8-541

8-542

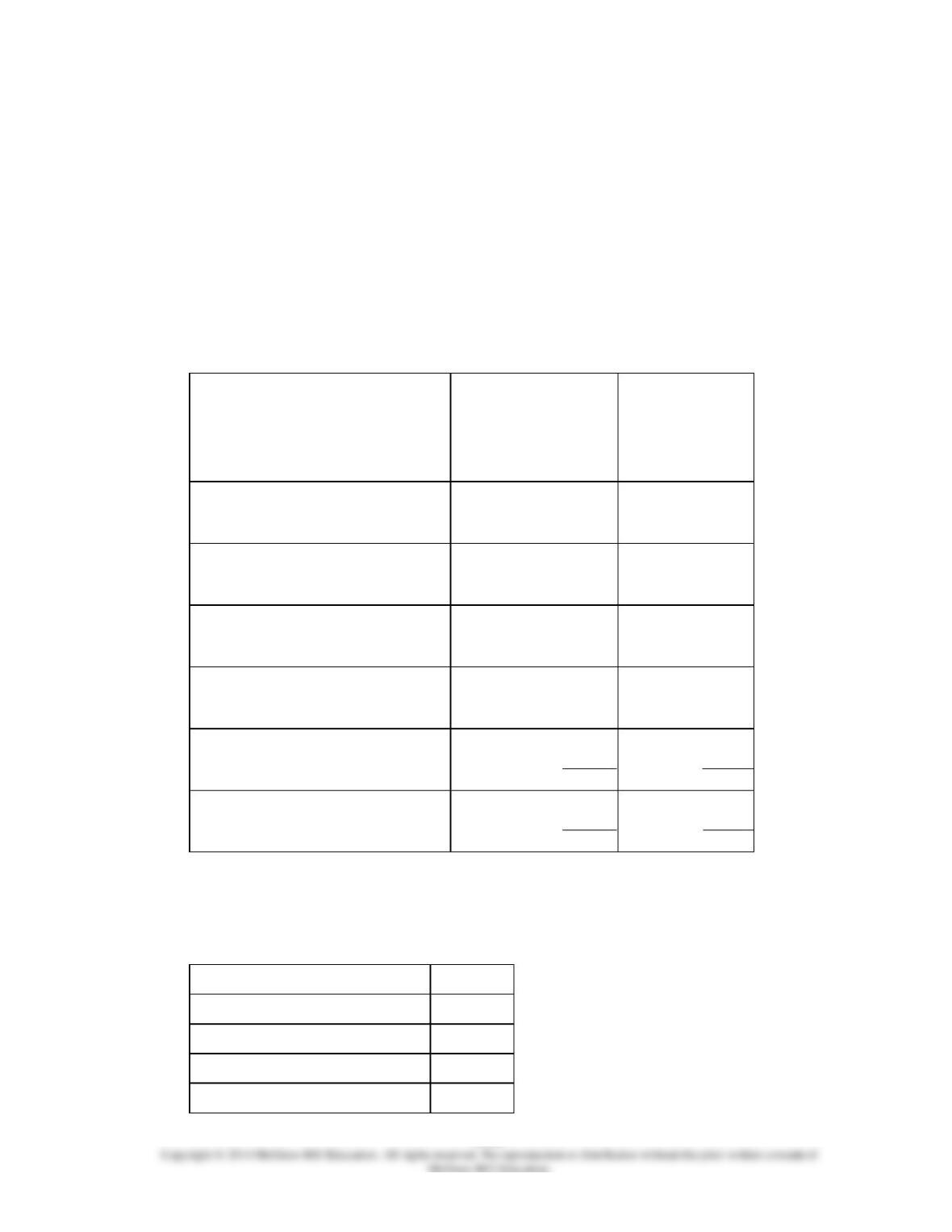

110.

