Chapter 11 Capital Budgeting Decisions

Chapter 11

Lecture Notes

Chapter theme: The term capital budgeting is used to

describe how managers plan significant cash outlays on

I. Capital budgeting – an overview

A. Typical capital budgeting decisions

i. Capital budgeting analysis can be used for

any decision that involves an outlay now in

order to obtain some future return. Typical

capital budgeting decisions include:

1. Cost reduction decisions. Should new

equipment be purchased to reduce costs?

Chapter 11 Capital Budgeting Decisions

B. Types of capital budgeting decisions

i. There are two main types of capital

budgeting decisions:

1. Screening decisions relate to whether a

proposed project passes a preset hurdle.

2. Preference decisions relate to selecting

among several competing courses of action.

a. For example, a company may be

C. Cash flows versus net operating income

i. The payback method, the net present value

method and the internal rate of return method

ii. Examples of cash outflows and cash inflows

that accompany capital investment projects

are as follows:

1. Cash outflows include those shown on this

slide. Notice the term working capital,

5

Chapter 11 Capital Budgeting Decisions

3

Helpful Hint: The role of working capital in capital

budgeting often confuses students. Emphasize that the

initial investment in working capital at the beginning of

D. The time value of money

i. The time value of money concept recognizes

that a dollar today is worth more than a

dollar a year from now. Therefore, projects

that promise earlier returns are preferable to

7

5

Chapter 11 Capital Budgeting Decisions

4

11

II. The payback method

Learning Objective 11-1: Determine the payback

A. The payback method focuses on the payback period,

which is the length of time that it takes for a project to

recoup its initial cost out of the cash receipts that it

generates.

i. Key concepts

1. The payback method analyzes cash flows;

ii. The Daily Grind – an example

1. Assume the management of the Daily Grind

wants to install an espresso bar in its

restaurant.

a. The cost of the espresso bar is

$140,000 and it has a 10-year life.

2. The payback period is 4.0 years. Therefore,

management would choose to invest in the

bar.

10

13

12

Chapter 11 Capital Budgeting Decisions

5

Quick Check – the payback method

iii. Evaluation of the payback method

1. Criticisms

a. A shorter payback period does not

always mean that one investment is

more desirable than another.

Helpful Hint: Ask students to choose between two

options that each require an initial investment of

$4,000. Option A returns $1,000 at the end of each four

years; option B returns $4,000 at the end of the fourth

year. Under the payback method, options A and B are

14–15

Chapter 11 Capital Budgeting Decisions

2. Strengths

a. It can serve as a screening tool to help

identify which investment proposals

are in the “ballpark.”

iv. Payback and uneven cash flows

1. When the cash flows associated with an

investment project change from year to year,

the payback formula introduced earlier

III. The net present value method

Learning Objective 11-2: Evaluate the acceptability of

18

Chapter 11 Capital Budgeting Decisions

7

A. Key concepts/assumptions

i. The net present value method compares the

ii. Two simplifying assumptions are usually

made in net present value analysis:

1. The first assumption is that all cash flows

B. The net present value method: an example using

discount factors from Exhibits 11B-1 and 11B-2

i. Assume the information as shown with

respect to Lester Company.

1. Also assume that at the end of five years the

23

Chapter 11 Capital Budgeting Decisions

27

29

30

35

iii. Since the investments in equipment

($160,000) and working capital ($100,000)

occur immediately, the discounting factor

used is 1.000.

v. The present value factor of $1 for three years

at 11% is 0.731. Therefore, the present value

of the cost of relining the equipment in three

years is $21,930.

Quick Check – net present value calculations

C. The net present value method: an example using

discount factors from Exhibits 11B-1

i. For this next example, we’ll use the same

information from Lester Company.

28

31–33

26

34

Chapter 11 Capital Budgeting Decisions

9

38

39

ii. Since the investments in equipment

iii. The total cash flows for years 1-5 are

discounted to their present values using the

discount factors from Exhibit 11B-1.

iv. For example, the total cash flows in year 1 of

vi. The net present value of the investment

opportunity is $76,015. Notice this amount

equals the net present value from the earlier

approach.

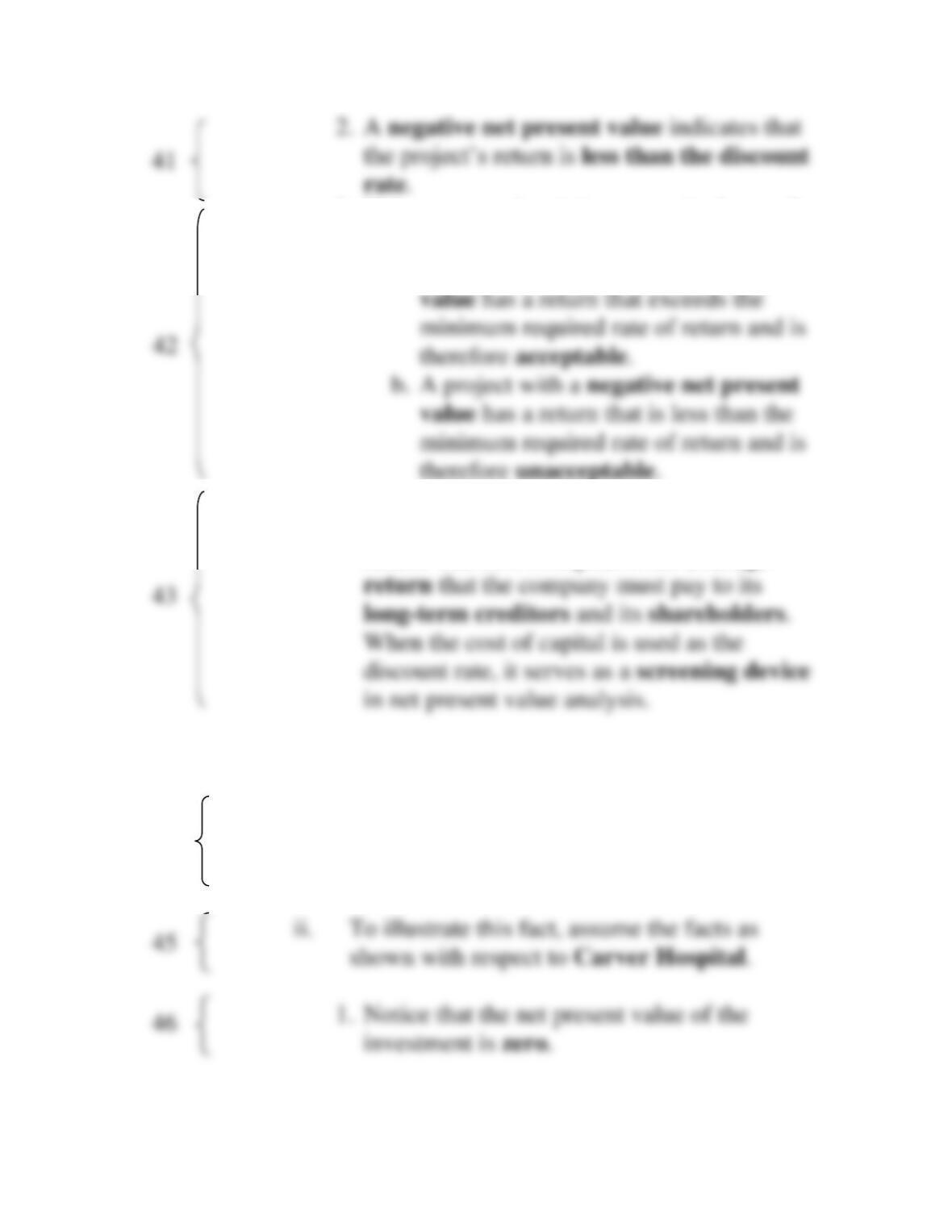

D. The net present value method: interpreting the

results

i. Once you have computed a net present value,

you should interpret the results as follows:

40

37

36

Chapter 11 Capital Budgeting Decisions

10

3. If the company’s minimum required rate of

return is used as the discount rate:

a. A project with a positive net present

4. A company’s cost of capital is usually

regarded as its minimum required rate of

return. The cost of capital is the average

E. Recovery of the original investment

i. The net present value method automatically

provides for return of the original

investment.

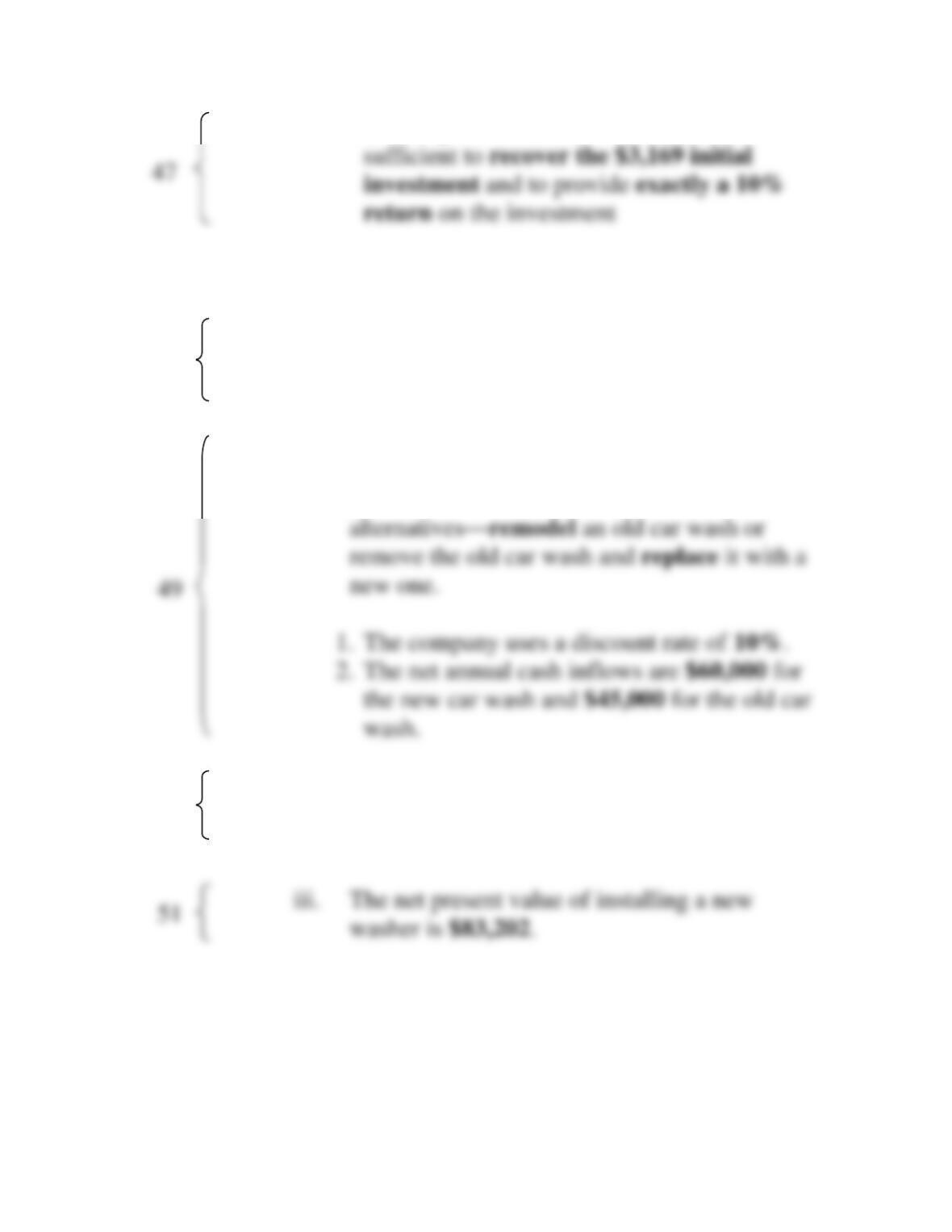

ii. To illustrate this fact, assume the facts as

44

Chapter 11 Capital Budgeting Decisions

11

51

2. This implies that the cash inflows are

IV. Expanding the net present value method

A. We will now expand the net present value method to

include two alternatives. We will analyze the

alternatives using the total cost approach.

B. Net present value analysis: an expanded example

i. Assume that White Co. has two

ii. In addition, assume that the information as

shown relates to the installation of a new

washer.

48

50

Chapter 11 Capital Budgeting Decisions

12

55

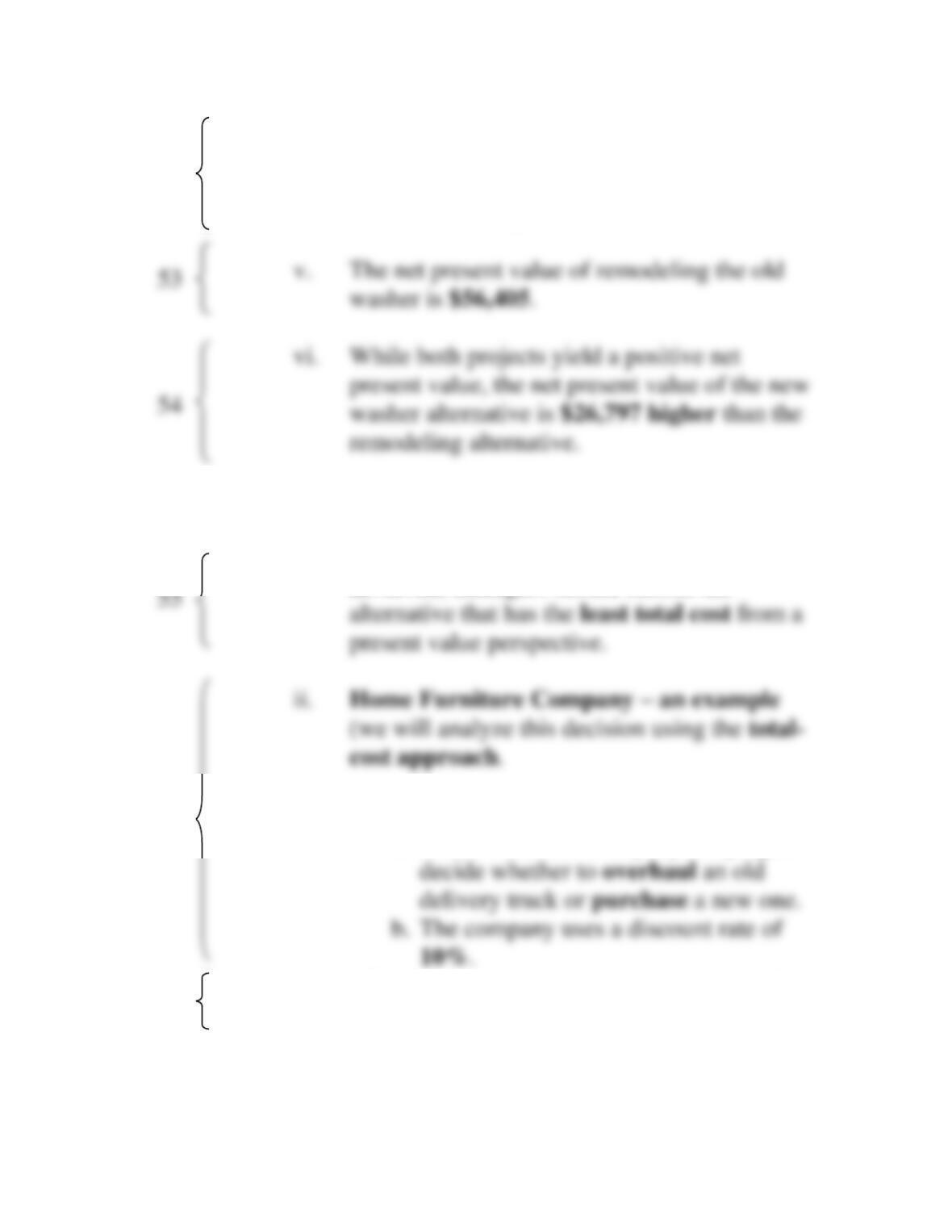

iv. If White chooses to remodel the existing

washer, the remodeling costs would be

$175,000 and the cost to replace the brushes

at the end of six years would be $80,000.

C. Least cost decisions

i. In decisions where revenues are not directly

involved, managers should choose the

1. Assume the following:

a. Home Furniture Company is trying to

2. The information pertaining to the old and

new trucks is as shown.

52

56

57

53

54

Chapter 11 Capital Budgeting Decisions

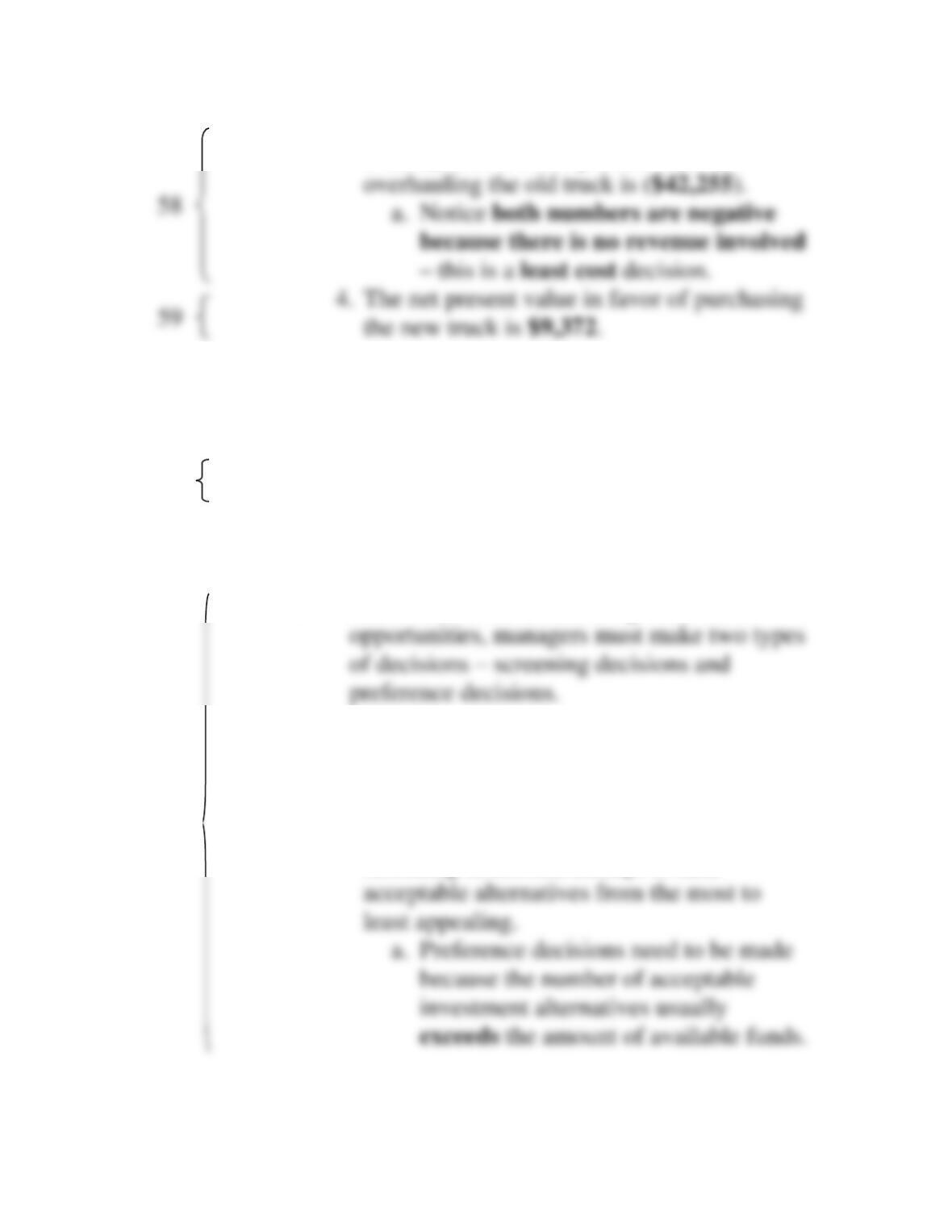

13

3. The net present value of buying a new truck

is ($32,883). The net present value of

V. Preference decisions – the ranking of investment

projects

Learning Objective 11-3: Rank investment projects in

order of preference.

A. Background

i. Recall that when considering investment

1. Screening decisions, which come first,

pertain to whether or not some proposed

investment is acceptable.

2. Preference decisions, which come after

screening decisions, attempt to rank

61

60

58

59

Chapter 11 Capital Budgeting Decisions

14

B. Net present value method

i. The net present value of one project cannot

ii. In the case of unequal investments, a project

profitability index can be computed as

shown. Notice:

1. The project profitability indexes for

investments A and B are 0.01 and 0.20,

respectively.

Chapter 11 Capital Budgeting Decisions

15

VI. The simple rate of return method

Learning Objective 11-4: Compute the simple rate of

return for an investment.

i. Key concepts

1. The simple rate of return method (also

known as the accounting rate of return or

of return is as shown.

ii. The Daily Grind – an example

1. Assume the management of the Daily Grind

wants to install an espresso bar in its

restaurant.

a. The cost of the espresso bar is

iii. Criticisms of the simple rate of return

1. It does not consider the time value of

money.

68

64

Chapter 11 Capital Budgeting Decisions

16

2. The simple rate of return fluctuates from

year to year when used to evaluate projects

iv. The behavioral implications of the simple

rate of return

1. When investment center managers are

VII. Postaudit of investment projects

A. A postaudit is a follow-up after the project has been

completed to see whether or not expected results were

actually realized.

i. The data used in a postaudit analysis should