Exercise 3-9 (continued)

2. Activity costs are assigned to the two hospitals as follows:

City General:

Activity Cost Pool

(a)

Activity Rate

(b)

Activity

(a) × (b)

ABC Cost

Manual order processing ……

$75.00

per order

orders

Electronic order processing ..

$16.00

per order

orders

Total activity costs ……………

County General:

Activity Cost Pool

(a)

Activity Rate

(b)

Activity

(a) × (b)

ABC Cost

Customer deliveries ………….

$80.00

per delivery

20

deliveries

$ 1,600

Manual order processing ……

$75.00

per order

40

orders

Electronic order processing ..

$16.00

per order

orders

Line item picking ……………..

per line item

line items

3. Hospitals that require frequent deliveries, place a high volume of manual orders, and order many line

items are likely to be more expensive to serve.

Exercise 3-10 (30 minutes)

1. Under the traditional direct labor-hour based costing system,

manufacturing overhead is applied to products using the predetermined

overhead rate computed as follows:

Estimated total manufacturing overhead cost

Predetermined =

overhead rate Estimated total direct labor –hours

Exercise 3-10 (continued)

2. The activity rates are computed as follows:

Activity Cost Pools

(a)

Total

Cost

(b)

Total Activity

(a) ÷ (b)

Activity Rate

3. Under the activity-based costing system, the unit product costs would

be computed as follows:

Xactive

Pathbreaker

Direct materials ………………..

$1,620,000

$3,825,000

Supporting direct labor ………

Batch setups ……………………

General factory

Total cost (a) …………………..

$3,096,875

Unit product cost (a) ÷ (b) …

4. The traditional system uses one unit-level activity measure, direct labor

hours, to assign 31.8% ($700,000 ÷ $2,200,000) of all overhead to the

Exercise 3-11 (30 minutes)

1. The activity rates are computed as follows:

Activity Cost Pool

(a)

Estimated

Overhead

Cost

(b)

Expected

Activity

(a) ÷ (b)

Activity Rate

2. a. Overhead cost is assigned to the products as follows:

Product A

Activity Cost Pool

(a)

Activity Rate

(b)

Actual Activity

(a) × (b)

ABC Cost

Exercise 3-11 (continued)

Product B

Activity Cost Pool

(a)

Activity Rate

(b)

Actual Activity

(a) × (b)

ABC Cost

Labor related ……..

$9.00

per DLH

100

DLHs

$ 900

Purchase orders ….

$2.00

per order

105

orders

Template etching ..

per template

templates

Total ………………..

$13,060

Product C

Activity Cost Pool

(a)

Activity Rate

(b)

Actual Activity

(a) × (b)

ABC Cost

Labor related ……..

$9.00

per DLH

700

DLHs

Purchase orders ….

$2.00

per order

180

orders

Product testing …..

per test

tests

Template etching ..

per template

templates

Total ………………..

$15,910

Product D

Activity Cost Pool

(a)

Activity Rate

(b)

Actual Activity

(a) × (b)

ABC Cost

Labor related ……..

$9.00

per DLH

700

DLHs

Purchase orders ….

$2.00

per order

160

orders

Product testing …..

per test

tests

Template etching ..

per template

templates

Total ………………..

$20,620

Exercise 3-11 (continued)

3. The conventional system would assign 5% (100 DLH ÷ 2,000 DLH) of all

overhead costs to Product B. The ABC system would assign 20% (105

orders ÷ 525 orders) of the purchase order activity costs to Product B.

Problem 3-12A (30 minutes)

1. Under the traditional direct labor-dollar based costing system,

manufacturing overhead is applied to products using the predetermined

overhead rate computed as follows:

Problem 3-12A (continued)

2. The activity rates are computed as follows:

Activity Cost Pools

(a)

Total

Cost

(b)

Total Activity

(a) ÷ (b)

Activity Rate

Machining …………..

$198,250

152,500

MHR

$1.30

per MHR

Setups ……………….

$150,000

setup hrs.

per setup hr.

General factory ……

162,500

$0.37

per DL$

727,850

3. The traditional system uses one unit-level activity measure, direct labor

dollars, to assign 73.8% ($375,600 ÷ $508,625) of all overhead costs to

Problem 3-13A (15 minutes)

Activity

Level

Possible Activity Measures

a.

A percentage of all completed

goods are inspected on a

Unit

Facility

Arbitrary*

Employees are trained in

Facility or

Milling machines are used to

make components for

Unit

Number of units processed;

Machine-hours

general procedures.

Product

f.

The human resources

department screens and hires

new employees.

Facility

Arbitrary*

g.

Purchase orders are issued for

materials required in

production.

Batch

Number of purchase orders

Material is received on the

the production area.

Number of material moves

i.

The plant controller prepares

j.

