3-643

3-644

176.

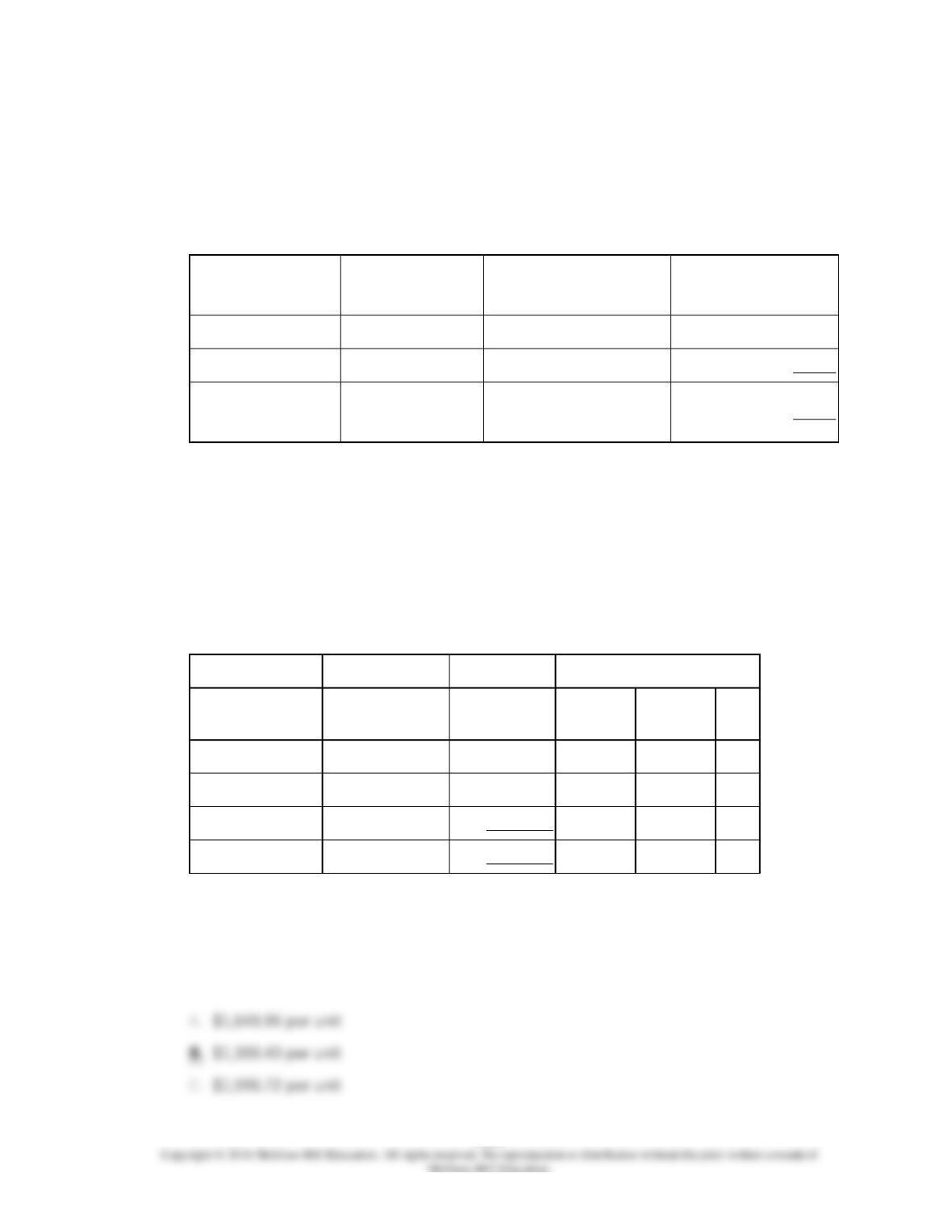

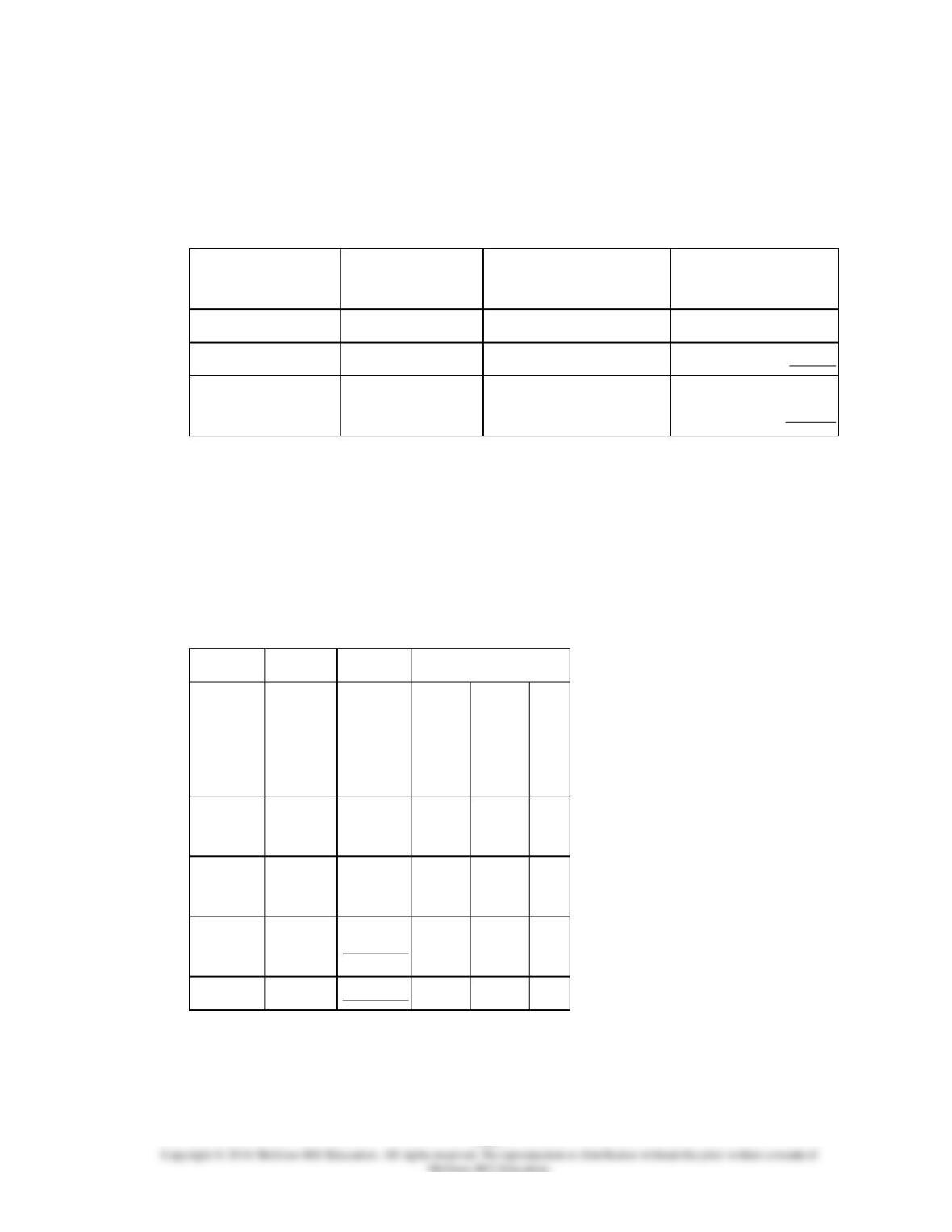

Betenbaugh, Inc., manufactures and sells two products: Product E4 and Product L8. Data

concerning the expected production of each product and the expected total direct labor-

hours (DLHs) required to produce that output appear below:

Expected

Production

Direct Labor-Hours Per

Unit

Total Direct Labor-

Hours

Product E4

100

7.0

700

Product L8

400

6.0

2,400

Total direct labor-

hours

3,100

The direct labor rate is $29.00 per DLH. The direct materials cost per unit is $223.90 for

Product E4 and $122.30 for Product L8

.

The company is considering adopting an activity-based costing system with the following

activity cost pools, activity measures, and expected activity:

Estimated

Expected Activity

Activity Cost Pools

Activity Measures

Overhead Cost

Product E4

Product L8

Total

Labor-related

DLHs

$73,005

700

2,400

3,100

Production orders

orders

42,924

500

700

1,200

General factory

MHs

709,050

4,300

4,400

8,700

$824,979

The overhead applied to each unit of Product L8 under activity-based costing is closest

to:

3-645

3-646

177.

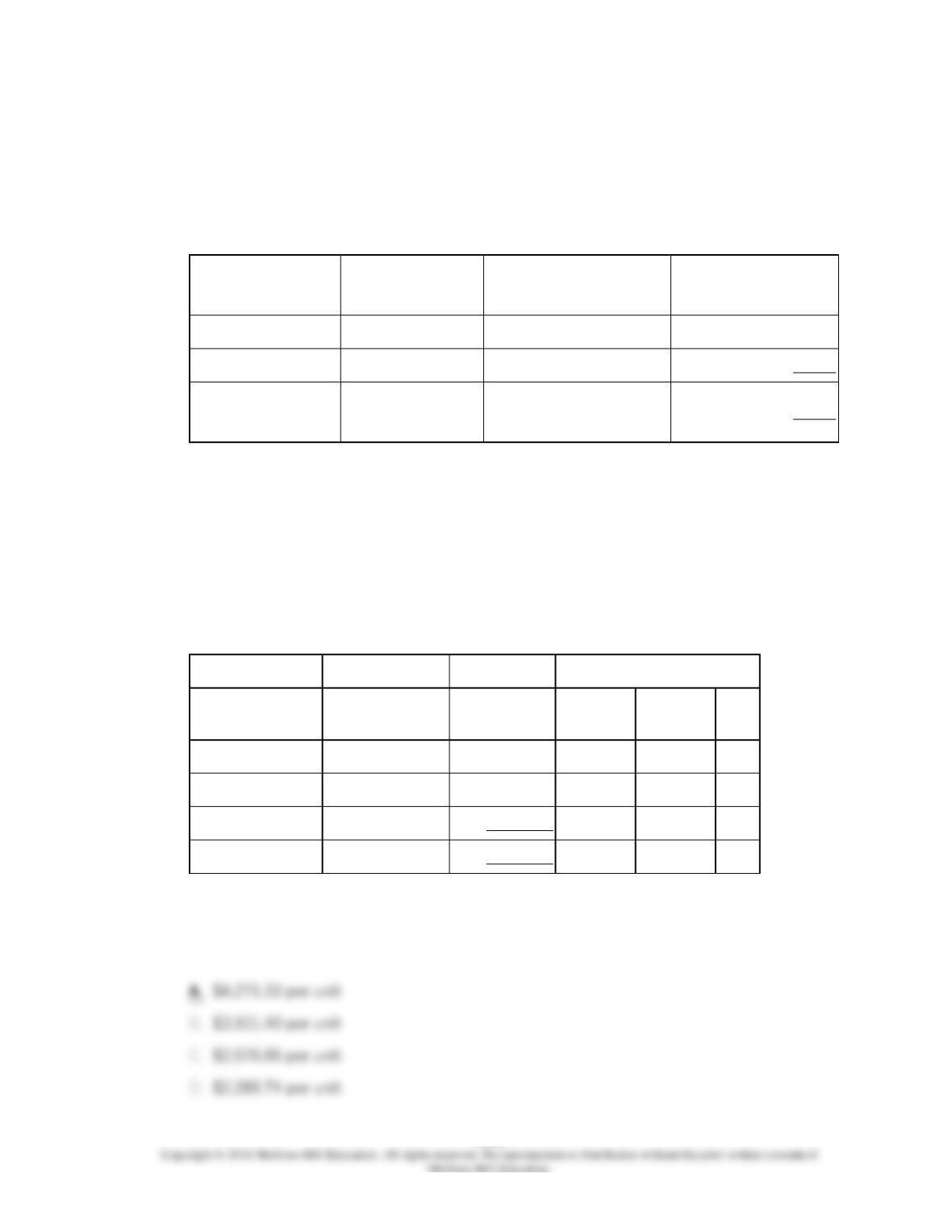

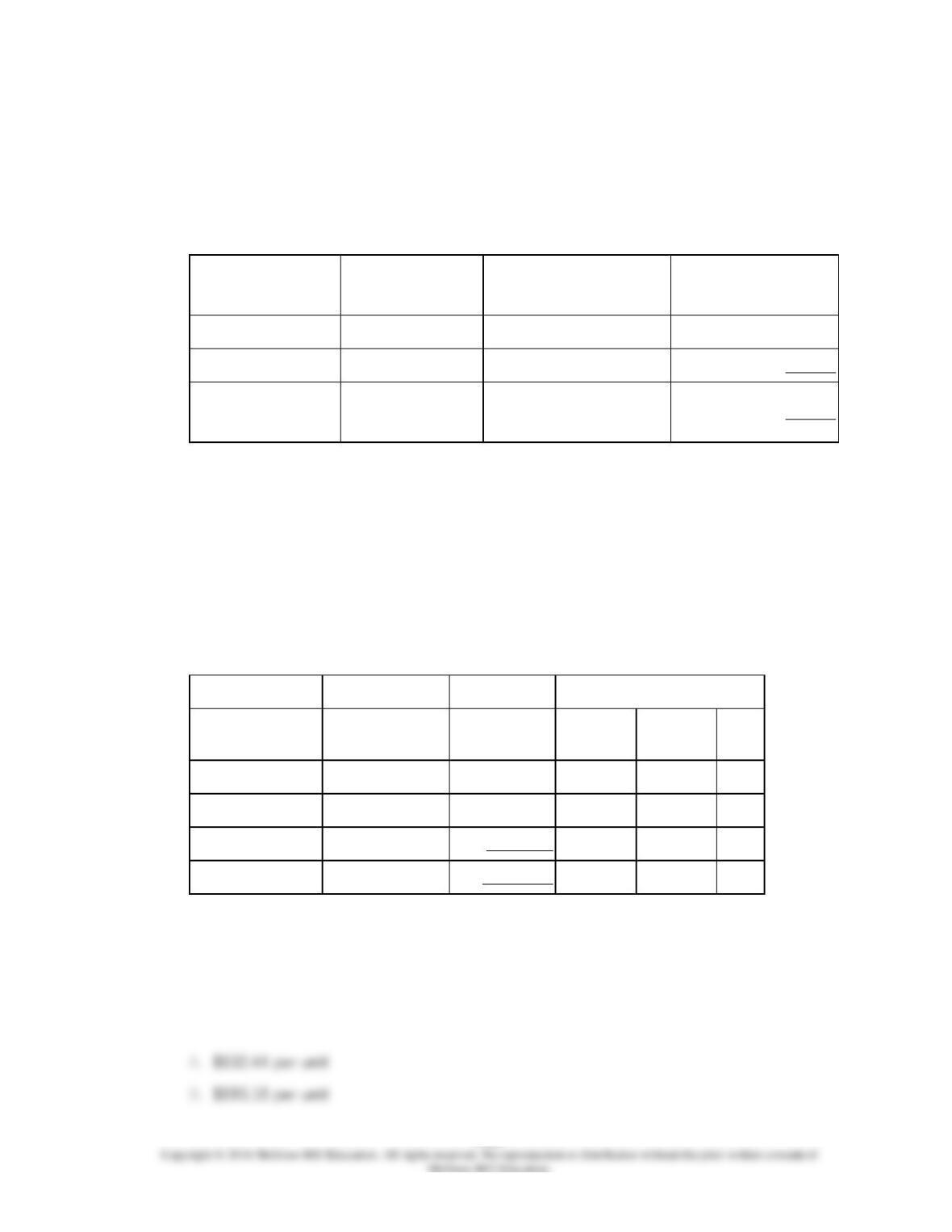

Betenbaugh, Inc., manufactures and sells two products: Product E4 and Product L8. Data

concerning the expected production of each product and the expected total direct labor-

hours (DLHs) required to produce that output appear below:

Expected

Production

Direct Labor-Hours Per

Unit

Total Direct Labor-

Hours

Product E4

100

7.0

700

Product L8

400

6.0

2,400

Total direct labor-

hours

3,100

The direct labor rate is $29.00 per DLH. The direct materials cost per unit is $223.90 for

Product E4 and $122.30 for Product L8

.

The company is considering adopting an activity-based costing system with the following

activity cost pools, activity measures, and expected activity:

Estimated

Expected Activity

Activity Cost Pools

Activity Measures

Overhead Cost

Product E4

Product L8

Total

Labor-related

DLHs

$73,005

700

2,400

3,100

Production orders

orders

42,924

500

700

1,200

General factory

MHs

709,050

4,300

4,400

8,700

$824,979

The unit product cost of Product E4 under activity-based costing is closest to:

3-647

3-648

3-649

178.

Swimm Company allocates materials handling cost to the company’s two products using

the below data:

Modular Homes

Prefab Barns

Total expected units produced

3,000

4,000

Total expected material moves

400

100

Expected direct labor-hours per unit

700

200

The total materials handling cost for the year is expected to be $72,065.

