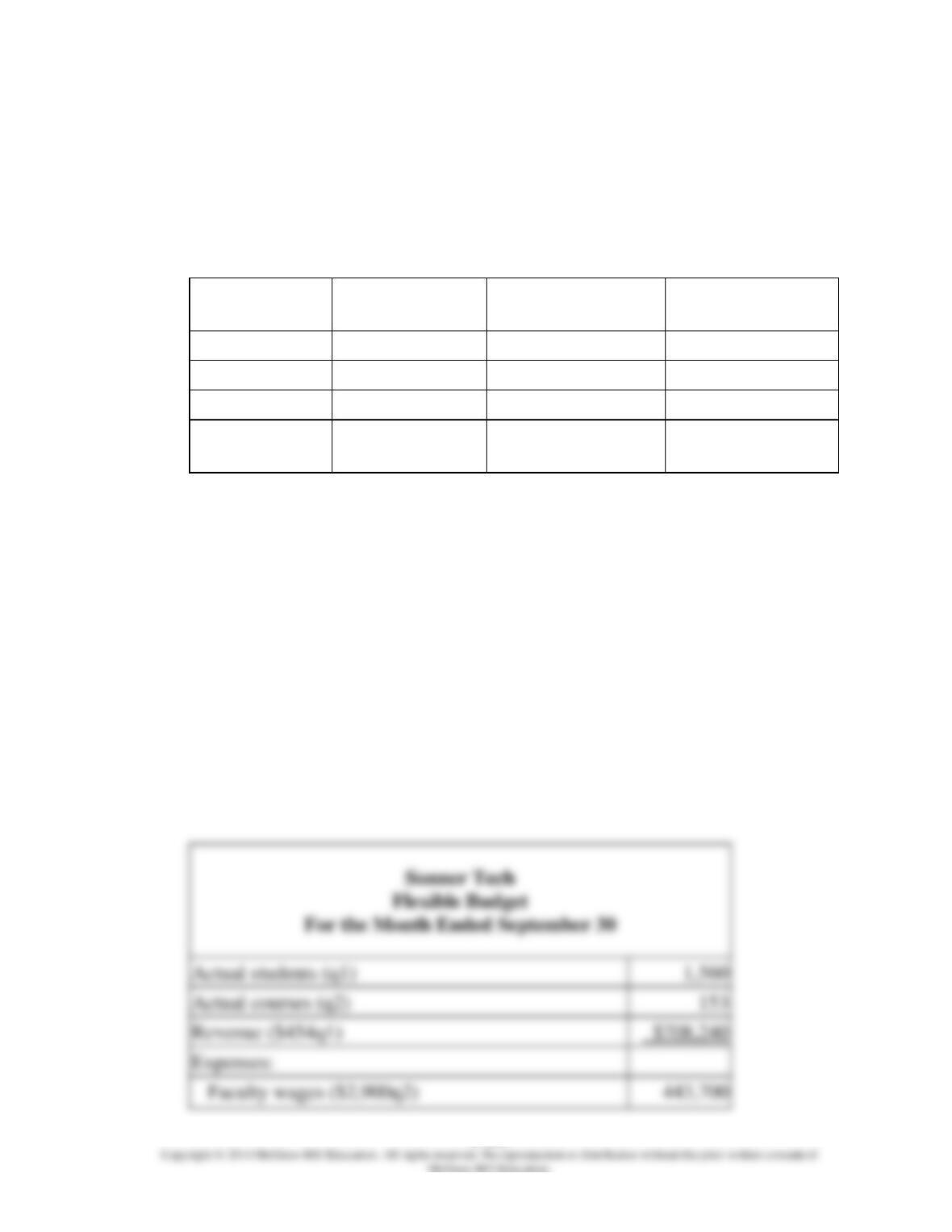

Expenses:

Faculty wages ($2,400q2)

331,200

Course supplies ($69q1 +$46q2)

103,638

Administrative expenses ($33,100

+$15q1 +$33q2)

58,804

8-1042

401.

Sonner Tech is a for-profit vocational school. The school bases its budgets on two

measures of activity (i.e., cost drivers), namely student and course. The school uses the

following data in its budgeting:

Fixed element

per month

Variable element

per student

Variable element

per course

Revenue

$0

$454

$0

Faculty wages

$0

$0

$2,900

Course supplies

$0

$77

$13

Administrative

expenses

$64,400

$17

$35

Actual students (q1)

Actual courses (q2)

Revenue ($454q1)

In September, the school budgeted for 1,760 students and 156 courses. The actual

activity for the month was 1,560 students and 153 courses.

Required:

Prepare the school’s flexible budget for the actual level of activity in September.

8-1043

8-1044

402.

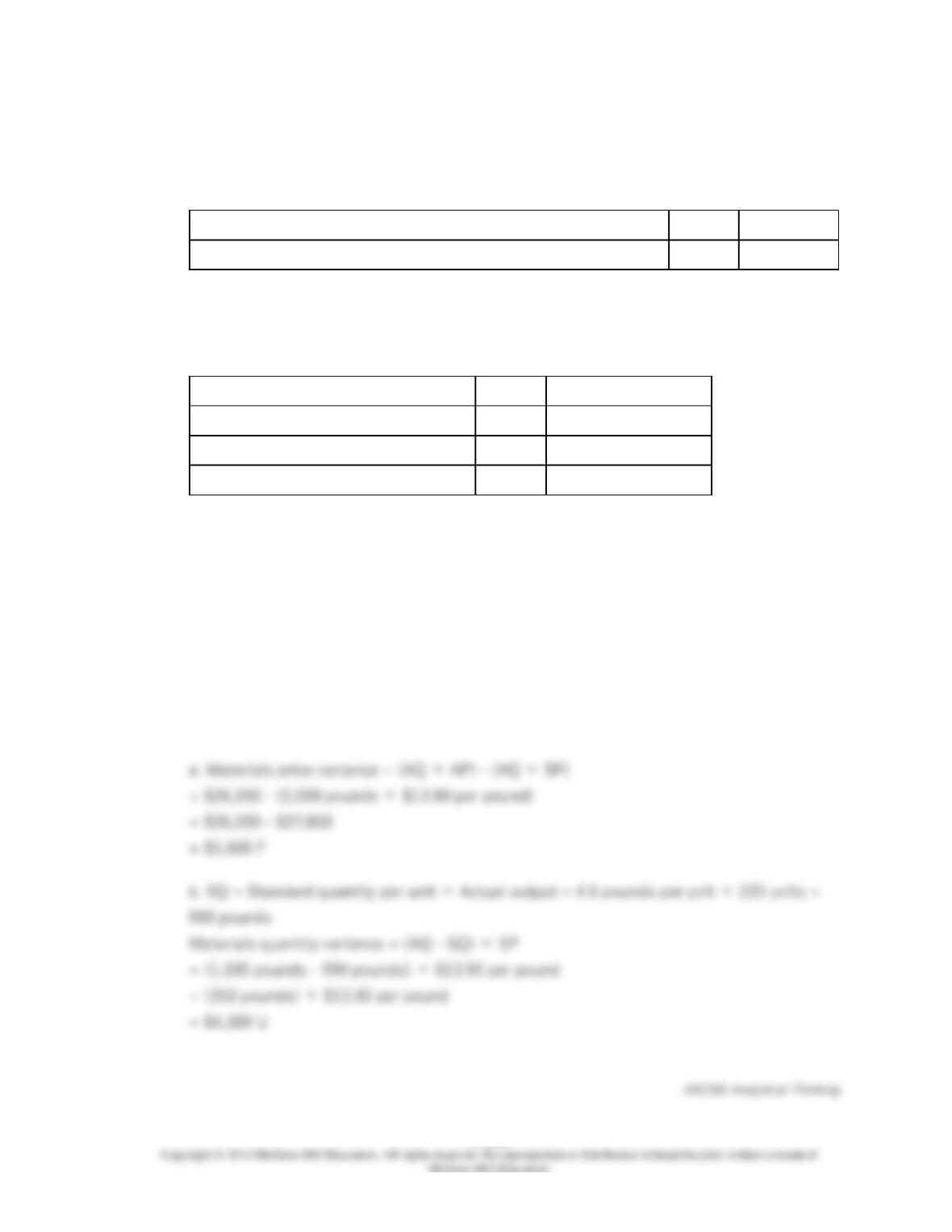

The standards for product K17 call for 5.0 meters of a raw material that costs $19.10 per

meter. Last month, 2,700 meters of the raw material were purchased for $51,435. The

actual output of the month was 460 units of product K17. A total of 2,500 meters of the

raw material were used to produce this output.

The direct materials purchases variance is computed when the materials are purchased.

Required:

a. What is the materials price variance for the month?

b. What is the materials quantity variance for the month?

8-1045

403.

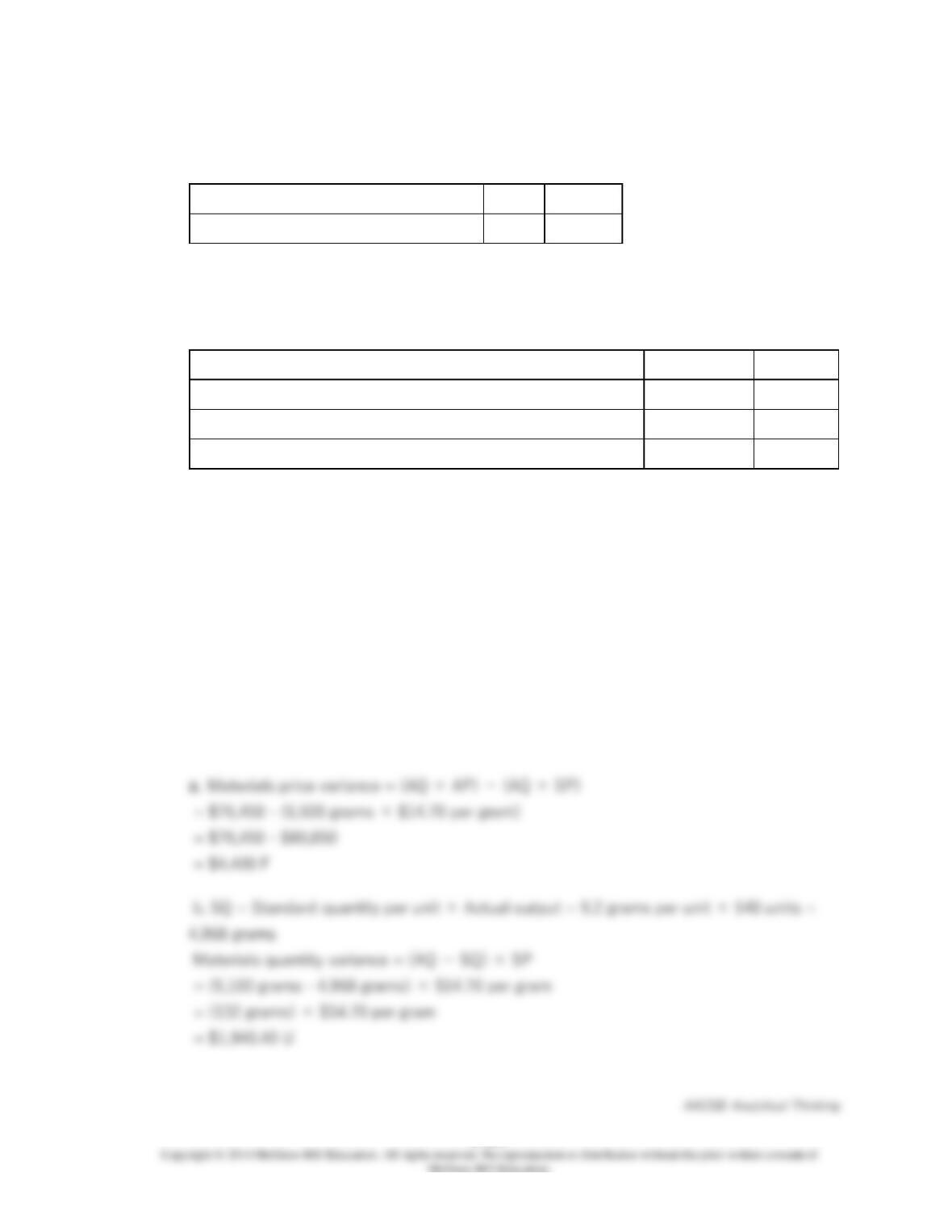

The following standards have been established for a raw material used to make product

I92:

Standard quantity of the material per unit of output

4.5

pounds

Standard price of the material

$13.90

per pound

The following data pertain to a recent month’s operations:

Actual material purchased

2,000

pounds

Actual cost of material purchased

$26,200

Actual material used in production

1,300

pounds

Actual output

220

units of product I92

The direct materials purchases variance is computed when the materials are purchased.

Required:

a. What is the materials price variance for the month?

b. What is the materials quantity variance for the month?

8-1046

404.

Sizzle Company uses a standard cost system to collect costs related to the production of

its “No-Stick” lawn chairs. The direct material for the chairs is teflon. Sizzle uses a

standard direct material cost of $40.00 per chair (0.8 pounds of teflon × $50.00 per

pound). During April, Sizzle purchased 2,100 pounds of teflon for $106,575. Sizzle used

1,750 pounds of this teflon in April to produce 1,800 lawn chairs.

Required:

Calculate Sizzle’s materials price and materials quantity variances for April.

8-1047

405.

The following materials standards have been established for a particular product:

Standard quantity per unit of output

9.2

grams

Standard price

$14.70

per gram

The following data pertain to operations concerning the product for the last month:

Actual materials purchased

5,500

grams

Actual cost of materials purchased

$76,450

Actual materials used in production

5,100

grams

Actual output

540

units

The direct materials purchases variance is computed when the materials are purchased.

Required:

a. What is the materials price variance for the month?

b. What is the materials quantity variance for the month?

8-1048

8-1049

406.

Zee Corporation has developed the following cost standards for the production of its

leather backpacks:

Standard Cost Per

Backpack

Leather (0.9 yards × $22 per yard)

$19.80

Direct labor (1.3 hours × $9.00 per hour)

$11.70

Variable overhead (1.3 hours × $15.00 per

hour)

$19.50

Variable overhead at Zee is applied on the basis of direct labor hours. The actual results

for last month were as follows:

Number of backpacks

produced

15,000

Direct labor hours incurred

18,800

Yards of leather purchased

14,500

Yards of leather used in

production

14,100

Cost of leather purchased

$306,675

Direct labor cost

$159,800

Variable overhead cost

$285,760

The direct materials purchases variance is computed when the materials are purchased.

Required:

Compute the following variances for Zee.

a. Materials price variance.

b. Materials quantity variance.

c. Labor efficiency variance.

d. Variable overhead rate variance.

8-1050

8-1051

407.

Rardin Corporation makes a product with the following standard costs:

Standard

Quantity

or Hours

Standard

Price or

Rate

Direct

materials

7.4

ounces

$8.00 per

ounce

Direct

labor

0.3 hours

$16.00

per hour

Variable

overhead

0.3 hours

$7.00 per

hour

The company reported the following results concerning this product in July.

Actual output

2,200

units

Raw materials used in production

16,420

ounces

Purchases of raw materials

17,900

ounces

Actual direct labor-hours

720

hours

Actual cost of raw materials purchases

$141,410

Actual direct labor cost

$12,528

Actual variable overhead cost

$5,112

The company applies variable overhead on the basis of direct labor-hours. The direct

materials purchases variance is computed when the materials are purchased.

Required:

a. Compute the materials quantity variance.

b. Compute the materials price variance.

c. Compute the labor efficiency variance.

d. Compute the labor rate variance.

8-1052

e. Compute the variable overhead efficiency variance.

f. Compute the variable overhead rate variance.

8-1053

8-1054

408.

Graybeal Corporation makes a product with the following standard costs:

Standard Quantity or Hours

Standard Price or Rate

Direct materials

4.3 ounces

$6.00 per ounce

Direct labor

0.7 hours

$21.00 per hour

Variable overhead

0.7 hours

$7.00 per hour

The company reported the following results concerning this product in March.

Actual output

3,500

units

Raw materials used in production

14,710

ounces

Actual direct labor-hours

2,270

hours

Purchases of raw materials

16,700

ounces

Actual price of raw materials

$5.80

per ounce

Actual direct labor rate

$21.90

per hour

Actual variable overhead rate

$7.30

per hour

The materials price variance is recognized when materials are purchased. Variable

overhead is applied on the basis of direct labor-hours.

Required:

a. Compute the materials quantity variance.

b. Compute the materials price variance.

c. Compute the labor efficiency variance.

d. Compute the labor rate variance.

e. Compute the variable overhead efficiency variance.

f. Compute the variable overhead rate variance.

8-1055

8-1056

409.

Smyer Corporation makes a product with the following standard costs:

Standard

Quantity

or Hours

Standard

Price or

Rate

Standard

Cost Per

Unit

Direct

materials

7.1

pounds

$5.00 per

pound

$35.50

Direct

labor

0.8 hours

$17.00

per hour

$13.60

Variable

overhead

0.8 hours

$7.00 per

hour

$5.60

The company reported the following results concerning this product in July.

Originally budgeted output

4,700

units

Actual output

4,500

units

Raw materials used in production

34,150

pounds

Actual direct labor-hours

3,610

hours

Purchases of raw materials

36,500

pounds

Actual price of raw materials

$5.10

per pound

Actual direct labor rate

$18.10

per hour

Actual variable overhead rate

$6.70

per hour

The materials price variance is recognized when materials are purchased. Variable

overhead is applied on the basis of direct labor-hours.

Required:

a. Compute the materials quantity variance.

b. Compute the materials price variance.

c. Compute the labor efficiency variance.

8-1057

d. Compute the labor rate variance.

e. Compute the variable overhead efficiency variance.

f. Compute the variable overhead rate variance.

8-1058

8-1059

410.

Moates Corporation makes a product with the following standard costs:

Standard

Quantity

or Hours

Standard

Price or

Rate

Direct

materials

6.5 kilos

$1.00 per

kilo

Direct

labor

0.2 hours

$21.00

per hour

Variable

overhead

0.2 hours

$7.00 per

hour

In January the company produced 5,800 units using 38,740 kilos of the direct material and

1,110 direct labor-hours. During the month, the company purchased 41,000 kilos of the

direct material at a total cost of $49,200. The actual direct labor cost for the month was

$20,979 and the actual variable overhead cost was $6,993. The company applies variable

overhead on the basis of direct labor-hours. The direct materials purchases variance is

computed when the materials are purchased.

Required:

a. Compute the materials quantity variance.

b. Compute the materials price variance.

c. Compute the labor efficiency variance.

d. Compute the labor rate variance.

e. Compute the variable overhead efficiency variance.

f. Compute the variable overhead rate variance.