Chapter 11

Capital Budgeting Decisions

Solutions to Questions

11-1 A capital budgeting screening decision is

concerned with whether a proposed investment

11-2 The “time value of money” refers to the

fact that a dollar received today is more valuable

than a dollar received in the future simply

because a dollar received today can be invested

to yield more than a dollar in the future.

11-3 Discounting is the process of computing

the present value of a future cash flow.

11-4 Accounting net income is based on

accruals rather than on cash flows. Both the net

present value and internal rate of return

methods focus on cash flows.

11-5 Unlike other common capital budgeting

methods, discounted cash flow methods

11-6 Net present value is the present value of

11-7 One assumption is that all cash flows

11-8 No. The cost of capital is not simply the

interest paid on long-term debt. The cost of

value method, the cost of capital is used as the

discount rate. If the net present value of the

project is positive, then the project is acceptable

because its rate of return is greater than the

cost of capital. (b) In the case of the internal

rate of return method, the cost of capital is

compared to a project’s internal rate of return. If

the project’s internal rate of return is greater

present value of a given future cash flow

decreases. For example, the present value factor

for a discount rate of 12% for cash to be

received ten years from now is 0.322, whereas

the present value factor for a discount rate of

14% over the same period is 0.270. If the cash

to be received in ten years is $10,000, the

present value in the first case is $3,220, but only

discount rate) is zero. The internal rate of return

would be less than 14% if the net present value

11-12 The project profitability index is

computed by dividing the net present value of

11-13 The payback period is the length of time

for an investment to fully recover its initial cost

investment proposals. The payback method is

useful when a company has cash flow problems.

dollar received today. Furthermore, the payback

method ignores all cash flows that occur after

the initial investment has been recovered.

The Foundational 15

1. The depreciation expense of $535,000 is the only non-cash expense.

2. The annual net cash inflows are computed as follows:

3. The present value of the annual net cash inflows is computed as

follows:

4. The present value of the equipment’s salvage value is computed as

follows:

Factor

5. The project’s net present value is computed as follows:

Item

Year(s)

Amount of

Cash Flows

14%

Factor

Present Value

of Cash Flows

Cost of the equipment ……………

Now

$(2,975,000)

1.000

$(2,975,000)

Annual net cash inflows ………….

3.433

The Foundational 15 (continued)

6. The project profitability index for the project is:

Project

7. The payback period is determined as follows:

Year

Investment

Cash

Inflow

Unrecovered

Investment

1

$2,975,000

$1,000,000

$1,975,000

8. The simple rate of return is computed as follows:

The Foundational 15 (continued)

9. If the discount rate was 16% instead of 14% the project’s net present

value would be lower because the discount factors would be smaller.

10. The payback period would be the same because the initial investment

11. The net present value would be higher because a higher salvage value

translates into a larger cash inflow at the end of five years. If we hold

12. The first step in computing the simple rate of return is to realize that if

the salvage value increases by $200,000, then the annual depreciation

expense will decrease by $40,000 ($200,000 ÷ 5 year useful life). The

The Foundational 15 (continued)

13. The new contribution margin would be $2,735,000 × 55% =

$1,504,250. The new net operating income would be $1,504,250 –

$1,270,000 = $234,250. The remaining calculations are as follows:

Net operating income …………………………..

$234,250

Add: Noncash deduction for depreciation ….

Year(s)

Cost of the equipment ……………

1.000

Annual net cash inflows ………….

1-5

3.433

14. The payback period is computed as follows:

Year

Investment

Cash

Inflow

Unrecovered

Investment

1

$2,975,000

$769,250

$2,205,750

2

$769,250

$1,436,500

3

$769,250

4

$769,250

15. The simple rate of return is computed as follows:

Exercise 11-1 (10 minutes)

1. The payback period is determined as follows:

Year

Investment

Cash Inflow

Unrecovered

Investment

1

$15,000

$1,000

$14,000

6

$6,000

7

$5,000

2. Because the investment is recovered prior to the last year, the amount

of the cash inflow in the last year has no effect on the payback period.

Exercise 11-2 (10 minutes)

1.

Now

1

2

3

4

5

Purchase of machine ………………….

$(27,000)

Reduced operating costs …………….

________

$7,000

$7,000

$7,000

Total cash flows (a) …………………..

$(27,000)

$7,000

$7,000

$7,000

Discount factor (12%) (b) …………..

Present value (a)×(b) ………………..

$(27,000)

$6,251

$5,579

$4,984

Net present value ……………………..

$(1,765)

2.

Item

Cash

Flow

Years

Total

Cash

Flows

Annual cost savings ..

$7,000

5

$ 35,000

Initial investment …..

1

Net cash flow ………..

Exercise 11-3 (10 minutes)

1. The project profitability index for each proposal is:

Proposal

Number

Net Present

Value

(a)

Investment

Required

(b)

Project Profitability

Index

(a) (b)

0.38

C

0.50

D

0.33

2. The ranking is:

Proposal

Number

Project Profitability

Index

C

0.50

D

0.33

Exercise 11-4 (10 minutes)

This is a cost reduction project, so the simple rate of return would be

computed as follows:

Operating cost of old machine ………………..

$ 30,000

Annual incremental net operating income …

$ 6,000

Cost of the new machine ………………………

Scrap value of old machine ……………………

40,000

Exercise 11–5 (15 minutes)

Project A:

Now

1

2

3

4

5

6

Purchase of equipment …..

$(100,000)

Annual cash inflows ………

$21,000

$21,000

$21,000

$21,000

Salvage value ………………

Total cash flows (a) ………

$(100,000)

$21,000

$21,000

Discount factor (14%) (b)

Present value (a)×(b) ……

$12,432

$10,899

Net present value …………

Project B:

Now

1

2

3

4

5

6

Working capital invested ..

$(100,000)

Annual cash inflows ………

$16,000

$16,000

$16,000

$16,000

$16,000

$ 16,000

Working capital released ..

Total cash flows (a) ………

$16,000

$16,000

$16,000

$16,000

$16,000

Discount factor (14%) (b)

Present value (a)×(b) ……

$12,304

Net present value …………

Exercise 11-6 (15 minutes)

1. Computation of the annual cash inflow associated with the new

electronic games:

Net operating income ……………………………………

$40,000

Add noncash deduction for depreciation …………….

35,000

2. The simple rate of return would be:

Exercise 11-7 (20 minutes)

1. The net present value is computed as follows:

Now

1

2

3

4

5

Purchase of

equipment …………….

$(3,000,000)

Sales ……………………

$2,500,000

Variable expenses …..

Total cash flows (a) ..

$(3,000,000)

Discount factor (b) ….

Present value

2. The simple rate of return would be:

3. The company would want Derrick to pursue the investment opportunity because it has a positive net

present value of $17,700. However, Derrick might be inclined to reject the opportunity because its

Exercise 11–8 (10 minutes)

Now

1

2

3

Purchase of stock…………………………

$(13,000)

Annual cash dividend ……………………

Sale of stock …………………………..…..

Total cash flows (a) ……………………..

$(13,000)

Discount factor (14%) (b) ……………..

Present value (a)×(b) …………………..

$(13,000)

Net present value ………………………..

Problem 11-9 (30 minutes)

1. The project profitability index is computed as follows:

Project

Net Present

Value

(a)

Investment

Required

(b)

Project

Profitability

Index

(a) ÷ (b)

A …………

$44,323

$160,000

0.28

B …………

$42,000

$135,000

0.31

C …………

$35,035

$100,000

0.35

D …………

$38,136

$175,000

0.22

2. a., b., and c.

Net Present

Value

Project

Profitability

Index

Internal Rate

of Return

First preference ……..

A

C

D

Second preference ….

B

B

C

Third preference …….

A

A

Fourth preference …..

C

B

Problem 11-9 (continued)

3. Oxford Company’s opportunities for reinvesting funds as they are

released from a project will determine which ranking is best. The

internal rate of return method assumes that any released funds are

reinvested at the rate of return shown for a project. This means that

funds released from project D would have to be reinvested in another

Exercise 11-10 (15 minutes)

1. The payback period is:

2. The simple rate of return would be computed as follows:

Annual cost savings ………………………………………..

$90,000

Less annual depreciation ($432,000 ÷ 12 years) ……

36,000

Annual incremental net operating income ……………

$54,000

Exercise 11–11 (10 minutes)

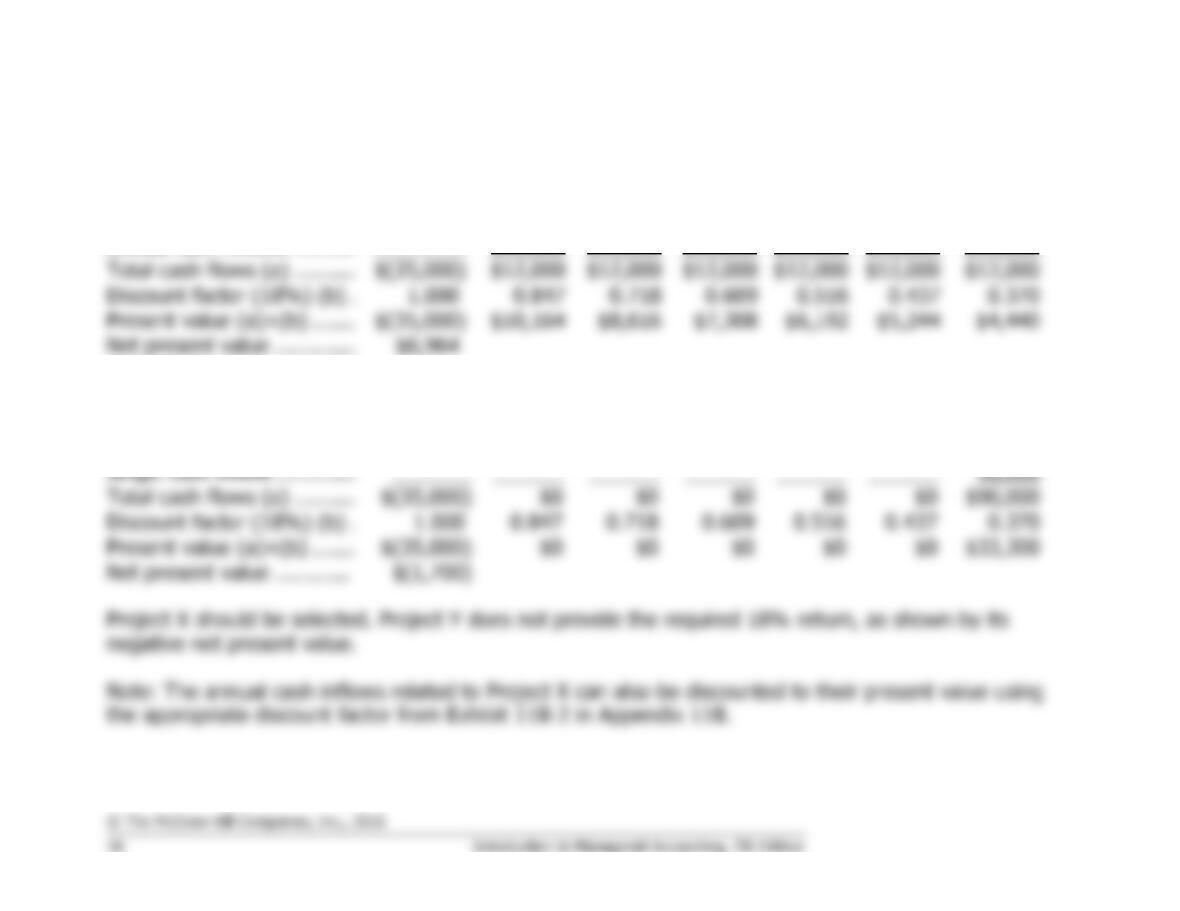

Project X:

Now

1

2

3

4

5

6

Initial investment …………..

$(35,000)

Annual cash inflows ……….

________

$12,000

$12,000

$12,000

$12,000

$12,000

$12,000

Total cash flows (a) ……….

$(35,000)

$12,000

$12,000

$12,000

$12,000

$12,000

$12,000

Discount factor (18%) (b) .

Present value (a)×(b) …….

$(35,000)

$10,164

$6,192

$5,244

Net present value ………….

Project Y:

Now

1

2

3

4

5

6

Initial investment …………..

$(35,000)

Single cash inflow ………….

______

______

Total cash flows (a) ……….

$(35,000)

Discount factor (18%) (b) .

Present value (a)×(b) …….

$(35,000)

Net present value ………….

Problem 11-12A (20 minutes)

Now

1

2

3

4

Purchase of equipment ……….

$(275,000)

Working capital investment …

(100,000)

Annual net cash receipts …….

$120,000

$120,000

$120,000

$120,000

Road construction ……………..

Working capital released …….

Salvage value of equipment …

_______

Total cash flows (a) …………..

$(375,000)

$120,000

$120,000

$80,000

$285,000

Discount factor (20%) (b) …..

Present value (a)×(b) ………..

$46,320

$137,370

Net present value ……………..

Problem 11-13A (20 minutes)

1. The net present value is computed as follows:

Now

1

2

3

4

5

Purchase of

equipment …………….

$(3,500,000)

Sales ……………………

$3,400,000

$3,400,000

$3,400,000

$3,400,000

$3,400,000

Variable expenses …..

Out-of-pocket costs …

Total cash flows (a) ..

Discount factor (b) ….

Present value

(a)×(b) ………………..

$(3,500,000)

Net present value …..