If the materials handling cost is allocated on the basis of direct labor-hours, the total

materials handling cost allocated to the prefab barns is closest to:

179.

Swimm Company allocates materials handling cost to the company’s two products using

the below data:

Modular Homes

Prefab Barns

Total expected units produced

3,000

4,000

Total expected material moves

400

100

Expected direct labor-hours per unit

700

200

The total materials handling cost for the year is expected to be $72,065.

If the materials handling cost is allocated on the basis of material moves, the total

materials handling cost allocated to the modular homes is closest to:

3-651

3-652

180.

Sampaga, Inc., manufactures and sells two products: Product S6 and Product U3. Data

concerning the expected production of each product and the expected total direct labor-

hours (DLHs) required to produce that output appear below:

Expected

Production

Direct Labor-Hours Per

Unit

Total Direct Labor-

Hours

Product S6

200

8.0

1,600

Product U3

900

9.0

8,100

Total direct labor-

hours

9,700

The direct labor rate is $20.90 per DLH. The direct materials cost per unit is $145.30 for

Product S6 and $221.50 for Product U3

.

The company is considering adopting an activity-based costing system with the following

activity cost pools, activity measures, and expected activity:

Estimated

Expected Activity

Activity Cost Pools

Activity Measures

Overhead Cost

Product S6

Product U3

Total

Labor-related

DLHs

$251,230

1,600

8,100

9,700

Production orders

orders

98,150

400

600

1,000

General factory

MHs

171,044

3,200

2,900

6,100

$520,424

If the company allocates all of its overhead based on direct labor-hours using its

traditional costing method, the overhead assigned to each unit of Product U3 would be

closest to:

3-653

3-654

181.

