Chapter 9

Take Two Solutions

Exercise 9-1 (10 minutes)

1.

Net operating income

Margin = Sales

Exercise 9-2 (10 minutes)

Average operating assets ………………….

$2,800,000

Net operating income ……………………….

Exercise 9-3 (20 minutes)

1.

Throughput time =

Process time + Inspection time + Move time +

Queue time

=

4.8 days + 0.3 days + 1.0 days + 5.0 days

=

11.1 days

4.

Delivery cycle time =

Wait time + Throughput time

=

14.0 days + 11.1 days

=

25.1 days

Exercise 9-6 (20 minutes)

1. ROI computations:

Net operating income Sales

ROI = ×

Sales Average operating assets

2.

Osaka

Yokohama

Average operating assets (a) ………………….

$1,000,000

$4,000,000

Net operating income …………………………..

Residual income ………………………………….

3. No, the Yokohama Division is simply larger than the Osaka Division and

for this reason one would expect that it would have a greater amount of

Exercise 9-11 (30 minutes)

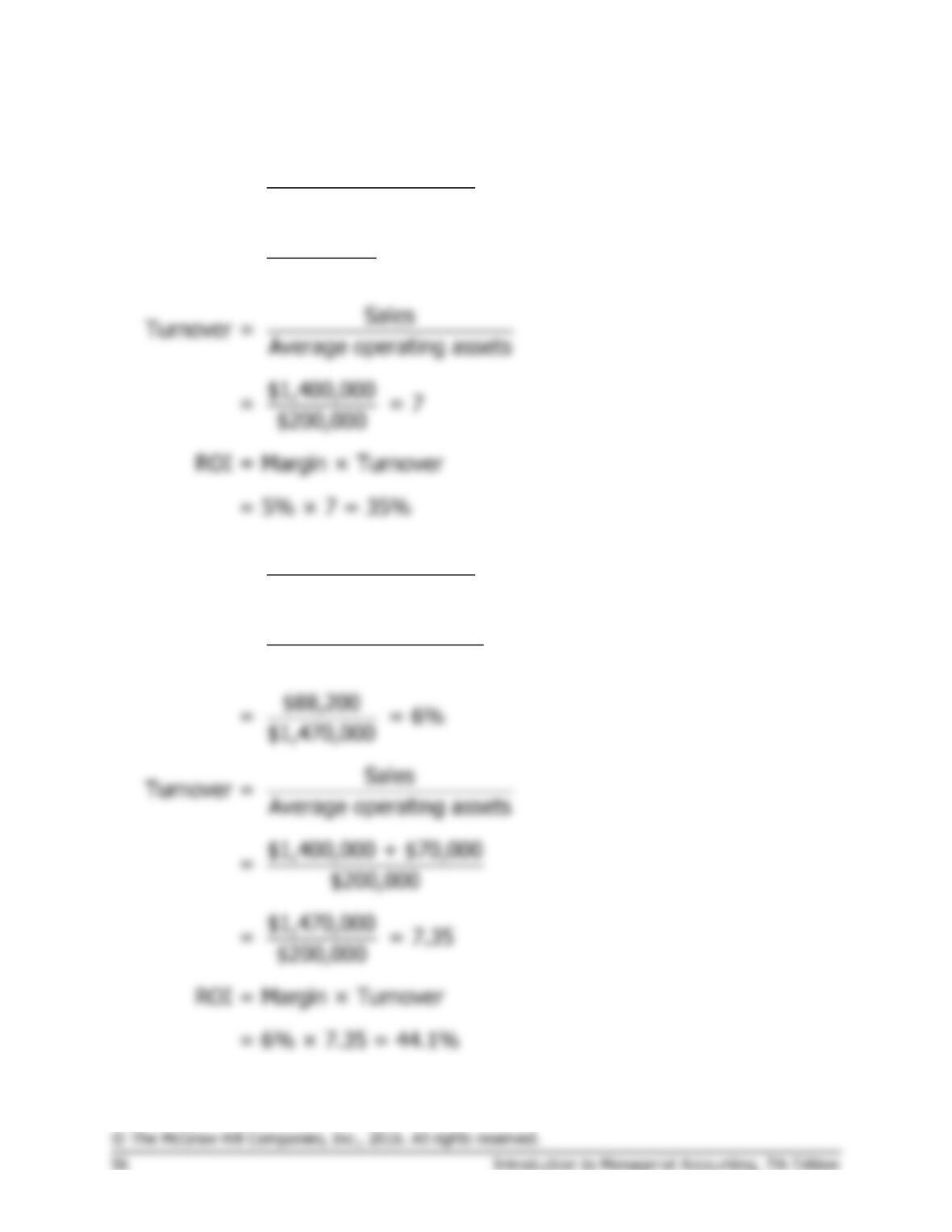

1.

Net operating income

Margin = Sales

$70,000

= = 5%

$1,400,000

2.

Net operating income

Margin = Sales

$70,000 + $18,200

=

$1,400,000 + $70,000

Exercise 9-11 (continued)

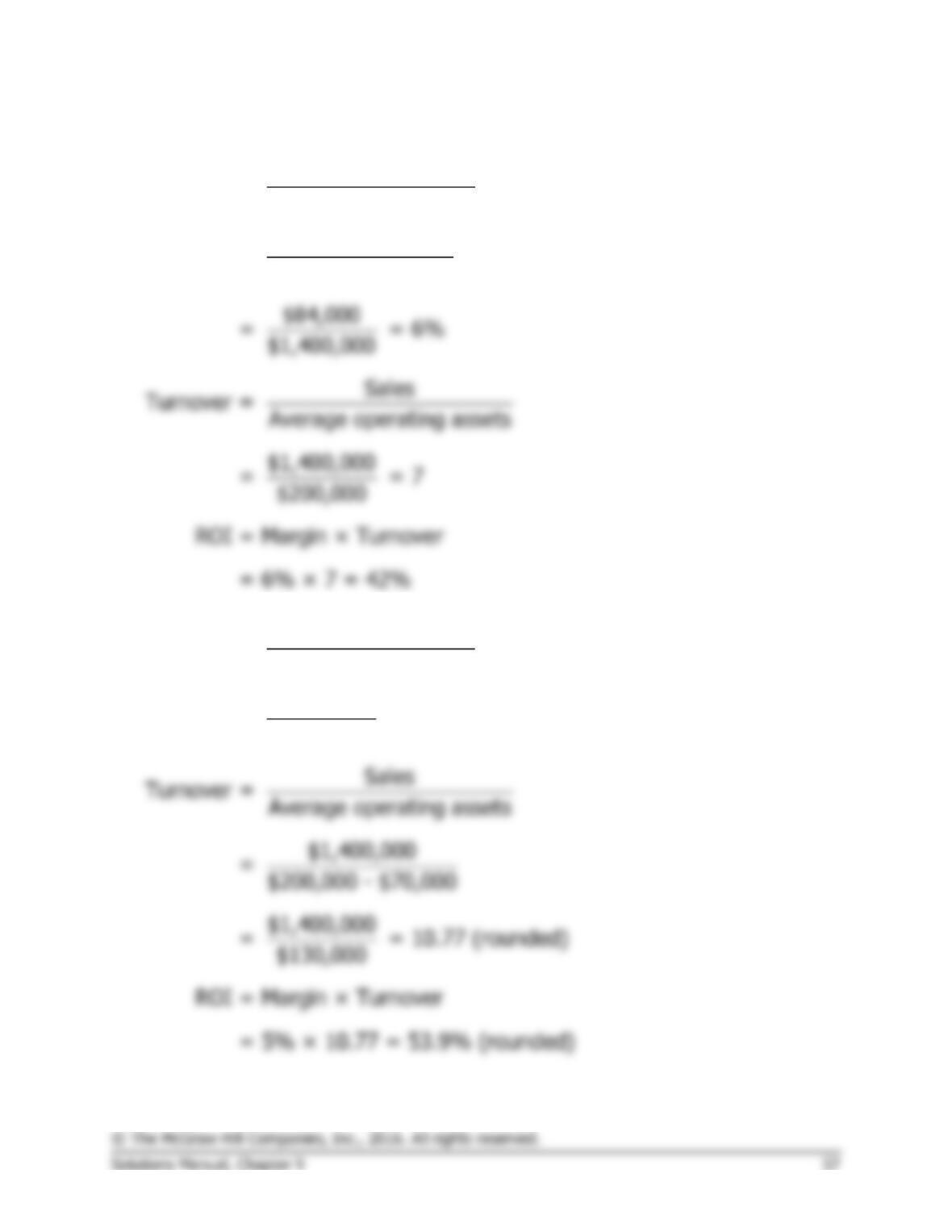

3.

Net operating income

Margin = Sales

$70,000 + $14,000

=

$1,400,000

4.

Net operating income

Margin =

Sales

$70,000

= = 5%

$1,400,000

Exercise 9-12 (30 minutes)

1. ROI computations:

Net operating income Sales

ROI = ×

Sales Average operating assets

Division A:

2.

Division A

Division B

Division C

Average operating assets ………

$3,000,000

$7,000,000

$5,000,000

Required rate of return………….

× 17%

× 17%

× 17%

Required operating income …….

$ 510,000

Actual operating income ………..