Zenon Kennel uses tenant-days as its measure of activity; an animal housed in the kennel

for one day is counted as one tenant-day. During July, the kennel budgeted for 3,300

tenant-days, but its actual level of activity was 3,260 tenant-days. The kennel has

provided the following data concerning the formulas used in its budgeting and its actual

results for July:

Data used in budgeting:

Fixed element

per month

Variable

element

per

tenant-

day

Revenue

−

$27.60

Wages and salaries

$3,400

$5.10

Food and supplies

1,000

8.20

Facility expenses

8,600

4.90

Administrative expenses

7,000

0.40

Total expenses

$20,000

$18.60

Actual results for July:

Revenue

$87,446

Wages and salaries

$19,796

Food and supplies

$27,262

Facility expenses

$25,004

Administrative expenses

$8,704

The facility expenses in the flexible budget for July would be closest to:

8-543

8-544

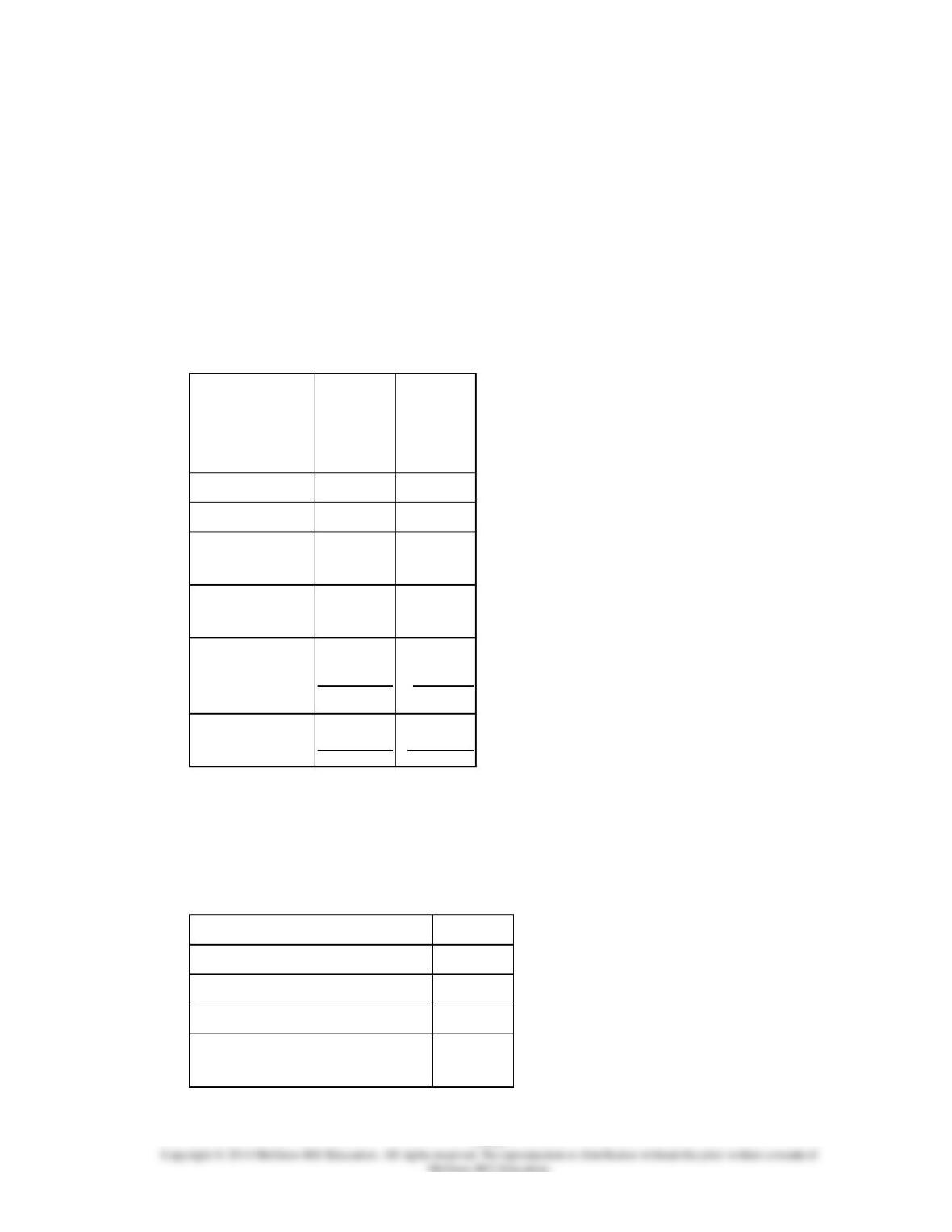

111.

Zenon Kennel uses tenant-days as its measure of activity; an animal housed in the kennel

for one day is counted as one tenant-day. During July, the kennel budgeted for 3,300

tenant-days, but its actual level of activity was 3,260 tenant-days. The kennel has

provided the following data concerning the formulas used in its budgeting and its actual

results for July:

Data used in budgeting:

Fixed element

per month

Variable

element per

tenant-day

Revenue

−

$27.60

Wages and salaries

$3,400

$5.10

Food and supplies

1,000

8.20

Facility expenses

8,600

4.90

Administrative expenses

7,000

0.40

Total expenses

$20,000

$18.60

Actual results for July:

Revenue

$87,446

Wages and salaries

$19,796

Food and supplies

$27,262

Facility expenses

$25,004

Administrative expenses

$8,704

8-545

The net operating income in the flexible budget for July would be closest to:

8-546

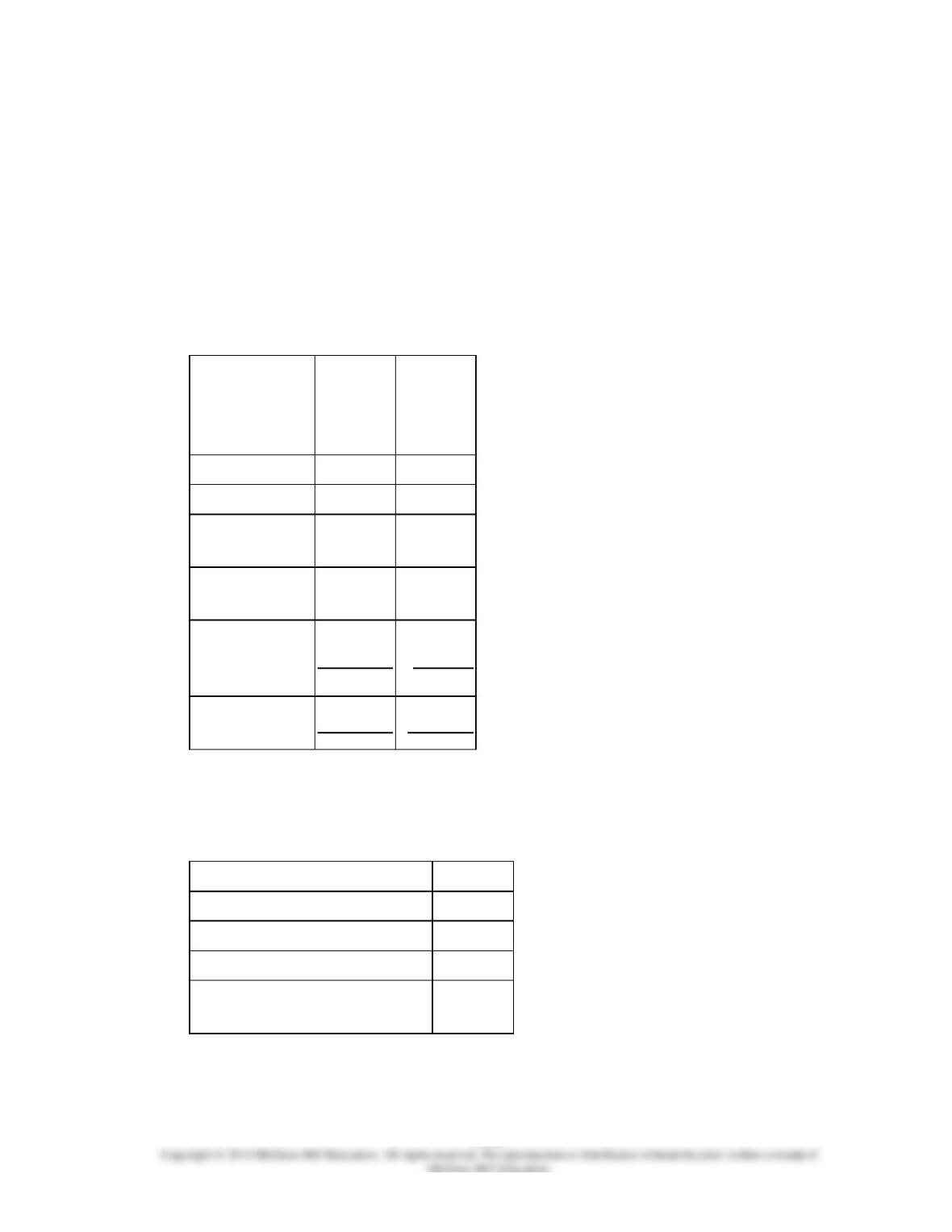

112.