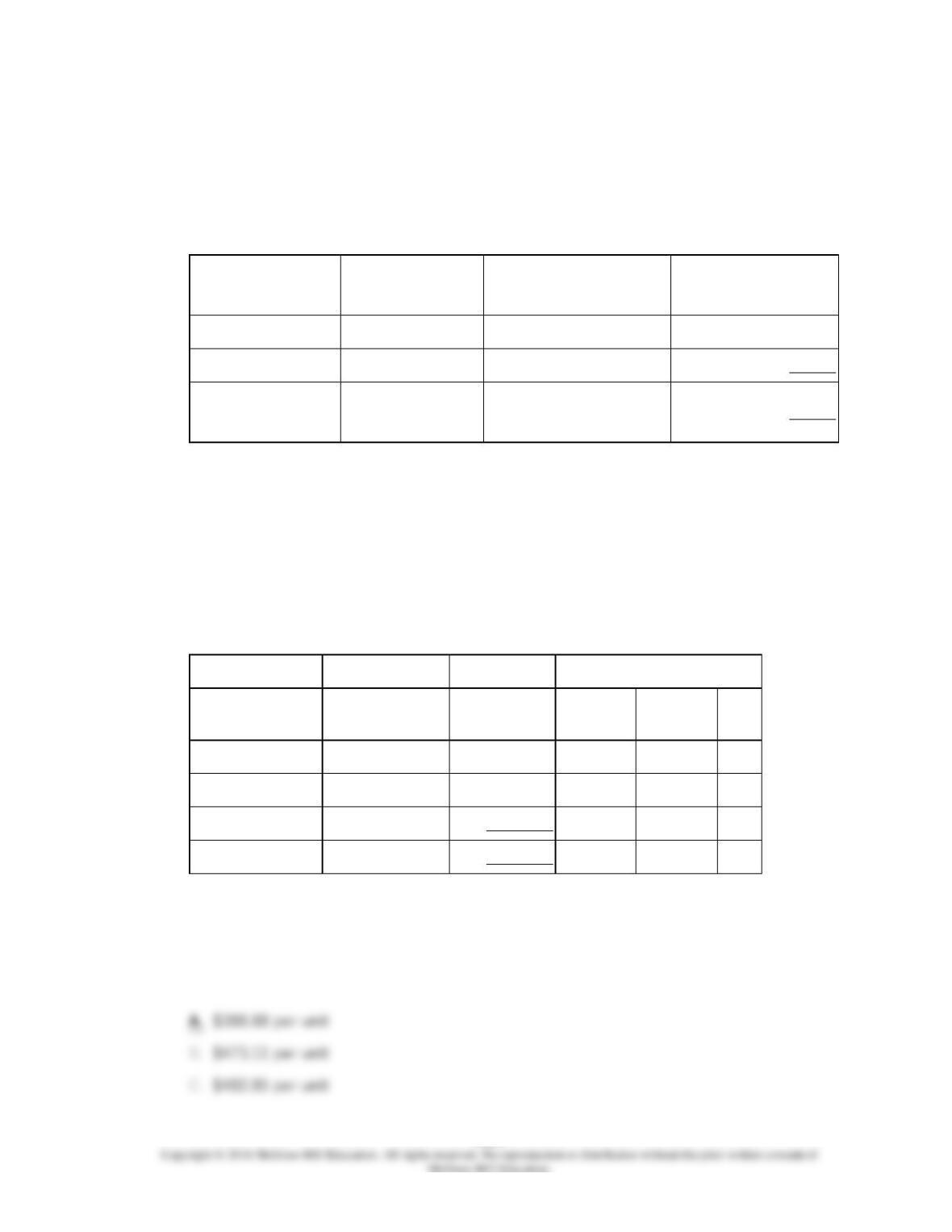

Sampaga, Inc., manufactures and sells two products: Product S6 and Product U3. Data

concerning the expected production of each product and the expected total direct labor-

hours (DLHs) required to produce that output appear below:

Expected

Production

Direct Labor-Hours Per

Unit

Total Direct Labor-

Hours

Product S6

200

8.0

1,600

Product U3

900

9.0

8,100

Total direct labor-

hours

9,700

The direct labor rate is $20.90 per DLH. The direct materials cost per unit is $145.30 for

Product S6 and $221.50 for Product U3

.

The company is considering adopting an activity-based costing system with the following

activity cost pools, activity measures, and expected activity:

Estimated

Expected Activity

Activity Cost Pools

Activity Measures

Overhead Cost

Product S6

Product U3

Total

Labor-related

DLHs

$251,230

1,600

8,100

9,700

Production orders

orders

98,150

400

600

1,000

General factory

MHs

171,044

3,200

2,900

6,100

$520,424

The overhead applied to each unit of Product U3 under activity-based costing is closest

to:

3-655

3-656

3-657

182.

Sampaga, Inc., manufactures and sells two products: Product S6 and Product U3. Data

concerning the expected production of each product and the expected total direct labor-

hours (DLHs) required to produce that output appear below:

Expected

Production

Direct Labor-Hours Per

Unit

Total Direct Labor-

Hours

Product S6

200

8.0

1,600

Product U3

900

9.0

8,100

Total direct labor-

hours

9,700

The direct labor rate is $20.90 per DLH. The direct materials cost per unit is $145.30 for

Product S6 and $221.50 for Product U3

.

The company is considering adopting an activity-based costing system with the following

activity cost pools, activity measures, and expected activity:

Expected Activity

Activity

Cost

Pools

Activity

Measures

Estimated

Overhead

Cost

Product

S6

Product

U3

Total

Labor-

related

DLHs

$251,230

1,600

8,100

9,700

Production

orders

orders

98,150

400

600

1,000

General

factory

MHs

171,044

3,200

2,900

6,100

$520,424

Which of the following statements concerning the unit product cost of Product U3 is

true?

3-658

3-660

3-661

183.

Mellencamp, Inc., manufactures and sells two products: Product A3 and Product Y6. Data

concerning the expected production of each product and the expected total direct labor-

hours (DLHs) required to produce that output appear below:

Expected

Production

Direct Labor-Hours Per

Unit

Total Direct Labor-

Hours

Product A3

900

8.0

7,200

Product Y6

800

10.0

8,000

Total direct labor-

hours

15,200

The direct labor rate is $24.20 per DLH. The direct materials cost per unit is $146.60 for

Product A3 and $256.20 for Product Y6

.

The company is considering adopting an activity-based costing system with the following

activity cost pools, activity measures, and expected activity:

Estimated

Expected Activity

Activity Cost Pools

Activity Measures

Overhead Cost

Product A3

Product Y6

Total

Labor-related

DLHs

$670,624

7,200

8,000

15,200

Production orders

orders

41,545

400

300

700

General factory

MHs

281,281

3,800

3,900

7,700

$993,450

The unit product cost of Product A3 under the company’s traditional costing method in

which all overhead is allocated on the basis of direct labor-hours is closest to:

3-662