$ 600,000

$ 560,000

Residual income ………………….

Exercise 9-12 (continued)

3. a. and b.

Division A

Division B

Division C

Return on investment (ROI) ………..

20%

8%

16%

Therefore, if the division is

presented with an investment

If performance is being measured by ROI, both Division A and Division C

probably would reject the 15% investment opportunity. These divisions’

ROIs currently exceed 15%; accepting a new investment with a 15%

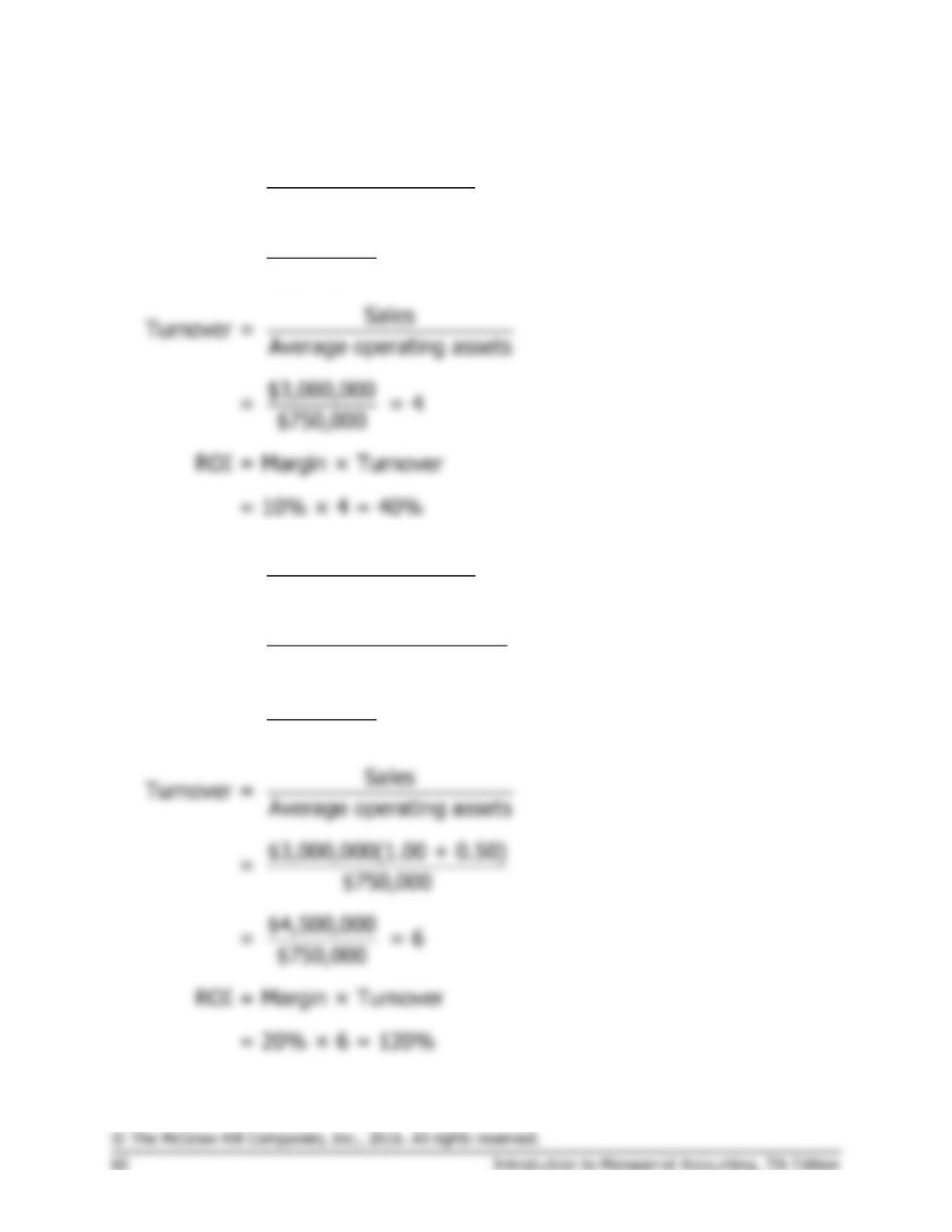

Exercise 9-13 (15 minutes)

1.

Net operating income

Margin = Sales

$300,000

= = 10%

$3,000,000

2.

Net operating income

Margin = Sales

$300,000(1.00 + 2.00)

=

$3,000,000(1.00 + 0.50)

$900,000

= = 20%

$4,500,000

Exercise 9-13 (continued)

3.

Net operating income

Margin = Sales

$300,000 + $200,000

=

$3,000,000 + $1,000,000

$500,000

= = 12.5%

$4,000,000