Prater Corporation manufactures and sells a single product. The company uses units as

the measure of activity in its budgets and performance reports. During February, the

company budgeted for 5,400 units, but its actual level of activity was 5,380 units. The

company has provided the following data concerning the formulas used in its budgeting

and its actual results for February:

Data used in budgeting:

Fixed

element

per

month

Variable

element

per unit

Revenue

−

$31.10

Direct labor

$0

$3.30

Direct

materials

0

9.00

Manufacturing

overhead

44,600

1.80

Selling and

administrative

expenses

26,700

0.10

Total

expenses

$71,300

$14.20

Actual results for February:

Revenue

$169,648

Direct labor

$18,164

Direct materials

$50,810

Manufacturing overhead

$53,734

Selling and administrative

expenses

$28,278

8-547

The direct labor in the planning budget for February would be closest to:

8-548

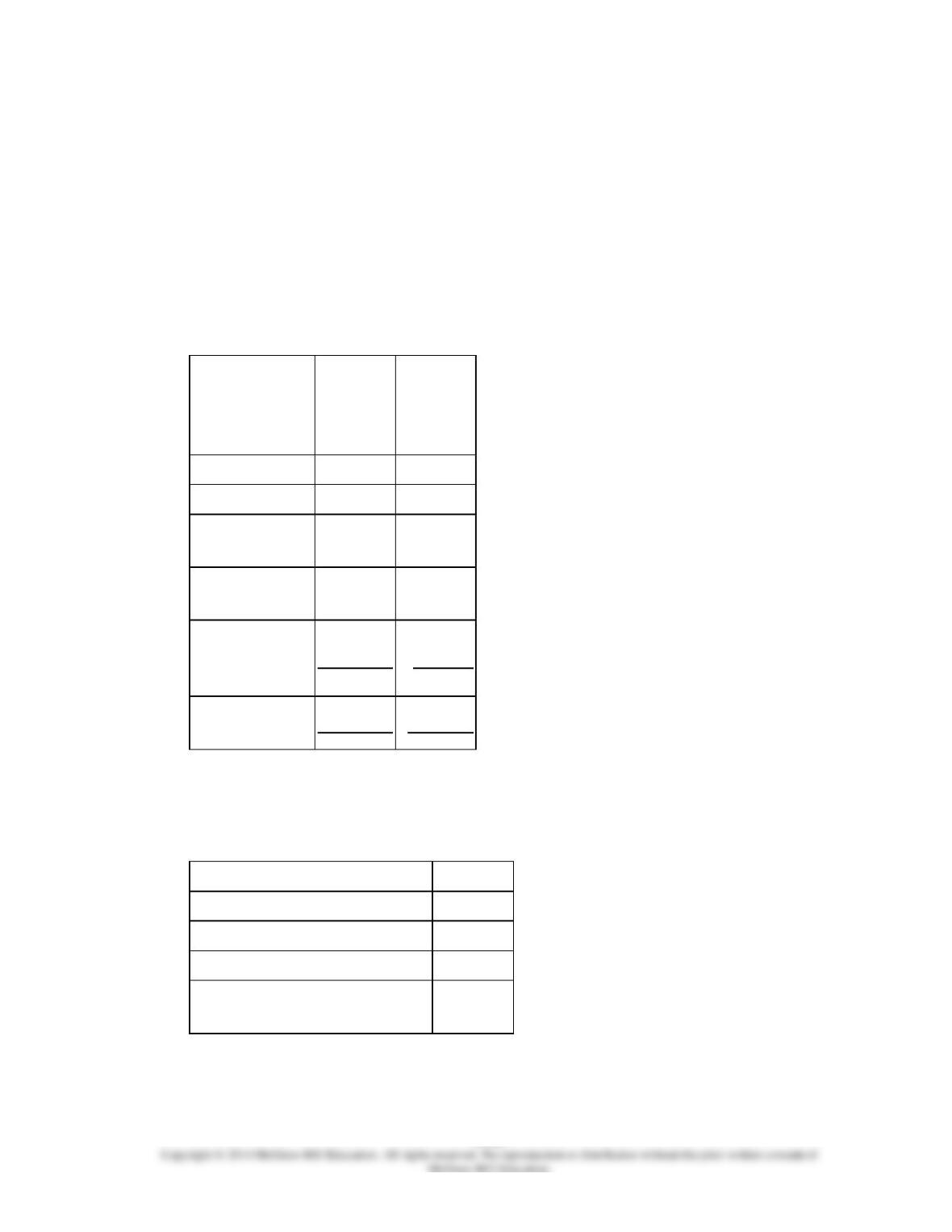

113.

