Problem 6-23A (60 minutes)

1. a. Absorption costing unit product cost is:

Direct materials …………………………….

$ 3.50

Direct labor ………………………………….

Variable manufacturing overhead ……..

Fixed manufacturing overhead

10.00

Absorption costing unit product cost ….

$26.50

b. The absorption costing income statement is:

Sales (28,000 units) ……………………………………….

$1,120,000

Cost of goods sold (28,000 units × $26.50 per unit)

742,000

Gross margin ………………………………………………..

378,000

Selling and administrative expenses

[$200,000 + (28,000 units × $6.00 per unit)] ……

368,000

Net operating income ……………………………………..

$ 10,000

c. The reconciliation is as follows:

Units in ending inventory = Units in beginning inventory + Units

Variable costing net loss ………………………………….

Absorption costing net operating income …………….

Problem 6-23A (continued)

2. Under absorption costing, the company did earn a profit for the quarter.

However, before the question can really be answered, one must first

define what is meant by a “profit.” The central issue here relates to

timing

of release of fixed manufacturing overhead costs to expense.

Advocates of variable costing argue that all such costs should be

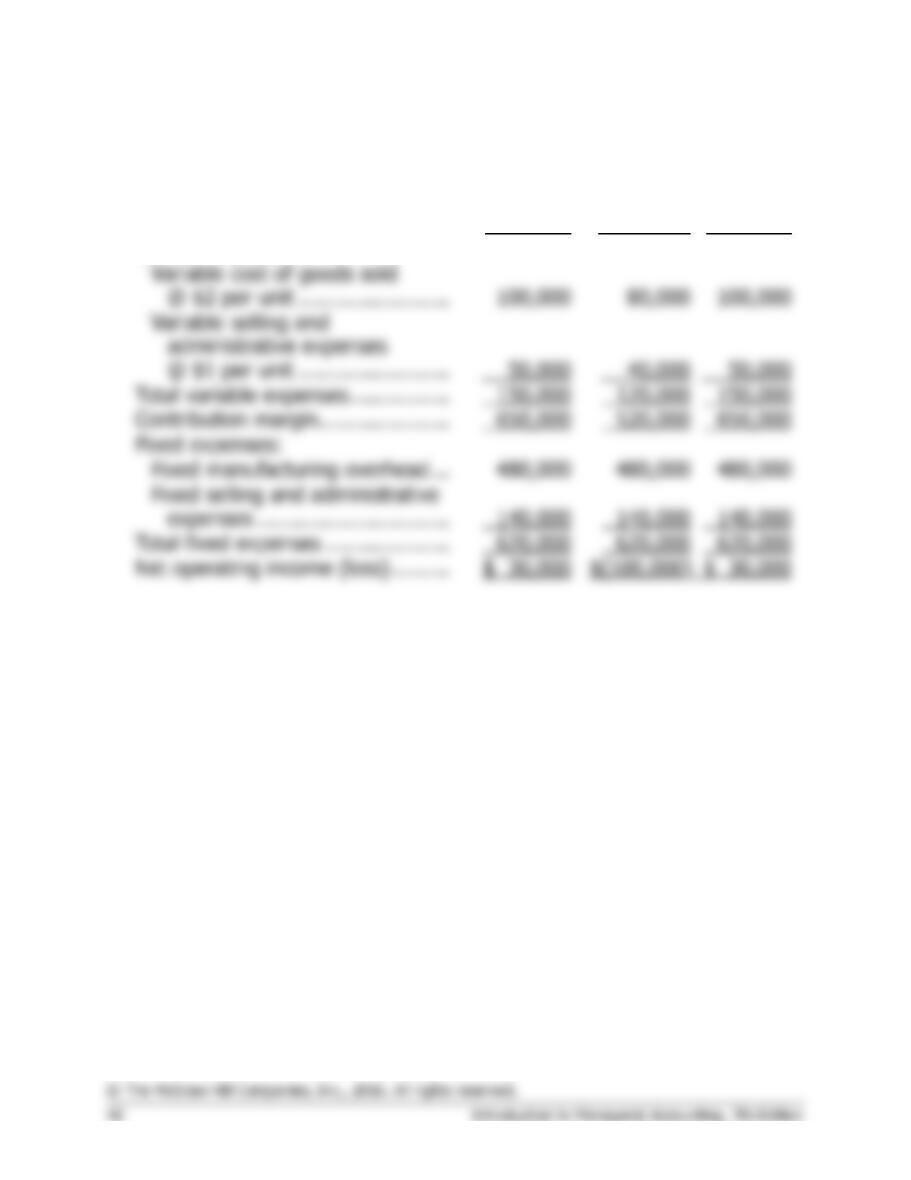

3. a. The variable costing income statement is:

Sales (32,000 units × $40 per unit) …………

$1,280,000

Variable expenses:

Contribution margin …………………………….

Fixed expenses:

Net operating income …………………………..

Problem 6-23A (continued)

b. The absorption costing income statement would be constructed as

follows:

The absorption costing unit product cost will remain at $26.50, the

c. The reconciliation of variable costing and absorption costing income

is:

Problem 6-24A (45 minutes)

1. The intern’s decision to use the absorption format for her segmented

income statements is a bad idea because it does not focus on cost

2. To answer this question, students must understand that cost of goods

sold for a merchandiser is a variable cost. Thus, all of the company’s

fixed costs plus its sales commissions are reported as part of selling and

administrative expenses. The amount of common fixed expenses

allocated to each segment is computed as follows:

Total

Commercial

Residential

Total selling and administrative

expense (a) …………………………..

$240,000

$104,000

$136,000

Sales commissions

Problem 6-24A (continued)

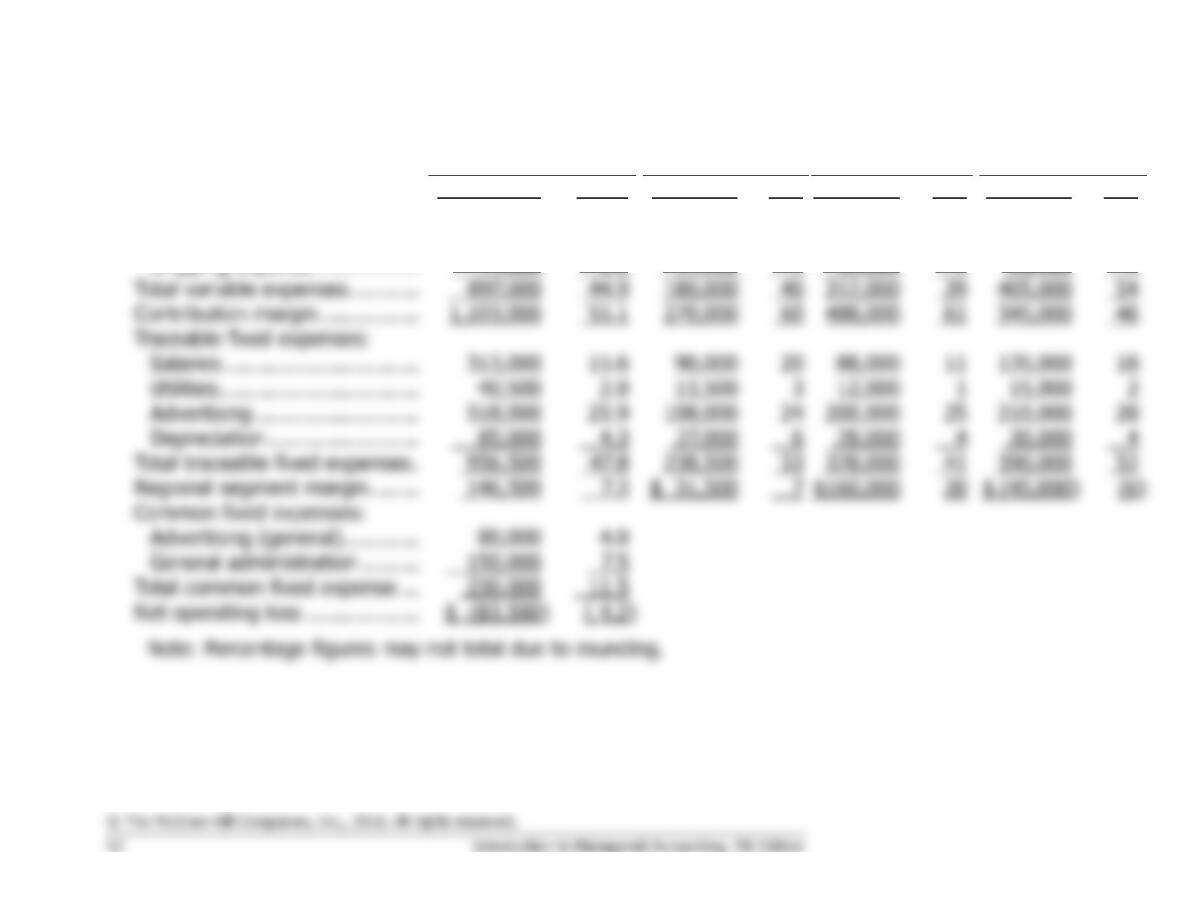

3. The contribution format segmented income statements would appear as

follows:

Total

Company

Commercial

Residential

Sales ………………………………

$750,000

$250,000

$500,000

Variable expenses:

Cost of goods sold …………..

Sales commissions (10%) …

Total variable expenses ……….

Contribution margin ……………

Traceable fixed expenses …….

Segment margin ………………..

Common fixed expenses ……..

Net operating income …………

Problem 6-24A (continued)

4. The companywide break-even point is computed as follows:

0.233 (rounded)

=

$708,155 (rounded)

5. The break-even point for the Commercial Division is computed as follows:

0.34

=

$161,765 (rounded)

Problem 6-24A (continued)

The break-even point for the Residential Division is computed as follows:

6. The new break-even point for the Commercial Division is computed as

follows:

Problem 6-25A (75 minutes)

1.

Year 1

Year 2

Year 3

Unit sales ………………………………

50,000

40,000

50,000

Sales ……………………………………

$800,000

$ 640,000

$800,000

Variable expenses:

Total variable expenses …………….

Contribution margin …………………

Fixed expenses:

480,000

Total fixed expenses ………………..

Net operating income (loss) ………

Problem 6-25A (continued)

2.

a.

Year 1

Year 2

Year 3

Variable manufacturing cost …………….

$ 2.00

$ 2.00

$ 2.00

Fixed manufacturing cost:

Absorption costing unit product cost ….

$11.60

$10.00

$14.00

b.

Units in beginning inventory …………….

0

0

20,000

+ Units produced …………………………..

50,000

60,000

40,000

− Units sold …………………………………

50,000

40,000

50,000

= Units in ending inventory ……………..

0

20,000

10,000

0

$30,000

$(100,000)

$30,000

3. Production went up sharply in Year 2, thereby reducing the unit product

cost, as shown in (2a) above. This reduction in cost per unit, combined

4. The fixed manufacturing overhead deferred in inventory from Year 2

Problem 6-25A (continued)

5. a. With lean production, production would have been tied to sales in

each year so that little or no inventory of finished goods would have

been built up in either Year 2 or Year 3.

b. If lean production had been in use, the net operating income under

absorption costing would have been the same as under variable

Year 1

Year 2

Year 3

Unit sales …………………………

50,000

40,000

50,000

Sales ………………………………

$ 800,000

$ 640,000

$ 800,000

Cost of goods sold:

*

Cost of goods sold ……………..

Gross margin ……………………

Net operating income (loss) …

Cost of goods

Problem 6-26A (60 minutes)

1. The disadvantages or weaknesses of the company’s version of a

segmented income statement are as follows:

a. The company should include a column showing the combined results

2. Corporate advertising expenses have been allocated on the basis of

sales dollars; the general administrative expenses have been allocated

evenly among the three regions. Such allocations can be misleading to

Problem 6-26A (continued)

3.

Total Company

West

Central

East

Sales ……………………………….

$2,000,000

100.0

$450,000

100

$800,000

100

$750,000

100

Variable expenses:

Cost of goods sold ……………

819,400

41.0

162,900

36

280,000

35

376,500

50

Shipping expense ……………..

77,600

3.9

17,100

4

32,000

4

28,500

4

Total variable expenses ………..

180,000

39

54

Contribution margin …………….

Traceable fixed expenses:

Salaries ………………………….

313,000

90,000

135,000

18

Utilities …………………………..

12,000

15,000

Advertising ……………………..

518,000

108,000

200,000

210,000

Depreciation ……………………

85,000

4.3

27,000

6

4

4

Total traceable fixed expenses .

Regional segment margin ……..

$ 31,500

Common fixed expenses:

Advertising (general) …………

General administration ………

Total common fixed expense …

Net operating loss ………………

Problem 6-26A (continued)

4. The following points should be brought to the attention of management:

a. Sales in the West are much lower than in the other two regions. This

is not due to lack of salespeople—salaries in the West are about the

same as in the Central Region, which has the highest sales of the

three regions.

Ethics Challenge (30 minutes)

1. Because of soft demand for the Brazilian Division’s product, the

inventory should be drawn down to the minimum level of 50 units.

Drawing inventory down to the minimum level would require production

as follows during the last quarter:

2. To maximize the Brazilian Division’s operating income, Mr. Cavalas could

produce as many units as storage facilities will allow. By building

inventory to the maximum level, Mr. Cavalas would be able to defer a

portion of the year’s fixed manufacturing overhead costs to future years

Ethics Challenge (continued)

Thus, by producing enough units to build inventory to the maximum

3. By setting a production schedule that will maximize his division’s net

operating income—and maximize his own bonus—Mr. Cavalas would be

acting against the best interests of the company as a whole. The extra

units aren’t needed and would be expensive to carry in inventory.

Analytical Thinking (45 minutes)

1.

Total

Company

Cook–

book

Travel

Guide

Handy

Speller

Sales …………………………..……

$300,000

$90,000

$150,000

$60,000

Variable expenses:

Printing cost …………………….

102,000

27,000

63,000

12,000

Sales commissions…………….

30,000

9,000

15,000

6,000

36,000

78,000

18,000

54,000

72,000

42,000

Traceable fixed expenses:

Salaries ………………………….

33,000

18,000

Equipment depreciation*

Warehouse rent** …………….

12,000

1,800

6,000

90,000

36,000

39,000

15,000

Product line segment margin …

78,000

$18,000

$ 33,000

Common fixed expenses:

General sales …………………..

18,000

General administration ……….

42,000

63,000

Net operating income …………..

$ 15,000

*

$9,000 × 30%, 50%, and 20%, respectively.