Problem 7-24A (45 minutes)

1. a. The reasons that Marge Atkins and Pete Granger use budgetary slack

include the following:

• These employees are hedging against the unexpected (reducing

b. The use of budgetary slack can adversely affect Atkins and Granger

by:

• limiting the usefulness of the budget to motivate their employees to

top performance.

Problem 7-24A (continued)

2. The use of budgetary slack, particularly if it has a detrimental effect on

the company, may be unethical. In assessing the situation, the specific

standards contained in “Standards of Ethical Conduct for Management

Accountants” that should be considered are listed below.

Competence

Clear reports using relevant and reliable information should be

prepared.

Problem 7-25A (45 minutes)

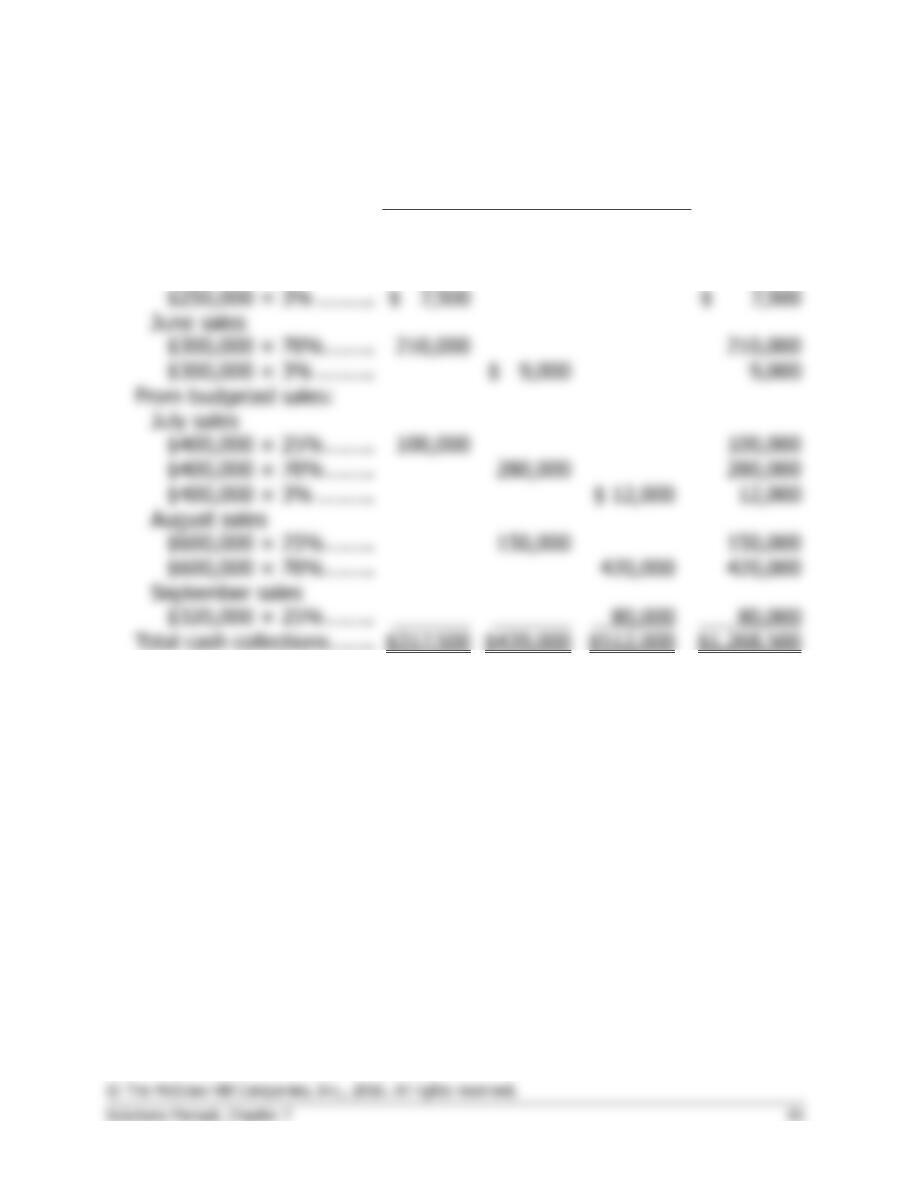

1. Schedule of expected cash collections:

Month

July

August

September

Quarter

From accounts receivable:

August sales

May sales

Problem 7-25A (continued)

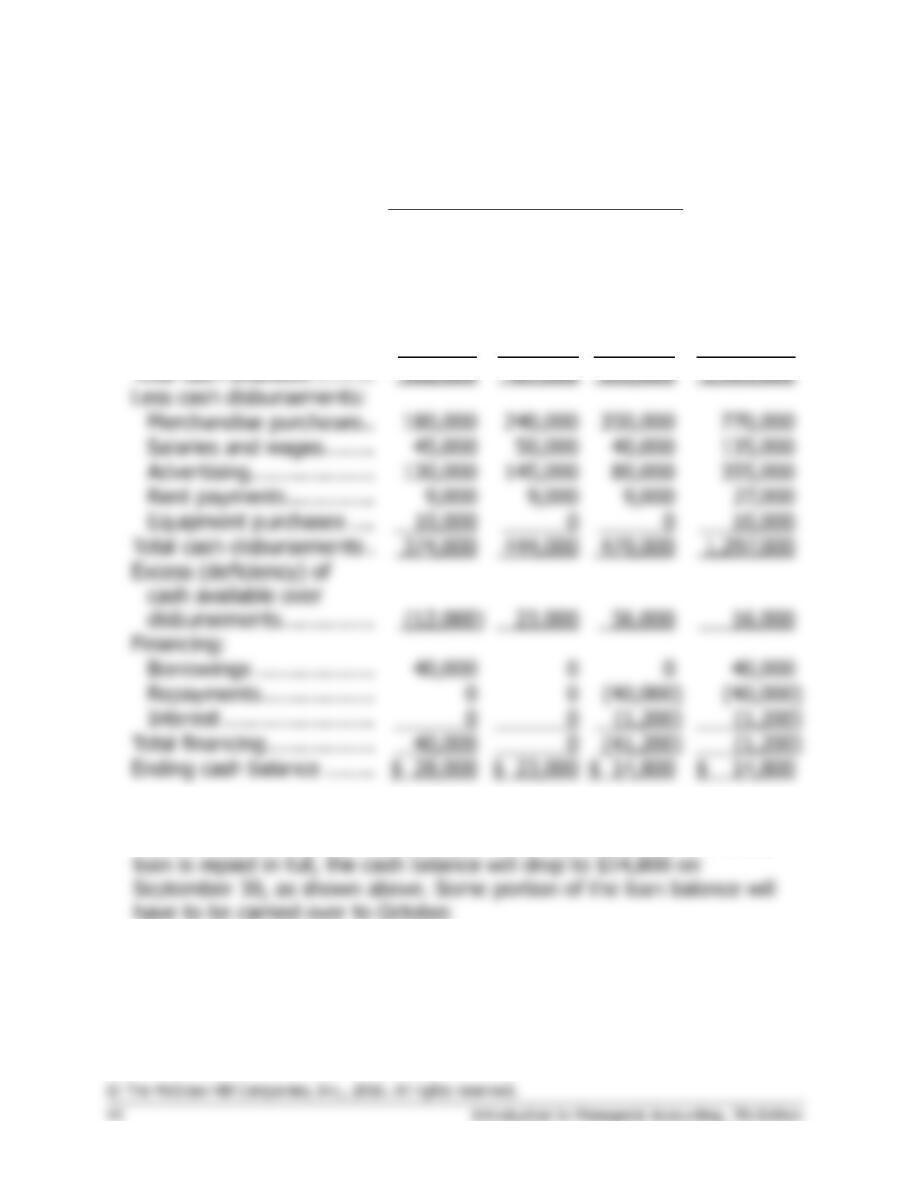

2. Cash budget:

Month

July

August

Septem-

ber

Quarter

Beginning cash balance ….

$ 44,500

$ 28,000

$ 23,000

$ 44,500

Add receipts:

Collections from

customers ………………

317,500

439,000

512,000

1,268,500

Total cash available ……….

362,000

467,000

535,000

1,313,000

Less cash disbursements:

130,000

0

Total cash disbursements .

374,000

479,000

Financing:

(1,200)

(1,200)

Total financing ……………..

(1,200)

Ending cash balance ……..

$ 23,000

3. If the company needs a $20,000 minimum cash balance to start each

month, then the loan cannot be repaid in full by September 30. If the

Problem 7-26A (60 minutes)