The engineering department

makes modifications in the

Product

Engineering time

Machines are set up between

Facility

Arbitrary*

Problem 3-14A (60 minutes)

1. The first step is to determine the activity rates:

Serving a Party

Serving a Diner

Serving Drinks

Total activity (b) …………………..

parties

diners

drinks

2. According to the ABC system, the cost of serving each of the parties can be computed as follows:

Serving a Party

Serving a Diner

Serving Drinks

Cost per unit of activity .

$4.10

per party

$6.60

per diner

$1.20

per drink

a. A party of four diners who order three drinks:

Cost ………………………..

Problem 3-14A (continued)

3. The average cost per diner for each party can be computed by dividing

the total cost of the party by the number of diners in the party as

follows:

4. The average cost per diner differs from party to party under the activity-

based costing system for two reasons. First, the cost of serving a party

($4.10) does not depend on the number of diners in the party.

Therefore, the average cost per diner of this activity decreases as the

number of diners in the party increases. With only one diner, the cost is

Problem 3-15A (45 minutes)

1. The company’s estimated total direct labor-hours for the year can be

computed as follows:

Flexible model: 1,000 units × 2.0 DLH per unit ….

2,000

Rigid model: 10,000 units × 1.0 DLH per unit ……

10,000

Total direct labor-hours ………………………………..

12,000

The unit product costs are computed as follows:

Flexible

Rigid

Direct materials ……………………

$110.00

$ 80.00

Direct labor …………………………

$50.00 per DLH × 2.0 DLHs …

Unit product cost …………………

$240.00

2. Activity rates can be computed as follows:

(a)

Estimated

(b)

Expected

Activity

(a) ÷ (b)

Activity Rate

Overhead

Activity Cost Pool

Cost

Purchase orders …

$20,000

400

orders

$50.00

per order

Rework requests ..

$10,000

200

requests

$50.00

Machine related …

MHs

$90.00

per MH

Problem 3-15A (continued)

3. a.

Flexible

Rigid

Expected

Expected

Activity

Amount

Activity

Amount

Purchase orders, at $50.00 per order ………

100

$ 5,000

300

$ 15,000

Product testing, at $100.00 per test ………..

Machine related, at $90.00 per MH ………….

225,000

Total overhead cost assigned (a) ……………

Number of units produced (b) ………………..

Overhead cost per unit (a) ÷ (b) …………….

b. Using activity-based costing, the unit product costs would be:

Flexible

Rigid

Direct materials ……………..

$110.00

$ 80.00

Direct labor …………………..

Manufacturing overhead ….

233.00

Unit product cost …………..

$373.00

Problem 3-15A (continued)

4. Unit product costs are distorted as a result of using direct labor-hours as

the base for applying overhead costs to products. Although the flexible

model requires twice as much labor as the rigid model, it still is not

being assigned enough overhead cost according to the activity-based

Problem 3-16A (45 minutes)

1. The company expects to work 40,000 direct labor-hours, computed as

follows:

LEC 40: 60,000 units × 0.40 DLH per unit ………….

24,000

DLHs

LEC 90: 20,000 units × 0.80 DLH per unit ………….

16,000

DLHs

Total direct labor-hours ………………………………….

40,000

DLHs

Using direct labor-hours as the base, the predetermined manufacturing

overhead rate would be:

Direct materials ………………………

Direct labor …………………………...

Unit product cost ……………………

Problem 3-16A (continued)

2. Activity rates can be computed as follows:

Activity Cost Pool

(a)

Estimated

Overhead

Cost

(b)

Expected Activity

(a) ÷ (b)

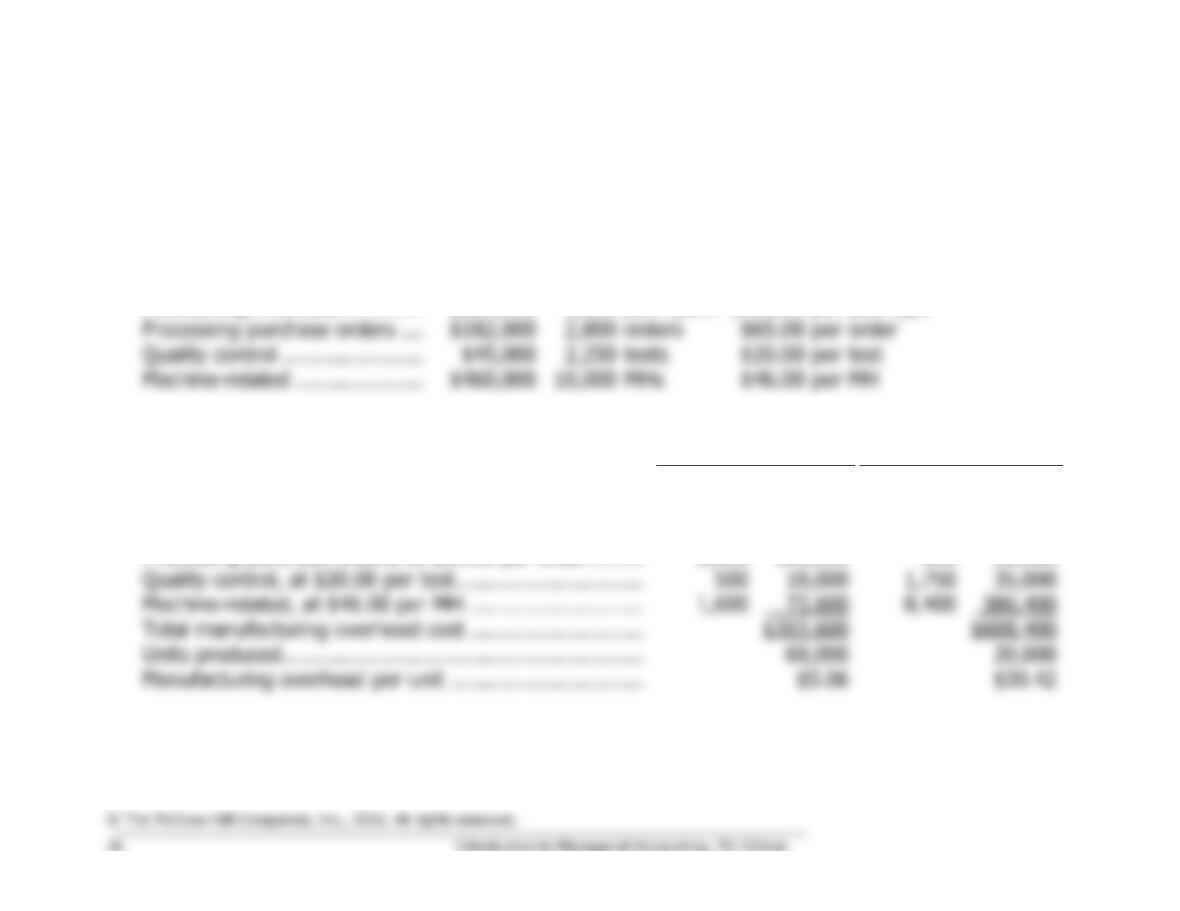

Activity Rate

Maintaining inventory ………….

$225,000

1,500

part types

$150.00

per part type

Processing purchase orders ….

orders

per order

Quality control …………………..

2,250

tests

per test

Machine-related …………………

$460,000

MHs

per MH

3 a.

LEC 40

LEC 90

Expected

Activity

Amount

Expected

Activity

Amount

Maintaining parts inventory, at $150.00 per part type..

600

$ 90,000

900

$135,000

Processing purchase orders, at $65.00 per order ………

2,000

130,000

800

52,000

Quality control, at $20.00 per test …………………………

500

Machine-related, at $46.00 per MH ……………………….

1,600

Total manufacturing overhead cost ……………………….

$303,600

$608,400

Units produced………………………………………………….

Manufacturing overhead per unit ………………………….

$30.42

Problem 3-16A (continued)

b. Using activity-based costing, the unit product costs would be:

4. Although the LEC 90 accounts for only 25% of the company’s total

production, it is responsible for 60% of the part types carried in

inventory and 84% of the machine-hours worked. It is also responsible

for 78% of the tests needed for quality control. These factors have been

Problem 3-17A (45 minutes)

1. a. When direct labor-hours are used to apply overhead costs to

products, other factors affecting the incurrence of overhead costs are

b. The unit product costs are computed as follows:

Model N

800 XL

Model N

500

2. a. Activity rates can be computed as follows:

Activity Cost Pool

(a)

Estimated

Overhead

Cost

(b)

Expected

Activity

(a) ÷ (b)

Activity Rate

Problem 3-17A (continued)

b. The unit product costs would now be computed as follows, starting

with the computation of the manufacturing overhead:

Model N 800

XL

Model N

500

Machine setups:

$1,200.00 per setup × 100 setups ….

$120,000

Special processing:

$60.00 per DLH × 12,000 DLHs ……..

720,000

Total overhead cost (a) ………………….

$825,000

Number of units produced (b) ………….

Model N 800

XL

Model N

500

Direct materials ……………………………..

$ 75.00

$25.00

Direct labor:

$18.00 per DLH × 3.0 DLHs …………..

Unit product cost …………………………..

3. It is important to note that, even under activity-based costing, 71% of

Machine setups (number of setups) …..

%

General factory (direct labor-hours) …..

Total …………………………..……………..

%

Problem 3-17A (continued)

Thus, the shift in overhead cost from the high-volume product Model N

500 to the low-volume product Model N 800 XL occurred as a result of

reassigning only 29% of the company’s overhead costs.

The increase in unit cost of Model N 800 XL can be explained as follows:

First, where possible, overhead costs have been traced to the products

Model N 800 XL:

Machine setup cost from ABC system (a)

$1,200

per setup

Average number of units per setup

3,000 units ÷ 100 setups (b) ……………

30

units per setup

Average setup cost per unit (a) ÷ (b) …..

$40.00

per unit

Model N 500:

per setup

60

units per setup

per unit