Prater Corporation manufactures and sells a single product. The company uses units as

the measure of activity in its budgets and performance reports. During February, the

company budgeted for 5,400 units, but its actual level of activity was 5,380 units. The

company has provided the following data concerning the formulas used in its budgeting

and its actual results for February:

Data used in budgeting:

Fixed

element

per

month

Variable

element

per unit

Revenue

−

$31.10

Direct labor

$0

$3.30

Direct

materials

0

9.00

Manufacturing

overhead

44,600

1.80

Selling and

administrative

expenses

26,700

0.10

Total

expenses

$71,300

$14.20

Actual results for February:

Revenue

$169,648

Direct labor

$18,164

Direct materials

$50,810

Manufacturing overhead

$53,734

Selling and administrative

expenses

$28,278

8-549

The manufacturing overhead in the flexible budget for February would be closest to:

8-550

114.

Prater Corporation manufactures and sells a single product. The company uses units as

the measure of activity in its budgets and performance reports. During February, the

company budgeted for 5,400 units, but its actual level of activity was 5,380 units. The

company has provided the following data concerning the formulas used in its budgeting

and its actual results for February:

Data used in budgeting:

Fixed

element

per

month

Variable

element

per unit

Revenue

−

$31.10

Direct labor

$0

$3.30

Direct

materials

0

9.00

Manufacturing

overhead

44,600

1.80

Selling and

administrative

expenses

26,700

0.10

Total

expenses

$71,300

$14.20

Actual results for February:

Revenue

$169,648

Direct labor

$18,164

Direct materials

$50,810

Manufacturing overhead

$53,734

Selling and administrative

expenses

$28,278

8-551

The net operating income in the flexible budget for February would be closest to:

8-552

115.