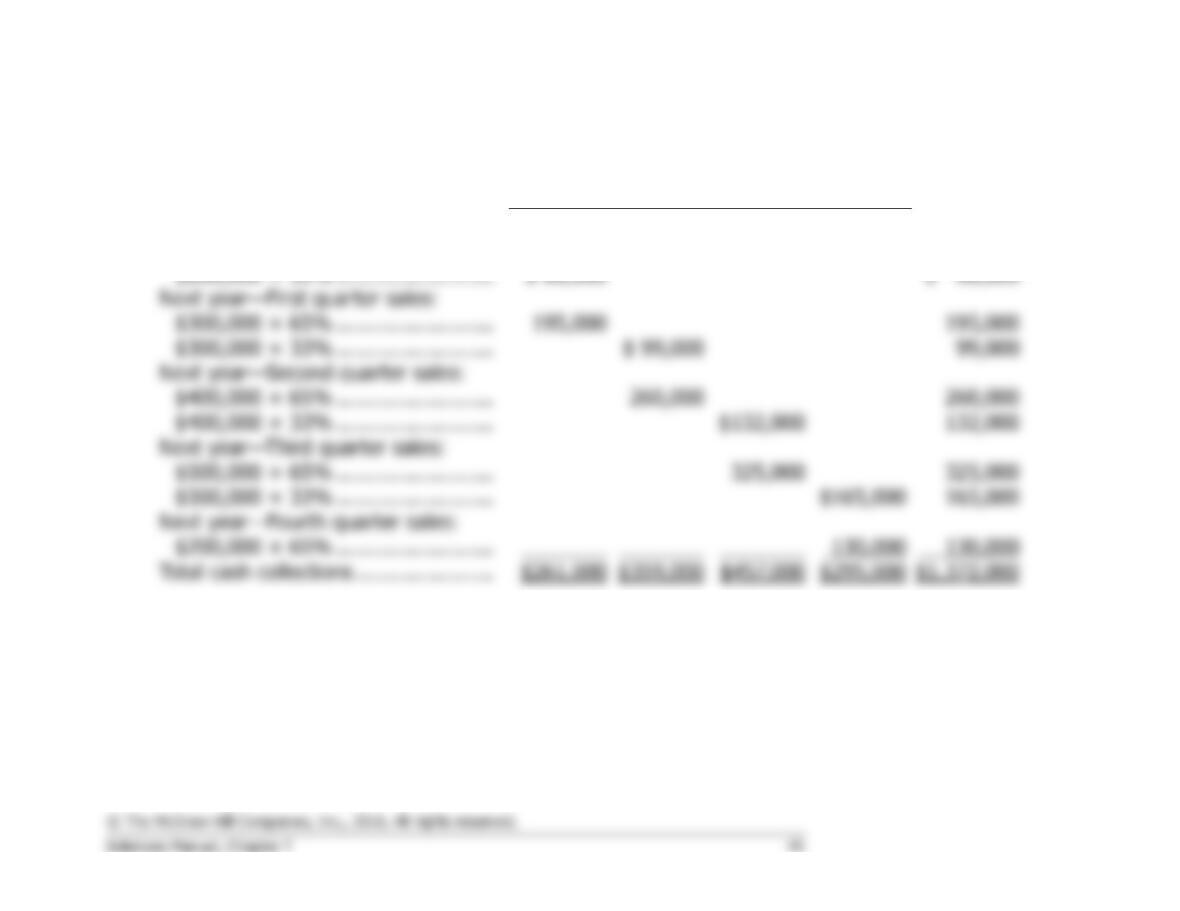

1. a. Schedule of expected cash collections:

Next Year’s Quarter

First

Second

Third

Fourth

Total

Current year—Fourth quarter sales:

Next year—Second quarter sales:

Next year—Fourth quarter sales:

Problem 7-26A (continued)

b. Schedule of expected cash disbursements for merchandise purchases for next year:

Quarter

First

Second

Third

Fourth

Total

Current year—Fourth quarter purchases:

$126,000 × 20% ………………………….

$ 25,200

$ 25,200

Next year—Second quarter purchases:

Next year—Fourth quarter purchases:

Problem 7-26A (continued)

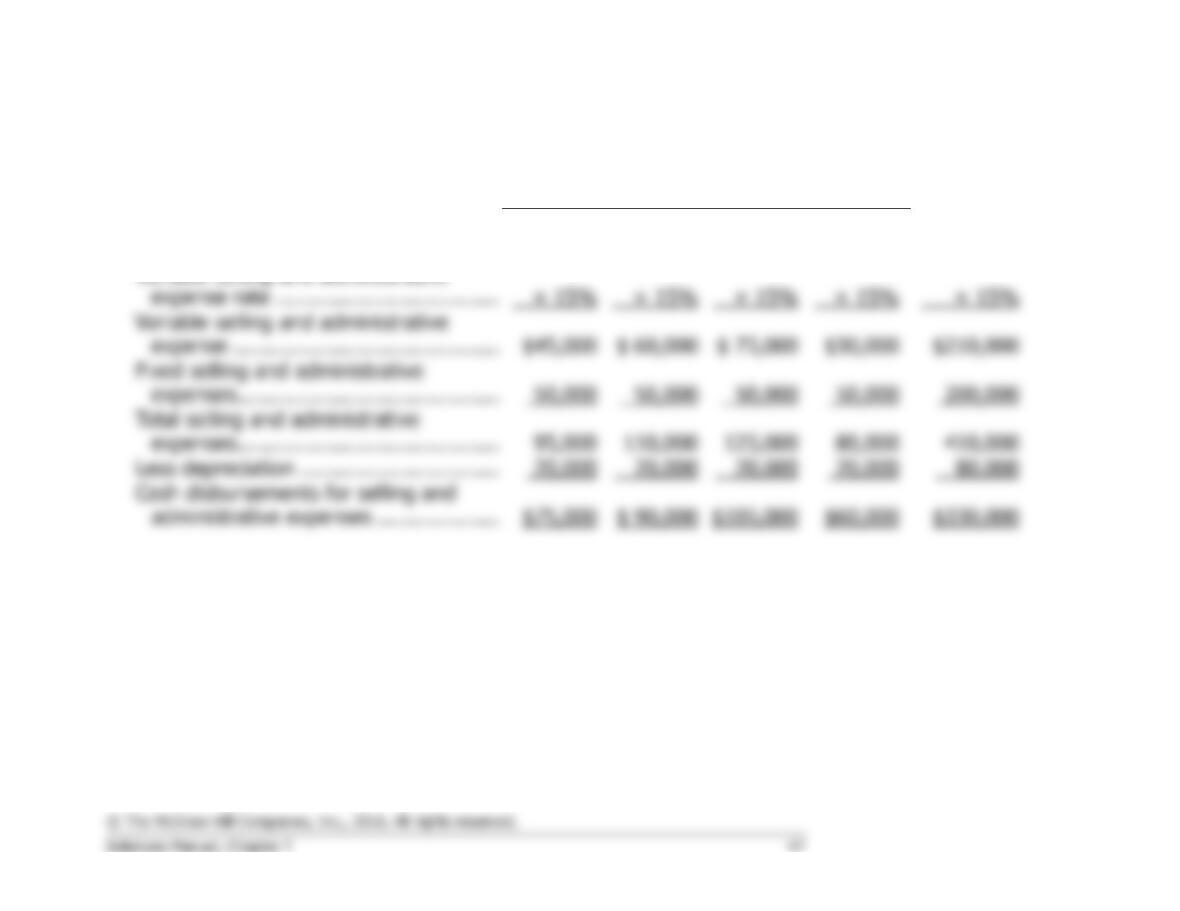

2. Budgeted selling and administrative expenses for next year:

Quarter

First

Second

Third

Fourth

Year

Budgeted sales in dollars …………………

$300,000

$400,000

$500,000

$200,000

$1,400,000

Variable selling and administrative

Problem 7-26A (continued)

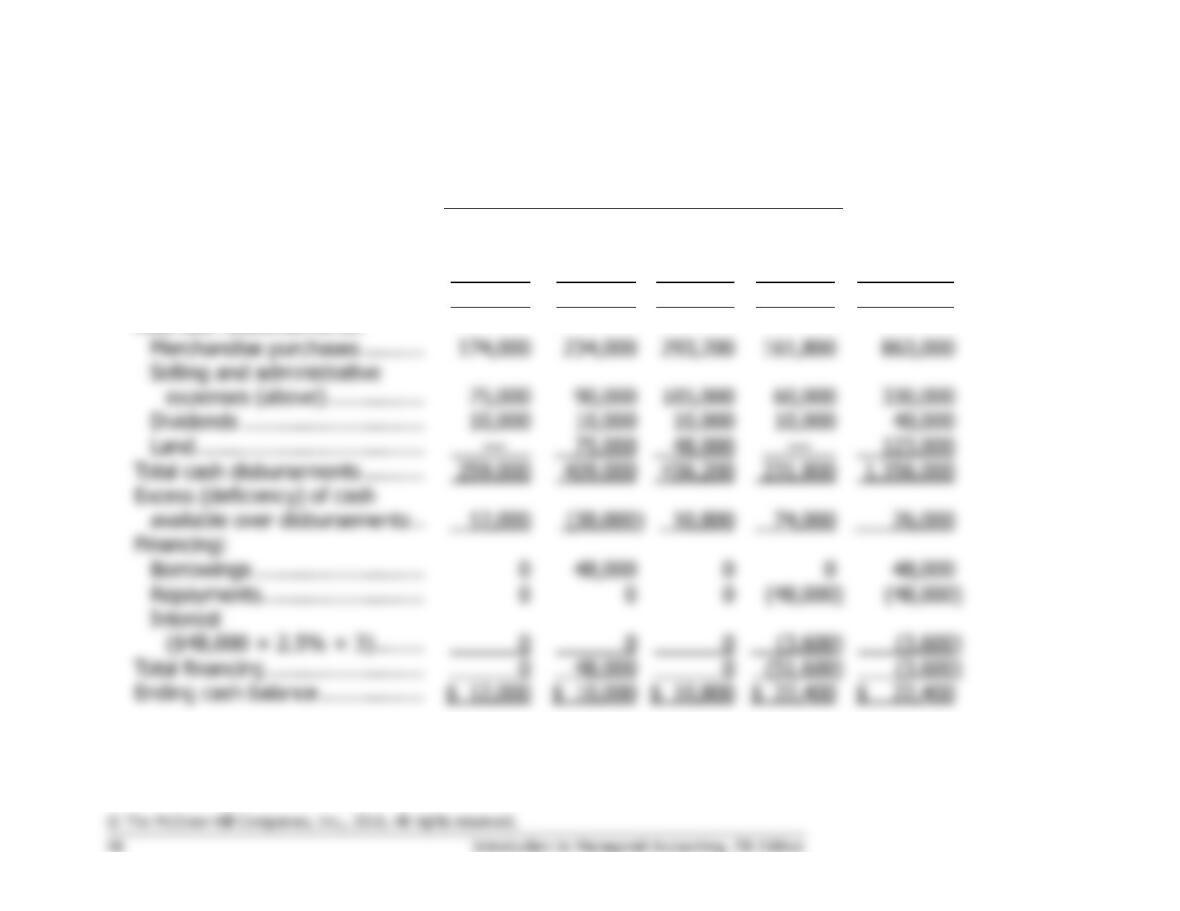

3. Cash budget for next year:

Quarter

First

Second

Third

Fourth

Year

Beginning cash balance ………….

$ 10,000

$ 12,000

$ 10,000

$ 10,800

$ 10,000

Add collections from customers .

261,000

359,000

457,000

295,000

1,372,000

Total cash available ……………….

271,000

371,000

467,000

305,800

1,382,000

Less cash disbursements:

174,000

––

123,000

Total cash disbursements ……….

259,000

409,000

231,800

1,356,000

74,000

26,000

Financing:

0

0

(3,600)

Total financing ……………………..

0

(3,600)

Ending cash balance ……………..

$ 10,000

$ 10,800

Problem 7-27A (120 minutes)

1. Schedule of expected cash collections:

April

May

June

Quarter

Cash sales ………………..

$36,000

*

$43,200

$54,000

$133,200

*

24,000

Total collections …………

$56,000

*

$67,200

$82,800

$206,000

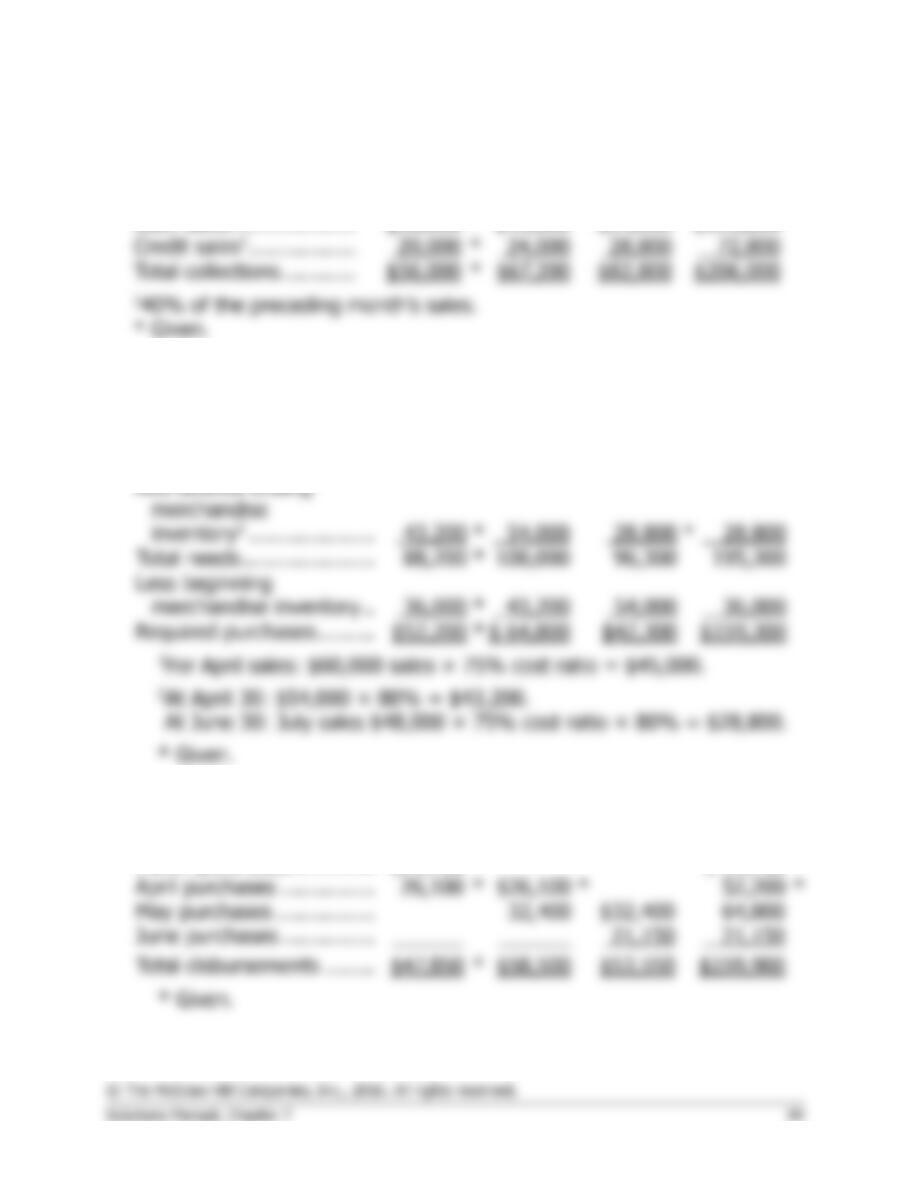

2. Merchandise purchases budget:

April

May

June

Quarter

Budgeted cost of goods

sold1 ……………………….

$45,000

*

$ 54,000

*

$67,500

$166,500

*

*

28,800

Total needs …………………

*

Required purchases ………

$52,200

*

$ 64,800

$42,300

$159,300

Schedule of expected cash disbursements—merchandise purchases

April

May

June

Quarter

March purchases ………….

$21,750

*

$ 21,750

*

April purchases ……………

*

*

*

Total disbursements ……..

$47,850

*

Problem 7-27A (continued)

3. Cash budget:

April

May

June

Quarter

Beginning cash balance .

$ 8,000

*

$ 4,350

$ 4,590

$ 8,000

Add collections from

customers ………………

56,000

*

67,200

82,800

206,000

Total cash available …….

*

Less cash

disbursements:

For inventory …………..

47,850

*

159,900

For expenses …………..

13,300

*

*

Total cash

disbursements …………

62,650

*

73,960

72,250

208,860

Excess (deficiency) of

cash available over

disbursements …………

1,350

*

(2,410)

15,140

5,140

Financing:

Borrowings ……………..

0

0

(230)

(230)

Total financing …………..

3,000

7,000

(10,230)

(230)

Ending cash balance ……

Problem 7-27A (continued)

4.

Shilow Company

Income Statement

For the Quarter Ended June 30

Sales ($60,000 + $72,000 + $90,000) …….

$222,000

Cost of goods sold:

Beginning inventory (Given) ……………….

Add purchases (Part 2) ………………………

Goods available for sale ……………………..

28,800

166,500

*

Gross margin ……………………………………..

55,500

Selling and administrative expenses:

Commissions (12% of sales) ……………….

26,640

Rent ($2,500 × 3) …………………………….

7,500

13,320

Net operating income ………………………….

Interest expense (Part 3) ……………………..

Net income ……………………………………….

Problem 7-27A (continued)

5.

Shilow Company

Balance Sheet

June 30

Assets

Current assets:

Cash (Part 4) …………………………..………………………….

$ 4,910

Accounts receivable ($90,000 × 40%) ………………………

Total current assets ………………………………………………..

Total assets …………………………………………………………..

Liabilities and Stockholders’ Equity

Accounts payable (Part 2: $42,300 × 50%) ..

$ 21,150

Stockholders’ equity:

Common stock (Given) ………………………..

Retained earnings* …………………………….

17,360

Total liabilities and stockholders’ equity ……..

Beginning retained earnings ………………..

Add net income …………………………..…….

Ending retained earnings …………………….

Problem 7-28A (60 minutes)

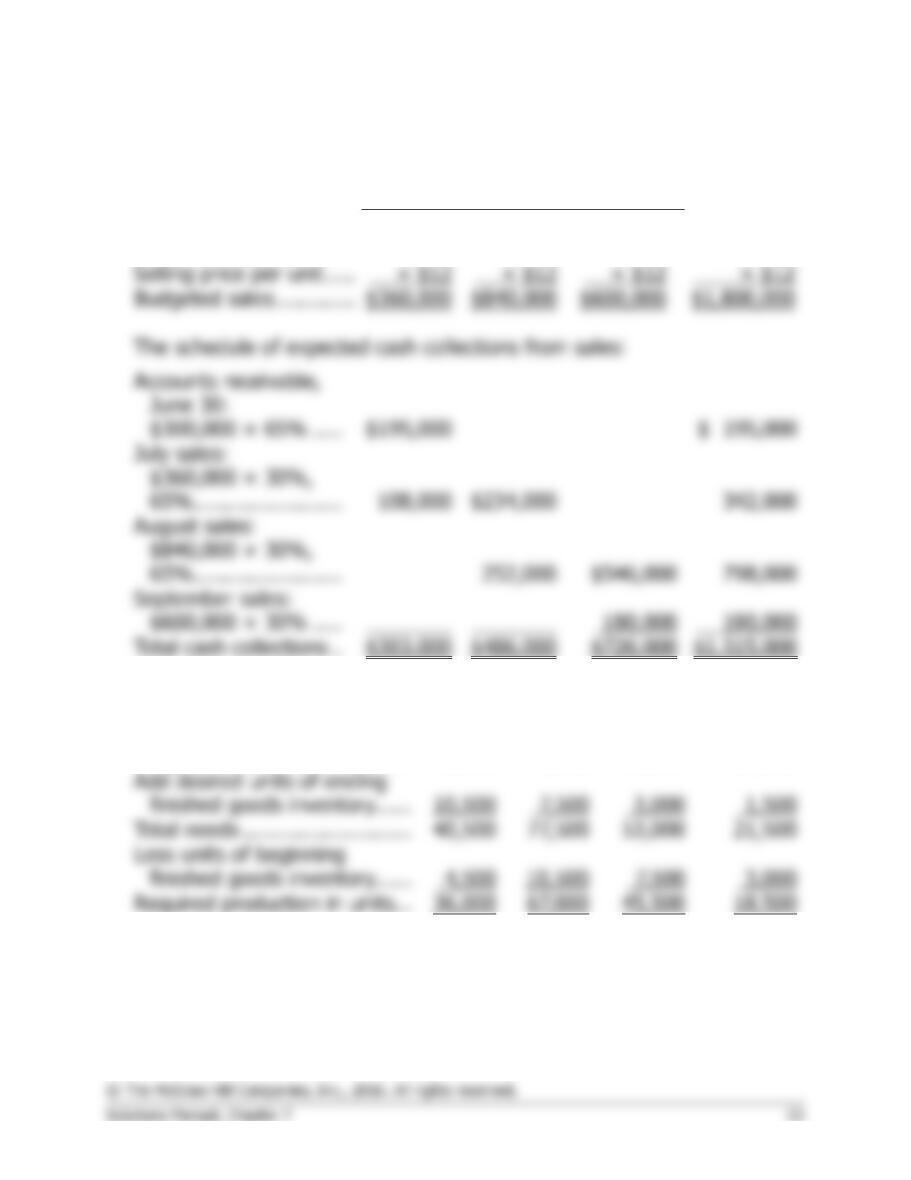

1. The sales budget for the third quarter:

Month

July

August

September

Quarter

Budgeted units sales …..

30,000

70,000

50,000

150,000

Selling price per unit …..

× $12

Budgeted sales ………….

Total cash collections ..

2. The production budget for July-October:

July

August

September

October

Budgeted unit sales ……………

30,000

70,000

50,000

20,000

1,500

Total needs ………………………

53,000

4,500

10,500

3,000

Required production in units…

36,000

45,500

18,500

Problem 7-28A (continued)

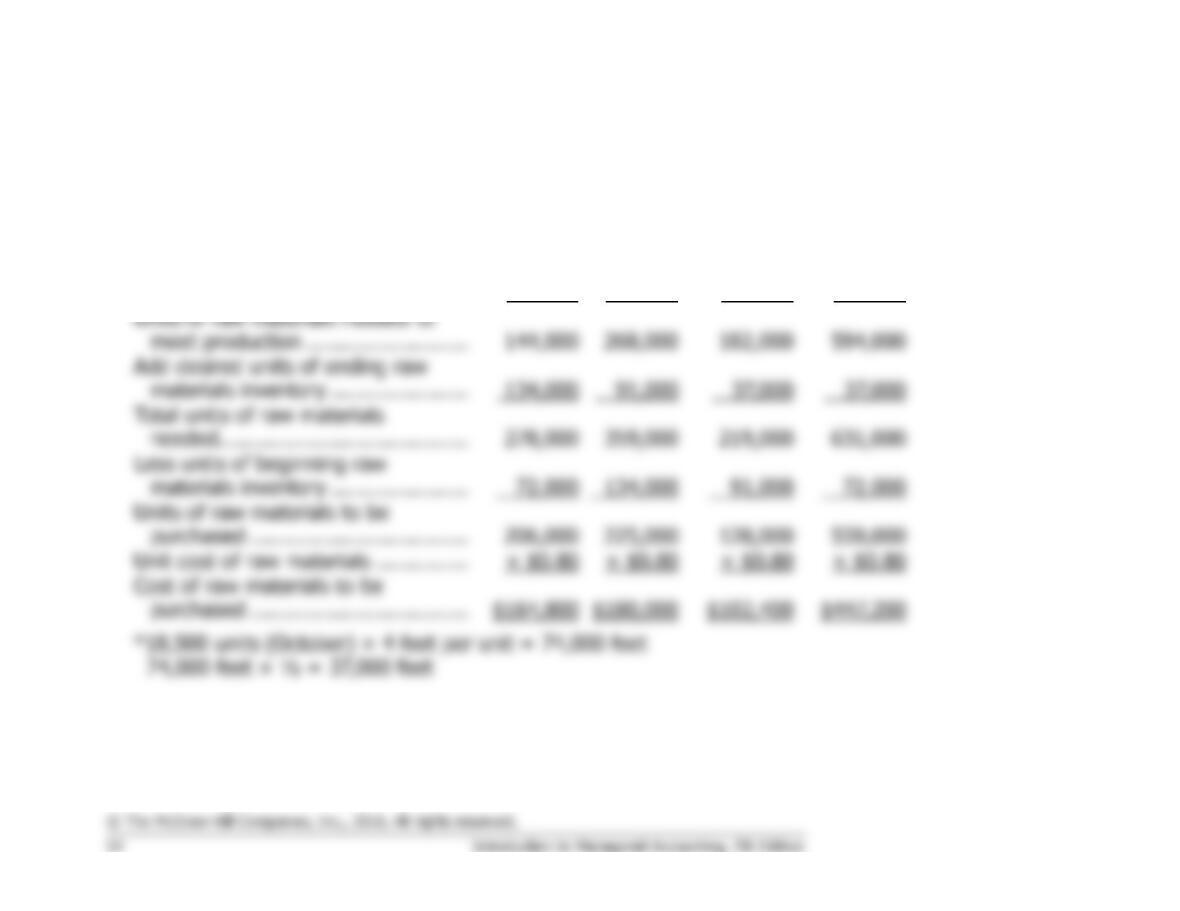

3. The direct materials budget for the third quarter:

July

August

September

Quarter

Required production in units of

finished goods ………………………..

36,000

67,000

45,500

148,500

Units of raw materials needed per

unit of finished goods ……………….

× 4

× 4

× 4

× 4

Units of raw materials needed to

meet production ……………………..

594,000

materials inventory ………………….

37,000

Total units of raw materials

needed ………………………………….

631,000

91,000

Units of raw materials to be

purchased ……………………………..

Unit cost of raw materials ……………

× $0.80

× $0.80

× $0.80

Cost of raw materials to be

Problem 7-28A (continued)

3. The schedule of expected cash disbursements for materials purchases:

July

August

September

Quarter

Accounts payable,

June 30 ……………………

$ 76,000

$ 76,000

August purchases:

Problem 7-29A (120 minutes)

1. Schedule of expected cash collections:

January

February

March

Quarter

Cash sales ………………..

$ 80,000

*

$120,000

$ 60,000

$ 260,000

Credit sales ………………

224,000

*

320,000

480,000

1,024,000

Total cash collections ….

*

$440,000

$540,000

$1,284,000

2. a. Merchandise purchases budget:

January

February

March

Quarter

Budgeted cost of goods

sold1 ……………………..

$240,000

*

$360,000

*

$180,000

$780,000

90,000

*

45,000

30,000

30,000

*

Required purchases …….

$270,000

*

$315,000

$165,000

$750,000

* Given.

Add desired ending

b. Schedule of expected cash disbursements for merchandise purchases:

January

February

March

Quarter

December

purchases …………

$ 93,000

*

$ 93,000

*

January purchases ..

*

$135,000

*

*

February purchases .

March purchases …..

82,500

purchases …………

$228,000

*

$292,500

$240,000

$760,500

Problem 7-29A (continued)

3. Cash budget:

January

February

March

Quarter

Beginning cash balance …..

$ 48,000

*

$ 30,000

$ 30,800

$ 48,000

Add collections from

customers ………………….

304,000

*

440,000

540,000

1,284,000

Total cash available ………..

352,000

*

470,000

570,800

1,332,000

Less cash disbursements:

Inventory purchases …….

*

292,500

*

145,000

45,000

*

0

0

45,000

Total cash disbursements ..

402,000

*

439,200

445,500

1,286,700

*

30,800

125,300

45,300

Financing:

Borrowings ………………..

80,000

0

0

80,000

Repayments ……………….

0

0

(80,000)

(80,000)

0

(2,400)

Total financing ………………

80,000

0

(2,400)

Ending cash balance ………

$ 30,000

$ 30,800

$ 42,900

$ 42,900

Problem 7-29A (continued)

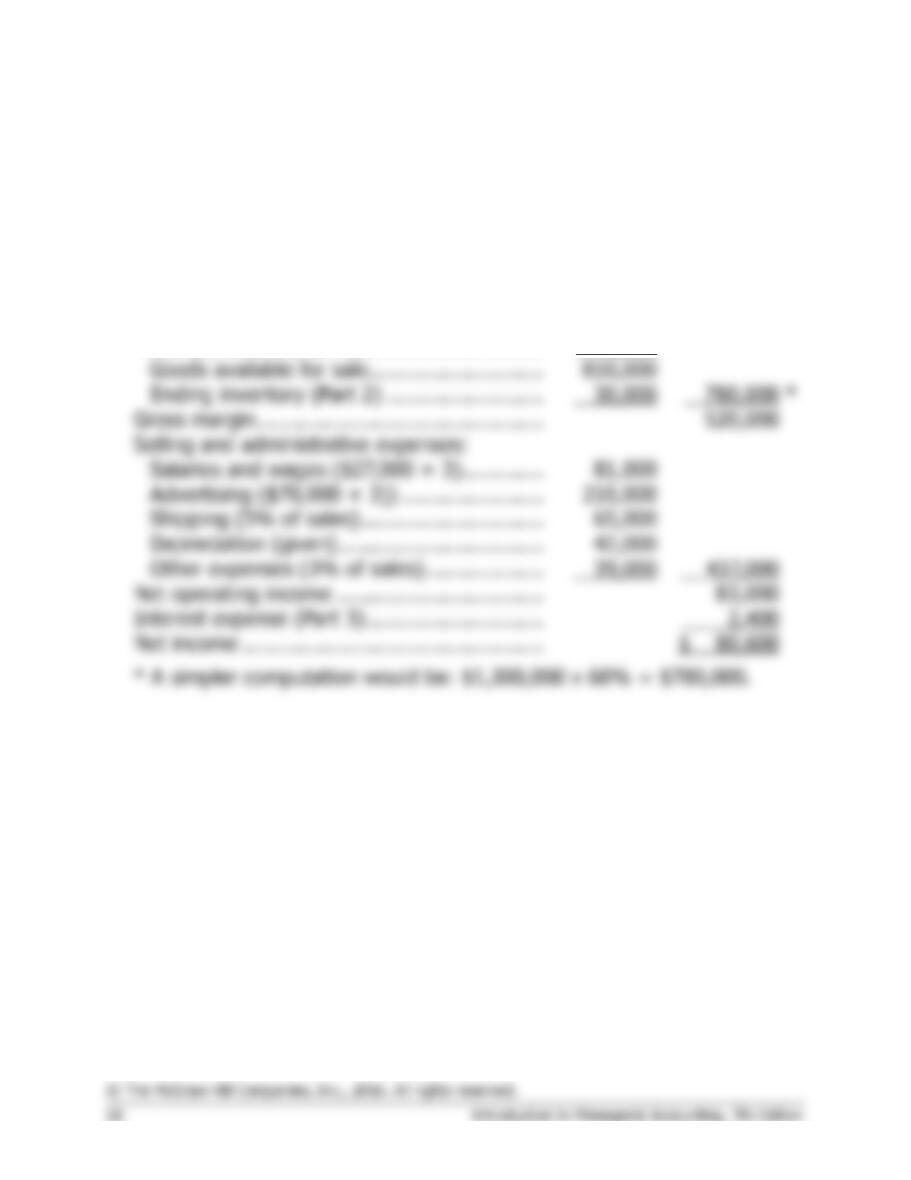

4. Income statement:

Hillyard Company

Income Statement

For the Quarter Ended March 31

Sales …………………………………………………

$1,300,000

Cost of goods sold:

Beginning inventory (Given) …………………

$ 60,000

Add purchases (Part 2) ………………………..

750,000

Goods available for sale ……………………….

*

Gross margin ……………………………………….

Selling and administrative expenses:

Salaries and wages ($27,000 × 3) ………….

Advertising ($70,000 × 3)) …………………..

Other expenses (3% of sales) ……………….

437,000

Net operating income …………………………...

Interest expense (Part 3) ……………………….

2,400

Net income …………………………………………

5. Balance sheet:

Hillyard Company

Balance Sheet

March 31

Assets

Current assets:

Cash (Part 4) …………………………..………………………….

$ 42,900

Accounts receivable (80% × $300,000) …………………….

Total current assets ………………………………………………..

Liabilities and Stockholders’ Equity

Current liabilities:

Accounts payable (Part 2: 50% × $165,000) ..

$ 82,500

Total liabilities and stockholders’ equity ………….

*

Beginning retained earnings ……………..

Add net income ………………………………

Ending retained earnings ………………….

Ethics Challenge (75 minutes)

1. Stokes is using the budget as a club to pressure employees and as a

way to find someone to blame rather than as a legitimate planning and

2. The way in which the budget is being used is likely to breed hostility,

tension, mistrust, lack of respect, and actions designed to meet targets

3. As the old saying goes, Keri Kalani is “between a rock and a hard place.”

The Statement of Ethical Professional Practice established by the

Institute of Management Accountants states that management

accountants have a responsibility to “disclose all relevant information

that could reasonably be expected to influence an intended user’s