8-461

43.

Akey Hospital bases its budgets on patient-visits. The hospital’s static budget for March

appears below:

Budgeted number of patient-visits

2,700

Budgeted variable overhead costs:

Supplies (@ $3.90 per patient-visit)

$10,530

Laundry (@ $9.70 per patient-visit)

26,190

Total variable overhead cost

36,720

Budgeted fixed overhead costs:

Wages and salaries

15,660

Occupancy costs

35,640

Total fixed overhead cost

51,300

Total budgeted overhead cost

$88,020

The total overhead cost at an activity level of 3,000 patient-visits per month should be:

44.

Dehnert Midwifery’s cost formula for its wages and salaries is $2,030 per month plus $409

per birth. For the month of May, the company planned for activity of 112 births, but the

actual level of activity was 114 births. The actual wages and salaries for the month was

$50,800. The wages and salaries in the planning budget for May would be closest to:

8-463

45.

Towne Snow Removal’s cost formula for its vehicle operating cost is $1,470 per month

plus $399 per snow-day. For the month of November, the company planned for activity of

13 snow-days, but the actual level of activity was 9 snow-days. The actual vehicle

operating cost for the month was $5,230. The vehicle operating cost in the flexible budget

for November would be closest to:

8-464

46.

Pettry Snow Removal’s cost formula for its vehicle operating cost is $2,170 per month plus

$408 per snow-day. For the month of December, the company planned for activity of 16

snow-days, but the actual level of activity was 13 snow-days. The actual vehicle operating

cost for the month was $7,600. The vehicle operating cost in the planning budget for

December would be closest to:

47.

Tulip Midwifery’s cost formula for its wages and salaries is $2,420 per month plus $388

per birth. For the month of January, the company planned for activity of 119 births, but the

actual level of activity was 123 births. The actual wages and salaries for the month was

$50,540. The wages and salaries in the flexible budget for January would be closest to:

8-465

8-466

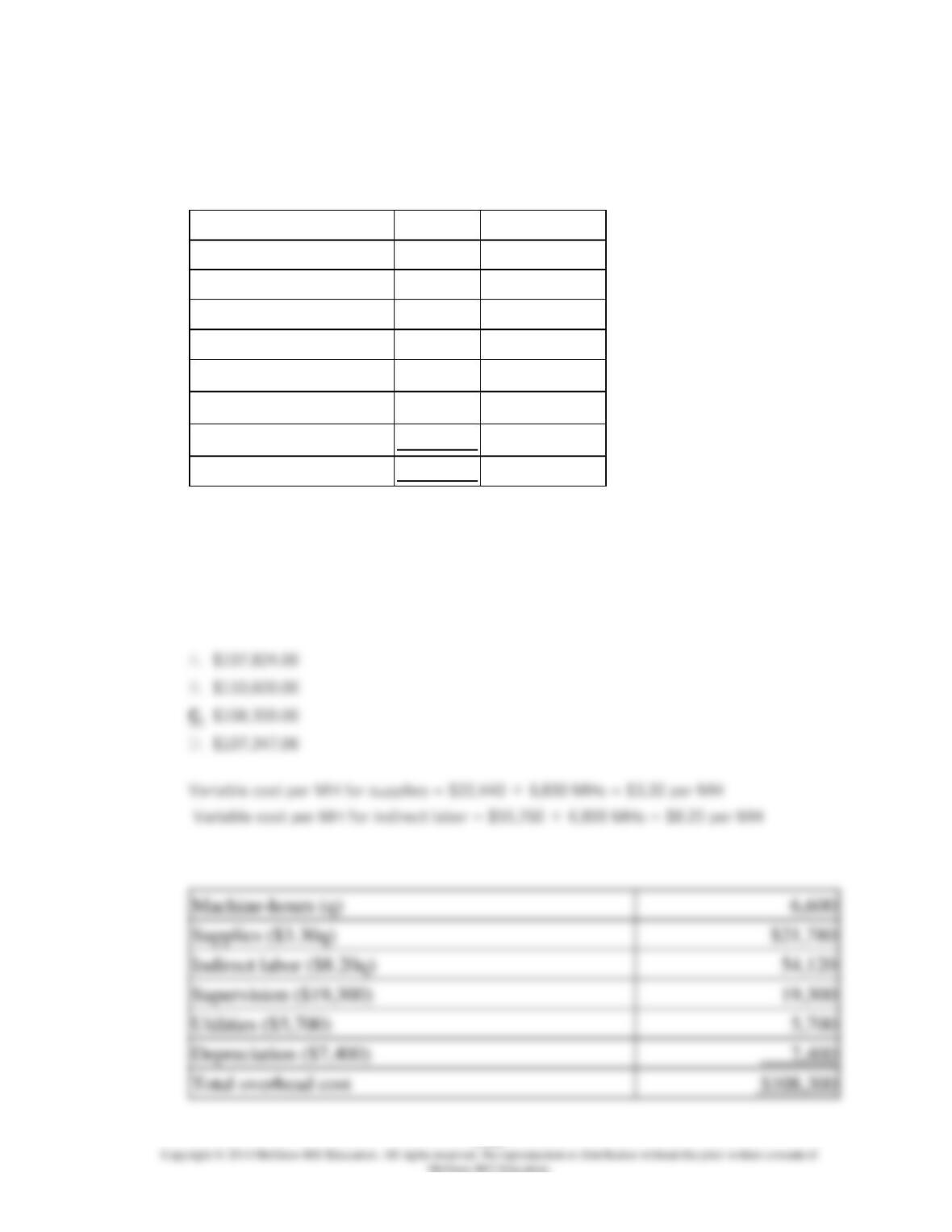

48.

Hatzenbuhler Manufacturing Corporation has prepared the following overhead budget for

next month.

Activity level

6,800

machine-hours

Variable overhead costs:

Supplies

$22,440

Indirect labor

55,760

Fixed overhead costs:

Supervision

19,300

Utilities

5,700

Depreciation

7,400

Total overhead cost

$110,600

Machine-hours (q)

Supplies ($3.30q)

Indirect labor ($8.20q)

Supervision ($19,300)

Utilities ($5,700)

Depreciation ($7,400)

The company’s variable overhead costs are driven by machine-hours.

What would be the total budgeted overhead cost for next month if the activity level is

6,600 machine-hours rather than 6,800 machine-hours?

8-467

49.

Peixoto Framing’s cost formula for its supplies cost is $1,150 per month plus $14 per

frame. For the month of July, the company planned for activity of 556 frames, but the

actual level of activity was 555 frames. The actual supplies cost for the month was $9,190.

The supplies cost in the planning budget for July would be closest to:

8-468

50.

Loomer Catering uses two measures of activity, jobs and meals, in the cost formulas in its

budgets and performance reports. The cost formula for catering supplies is $550 per

month plus $95 per job plus $21 per meal. A typical job involves serving a number of meals

to guests at a corporate function or at a host’s home. The company expected its activity in

July to be 12 jobs and 136 meals, but the actual activity was 13 jobs and 137 meals. The

actual cost for catering supplies in July was $4,770. The catering supplies in the planning

budget for July would be closest to:

8-469

51.

Lynne Catering uses two measures of activity, jobs and meals, in the cost formulas in its

budgets and performance reports. The cost formula for catering supplies is $480 per

month plus $91 per job plus $14 per meal. A typical job involves serving a number of meals

to guests at a corporate function or at a host’s home. The company expected its activity in

June to be 10 jobs and 79 meals, but the actual activity was 14 jobs and 77 meals. The

actual cost for catering supplies in June was $2,970. The catering supplies in the flexible

budget for June would be closest to:

52.

Paradiso Medical Clinic measures its activity in terms of patient-visits. Last month, the

budgeted level of activity was 1,060 patient-visits and the actual level of activity was 1,050

patient-visits. The cost formula for administrative expenses is $3.00 per patient-visit plus

$17,000 per month. The actual administrative expense was $19,300. In the clinic’s

performance report for last month, the spending variance for administrative expenses was:

53.

Ros Corporation’s flexible budget cost formula for indirect materials, a variable cost, is

$0.90 per unit of output. If the company’s performance report for last month shows a $500

unfavorable spending variance for indirect materials and if 8,000 units of output were

produced last month, then the actual costs incurred for indirect materials for the month

must have been:

54.

Loggin Midwifery’s cost formula for its wages and salaries is $2,380 per month plus $231

per birth. For the month of April, the company planned for activity of 100 births, but the

actual level of activity was 102 births. The actual wages and salaries for the month was

$25,510. The spending variance for wages and salaries in April would be closest to:

55.

Olivera Corporation’s performance report for last month shows that actual indirect

materials cost, a variable cost, was $31,178 and that the spending variance for indirect

materials cost was $2,261 unfavorable. During that month, the company worked 11,900

machine-hours. Budgeted activity for the month had been 12,200 machine-hours. The cost

formula per machine-hour for indirect materials cost must have been closest to:

56.

Biggs Enterprise’s flexible budget cost formula for indirect materials, a variable cost, is

$0.60 per unit of output. If the company’s performance report for last month shows a $200

favorable spending variance for indirect materials and if 9,000 units of output were

produced last month, then the actual costs incurred for indirect materials for the month

must have been:

57.

At Worthe Corporation, indirect labor is a variable cost that varies with direct labor-hours.

Last month’s performance report showed that actual indirect labor cost totaled $7,920 for

the month and that the associated spending variance was $240 F. If 10,200 direct labor-

hours were actually worked last month, then the flexible budget cost formula for indirect

labor must be (per direct labor-hour) closest to:

58.

Gastineau Tile Installation Corporation measures its activity in terms of square feet of tile

installed. Last month, the budgeted level of activity was 1,230 square feet and the actual

level of activity was 1,200 square feet. The company’s owner budgets for supply costs, a

variable cost, at $2.70 per square foot. The actual supply cost last month was $2,690. In

the company’s performance report for last month, what would have been the spending

variance for supply costs?

59.

Tysor Framing’s cost formula for its supplies cost is $2,610 per month plus $17 per frame.

For the month of July, the company planned for activity of 710 frames, but the actual level

of activity was 712 frames. The actual supplies cost for the month was $14,540. The

spending variance for supplies cost in July would be closest to:

60.

Randt Footwear Corporation’s flexible budget cost formula for supplies, a variable cost, is

$2.79 per unit of output. The company’s performance report for last month showed a

$5,363 favorable spending variance for supplies. During that month, 17,300 units were

produced. Budgeted activity for the month had been 17,200 units. The actual cost per unit

for indirect materials must have been closest to:

61.

Petroski Natural Dying Corporation measures its activity in terms of skeins of yarn dyed.

Last month, the budgeted level of activity was 19,700 skeins and the actual level of activity

was 19,900 skeins. The company’s owner budgets for dye costs, a variable cost, at $0.67

per skein. The actual dye cost last month was $13,910. In the company’s performance

report for last month, what would have been the spending variance for dye costs?

62.

Ishibashi Snow Removal’s cost formula for its vehicle operating cost is $1,240 per month

plus $337 per snow-day. For the month of February, the company planned for activity of 17

snow-days, but the actual level of activity was 12 snow-days. The actual vehicle operating

cost for the month was $5,140. The spending variance for vehicle operating cost in

February would be closest to: