Chapter 7

Master Budgeting

Solutions to Questions

7-1 A budget is a detailed quantitative plan

for the acquisition and use of financial and other

7-2

1. Budgets communicate management’s

plans throughout the organization.

2. Budgets force managers to think about

and plan for the future. In the absence of the

necessity to prepare a budget, many managers

would spend all of their time dealing with day–

to-day emergencies.

7-3 Responsibility accounting is a system in

which a manager is held responsible for those

items of revenues and costs—and only those

7-4 A master budget represents a summary

of all of management’s plans and goals for the

future, and outlines the way in which these

plans are to be accomplished. The master

master budget usually also contains a budgeted

income statement, budgeted balance sheet, and

cash budget.

7-5 The level of sales impacts virtually every

other aspect of the firm’s activities. It

determines the production budget, cash

collections, cash disbursements, and selling and

administrative budget that in turn determine the

assumptions impact all supporting schedules and

the projected financial statements.

7-8 A self-imposed budget is one in which

recognized as members of the team whose

views and judgments are valued. (2) Budget

estimates prepared by front-line managers are

often more accurate and reliable than estimates

prepared by top managers who have less

intimate knowledge of markets and day-to-day

operations. (3) Motivation is generally higher

7-9 The direct labor budget and other

budgets can be used to forecast workforce

staffing needs. Careful planning can help a

company avoid erratic hiring and laying off of

The Foundational 15

1. The budgeted sales for July are computed as follows:

Unit sales (a) ………………………..

Selling price per unit (b) ………….

Total sales (a) × (b) ……………….

2. The expected cash collections for July are computed as follows:

July

Total cash collections …………….

3. The accounts receivable balance at the end of July is:

July sales (a) ………………………..

Percent uncollected (b) ……………

Accounts receivable (a) × (b) ……

4. The required production for July is computed as follows:

July

Budgeted sales in units ………………

10,000

Add desired ending inventory* …….

Total needs ……………………………..

Less beginning inventory** …………

Required production ………………….

The Foundational 15 (continued)

5. The raw material purchases for July are computed as follows:

July

Required production in units of finished goods ……………..

10,400

Units of raw materials needed per unit of finished goods ..

Units of raw materials needed to meet production …………

Add desired units of ending raw materials inventory* …….

Total units of raw materials needed …………………………...

Less units of beginning raw materials inventory** …………

Units of raw materials to be purchased ……………………….

6. The cost of raw material purchases for July is computed as follows:

Units of raw materials to be purchased (a)………

Unit cost of raw materials (b) ……………………….

Cost of raw materials to be purchased (a) × (b) .

7. The estimated cash disbursements for materials purchases in July is

computed as follows:

July

Total cash disbursements ………..

8. The accounts payable balance at the end of July is:

July purchases (a) ………………….

$105,800

Percent unpaid (b) …………………

Accounts payable (a) × (b) ………

The Foundational 15 (continued)

9. The estimated raw materials inventory balance at the end of July is

computed as follows:

Ending raw materials inventory (pounds) (a) ……

10. The estimated direct labor cost for July is computed as follows:

July

Required production in units …………..

Direct labor hours per unit ……………..

Total direct labor-hours needed (a)…..

11. The estimated unit product cost is computed as follows:

Quantity

Cost

Total

Direct materials …………………..

Direct labor ………………………..

Manufacturing overhead ……….

12. The estimated finished goods inventory balance at the end of July is

computed as follows:

Ending finished goods inventory in units (a) …….

Unit product cost (b) ………………………………….

Ending finished goods inventory (a) × (b) ……….

The Foundational 15 (continued)

13. The estimated cost of goods sold for July is computed as follows:

Unit sales (a) ……………………………………………

10,000

Unit product cost (b) ………………………………….

Total sales (a) …………………………………………..

14. The estimated selling and administrative expense for July is computed

as follows:

July

Budgeted unit sales ……………………………..

Total selling and administrative expenses …

15. The estimated net operating income for July is computed as follows:

Selling and administrative expenses (b) ………….

Net operating income (a) – (b) ……………………..

Exercise 7-1 (20 minutes)

1.

April

May

June

Total

February sales:

$230,000 × 10% …….

$ 23,000

$ 23,000

April sales: $300,000 ×

20%, 70%, 10% …….

$ 30,000

May sales: $500,000 ×

June sales: $200,000 ×

Total cash collections ….

$336,000

March sales: $260,000

2. Accounts receivable at June 30:

From May sales: $500,000 × 10% ……………………

From June sales: $200,000 × (70% + 10%) ………

Total accounts receivable at June 30 …………………

$210,000

Exercise 7-2 (10 minutes)

April

May

June

Quarter

Budgeted unit sales ……………..

50,000

75,000

90,000

215,000

Total needs ………………………..

Required production in units …..

Exercise 7-3 (15 minutes)

Quarter—Year 2

First

Second

Third

Fourth

Year

Required production in units of finished

goods ………………………………………………

60,000

90,000

150,000

100,000

400,000

Units of raw materials needed to meet

production ………………………………………..

180,000

270,000

450,000

300,000

Total units of raw materials needed ………….

Less units of beginning raw materials

Units of raw materials to be purchased ……..

Unit cost of raw materials ……………………….

Cost of raw materials to purchased …………..

Units of raw materials needed per unit of

Exercise 7-4 (20 minutes)

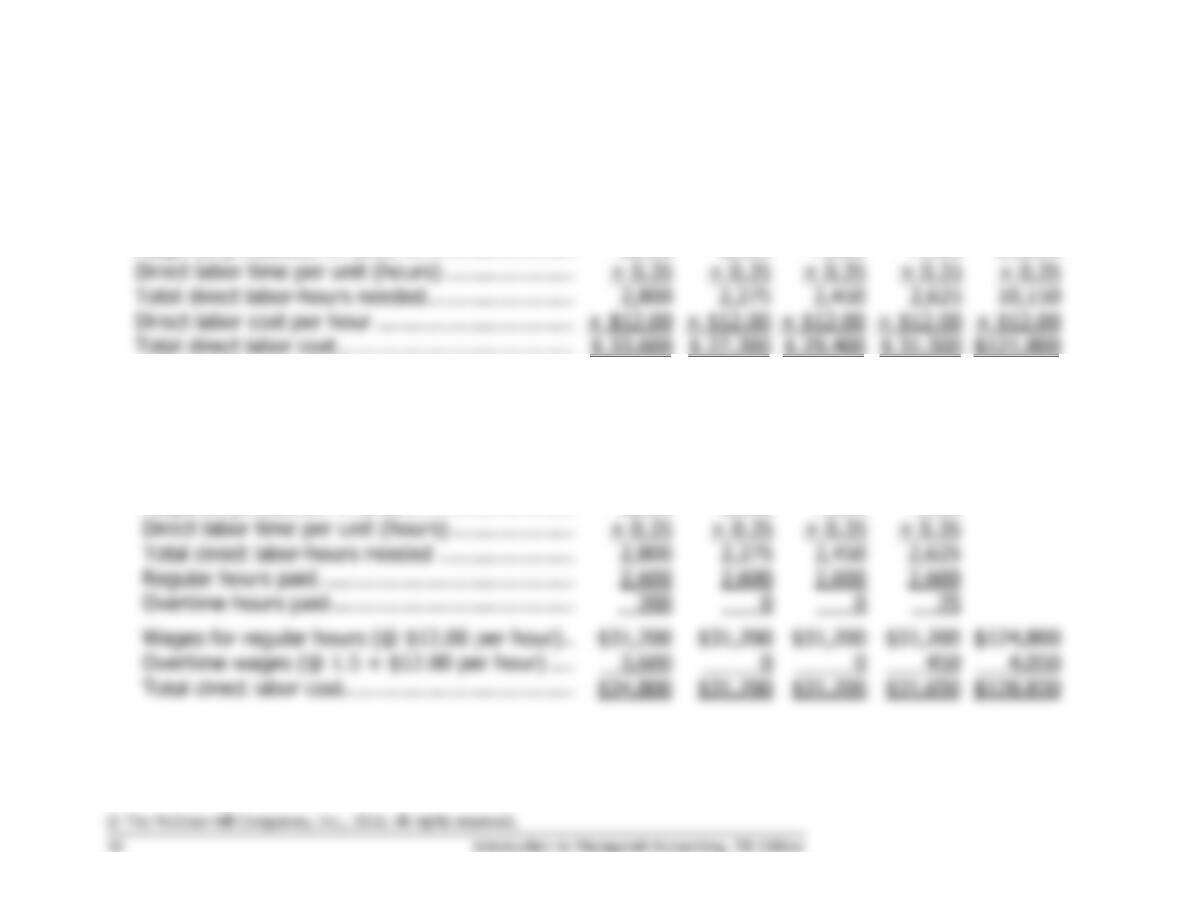

1. Assuming that the direct labor workforce is adjusted each quarter, the direct labor budget is:

1st

Quarter

2nd

Quarter

3rd

Quarter

4th

Quarter

Year

Required production in units ……………………….

8,000

6,500

7,000

7,500

29,000

Total direct labor-hours needed……………………

2,800

Direct labor cost per hour …………………………..

Total direct labor cost ………………………………..

2. Assuming that the direct labor workforce is not adjusted each quarter and that overtime wages are

paid, the direct labor budget is:

1st

Quarter

2nd

Quarter

3rd

Quarter

4th

Quarter

Year

Required production in units ………………………

8,000

6,500

7,000

7,500

Direct labor time per unit (hours) ………………..

Total direct labor-hours needed ………………….

2,800

2,275

2,450

2,625

Regular hours paid …………………………..………

2,600

2,600

2,600

2,600

Overtime hours paid …………………………………

0

25

Wages for regular hours (@ $12.00 per hour) ..

Overtime wages (@ 1.5 × $12.00 per hour) ….

Total direct labor cost ……………………………….

Exercise 7-5 (15 minutes)

1.

Yuvwell Corporation

Manufacturing Overhead Budget

1st

Quarter

2nd

Quarter

3rd

Quarter

4th

Quarter

Year

Budgeted direct labor-hours …………………………..

8,000

8,200

8,500

7,800

32,500

Variable manufacturing overhead rate ……………..

Variable manufacturing overhead ……………………

Fixed manufacturing overhead ……………………….

Total manufacturing overhead ……………………….

Less depreciation ………………………………………..

Cash disbursements for manufacturing overhead .

2.

Total budgeted manufacturing overhead for the year (a) …

$297,625

Budgeted direct labor-hours for the year (b) …………………

Predetermined overhead rate for the year (a) ÷ (b) ……….

Exercise 7-6 (15 minutes)

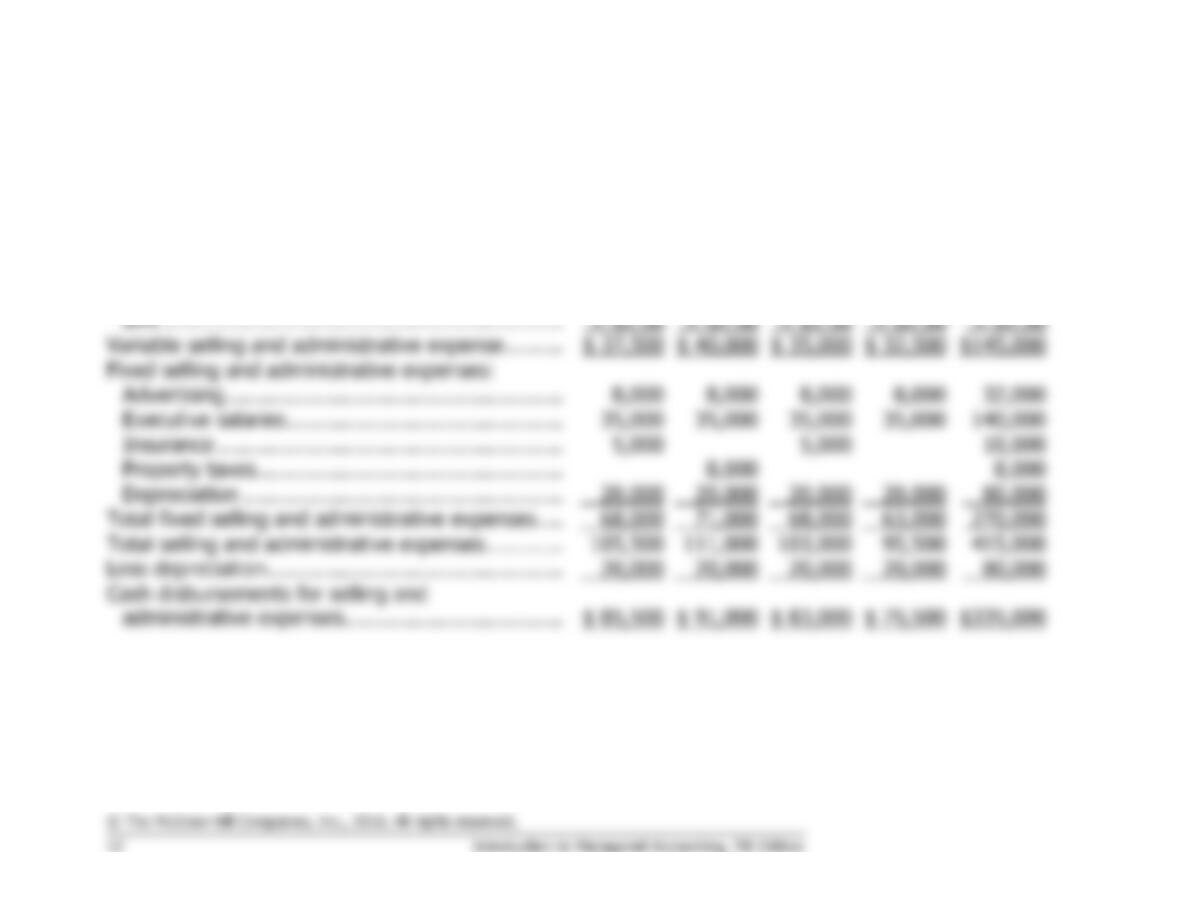

Weller Company

Selling and Administrative Expense Budget

1st

Quarter

2nd

Quarter

3rd

Quarter

4th

Quarter

Year

Budgeted unit sales …………………………..………..

15,000

16,000

14,000

13,000

58,000

Variable selling and administrative expense ………

Fixed selling and administrative expenses:

Total fixed selling and administrative expenses ….

Variable selling and administrative expense per

Exercise 7-7 (15 minutes)

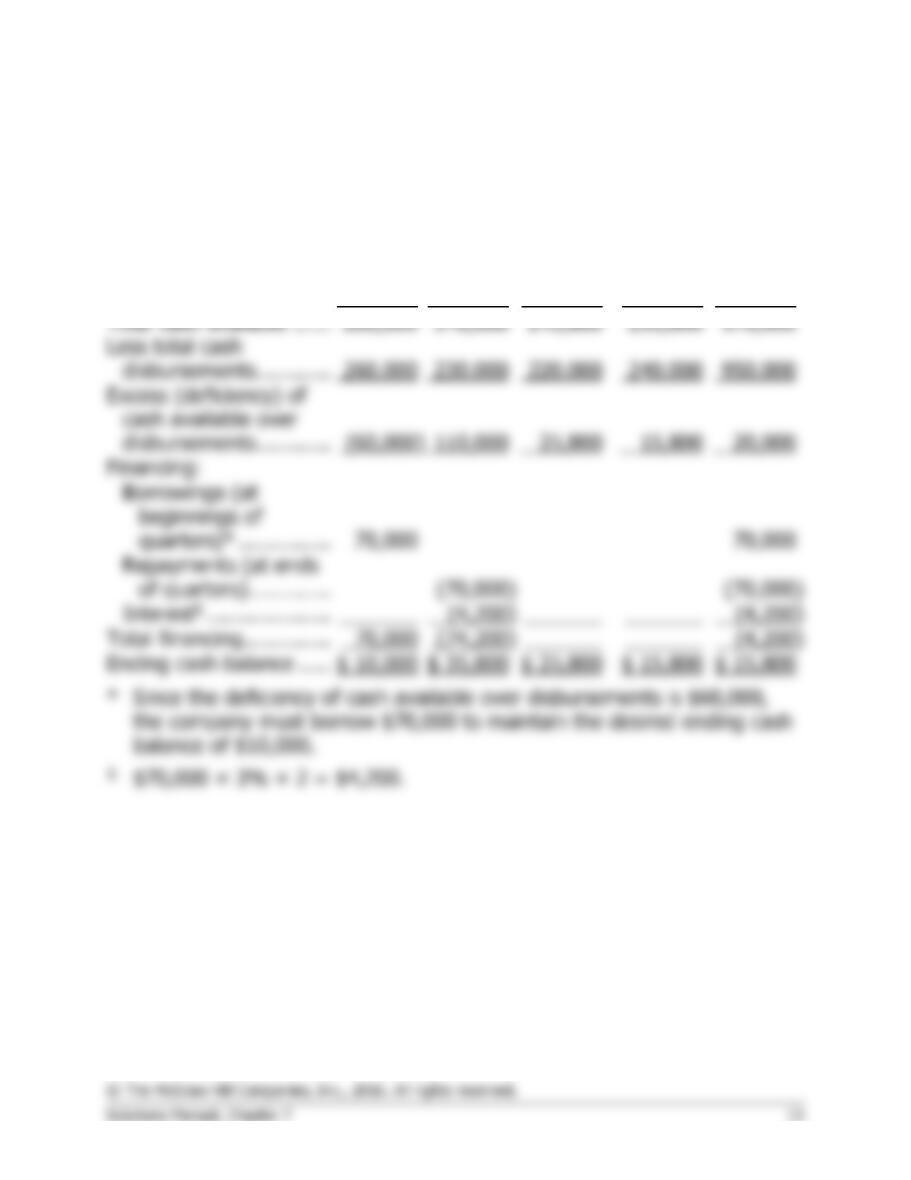

Garden Depot

Cash Budget

1st

Quarter

2nd

Quarter

3rd

Quarter

4th

Quarter

Year

Beginning cash balance .

$ 20,000

$ 10,000

$ 35,800

$ 25,800

$ 20,000

Total cash receipts ……..

180,000

330,000

210,000

230,000

950,000

Total cash available ……

260,000

Financing:

(4,200)

(4,200)

Total financing …………..

(74,200)

(4,200)

Ending cash balance …..

$ 10,000

Exercise 7-8 (10 minutes)

Gig Harbor Boating

Budgeted Income Statement

Sales (460 units × $1,950 per unit) ………………….

$897,000

Selling and administrative expenses* ………………..

Net operating income …………………………………….

Interest expense …………………………………………..

Net income ………………………………………………….

Exercise 7-9 (15 minutes)

Mecca Copy

Budgeted Balance Sheet

Assets

Current assets:

Cash* …………………………………………

$12,200

Accounts receivable ……………………….

Supplies inventory …………………………

Total current assets …………………………

Plant and equipment:

Equipment …………………………………..

Accumulated depreciation ……………….

Plant and equipment, net ………………….

Total assets …………………………..……….

Liabilities and Stockholders’ Equity

Current liabilities:

Accounts payable ………………………….

$ 1,800

Stockholders’ equity:

Common stock ……………………………..

$ 5,000

Retained earnings# ……………………….

Total stockholders’ equity ………………….

39,700

Total liabilities and stockholders’ equity ..

#

Retained earnings, beginning balance ..

Add net income …………………………….

Deduct dividends …………………………..

4,800

Retained earnings, ending balance ……

Exercise 7-10 (45 minutes)

1. Production budget:

July

August

Septem-

ber

October

Budgeted unit sales ……………

35,000

40,000

50,000

30,000

2. During July and August the company is building inventories in

anticipation of peak sales in September. Therefore, production exceeds

Exercise 7-10 (continued)

3. Direct materials budget:

July

August

Septem-

ber

Third

Quarter

Required production in units of finished goods …….

36,000

42,000

46,000

124,000

Units of raw materials needed per unit of finished

Exercise 7-11 (20 minutes)

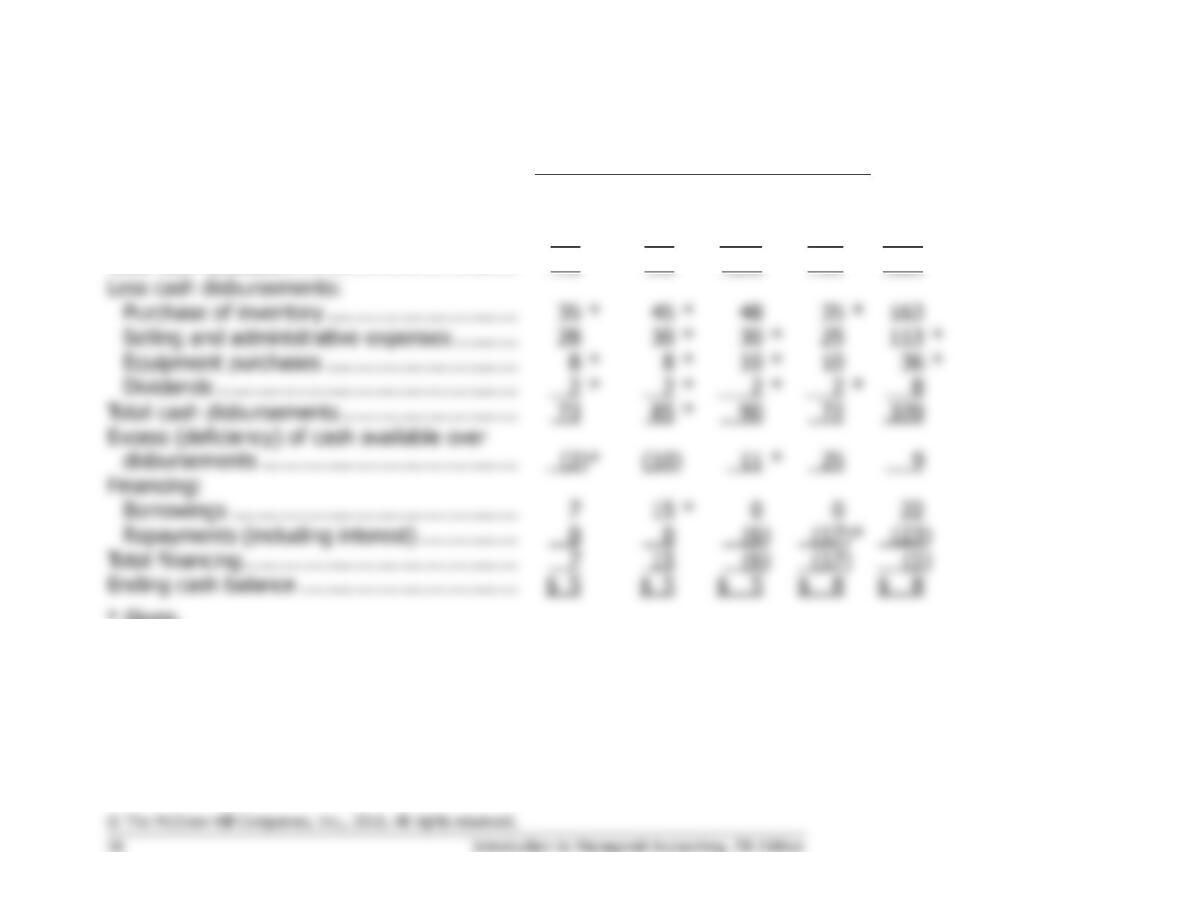

Quarter (000 omitted)

1

2

3

4

Year

Beginning cash balance ………………………….

$ 6

*

$ 5

$ 5

$ 5

$ 6

Add collections from customers ……………….

65

70

96

*

92

323

*

Total cash available ……………………………….

71

*

75

101

97

329

Less cash disbursements:

*

*

*

*

*

*

*

*

*

*

*

*

2

*

*

Total cash disbursements ……………………….

*

90

*

*

Financing:

*

*

Total financing ……………………………………..

(1)

Ending cash balance ……………………………..

$ 5

$ 5

$ 5

$ 8

$ 8

* Given.

Exercise 7-12 (30 minutes)

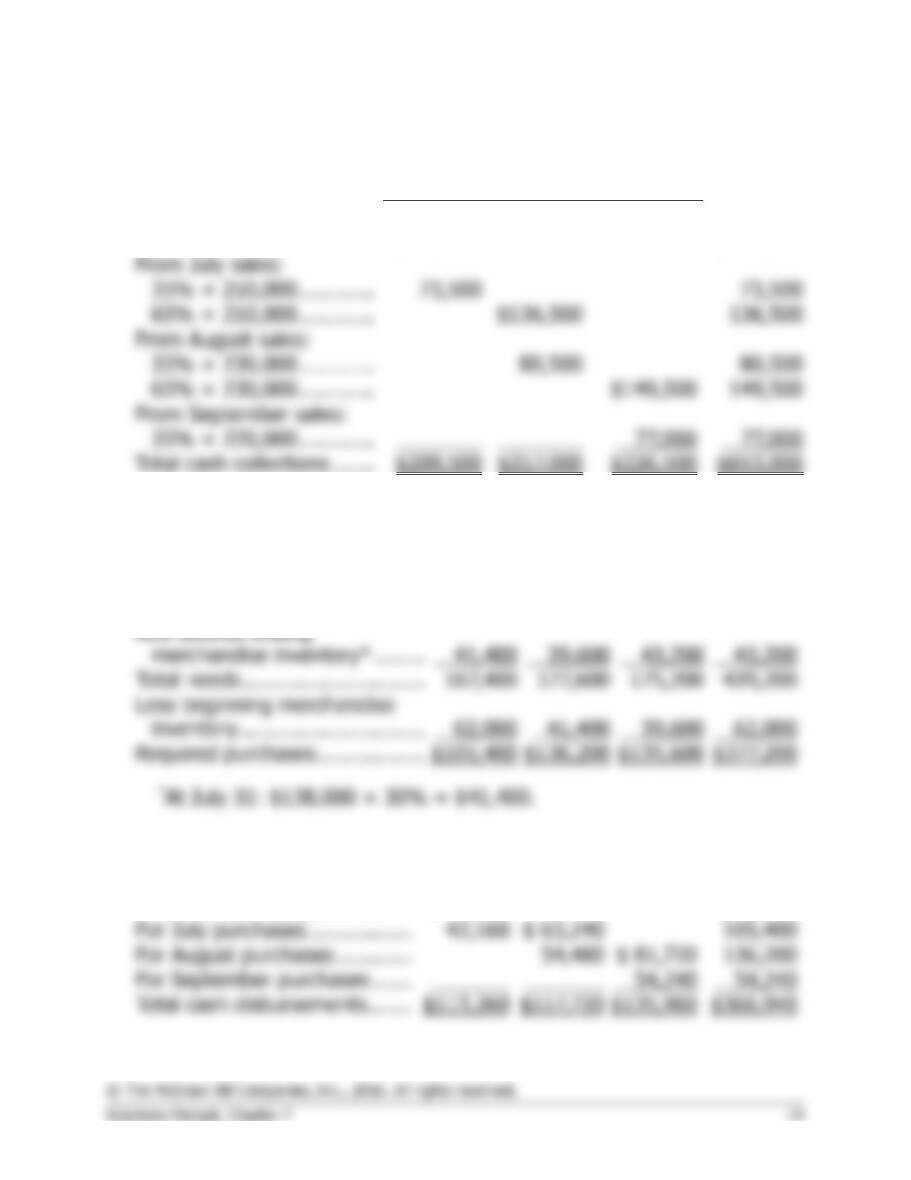

1. Schedule of expected cash collections:

Month

July

August

Sept.

Quarter

From accounts receivable .

$136,000

$136,000

From July sales:

From August sales:

From September sales:

Total cash collections …….

2. a. Merchandise purchases budget:

July

August

Sept.

Total

Budgeted cost of goods sold

(60% of sales)………………….

$126,000

$138,000

$132,000

$396,000

Total needs ………………………..

Required purchases ……………..

b. Schedule of cash disbursements for purchases:

July

August

Sept.

Total

From accounts payable ……….

$ 71,100

$ 71,100

For July purchases ……………..

For August purchases …………

For September purchases ……

Total cash disbursements …….

Exercise 7-12 (continued)

3.

Beech Corporation

Income Statement

For the Quarter Ended September 30

4.

Beech Corporation

Balance Sheet

September 30

Assets

Cash ($90,000 + $653,000 – $366,940 – ($55,000 ×

3)) ……………………………………………………………

$211,060