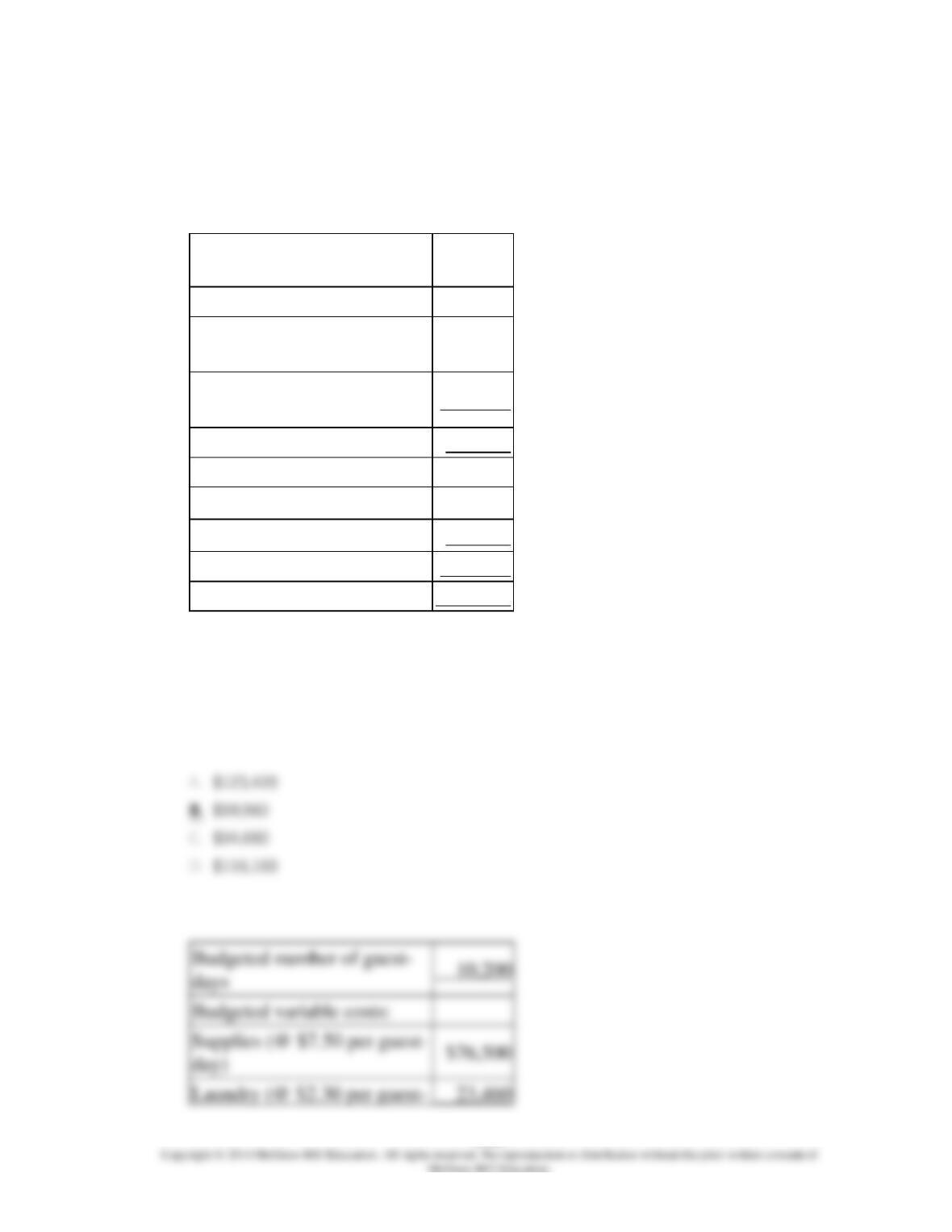

Bard Hotel bases its budgets on guest-days. The hotel’s static budget for January appears

below:

Budgeted number of guest-

days

9,600

Budgeted variable costs:

Supplies (@ $7.50 per

guest-day)

$72,000

Laundry (@ $2.30 per

guest-day)

22,080

Total variable cost

94,080

Budgeted fixed costs:

Wages and salaries

95,040

Occupancy costs

21,120

Total fixed cost

116,160

Total cost

$210,240

Budgeted variable costs:

Supplies (@ $7.50 per guest-

day)

The total variable cost at the activity level of 10,200 guest-days per month should be:

8-553

8-554

116.

Bard Hotel bases its budgets on guest-days. The hotel’s static budget for January appears

below:

Budgeted number of guest-

days

9,600

Budgeted variable costs:

Supplies (@ $7.50 per

guest-day)

$72,000

Laundry (@ $2.30 per

guest-day)

22,080

Total variable cost

94,080

Budgeted fixed costs:

Wages and salaries

95,040

Occupancy costs

21,120

Total fixed cost

116,160

Total cost

$210,240

days

Budgeted fixed costs:

Wages and salaries

Occupancy costs

Total fixed cost

$116,160

The total fixed cost at the activity level of 10,600 guest-days per month should be:

8-555

8-556

117.

Bard Hotel bases its budgets on guest-days. The hotel’s static budget for January appears

below:

Budgeted number of guest-

days

9,600

Budgeted variable costs:

Supplies (@ $7.50 per

guest-day)

$72,000

Laundry (@ $2.30 per

guest-day)

22,080

Total variable cost

94,080

Budgeted fixed costs:

Wages and salaries

95,040

Occupancy costs

21,120

Total fixed cost

116,160

Total cost

$210,240

Budgeted variable costs:

The total cost at the activity level of 10,300 guest-days per month should be:

8-557

8-558

118.

Hettinger Hospital bases its budgets on patient-visits. The hospital’s static budget for

March appears below:

Budgeted number of

patient-visits

6,800

Budgeted variable costs:

Supplies (@ $4.80 per

patient-visit)

$32,640

Laundry (@ $6.70 per

patient-visit)

45,560

Total variable cost

78,200

Budgeted fixed costs:

Wages and salaries

42,160

Occupancy costs

67,320

Total fixed cost

109,480

Total cost

$187,680

visits

Budgeted variable costs:

patient-visit)

Laundry (@ $6.70 per

patient-visit)

Total variable cost

The total variable cost at the activity level of 7,200 patient-visits per month should be:

8-559

8-560

119.

Hettinger Hospital bases its budgets on patient-visits. The hospital’s static budget for

March appears below:

Budgeted number of patient-

visits

6,800

Budgeted variable costs:

Supplies (@ $4.80 per

patient-visit)

$32,640

Laundry (@ $6.70 per

patient-visit)

45,560

Total variable cost

78,200

Budgeted fixed costs:

Wages and salaries

42,160

Occupancy costs

67,320

Total fixed cost

109,480

Total cost

$187,680

7,700

Budgeted fixed costs:

Wages and salaries

Occupancy costs

Total fixed cost

$109,480

The total fixed cost at the activity level of 7,700 patient-visits per month should be: