8-901

8-902

317.

Eliezrie Corporation makes a product with the following standard costs:

Standard

Quantity

or Hours

Standard

Price

or Rate

Standard

Cost

Per Unit

Direct

materials

6.5 kilos

$1.00 per

kilo

$6.50

Direct

labor

0.3 hours

$10.00

per hour

$3.00

Variable

overhead

0.3 hours

$4.00 per

hour

$1.20

In January the company’s budgeted production was 7,400 units but the actual production

was 7,500 units. The company used 45,580 kilos of the direct material and 2,030 direct

labor-hours to produce this output. During the month, the company purchased 48,500 kilos

of the direct material at a cost of $53,350. The actual direct labor cost was $18,473 and

the actual variable overhead cost was $7,714.

The company applies variable overhead on the basis of direct labor-hours. The direct

materials purchases variance is computed when the materials are purchased.

The labor efficiency variance for January is:

8-903

318.

Eliezrie Corporation makes a product with the following standard costs:

Standard

Quantity

or Hours

Standard

Price

or Rate

Standard

Cost

Per Unit

Direct

materials

6.5 kilos

$1.00 per

kilo

$6.50

Direct

labor

0.3 hours

$10.00

per hour

$3.00

Variable

overhead

0.3 hours

$4.00 per

hour

$1.20

In January the company’s budgeted production was 7,400 units but the actual production

was 7,500 units. The company used 45,580 kilos of the direct material and 2,030 direct

labor-hours to produce this output. During the month, the company purchased 48,500 kilos

of the direct material at a cost of $53,350. The actual direct labor cost was $18,473 and

the actual variable overhead cost was $7,714.

The company applies variable overhead on the basis of direct labor-hours. The direct

materials purchases variance is computed when the materials are purchased.

The labor rate variance for January is:

8-905

8-906

319.

Eliezrie Corporation makes a product with the following standard costs:

Standard

Quantity

or Hours

Standard

Price

or Rate

Standard

Cost

Per Unit

Direct

materials

6.5 kilos

$1.00 per

kilo

$6.50

Direct

labor

0.3 hours

$10.00

per hour

$3.00

Variable

overhead

0.3 hours

$4.00 per

hour

$1.20

In January the company’s budgeted production was 7,400 units but the actual production

was 7,500 units. The company used 45,580 kilos of the direct material and 2,030 direct

labor-hours to produce this output. During the month, the company purchased 48,500 kilos

of the direct material at a cost of $53,350. The actual direct labor cost was $18,473 and

the actual variable overhead cost was $7,714.

The company applies variable overhead on the basis of direct labor-hours. The direct

materials purchases variance is computed when the materials are purchased.

The variable overhead efficiency variance for January is:

8-907

320.

Eliezrie Corporation makes a product with the following standard costs:

Standard

Quantity

or Hours

Standard

Price

or Rate

Standard

Cost

Per Unit

Direct

materials

6.5 kilos

$1.00 per

kilo

$6.50

Direct

labor

0.3 hours

$10.00

per hour

$3.00

Variable

overhead

0.3 hours

$4.00 per

hour

$1.20

In January the company’s budgeted production was 7,400 units but the actual production

was 7,500 units. The company used 45,580 kilos of the direct material and 2,030 direct

labor-hours to produce this output. During the month, the company purchased 48,500 kilos

of the direct material at a cost of $53,350. The actual direct labor cost was $18,473 and

the actual variable overhead cost was $7,714.

The company applies variable overhead on the basis of direct labor-hours. The direct

materials purchases variance is computed when the materials are purchased.

The variable overhead rate variance for January is:

8-909

8-910

321.

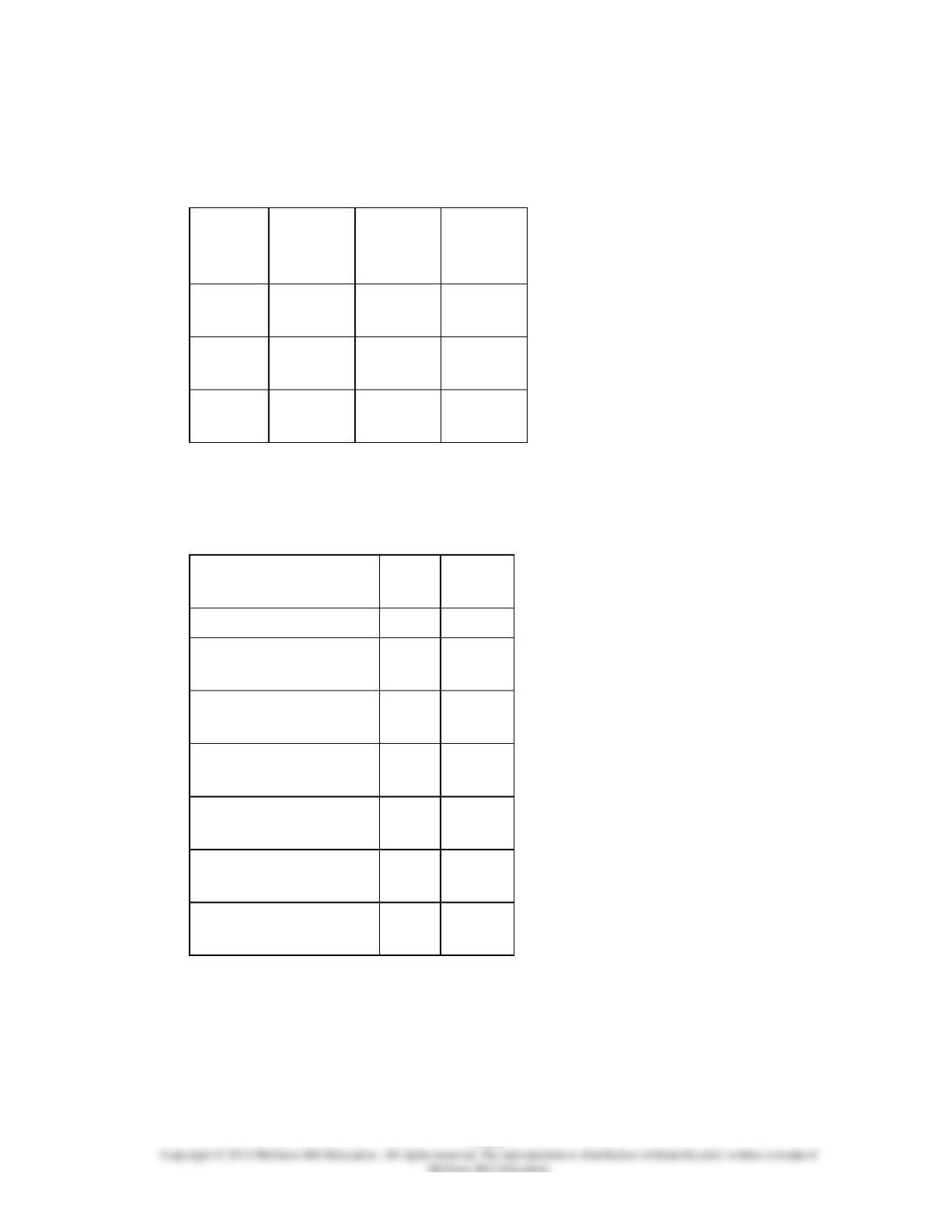

Oddo Corporation makes a product with the following standard costs:

8-911

8-912

322.

Oddo Corporation makes a product with the following standard costs:

Standard

Quantity

or Hours

Standard

Price or

Rate

Standard

Cost Per

Unit

Direct

materials

3.0

ounces

$7.00 per

ounce

$21.00

Direct

labor

0.7 hours

$20.00

per hour

$14.00

Variable

overhead

0.7 hours

$5.00 per

hour

$3.50

The company reported the following results concerning this product in December.

Originally budgeted

output

4,400

units

Actual output

4,200

units

Raw materials used in

production

12,820

ounces

Actual direct labor-

hours

3,160

hours

Purchases of raw

materials

14,500

ounces

Actual price of raw

materials

$6.80

per

ounce

Actual direct labor

rate

$18.30

per hour

Actual variable

overhead rate

$5.10

per hour

The company applies variable overhead on the basis of direct labor-hours. The direct

materials purchases variance is computed when the materials are purchased.

The materials price variance for December is:

8-914

323.

Oddo Corporation makes a product with the following standard costs:

Standard

Quantity

or Hours

Standard

Price or

Rate

Standard

Cost Per

Unit

Direct

materials

3.0

ounces

$7.00 per

ounce

$21.00

Direct

labor

0.7 hours

$20.00

per hour

$14.00

Variable

overhead

0.7 hours

$5.00 per

hour

$3.50

The company reported the following results concerning this product in December.

Originally budgeted

output

4,400

units

Actual output

4,200

units

Raw materials used in

production

12,820

ounces

Actual direct labor-

hours

3,160

hours

Purchases of raw

materials

14,500

ounces

Actual price of raw

materials

$6.80

per

ounce

Actual direct labor

rate

$18.30

per hour

Actual variable

overhead rate

$5.10

per hour

The company applies variable overhead on the basis of direct labor-hours. The direct

materials purchases variance is computed when the materials are purchased.

The labor efficiency variance for December is:

8-915

8-916

324.

Oddo Corporation makes a product with the following standard costs:

Standard

Quantity

or Hours

Standard

Price or

Rate

Standard

Cost Per

Unit

Direct

materials

3.0

ounces

$7.00 per

ounce

$21.00

Direct

labor

0.7 hours

$20.00

per hour

$14.00

Variable

overhead

0.7 hours

$5.00 per

hour

$3.50

The company reported the following results concerning this product in December.

Originally budgeted

output

4,400

units

Actual output

4,200

units

Raw materials used in

production

12,820

ounces

Actual direct labor-

hours

3,160

hours

Purchases of raw

materials

14,500

ounces

Actual price of raw

materials

$6.80

per

ounce

Actual direct labor

rate

$18.30

per hour

Actual variable

overhead rate

$5.10

per hour

The company applies variable overhead on the basis of direct labor-hours. The direct

materials purchases variance is computed when the materials are purchased.

The labor rate variance for December is:

8-917

8-918

325.

Oddo Corporation makes a product with the following standard costs:

Standard

Quantity

or Hours

Standard

Price or

Rate

Standard

Cost Per

Unit

Direct

materials

3.0

ounces

$7.00 per

ounce

$21.00

Direct

labor

0.7 hours

$20.00

per hour

$14.00

Variable

overhead

0.7 hours

$5.00 per

hour

$3.50

The company reported the following results concerning this product in December.

Originally budgeted

output

4,400

units

Actual output

4,200

units

Raw materials used in

production

12,820

ounces

Actual direct labor-

hours

3,160

hours

Purchases of raw

materials

14,500

ounces

Actual price of raw

materials

$6.80

per

ounce

Actual direct labor

rate

$18.30

per hour

Actual variable

overhead rate

$5.10

per hour

The company applies variable overhead on the basis of direct labor-hours. The direct

materials purchases variance is computed when the materials are purchased.

The variable overhead efficiency variance for December is:

8-919

8-920

326.

Oddo Corporation makes a product with the following standard costs:

Standard

Quantity

or Hours

Standard

Price or

Rate

Standard

Cost Per

Unit

Direct

materials

3.0

ounces

$7.00 per

ounce

$21.00

Direct

labor

0.7 hours

$20.00

per hour

$14.00

Variable

overhead

0.7 hours

$5.00 per

hour

$3.50

The company reported the following results concerning this product in December.

Originally budgeted

output

4,400

units

Actual output

4,200

units

Raw materials used in

production

12,820

ounces

Actual direct labor-

hours

3,160

hours

Purchases of raw

materials

14,500

ounces

Actual price of raw

materials

$6.80

per

ounce

Actual direct labor

rate

$18.30

per hour

Actual variable

overhead rate

$5.10

per hour

The company applies variable overhead on the basis of direct labor-hours. The direct

materials purchases variance is computed when the materials are purchased.

The variable overhead rate variance for December is: