting and Cost Concepts

Solutions to Questions

1-1 The three major elements of product

costs in a manufacturing company are direct

materials, direct labor, and manufacturing

overhead.

1-2

a. Direct materials are an integral part of a

finished product and their costs can be

conveniently traced to it.

b. Indirect materials are generally small

items of material such as glue and nails. They

1-3 A product cost is any cost involved in

purchasing or manufacturing goods. In the case

of manufactured goods, these costs consist of

1-4

a. Variable cost: The variable cost per unit is

constant, but total variable cost changes in

direct proportion to changes in volume.

b. Fixed cost: The total fixed cost is constant

within the relevant range. The

average

fixed

cost per unit varies inversely with changes

in volume.

c. Mixed cost: A mixed cost contains both

variable and fixed cost elements.

about variable and fixed cost behavior are

valid.

1-7 An activity base is a measure of

within the relevant range.

1-9 A discretionary fixed cost has a fairly

short planning horizon—usually a year. Such

costs arise from annual decisions by

1-10 Yes. As the anticipated level of activity

changes, the level of fixed costs needed to

support operations may also change. Most fixed

costs are adjusted upward and downward in

large steps, rather than being absolutely fixed at

one level for all ranges of activity.

1-11 The high-low method uses only two

points to determine a cost formula. These two

points are likely to be less than typical because

1-13 The term “least–squares regression”

means that the sum of the squares of the

deviations from the plotted points on a graph to

traditional approach organizes costs by function,

such as production, selling, and administration.

Within a functional area, fixed and variable costs

are intermingled.

1-15 The contribution margin is total sales

revenue less total variable expenses.

1-16 A differential cost is a cost that differs

between alternatives in a decision. An

The Foundational 15

1.

Direct materials ……………………………………………….

$ 6.00

Direct labor …………………………………………………….

3.50

Variable manufacturing overhead ………………………..

1.50

Variable manufacturing cost per unit ……………………

$11.00

Variable manufacturing cost per unit (a) ……………….

$11.00

Number of units produced (b) …………………………..

Total variable manufacturing cost (a) × (b) ……………

$110,000

Number of units produced (d) …………………………..

Total fixed manufacturing cost (c) × (d) ……………….

Total product (manufacturing) cost ………………………

$150,000

2.

Sales commissions ……………………………………………

$1.00

Variable administrative expense ………………………….

0.50

Variable selling and administrative per unit ……………

$1.50

Variable selling and admin. per unit (a)…………………

$1.50

Number of units sold (b) …………………………..

10,000

Number of units sold (d) …………………………..

Total period (nonmanufacturing) cost …………………..

The Foundational 15 (continued)

3.

Direct materials ……………………………………………….

$ 6.00

Direct labor …………………………………………………….

3.50

Variable manufacturing overhead ………………………..

Sales commissions ……………………………………………

Variable administrative expense …………………………..

Variable cost per unit sold …………………………..

4.

Direct materials ……………………………………………….

$ 6.00

Direct labor …………………………………………………….

3.50

Variable manufacturing overhead ………………………..

Sales commissions ……………………………………………

1.00

Variable administrative expense …………………………..

Variable cost per unit sold …………………………..

5.

Variable cost per unit sold (a)…………………………..

$12.50

Number of units sold (b) …………………………..

Total variable costs (a) × (b) …………………………..

6.

Variable cost per unit sold (a)…………………………..

$12.50

Number of units sold (b) …………………………..

Total variable costs (a) × (b) …………………………..

7.

Total fixed manufacturing cost

(see requirement 1) (a) …………………………..

$40,000

Number of units produced (b) …………………………..

8.

Total fixed manufacturing cost

(see requirement 1) (a) …………………………..

$40,000

Number of units produced (b) …………………………..

9.

Total fixed manufacturing cost

(see requirement 1) ……………………………………….

$40,000

The Foundational 15 (continued)

10.

Total fixed manufacturing cost

(see requirement 1) ……………………………………….

$40,000

11.

Variable overhead per unit (a) …………………………..

$1.50

Number of units produced (b) …………………………..

8,000

Total variable overhead cost (a) × (b) …………………..

Total fixed overhead (see requirement 1) ………………

Total manufacturing overhead cost ………………………

12.

Variable overhead per unit (a) …………………………..

$1.50

Number of units produced (b) …………………………..

12,500

Total variable overhead cost (a) × (b) …………………..

Total fixed overhead (see requirement 1) ………………

Total manufacturing overhead cost ………………………

13.

Selling price per unit …………………………………………

$22.00

(see requirement 4) ……………………………………….

Contribution margin per unit …………………………..

Variable cost per unit sold

The Foundational 15 (continued)

14.

Direct materials per unit …………………………..

$6.00

Direct labor per unit …………………………………………

3.50

Direct manufacturing cost per unit (a) ………………….

$9.50

Number of units produced (b) …………………………..

Total direct manufacturing cost (a) × (b) ………………

15.

Direct materials per unit …………………………..

$6.00

Direct labor per unit …………………………………………

3.50

Variable manufacturing overhead per unit ……………..

Incremental cost per unit produced ……………………..

Exercise 1-1 (15 minutes)

Cost

Cost Object

Direct

Cost

Indirect

Cost

1.

The wages of pediatric

nurses

The pediatric

department

X

2.

Prescription drugs

A particular patient

X

Heating the hospital

The pediatric

department

salary

A particular patient

Lab tests by outside

A particular patient

X

Exercise 1-2 (10 minutes)

1. The cost of a hard drive installed in a computer: direct materials.

2. The cost of advertising in the

Puget Sound Computer User

newspaper:

selling.

6. The wages of the company’s accountant: administrative.

7. Depreciation on equipment used to test assembled computers before

release to customers: manufacturing overhead.

Exercise 1-3 (15 minutes)

Product

Cost

Period

Cost

1.

Depreciation on salespersons’ cars ……………………

X

2.

Rent on equipment used in the factory ………………

X

3.

Lubricants used for machine maintenance…………..

X

X

X

6.

Factory supervisors’ salaries …………………………….

X

7.

X

X

9.

Advertising costs …………………………………………..

X

10.

Workers’ compensation insurance for factory

employees …………………………………………………

X

X

X

X

14.

X

X

Exercise 1-4 (15 minutes)

1.

Cups of Coffee Served

in a Week

2,000

2,100

2,200

Fixed cost …………………………..

Total cost …………………………..

Average cost per cup served * ..

2. The average cost of a cup of coffee declines as the number of cups of

Exercise 1-5 (20 minutes)

1.

Occupancy-

Days

Electrical

Costs

High activity level (August) ..

2,406

$5,148

Total cost (August) …………………………………………….

Fixed cost element …………………………………………….

2. Electrical costs may reflect seasonal factors other than just the variation

in occupancy days. For example, common areas such as the reception

area must be lighted for longer periods during the winter than in the

Exercise 1-6 (15 minutes)

1. Traditional income statement

Cherokee Inc.

Traditional Income Statement

Sales ($30 per unit × 20,000 units) ………………..

$600,000

Selling and administrative expenses:

Net operating income ………………………………….

$250,000

2. Contribution format income statement

Cherokee Inc.

Contribution Format Income Statement

Sales ……………………………………………………….

$600,000

Contribution margin …………………………………….

Fixed expenses:

Exercise 1-7 (15 minutes)

Item

Differential

Cost

Opportunity

Cost

Sunk

Cost

1.

Cost of the old X-ray machine ….

X

2.

The salary of the head of the

Radiology Department …………

3.

5.

Rent on the space occupied by

6.

The cost of maintaining the old

7.

Benefits from a new DNA

8.

Cost of electricity to run the X-

The salary of the head of the

Note: The costs of the salaries of the head of the Radiology Department

Exercise 1-8 (20 minutes)

1.

Kilometers

Driven

Total Annual

Cost*

High level of activity …………………….

105,000

$11,970

Low level of activity ……………………..

70,000

9,380

Change ……………………………………..

35,000

$ 2,590

*

105,000 kilometers × $0.114 per kilometer = $11,970

70,000 kilometers × $0.134 per kilometer = $9,380

Total cost at 105,000 kilometers …………………

Fixed cost per year ………………………………….

2. Y = $4,200 + $0.074X

3.

Fixed cost …………………………………………………

$ 4,200

Total annual cost ………………………………………..

Exercise 1-9 (10 minutes)

1. Product costs:

Direct materials ………………………

$ 80,000

Total product costs ………………….

2. Period costs:

Selling expenses ……………………..

3. Conversion costs:

Total conversion costs ……………..

4. Prime costs:

Total prime costs …………………….

Exercise 1-10 (20 minutes)

1. The company’s variable cost per unit is:

$180,000 =$6 per unit.

30,000 units

In accordance with the behavior of variable and fixed costs, the

completed schedule is:

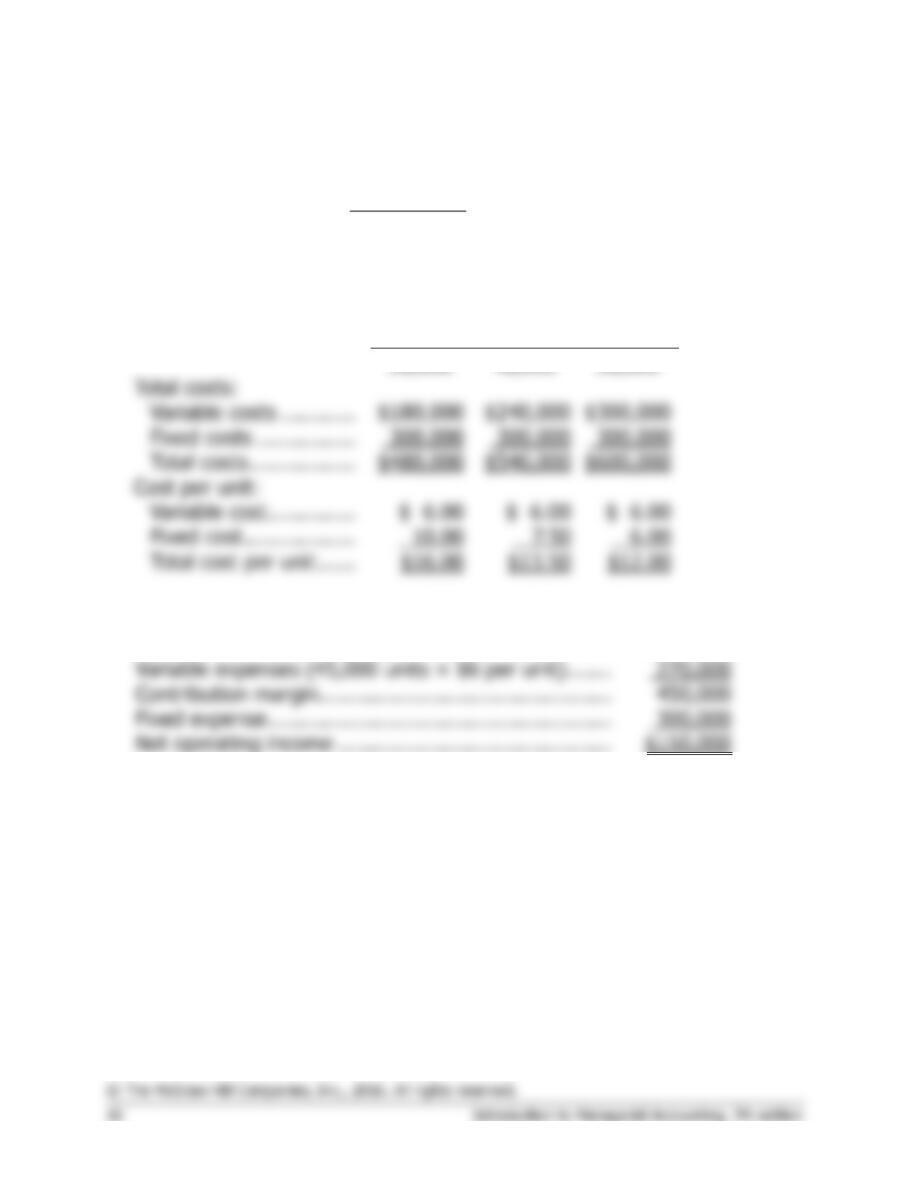

Units produced and sold

30,000

40,000

50,000

Total costs:

$240,000

Cost per unit:

2. The company’s income statement in the contribution format is:

Sales (45,000 units × $16 per unit) ……………………

$720,000

Variable expenses (45,000 units × $6 per unit) …….

Contribution margin………………………………………..

Exercise 1-11 (45 minutes)

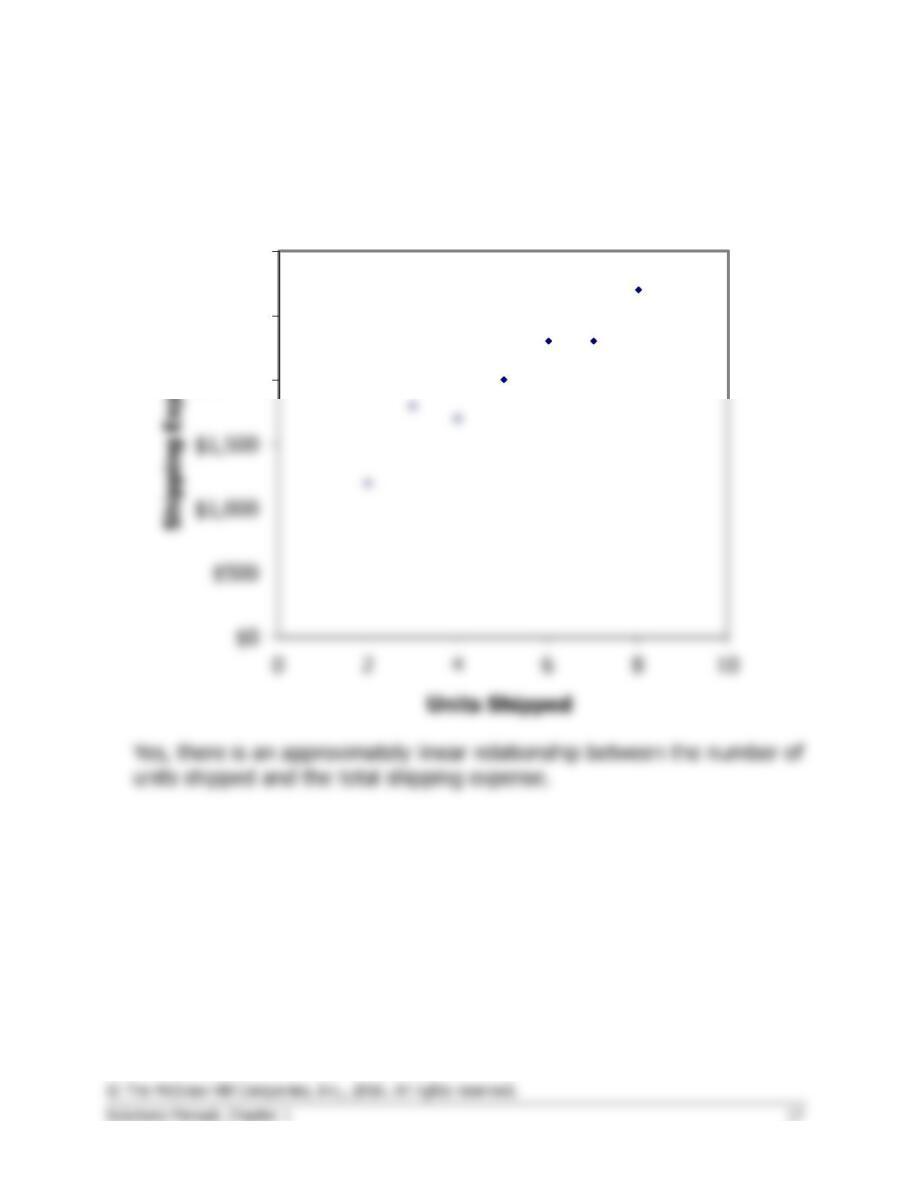

1. The scattergraph appears below:

$2,000

$2,500

$3,000

Exercise 1-11 (continued)

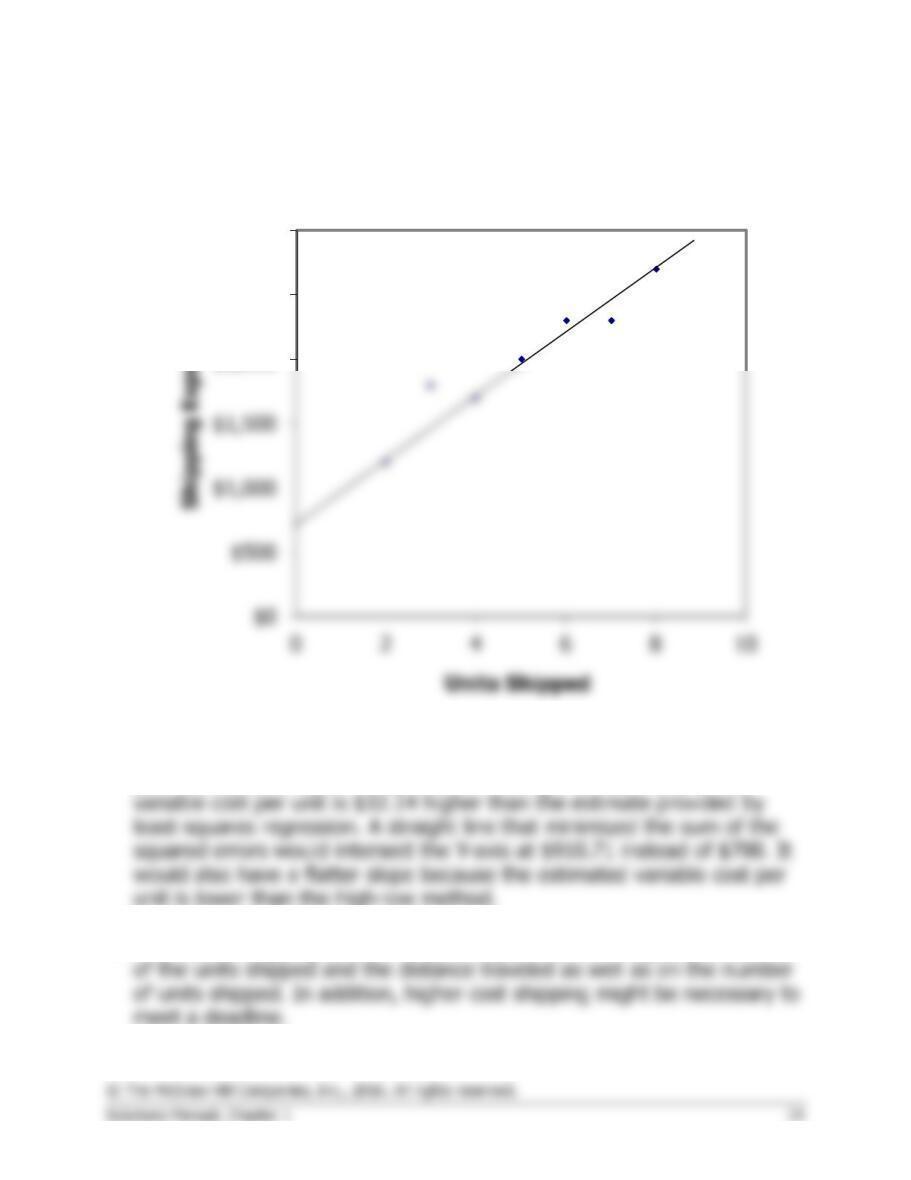

2. The high-low estimates and cost formula are computed as follows:

Units Shipped

Shipping Expense

High activity level (June) ……

8

$2,700

Low activity level (July) ……..

2

1,200

Change ………………………….

6

$1,500

Shipping expense at high activity level …………………..

Less variable cost element ($250 per unit × 8 units)…

Total fixed cost …………………………………………………

Exercise 1-11 (continued)

3. The high-low estimate of fixed costs is $210.71 lower than the estimate

provided by least–squares regression. The high-low estimate of the

4. The cost of shipping units is likely to depend on the weight and volume

$2,000

$2,500

$3,000

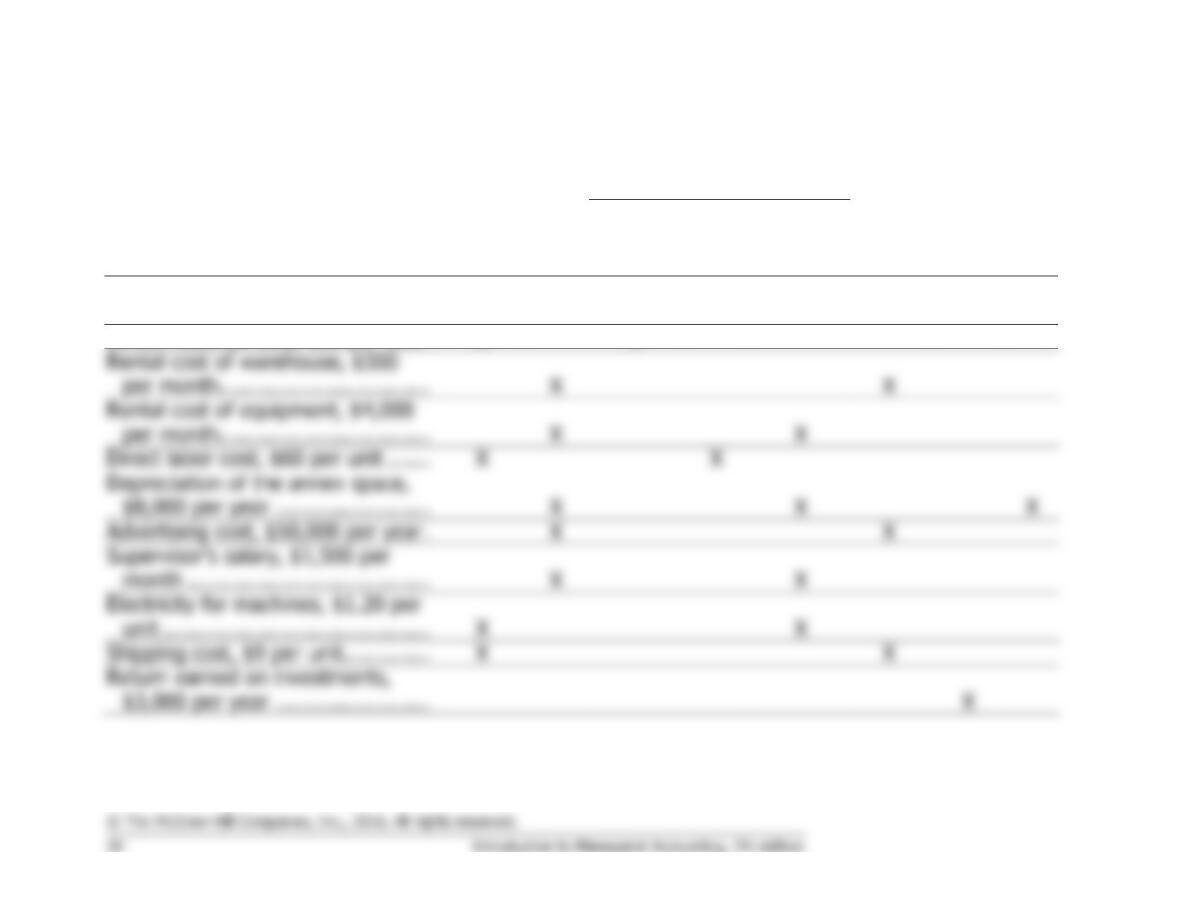

Exercise 1-12 (30 minutes)

Product Cost

Period

(Selling

Name of the Cost

Variable

Cost

Fixed

Cost

Direct

Materials

Direct

Labor

Manu-

facturing

Overhead

and

Admin)

Cost

Oppor-

tunity

Cost

Sunk

Cost

Rental revenue forgone, $30,000

per year ……………………………….

X

Direct materials cost, $80 per unit .

X

X

X

X

Rental cost of equipment, $4,000

per month…………………………….

X

X

Advertising cost, $50,000 per year .

X

X

Supervisor’s salary, $1,500 per

Electricity for machines, $1.20 per

Shipping cost, $9 per unit …………..

X

X

Return earned on investments,

$3,000 per year …………………….

X